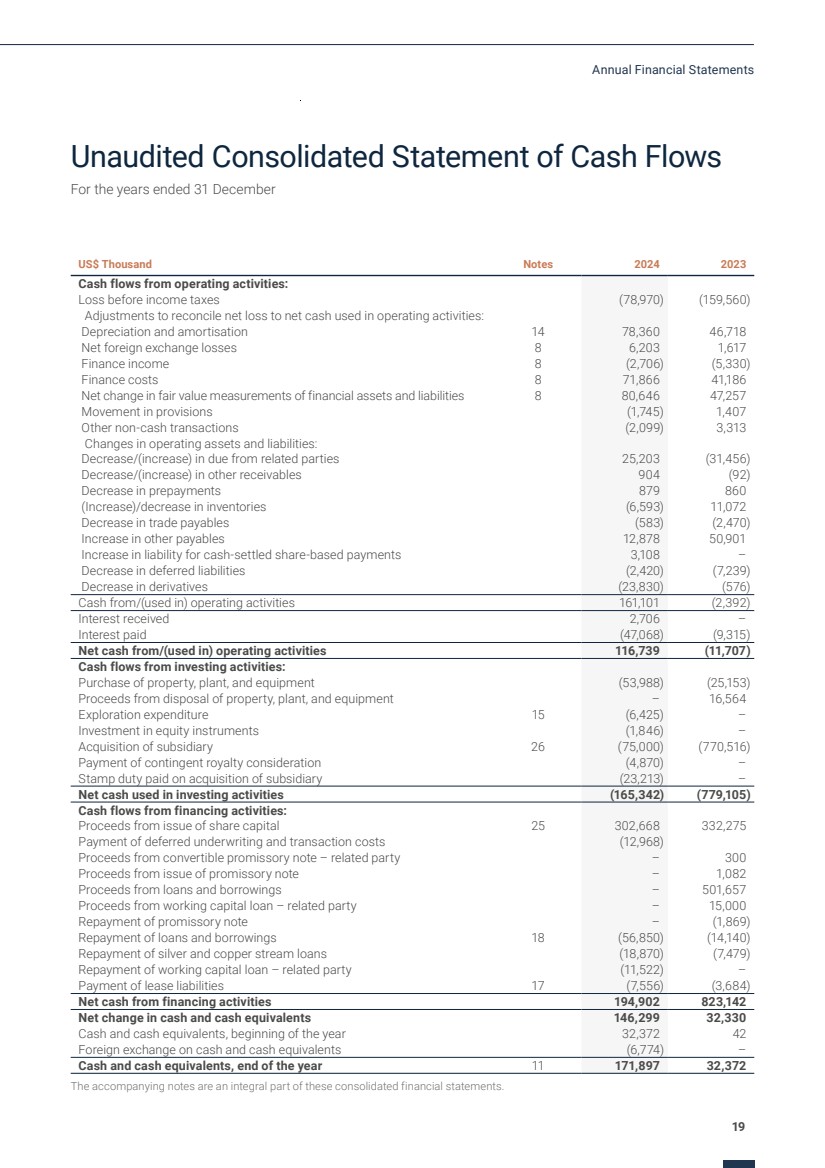

| Unaudited Consolidated Statement of Cash Flows

For the years ended 31 December

US$ Thousand Notes 2024 2023

Cash flows from operating activities:

Loss before income taxes (78,970) (159,560)

Adjustments to reconcile net loss to net cash used in operating activities:

Depreciation and amortisation 14 78,360 46,718

Net foreign exchange losses 8 6,203 1,617

Finance income 8 (2,706) (5,330)

Finance costs 8 71,866 41,186

Net change in fair value measurements of financial assets and liabilities 8 80,646 47,257

Movement in provisions (1,745) 1,407

Other non-cash transactions (2,099) 3,313

Changes in operating assets and liabilities:

Decrease/(increase) in due from related parties 25,203 (31,456)

Decrease/(increase) in other receivables 904 (92)

Decrease in prepayments 879 860

(Increase)/decrease in inventories (6,593) 11,072

Decrease in trade payables (583) (2,470)

Increase in other payables 12,878 50,901

Increase in liability for cash-settled share-based payments 3,108 –

Decrease in deferred liabilities (2,420) (7,239)

Decrease in derivatives (23,830) (576)

Cash from/(used in) operating activities 161,101 (2,392)

Interest received 2,706 –

Interest paid (47,068) (9,315)

Net cash from/(used in) operating activities 116,739 (11,707)

Cash flows from investing activities:

Purchase of property, plant, and equipment (53,988) (25,153)

Proceeds from disposal of property, plant, and equipment – 16,564

Exploration expenditure 15 (6,425) –

Investment in equity instruments (1,846) –

Acquisition of subsidiary 26 (75,000) (770,516)

Payment of contingent royalty consideration (4,870) –

Stamp duty paid on acquisition of subsidiary (23,213) –

Net cash used in investing activities (165,342) (779,105)

Cash flows from financing activities:

Proceeds from issue of share capital 25 302,668 332,275

Payment of deferred underwriting and transaction costs (12,968)

Proceeds from convertible promissory note – related party – 300

Proceeds from issue of promissory note – 1,082

Proceeds from loans and borrowings – 501,657

Proceeds from working capital loan – related party – 15,000

Repayment of promissory note – (1,869)

Repayment of loans and borrowings 18 (56,850) (14,140)

Repayment of silver and copper stream loans (18,870) (7,479)

Repayment of working capital loan – related party (11,522) –

Payment of lease liabilities 17 (7,556) (3,684)

Net cash from financing activities 194,902 823,142

Net change in cash and cash equivalents 146,299 32,330

Cash and cash equivalents, beginning of the year 32,372 42

Foreign exchange on cash and cash equivalents (6,774) –

Cash and cash equivalents, end of the year 11 171,897 32,372

The accompanying notes are an integral part of these consolidated financial statements.

19

Annual Financial Statements |