|

|

|

| Preliminary Pricing Supplement (To the

Prospectus dated July 19, 2013, the Prospectus Addendum dated February 3, 2015 and the Prospectus Supplement dated July 19, 2013) |

|

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-190038 |

The information in this preliminary pricing supplement is not complete and may be changed. This

preliminary pricing supplement and the accompanying prospectus, prospectus supplement and prospectus addendum do not constitute an offer to sell these securities, and we are not soliciting an offer to buy these securities in any state

where the offer or sale is not permitted.

Subject to Completion

Preliminary Pricing Supplement dated February 8, 2016

|

|

|

|

|

|

$[●]

Notes due March 7, 2019

Linked to the EquityCompass Share Buyback Index

Global Medium-Term Notes, Series A |

Terms used in this preliminary pricing supplement, but not defined herein, shall have the meanings ascribed to them in the

prospectus supplement.

|

|

|

| Issuer: |

|

Barclays Bank PLC |

|

|

| Initial Valuation Date: |

|

March 4, 2016 |

|

|

| Issue Date: |

|

March 9, 2016 |

|

|

| Final Valuation Date*: |

|

March 4, 2019 (or, if such date is not a Valuation Date, the next following Valuation Date) |

|

|

| Maturity Date*: |

|

March 7, 2019 |

|

|

| Denominations: |

|

Minimum denomination of $1,000 and integral multiples of $1,000 in excess thereof |

|

|

| Reference Asset: |

|

The EquityCompass Share Buyback Index (the “Index”) (Bloomberg ticker symbol “EQCOMPBB <Index>”). For information about the Index, see “Description of the Index” below. |

|

|

| Index Sponsor: |

|

The Index was created by Barclays Bank PLC, which is the owner of the intellectual property and licensing rights relating to the Index (in such capacity, the “index owner”). The Index is maintained and calculated by

Barclays Risk Analytics and Index Solutions Limited (the “index sponsor”), a wholly-owned subsidiary of Barclays Bank PLC. |

|

|

| Index Selection Agent: |

|

Choice Financial Partners, Inc., a wholly-owned subsidiary and affiliated SEC-registered investment adviser of Stifel Financial Corp. and an

affiliate of Stifel, Nicolaus & Company, Incorporated. One or more affiliates of

the Index Selection Agent may act as a dealer in the offering of the Notes and may receive a selling commission for its or their services as a dealer. In addition, the Index Selection Agent or any of its affiliates that act as a dealer in the

offering of the Notes may also be paid all or a portion of the investor fee on your Notes, as described under “Investor Fee Percentage” below. |

|

|

| Participation Rate: |

|

97.50% |

|

|

| Payment at Maturity: |

|

If your Notes are not called or early redeemed pursuant to the “Automatic Call” provisions or the “Issuer Redemption”

provisions described below prior to maturity, for each $1,000 principal amount Note you hold, you will receive (subject to our credit risk) on the Maturity Date a cash payment equal to (i) the Participation Rate times (ii) the greater of:

(a) $0 and

(b) the sum of (i) $1,000

plus (ii) $1,000 multiplied by the Indicative Note Return as of the Final Valuation Date.

You may lose up to 100% of the principal amount of your Notes. Any payment on the Notes, including any payment at maturity or upon early redemption or

repurchase, is not guaranteed by any third party and is subject to both the creditworthiness of the Issuer and to the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. If Barclays Bank PLC were to default on its payment

obligations or become subject to the exercise of any U.K. Bail-in Power (or any other resolution measure) by the relevant U.K. resolution authority, you might not receive any amounts owed to you under the Notes. See “Consent to U.K. Bail-in

Power” and “Selected Risk Considerations” in this preliminary pricing supplement and “Risk Factors” in the accompanying prospectus addendum for more information. |

|

|

| Consent to U.K. Bail-in Power: |

|

By acquiring the Notes, you acknowledge, agree to be bound by, and consent to the exercise of, any U.K. Bail-in Power. See “Consent to U.K. Bail-in Power” on page PPS-5 of this preliminary pricing

supplement. |

[Terms of the Notes Continue on the Next Page]

|

|

|

|

|

|

|

|

|

| |

|

Initial Issue

Price(1)(2) |

|

Price to Public |

|

Agent’s Commission(3) |

|

Proceeds to Barclays Bank PLC |

| Per Note |

|

$1,000 |

|

100% |

|

2.50% |

|

97.50% |

| Total |

|

$[●] |

|

$[●] |

|

$[●] |

|

$[●] |

| (1) |

Because dealers who purchase the Notes for sale to certain fee-based advisory accounts may forego some or all selling concessions, fees or commissions, the public offering price for investors purchasing the Notes in

such fee-based advisory accounts may be between $975.00 and $1,000 per Note. Investors that hold their Notes in fee-based advisory or trust accounts may be charged fees by the investment advisor or manager of such account based on the amount of

assets held in those accounts, including the Notes. |

| (2) |

If we were to price the Notes for initial sale to the public as of the date of this preliminary pricing supplement, our estimated value of the Notes at the time of such initial pricing would be $975.00 per Note. Our

estimated value is expected to be less than the initial issue price of the Notes. |

| (3) |

Barclays Capital Inc. will receive commissions from the Issuer of up 2.50% of the principal amount of the Notes, or $25.00 per $1,000 principal amount. Barclays Capital Inc. will use these commissions to pay selling

concessions or fees (including custodial or clearing fees) to other dealers. Dealers participating in the offering and receiving such commissions may include affiliates of the Index Selection Agent. See “Investor Fee Percentage” below and

“Selected Risk Considerations” in this preliminary pricing supplement for additional information. |

Investing in the Notes

involves a number of risks. See “Risk Factors” beginning on page S-6 of the prospectus supplement and on page PA-1 of the prospectus addendum and “Selected Risk Considerations” beginning on page PPS-12

of this preliminary pricing supplement.

The Notes will not be listed on any U.S. securities exchange or quotation system. Neither the Securities

and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined that this preliminary pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The Notes constitute our direct, unconditional, unsecured and unsubordinated obligations and are not deposit liabilities of Barclays Bank PLC and

are not insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency of the United States, the United Kingdom or any other jurisdiction.

Terms of the Notes, Continued

|

|

|

| Indicative Note Return: |

|

The Indicative Note Return as of any Valuation Date is the percentage change of the Closing Indicative Note Value per $1,000 principal amount

Note from the Initial Closing Indicative Note Value on the Initial Valuation Date to the Closing Indicative Note Value per $1,000 principal amount Note on such Valuation Date (the “Current Closing Indicative Note Value” or “Current

CINV”), calculated by the Calculation Agent on a formula basis as follows:

Current CINV – Initial CINV

Initial CINV |

|

|

| Closing Indicative Note Value: |

|

The Closing Indicative Note Value (or “CINV”) per $1,000 principal amount Note on the Initial Valuation Date will be deemed to be

100% of the principal amount per Note, or $1,000.00 (the “Initial CINV”) The

CINV per $1,000 principal amount Note on any subsequent Valuation Date until maturity or early redemption will equal (a) the CINV per $1,000 principal amount Note on the Note Rebalancing Date immediately preceding such Valuation Date (or the Initial

Closing Indicative Note Value if such Valuation Date occurs prior to the first Note Rebalancing Date), multiplied by (b) one plus the Net Index Periodic Return as of such Valuation Date, calculated by the Calculation Agent on a formula

basis as follows:

CINVt = CINVr × [1 + Net

Index Periodic Return t]

Where:

“CINVt” means the CINV per $1,000 principal amount Note on Valuation Date “t”;

“CINVr” means the CINV

per $1,000 principal amount Note on the Note Rebalancing Date immediately preceding Valuation Date “t” (or the Initial CINV if such Valuation Date occurs prior to the first Note Rebalancing Date); and

“Net Index Periodic Return

t” means the Net Index Periodic Return (as defined below) as of Valuation Date “t” |

|

|

| Net Index Periodic Return: |

|

The Net Index Periodic Return as of any Valuation Date will equal (a) the Index Periodic Return as of such Valuation Date, minus (b) the applicable Investor Fee Percentage as of such Valuation Date |

|

|

| Index Periodic Return: |

|

The Index Periodic Return as of any Valuation Date will equal the performance of the Index from the Index Closing Level on the Note

Rebalancing Date immediately preceding such Valuation Date (or the Initial Index Level if such Valuation Date occurs prior to the first Note Rebalancing Date) to the Index Closing Level on such Valuation Date, calculated by the Calculation Agent on

a formula basis as follows: Index Closing Level t – Index Closing Level r

Index Closing Level r

Where:

“Index Closing Level t” means the Index Closing Level on Valuation Date

“t”; and “Index Closing Level r” means the Index Closing Level on

the Note Rebalancing Date immediately preceding Valuation Date “t” (or the Initial Index Level if such Valuation Date occurs prior to the first Note Rebalancing Date) |

|

|

| Investor Fee Percentage:** |

|

The applicable Investor Fee Percentage as of the Initial Valuation Date is zero

The applicable Investor Fee Percentage as of any subsequent Valuation Date will equal

(a) 0.90% multiplied by (b) the number of calendar days from (but excluding) the Note Rebalancing Date immediately preceding such Valuation Date (or, if such Valuation Date occurs prior to the first Note Rebalancing Date, the

Initial Valuation Date) to (and including) such Valuation Date, divided by (c) 365, calculated by the Calculation Agent on a formula basis as follows:

0.90% × Number of Days (r, t)

365

Where:

“Number of Days (r, t)” means, with respect to Valuation Date “t”, the number of

calendar days from (but excluding) the Note Rebalancing Date immediately preceding Valuation Date “t” (or, if such Valuation Date occurs prior to the first Note Rebalancing Date, the Initial Valuation Date) to (and including) Valuation

Date “t” The Investor Fee Percentage reduces the amount of your return at

maturity or upon early redemption as described above. All or a portion of the investor fee may be used to pay fees or concessions to the Agent and other dealers. All or a portion of such investor fee may also be paid to the Index Selection Agent as

compensation for the Index Selection Agent’s services under the Index Selection Agreement. |

|

|

| Initial Index Level: |

|

[●], the Index Closing Level on the Initial Valuation Date |

|

|

| Index Closing Level: |

|

With respect to the Index, the official closing level of the Index published at the regular weekday close of trading on the relevant

valuation date as displayed on Bloomberg Professional® service page “EQCOMPBB <Index>” or any successor page on Bloomberg Professional® service or any successor service, as applicable

In certain circumstances, the closing level of the Index will be based on the alternate calculation of the Index as described under “Reference

Assets—Indices—Adjustments Relating to Securities with the Reference Asset Comprised of an Index or Indices” in the accompanying prospectus supplement |

|

|

| Note Rebalancing Dates: |

|

The sixth calendar day of each calendar month during the term of the Notes (or if such day is not a Valuation Date, the next following Valuation Date); provided that the first scheduled Note Rebalancing Date will be April 6,

2016. |

PPS–2

|

|

|

|

|

| Automatic Call: |

|

If the Closing Indicative Note Value per $1,000 principal amount Note on any Valuation Date prior to the Final Valuation Date is equal to or

less than $250.00 (such event, an “Automatic Call Trigger Event” and such Valuation Date, the “Automatic Call Trigger Date”), the Notes will be automatically called on the applicable Automatic Call Date; provided, however, that

if a Market Disruption Event occurs with respect to the Index on a Valuation Date, the Closing Indicative Note Value per $1,000 principal amount Note on such Valuation Date will be disregarded for purposes of determining whether an Automatic Call

Trigger Event occurs For a description of Market Disruption Events that are applicable

to the Index, please see “Reference Assets—Indices—Market Disruption Events for Securities with the Reference Asset Comprised of an Index or Indices of Equity Securities” in the accompanying prospectus supplement

If an Automatic Call Trigger Event occurs, the Notes will be automatically called on the

applicable Automatic Call Date and you will receive (subject to our credit risk) on the Automatic Call Date a cash payment per $1,000 principal amount Note equal to the Automatic Call Amount calculated by the Calculation Agent on the Automatic Call

Amount Calculation Date. We will deliver a notice to The Depository Trust Company (the “Automatic Call Notice”) in the form attached as Annex A hereto that specifies the Automatic Call Trigger Date, the Automatic Call Amount Calculation

Date and the Automatic Call Date |

|

|

Automatic Call Amount

Calculation Date:* |

|

With respect to an Automatic Call Trigger Date, the Automatic Call Amount Calculation Date will be the Valuation Date immediately following

the Automatic Call Trigger Date For a description of Market Disruption Events that are

applicable to the Index, please see “Reference Assets—Indices—Market Disruption Events for Securities with the Reference Asset Comprised of an Index or Indices of Equity Securities” in the accompanying prospectus

supplement. |

|

|

| Automatic Call Amount: |

|

With respect to an Automatic Call Date, for each $1,000 principal amount Note, a cash payment equal to (i) the Participation Rate times

(ii) the greater of: (a) $0 and

(b) the sum of (i) $1,000 plus (ii) $1,000 multiplied by the Indicative Note

Return as of the Automatic Call Amount Calculation Date |

|

|

| Automatic Call Date: |

|

The fifth Business Day following the applicable Automatic Call Amount Calculation Date, as set forth in the applicable Automatic Call Notice |

|

|

| Issuer Redemption: |

|

If the index sponsor determines on or prior to the Final Valuation Date that it will not be able to calculate and publish the Index as a result of the occurrence of any of the Termination Events as described under “Description

of the Index” in this preliminary pricing supplement, the Issuer may redeem the Notes, in whole but not in part, on the applicable Issuer Redemption Date at the applicable Issuer Redemption Price, provided the Issuer gives at least three (3)

business days’ prior written notice (the “Issuer Redemption Notice”) to The Depository Trust Company in the form attached as Annex B hereto that specifies the date on which the relevant Termination Event occurs, the Issuer Redemption

Price Calculation Date and the Issuer Redemption Date |

|

|

Issuer Redemption Price

Calculation Date:* |

|

The Valuation Date immediately following the date on which the relevant Termination Event occurs, as set forth in the applicable Issuer

Redemption Notice For a description of Market Disruption Events that are applicable to

the Index, please see “Reference Assets—Indices—Market Disruption Events for Securities with the Reference Asset Comprised of an Index or Indices of Equity Securities” in the accompanying prospectus supplement |

|

|

| Issuer Redemption Price: |

|

If a Termination Event occurs and the Issuer exercises its option to redeem the Notes pursuant to the “Issuer Redemption”

provisions above, you will receive (subject to our credit risk) on the applicable Issuer Redemption Date a cash payment per $1,000 principal amount Note equal to (i) the Participation Rate times (ii) the greater of:

(a) $0 and

(b) the sum of (i) $1,000 plus (ii) $1,000 multiplied by the Indicative Note Return as of the Issuer Redemption Price Calculation

Date |

|

|

| Issuer Redemption Date: |

|

The fifth Business Day following the applicable Issuer Redemption Price Calculation Date, as set forth in the applicable Issuer Redemption Notice |

|

|

Early Redemption at the Option of

Holders: |

|

Subject to the notification requirements described in this preliminary pricing supplement and the minimum redemption amount of at least 10

Notes (or a minimum redemption amount of at least $10,000 principal amount of Notes), you may elect to redeem your Notes prior to maturity, and you will receive the Optional Redemption Amount (calculated on the applicable Optional Redemption Amount

Calculation Date) on the applicable Optional Redemption Date For more information

relating to the procedures that you must follow in order to require Barclays Bank PLC to redeem your Notes prior to maturity, please see “Early Optional Holder Redemption Procedures” in this preliminary pricing supplement |

|

|

| Optional Redemption Amount: |

|

In the event that you deliver an effective notice of early redemption for your Notes, as described under “Early Optional Holder

Redemption Procedures” in this preliminary pricing supplement, you will receive (subject to our credit risk) on the applicable Optional Redemption Date a cash payment per $1,000 principal amount Note equal to (i) the Participation Rate

times (ii) the greater of:

(a) $0 and

(b) the sum of (i) $1,000 plus (ii) $1,000 multiplied by the Indicative Note

Return as of the Optional Redemption Amount Calculation Date |

PPS–3

|

|

|

|

|

Optional Redemption Amount

Calculation Date:* |

|

The date on which the notice of early redemption at the option of a holder of the Notes becomes effective, as described in this preliminary pricing supplement under “Early Optional Holder Redemption Procedures” (or, if

such date is not a Valuation Date, the next following Valuation Date) |

|

|

| Optional Redemption Date: |

|

The fifth business day following an Optional Redemption Amount Calculation Date. The final date on which an Optional Redemption Amount Calculation Date may occur is the fifth business day following the Valuation Date that is

immediately prior to the Final Valuation Date. |

|

|

| Valuation Date: |

|

A day on which (a) the value of the Index is published, and (b) trading is generally conducted on the markets on which the securities comprising the Index are traded, in each case as determined by the Calculation Agent in its sole

discretion |

|

|

| Business Days: |

|

New York and London |

|

|

| Calculation Agent: |

|

Barclays Bank PLC |

|

|

| CUSIP/ISIN: |

|

06741U5E0 / US06741U5E01 |

| * |

Subject to postponement in the event of a Market Disruption Event, as described under “Purchase Considerations—Market Disruption Events and Adjustments” in this preliminary pricing supplement.

|

| ** |

All or a portion of the investor fee as described under “Investor Fee Percentage” in this preliminary pricing supplement may be used to pay fees or concessions to the Agent and other dealers. All or a

portion of such investor fee may also be paid to the Index Selection Agent as compensation for the services provided by the Index Selection Agent under the Index Selection Agreement. |

PPS–4

You may revoke your offer to purchase the Notes at any time prior to the initial valuation date as described

on the cover of this preliminary pricing supplement. We reserve the right to change the terms of, or reject any offer to purchase the Notes prior to their issuance. In the event of any changes to the terms of the Notes, we will notify you and you

will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

ADDITIONAL DOCUMENTS RELATED TO THE OFFERING OF THE NOTES

You should read this preliminary pricing supplement together with the prospectus dated July 19, 2013, as supplemented by the prospectus supplement dated

July 19, 2013 and prospectus addendum dated February 3, 2015 relating to our Global Medium-Term Notes, Series A, of which these Notes are a part. This preliminary pricing supplement, together with the documents listed below, contains the

terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures,

brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the prospectus supplement and the prospectus addendum, as the Notes involve risks not

associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on

the SEC website):

| |

• |

|

Prospectus dated July

19, 2013: |

http://www.sec.gov/Archives/edgar/data/312070/000119312513295636/d570220df3asr.htm

| |

• |

|

Prospectus Supplement dated July

19, 2013: |

http://www.sec.gov/Archives/edgar/data/312070/000119312513295715/d570220d424b3.htm

| |

• |

|

Prospectus Addendum dated February

3, 2015: |

http://www.sec.gov/Archives/edgar/data/312070/000119312515031134/d864437d424b3.htm

Our SEC file number is 1-10257. As used in this preliminary pricing supplement, the “Company,” “we,” “us,” or

“our” refers to Barclays Bank PLC.

CONSENT TO U.K. BAIL-IN POWER

Under the U.K. Banking Act 2009, as recently amended, the relevant U.K. resolution authority may exercise a U.K. Bail-in Power under certain conditions which,

in summary, include that such authority determines that: (i) a relevant entity (such as the Issuer) is failing or is likely to fail, (ii) it is not reasonably likely that (ignoring the other stabilization powers under the U.K. Banking Act)

any other action will be taken to avoid the entity’s failure, (iii) the exercise of the stabilization powers are necessary taking into account certain public interest considerations such as the stability of the U.K. financial system,

public confidence in the U.K. banking system and the protection of depositors and (iv) the objectives of the resolution measures would not be met to the same extent by the winding up of the entity. Notwithstanding these conditions, there

remains uncertainty regarding how the relevant U.K. resolution authority would assess these conditions in deciding whether to exercise any U.K. Bail-in Power. The U.K. Bail-in Power includes any statutory write-down and conversion power, which

allows for the cancellation of all, or a portion, of any amounts payable on the Notes, including any repayment of principal and/or the conversion of all, or a portion, of any amounts payable on the Notes, including the repayment of principal, into

shares or other securities or other obligations of ours or another person, including by means of a variation to the terms of the Notes. Accordingly, if any U.K. Bail-in Power is exercised you may lose all or a part of the value of your investment in

the Notes or receive a different security, which may be worth significantly less than the Notes and which may have significantly fewer protections than those typically afforded to debt securities. Moreover, the relevant U.K. resolution authority may

exercise its authority to implement the U.K. Bail-in Power without providing any advance notice to the holders of the Notes.

By your acquisition of

the Notes, you acknowledge, agree to be bound by, and consent to the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority.

This is only a summary. For more information, please see “Selected Risk Considerations—You May Lose Some or All of Your Investment If Any U.K.

Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority” in this preliminary pricing supplement and the full definition of “U.K. Bail-in Power” as well as the risk factors in the accompanying prospectus addendum.

PPS–5

SELECTED PURCHASE CONSIDERATIONS

The Notes are not suitable for all investors. The Notes may be a suitable investment for you if all of the following statements are true:

| |

• |

|

You do not seek an investment that produces periodic interest or coupon payments or other sources of current income |

| |

• |

|

You are willing to accept the risk that you may lose some or all of the principal amount of your Notes |

| |

• |

|

You understand and accept that the level of the Index will depend upon the success of the Strategy and you believe that the Strategy will be successful |

| |

• |

|

You are willing to accept the risks associated with an investment linked to the performance of the Index |

| |

• |

|

You understand and are willing to accept that the daily deduction of the Investor Fee Percentage will reduce the amount of your return at maturity or upon early redemption |

| |

• |

|

You understand and accept that the Participation Rate of 97.50% will limit your participation in any positive performance of the Index and will magnify your participation in any negative performance of the Index

|

| |

• |

|

You are willing to accept the risk that we may redeem the Notes prior to the scheduled maturity following a Termination Event and that, upon such a redemption, the payment that you receive may be significantly less than

the principal amount of your Notes |

| |

• |

|

You are willing to accept the risk that the Notes will be automatically called prior to scheduled maturity following an Automatic Call Trigger Event and that, upon such an event, the payment that receive is highly

likely to be significantly less than the principal amount of your Notes |

| |

• |

|

You are willing to accept the risk that, upon an early redemption or an automatic call, you may not be able to reinvest your money in an alternative investment with comparable risk and yield |

| |

• |

|

You do not seek an investment for which there will be an active secondary market and you are either willing and able to hold the notes to maturity or willing to accept the limitations set forth herein with regard to

your ability to exercise your option to cause us to redeem your Notes prior to scheduled maturity |

| |

• |

|

You are willing to assume our credit risk for all payments on the Notes |

| |

• |

|

You are willing to consent to the exercise of any U.K. Bail-in Power by any relevant U.K. resolution authority |

The Notes may not be a suitable investment for you if any of the following statements are true:

| |

• |

|

You seek an investment that produces periodic interest or coupon payments or other sources of current income |

| |

• |

|

You seek an investment that provides for the full repayment of principal at maturity and you are unwilling to accept the risk that you may lose some or all of the principal amount of your Notes |

| |

• |

|

You do not believe that the Strategy will be successful and/or you are unwilling or unable to accept that the level of the Index will depend upon the success of the Strategy |

| |

• |

|

You are unwilling or unable to accept the risks associated with an investment linked to the performance of the Index |

| |

• |

|

You are not comfortable with the return on your investment being reduced by virtue of the Investor Fee Percentage |

| |

• |

|

You are not comfortable with the effect of the Participation Rate of 97.50% limiting your participation in any positive performance of the Index and magnifying your participation in any negative performance of the Index

|

| |

• |

|

You are unwilling or unable to accept the risk that the Notes may be redeemed or automatically called prior to scheduled maturity and, in either case, that you may suffer a significant loss of principal

|

| |

• |

|

You seek an investment for which there will be an active secondary market |

| |

• |

|

You are unable or unwilling to hold the Notes to maturity and/or you are not comfortable with the limitations regarding your ability to exercise your option to redeem your Notes prior to scheduled maturity

|

| |

• |

|

You are unwilling or unable to assume our credit risk for all payments on the Notes |

| |

• |

|

You are unwilling or unable to consent to the exercise of any U.K. Bail-in Power by any relevant U.K. resolution authority |

You must rely on your own evaluation of the merits of an investment in the Notes. You should reach a decision whether to invest in the Notes

after carefully considering, with your advisors, the suitability of the Notes in light of your investment objectives and the specific information set out in this preliminary pricing supplement, the prospectus supplement, the prospectus and the

prospectus addendum. Neither the Issuer nor Barclays Capital Inc. nor any dealer participating in the offering makes any recommendation as to the suitability of the Notes for investment.

PPS–6

ADDITIONAL TERMS OF THE NOTES

| • |

|

Market Disruption Events—In the event of a Market Disruption Event on a day that would otherwise be the Final Valuation Date, Automatic Call Amount Calculation Date, Issuer Redemption Price Calculation Date

or Optional Redemption Amount Calculation Date, as the case may be, the relevant date will be the first following Valuation Date on which no Market Disruption Event occurs or is continuing with respect to the Index. In no event, however, will the

relevant date be postponed by more than five scheduled Valuation Dates. If the Calculation Agent determines that a Market Disruption Event occurs or is continuing on such fifth day, the Calculation Agent will make an estimate of the Index Closing

Level that would have prevailed on that fifth day in the absence of such Market Disruption Event. |

| • |

|

Adjustments to the Index—The Index may be subject to adjustment in various circumstances, as described under “Modifications to the EquityCompass Share Buyback Index” in this preliminary pricing

supplement”. |

Notwithstanding anything to the contrary in the accompanying prospectus supplement, the Final Valuation

Date may be postponed by up to five scheduled Valuation Dates due to the occurrence or continuance of a Market Disruption Event on such date. In such a case, the Maturity Date will be postponed such that the number of business days between the Final

Valuation Date and the Maturity Date remains the same.

PPS–7

HYPOTHETICAL EXAMPLES OF AMOUNTS PAYABLE ON THE NOTES

Calculation of Closing Indicative Note Value per $1,000 Principal Amount Note on a Hypothetical Valuation Date

The following example sets forth the methodology used to calculate the Closing Indicative Note Value per $1,000 principal amount Note on a hypothetical

Valuation Date. The numbers set forth in the following example, which have been rounded for ease of reference, are purely hypothetical and are provided for illustrative purposes only. As shown in the following table, this example

assumes that the Index Closing Level was 113.50 on the hypothetical Valuation Date and 113.00 on the Note Rebalancing Date immediately preceding the hypothetical Valuation Date. The hypothetical calculation of the Investor Fee Percentage in the

example below is the amount of Investor Fee on the hypothetical Valuation Date only. The actual Investor Fee Percentage on any given Valuation Date will be dependent upon the number of calendar days from, but excluding, the immediately prior Note

Rebalancing Date to and including the relevant Valuation Date (or, if the Valuation Date occurs prior to the first Note Rebalancing Date, the number of calendar days from but excluding the Initial Valuation Date to and including the relevant

Valuation Date).

This example of the calculation of the Closing Indicative Note Value per $1,000 principal amount Note on a hypothetical Valuation Date

makes the following key assumptions:

| |

• |

|

Closing Indicative Note Value on Immediately Preceding Note Rebalancing Date: $1,115.00 |

| |

• |

|

Index Closing Level on Immediately Preceding Note Rebalancing Date: 113.00 |

| |

• |

|

Index Closing Level on the Hypothetical Valuation Date: 113.50 |

| |

• |

|

Number of Calendar Days From But Excluding the Immediately Preceding Note Rebalancing Date to and Including the Hypothetical Valuation Date: 30 |

| |

• |

|

The Notes are not called or early redeemed pursuant to the “Automatic Call” or “Issuer Redemption” provisions described elsewhere in this preliminary pricing supplement |

| |

• |

|

The effect of the Investor Fee Percentage has been properly accounted for on each Valuation Date |

| |

• |

|

No Market Disruption Events occurred or were continuing on any Valuation Date |

Step 1: Calculate the Index

Periodic Return as of the Hypothetical Valuation Date

Using the Index Closing Levels on the hypothetical Valuation Date and the Note Rebalancing Date

immediately preceding such Valuation Date, the Index Periodic Return is calculated as follows:

Index Periodic Return =

(113.50 – 113.00) / 113.00, or 0.442%

Step 2: Calculate the Investor Fee Percentage as of the Hypothetical Valuation Date

Using the number of days from, but excluding, the immediately preceding Note Rebalancing Date to and including the hypothetical Valuation Date, the Investor

Fee Percentage is calculated as follows:

Investor Fee Percentage = (0.90% × 30) / 365, or 0.074%

Step 3: Calculate the Net Index Periodic Return as of the Hypothetical Valuation Date

Using the Index Periodic Return and the Investor Fee Percentage calculated as of the relevant Valuation Date, the Net Index Periodic Return is calculated as

follows:

Net Index Periodic Return = 0.442% - 0.074%, or 0.368%

Step 4: Calculate the Closing Indicative Note Value per $1,000 principal amount Note as of the Hypothetical Valuation Date

Using the Closing Indicative Note Value as of the immediately preceding Note Rebalancing Date and the Net Index Periodic Return calculated as of the

hypothetical Valuation Date, the Closing Indicative Note Value per $1,000 principal amount Note on such Valuation Date, or the “Current Closing Indicative Note Value” as of such date, is calculated as follows:

Current CINV = $1,115.00 × [1 + 0.368%], or $1,119.10

PPS–8

Calculation of the Payment at Maturity or on an Optional Redemption Date per $1,000 Principal Amount Note

(Assuming that the Hypothetical Valuation Date in the Examples Above is Either the Final Valuation Date or the Optional Redemption Amount Calculation Date, as Applicable)

Step 1: Calculate the Indicative Note Return as of the Final Valuation Date or the Optional Redemption Amount Calculation Date, As Applicable

Using the Initial CINV of $1,000.00 and the Current CINV calculated in the examples above, the Indicative Note Return as of the Final Valuation Date or the

Optional Redemption Amount Calculation Date, as the case may be, is calculated as follows:

Indicative Note Return =

($1,119.10– $1,000.00) / $1,000.00 = 11.91%

Step 2: Calculate the Payment at Maturity or the Optional Redemption Amount, as Applicable

Step 2a: Using the Indicative Note Return as of the Final Valuation Date or the Optional Redemption Amount Calculation Date, as applicable and as calculated

above, calculate the sum of $1,000 plus $1,000 multiplied by such Indicative Note Return, as follows:

$1,000

+ ($1,000 × 11.91%) = $1,119.10

Step 2b: Because the payment at maturity (or the Optional Redemption Amount, as the case may be) will be equal to

(i) the Participation Rate times (ii) the greater of (a) $0.00 and (b) the amount calculated in Step 2a above, and because the amount calculated in Step 2a above is greater than $0.00, you will receive at maturity or on

the Optional Redemption Date, as the case may be, subject to our credit risk, $1,091.12 per $1,000 principal Note, calculated as follows:

97.50% × $1,119.10 = $1,091.12

PPS–9

Calculation of the Total Return on the Notes at Maturity

The following table illustrates the hypothetical total return at maturity on the Notes. The “total return”, as used in the following examples, is the

number (expressed as a percentage) that results from comparing the payment at maturity per $1,000 principal amount Note to $1,000. The hypothetical total returns set forth below are for illustrative purposes only and may not be the actual total

returns applicable to a purchaser of the Notes. The numbers appearing in the following table and examples have been rounded for ease of analysis. These examples do not take into account any tax consequences from investing in the Notes.

The actual Indicative Note Return on the Final Valuation Date will depend on the path taken by the Index from the Initial Valuation Date to the Final

Valuation Date, and will also depend on the cumulative effect of the Investor Fee Percentage. For examples of how the Investor Fee Percentage and the Indicative Note Return will be calculated on each Valuation Date during the term of the Notes, up

to and including the Final Valuation Date, please see “Calculation of Closing Indicative Note Value per $1,000 Principal Amount Note on a Hypothetical Valuation Date” above.

The examples in the table below make the following key assumptions:

| |

• |

|

Initial CINV: $1,000.00 |

| |

• |

|

The effect of the Investor Fee Percentage has been properly accounted for on each Valuation Date |

| |

• |

|

The Notes are not called or early redeemed pursuant to the “Automatic Call”, “Issuer Redemption” or “Early Redemption at the Option of Holders” provisions described elsewhere in this

preliminary pricing supplement |

|

|

|

|

|

|

|

| Closing Indicative Note

Value on the Final

Valuation Date |

|

Indicative Note

Return |

|

Payment at

Maturity* |

|

Total Return on Notes |

| $1,700.00 |

|

70.00% |

|

$1,657.50 |

|

65.75% |

| $1,600.00 |

|

60.00% |

|

$1,560.00 |

|

56.00% |

| $1,500.00 |

|

50.00% |

|

$1,462.50 |

|

46.25% |

| $1,400.00 |

|

40.00% |

|

$1,365.00 |

|

36.50% |

| $1,300.00 |

|

30.00% |

|

$1,267.50 |

|

26.75% |

| $1,200.00 |

|

20.00% |

|

$1,170.00 |

|

17.00% |

| $1,100.00 |

|

10.00% |

|

$1,072.50 |

|

7.25% |

| $1,025.64 |

|

2.564% |

|

$1,000.00 |

|

0.00% |

| $1,000.00 |

|

0.00% |

|

$975.00 |

|

-2.50% |

| $900.00 |

|

-10.00% |

|

$877.50 |

|

-12.25% |

| $800.00 |

|

-20.00% |

|

$780.00 |

|

-22.00% |

| $700.00 |

|

-30.00% |

|

$682.50 |

|

-31.75% |

| $600.00 |

|

-40.00% |

|

$585.00 |

|

-41.50% |

| $500.00 |

|

-50.00% |

|

$487.50 |

|

-51.25% |

| $400.00 |

|

-60.00% |

|

$390.00 |

|

-61.00% |

| $300.00 |

|

-70.00% |

|

$292.50 |

|

-70.75% |

| * |

Per $1,000 principal amount Note |

The following examples illustrate how the total returns set forth in the

table above are calculated.

Example 1: The Closing Indicative Note Value increases from an Initial Closing Indicative Note Value of $1,000.00 to a

Closing Indicative Note Value on the Final Valuation Date of $1,100.00.

In this case, you will receive a payment at maturity of $1,072.50 per $1,000

principal amount Note that you hold, calculated as follows:

Participation Rate x Greater of (a) $0 or

(b) [$1,000 + ($1,000 × Indicative Note Return as of the Final Valuation Date)]

97.50% × [$1,000 + ($1,000 ×

10.00%)] = $1,072.50

The total return on investment of the Notes is 7.25%

PPS–10

Example 2: The Closing Indicative Note Value decreases from an Initial Closing Indicative Note Value of

$1,000.00 to a Current Closing Indicative Note Value on the Final Valuation Date of $900.00.

In this case, you will receive a payment at maturity of

$877.50 per $1,000 principal amount Note that you hold, calculated as follows:

Participation Rate x Greater of (a) $0

or (b) [$1,000 + ($1,000 × Indicative Note Return as of the Final Valuation Date)]

97.50% x [$1,000 + ($1,000 × -10.00%)]

= $877.50

The total return on investment of the Notes is -12.25%.

Calculation of the Automatic Call Amount Following an Automatic Call Trigger Event

The following examples illustrate possible hypothetical Automatic Call Amounts per $1,000 principal amount Note on a hypothetical Automatic Call Date

following an Automatic Call Trigger Event. We have included a hypothetical example (a) where the Closing Indicative Note Value per $1,000 principal amount Note increases from the Automatic Call Trigger Date to the Automatic Call Amount

Calculation Date and (b) where the Closing Indicative Note Value per $1,000 principal amount Note decreases from the Automatic Call Trigger Date to the Automatic Call Amount Calculation Date. The figures in the following examples have been

rounded for ease of reference and do not take into account any tax consequences from investing in the Notes.

The examples below make the following key

assumptions:

| |

• |

|

The Notes have not been redeemed by us pursuant to the “Issuer Redemption” provisions or by you pursuant to the “Early Redemption at the Option of Holders” provisions described elsewhere in this

preliminary pricing supplement |

| |

• |

|

The effect of the Investor Fee Percentage has been properly accounted for on each Valuation Date |

| |

• |

|

Initial Closing Indicative Note Value: $1,000.00 |

|

|

|

|

|

|

|

|

|

|

|

| Automatic Call Trigger Date |

|

Automatic Call Amount

Calculation Date |

|

Automatic Call Date |

| Closing

Indicative Note

Value |

|

Indicative Note

Return |

|

Closing

Indicative Note

Value |

|

Indicative

Note Return |

|

Automatic Call

Amount* |

|

Return on Notes |

| $200.00 |

|

-80.00% |

|

$230.00 |

|

-77.00% |

|

$224.25 |

|

-77.58% |

| $200.00 |

|

-80.00% |

|

$170.00 |

|

-83.00% |

|

$165.75 |

|

-83.43% |

| * |

Per $1,000 principal amount Note |

Calculation of the Issuer Redemption Price Following a Termination

Event

The following examples illustrate possible hypothetical Issuer Redemption Prices per $1,000 Note on a hypothetical Issuer Redemption Date

following a Termination Event. We have included a hypothetical example (a) where the Closing Indicative Note Value per $1,000 principal amount Note increases from the date on which the Termination Event occurs to the Issuer Redemption Price

Calculation Date and (b) where the Closing Indicative Note Value per $1,000 principal amount Note decreases from the date on which the Termination Event occurs to the Issuer Redemption Price Calculation Date. The figures in the following

examples have been rounded for ease of reference and do not take into account any tax consequences from investing in the Notes.

The examples below make

the following key assumptions:

| |

• |

|

The Notes have not been automatically called by us pursuant to the “Automatic Call” provisions or by you pursuant to the “Early Redemption at the Option of Holders” provisions described elsewhere in

this preliminary pricing supplement |

| |

• |

|

The effect of the Investor Fee Percentage has been properly accounted for on each Valuation Date |

| |

• |

|

Initial Closing Indicative Note Value: $1,000.00 |

|

|

|

|

|

|

|

|

|

|

|

| Date on Which Termination Event

Occurs |

|

Issuer Redemption Price

Calculation Date |

|

Issuer Redemption Date |

| Closing

Indicative Note

Value |

|

Indicative Note

Return |

|

Closing

Indicative Note

Value |

|

Indicative

Note Return |

|

Issuer Redemption

Price* |

|

Return on Notes |

| $900.00 |

|

-10.00% |

|

$925.00 |

|

-7.50% |

|

$901.88 |

|

-9.81% |

| $900.00 |

|

-10.00% |

|

$875.00 |

|

-12.50% |

|

$853.13 |

|

-14.69% |

| * |

Per $1,000 principal amount Note |

PPS–11

SELECTED RISK CONSIDERATIONS

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Index or components of the Index.

These risks are explained in more detail in the “Risk Factors” sections of the prospectus supplement and the prospectus addendum, including but not limited to the risk factors discussed under the following headings of the prospectus

supplement (unless otherwise noted):

| |

• |

|

“Risk Factors—Risks Relating to All Securities”; |

| |

• |

|

“Risk Factors—Additional Risks Relating to Securities with Reference Assets That Are Equity Securities or Shares or Other Interests in Exchange-Traded Funds, That Contain Equity Securities or Shares or Other

Interests in Exchange-Traded Funds or That Are Based in Part on Equity Securities or Shares or Other Interests in Exchange-Traded Funds”; |

| |

• |

|

“Risk Factors—Additional Risks Relating to Securities Which We May Call or Redeem (Automatically or Otherwise); |

| |

• |

|

“Risk Factors—Additional Risks Relating to Notes Which Are Not Characterized as Being Fully Principal Protected or Are Characterized as Being Partially Protected or Contingently Protected”;

|

| |

• |

|

“Risk Factors—Additional Risks Relating to Notes Which Pay No Interest or Pay Interest at a Low Rate”; and |

| |

• |

|

“Risk Factors—Under The Terms of the Notes, You Have Agreed To Be Bound By The Exercise of Any U.K. Bail-in Power By The Relevant U.K. Resolution Authority” (in the accompanying prospectus addendum).

|

In addition to the risks discussed under the headings above, you should consider the following:

| • |

|

Your Investment in the Notes May Result in a Significant Loss—The Notes do not guarantee any return of principal. The return on the Notes at maturity or upon early redemption is linked to the performance of

the Index (after taking into account the cumulative effects of the Investor Fee Percentage over the term of the Notes). Your investment will be fully exposed to any decline in the Closing Indicative Note Value from the Initial CINV to the Closing

Indicative Note Value on the Final Valuation Date, Automatic Call Amount Calculation Date, Issuer Redemption Price Calculation Date or Optional Redemption Amount Calculation Date, as the case may be. Because the Notes are our senior unsecured

obligations, payment of any amount at maturity or upon early redemption is subject to our ability to pay our obligations as they become due and is not guaranteed by any third party. |

| • |

|

The Level of the Index Will Depend Upon the Success of the EquityCompass Share Buyback Strategy—The Index is based on the EquityCompass Share Buyback Strategy, which seeks to capture the returns that may be

available from investing in a selected basket of stocks of up to 30 companies with the most significant share buyback announcements in the three months prior to the relevant index portfolio constitution date and which meet other eligibility

requirements. The EquityCompass Share Buyback Strategy is based on the premise that stocks of companies that announce share buybacks will perform well because share buybacks are a signal to the market that the management of a company believes the

company’s shares are undervalued. This positive signal to the market may cause the value of the shares to rise after the share buyback announcement. However, the announcement of a share buyback within the relevant three month period and other

selection criteria used by the EquityCompass Share Buyback Strategy may not be accurate predictors of future share performance. If the EquityCompass Share Buyback Strategy selects stocks that subsequently decline in value, the level of the Index

will decline, which will have an adverse effect on the value of your Notes. |

| • |

|

We Are Not Obligated to Conduct Due Diligence on the EquityCompass Share Buyback Strategy or any Index Component—We are not obligated to conduct due diligence and analysis on any index component or the

EquityCompass Share Buyback Strategy. The EquityCompass Share Buyback Strategy is maintained exclusively by the Index Selection Agent and not by Barclays Bank PLC or any of our affiliates. We cannot provide you with any assurances regarding the

ability of the EquityCompass Share Buyback Strategy to meet its stated objectives, as described under “Description of the Index” in this preliminary pricing supplement. While we or our affiliates may conduct due diligence on any index

components from time to time, prior to and during the term of the Notes, we (or our affiliates) will conduct all such due diligence and analysis solely for our own benefit and in connection with our own risk management. Neither we nor our affiliates

will conduct any due diligence or analysis for the benefit of, or on behalf of, the holders of the Notes. You cannot rely for any purpose on any of our information, analysis and opinions concerning any stock included within the Index, the basket

selected by EquityCompass Strategies to be reflected in the Index or any Index component. You are urged to consult with your own advisers before investing in the Notes. |

| • |

|

The Participation Rate of 97.50% Will Reduce Your Participation in any Appreciation, and Will Magnify Your Participation in any Depreciation, of

the Closing Indicative Note Value; You May Receive Less than the Principal Amount of Your Notes Even if the Indicative Note Return is Positive—As described on the cover page of this preliminary pricing supplement, the payment at maturity or

on an Automatic Call Date or Issuer Redemption Date with respect to your Notes will reflect a Participation Rate of 97.50%. Accordingly, you will only participate in 97.5% of any positive Indicative Note Return from the Initial Valuation Date to the

Final Valuation Date, Automatic Call Amount Calculation Date, Issuer Redemption Price Calculation Date or Optional Redemption Amount Calculation Date, as the case may be. Similarly, in the event that the Indicative Note Return, as calculated on the

Final Valuation Date, Automatic Call Amount Calculation Date, Issuer Redemption Price Calculation Date or Optional Redemption Amount Calculation Date were not sufficiently high enough to offset the effects of the Participation Rate of 97.50%, you

may receive less than the principal amount of your Notes on the Maturity Date, Automatic Call Date, Issuer Redemption Date or Optional Redemption Date, as the case may be. In the event that the Indicative

|

PPS–12

| |

Note Return, as calculated on the Final Valuation Date, Automatic Call Amount Calculation Date, Issuer Redemption Date or Optional Redemption Date, as the case may be, were negative, you will

receive a percentage of the principal amount of your Notes on the Maturity Date, Automatic Call Date, Issuer Redemption Date or Optional Redemption Date, as the case may be, that is less than the percentage of the principal amount of your Notes that

you would have received had the Participation Rate been equal to 100%. |

| • |

|

Because the Closing Indicative Note Value will Reflect the Cumulative Effects of the Investor Fee Percentage on any Given Valuation Date, the Investor Fee Percentage May Offset All or a Portion of any Increases (And

Will Magnify Any Decreases) in the Index Closing Level from the Initial Valuation Date to the Final Valuation Date, Automatic Call Amount Calculation Date, Issuer Redemption Price Calculation Date or Optional Redemption Amount Calculation Date, as

the Case May Be—As described on the cover page of this preliminary pricing supplement, the Net Index Periodic Return and, accordingly, the Closing Indicative Note Value on any given Valuation Date, will reflect the subtraction of the

Investor Fee Percentage. The Investor Fee Percentage will be equal to 0.90% per annum and will be calculated on the basis of the number of calendar days from (but excluding) the Note Rebalancing Date immediately preceding the relevant Valuation

Date (or, if such Valuation Date occurs prior to the first Note Rebalancing Date, the Initial Valuation Date) to and including the relevant Valuation Date. The subtraction described in this paragraph will be reflected in the calculation of Closing

Indicative Note Value on each Valuation Date (including for the purposes of determining whether an Automatic Call Trigger Event has occurred and for the purposes of calculating the amount owed to you at maturity or on any Automatic Call Date or

Issuer Redemption Date, as applicable) and will reduce the return on your Notes regardless of whether or not the Index increases from the Initial Index Level during the term of the Notes. The level of the Index will have to increase from its Initial

Level to an Index Closing Level on the Final Valuation Date, Automatic Call Amount Calculation Date or Issuer Redemption Price Calculation Date, as applicable, by at least the amount of the reduction described in this paragraph in order to offset

the negative effects of such reduction. |

| • |

|

Credit of Issuer—The Notes are senior unsecured debt obligations of the issuer, Barclays Bank PLC and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the

Notes, including any payment at maturity or upon early redemption or repurchase, depends on the ability of Barclays Bank PLC to satisfy its obligations as they come due and is not guaranteed by any third party. In the event Barclays Bank PLC were to

default on its obligations, you may not receive any amounts owed to you under the terms of the Notes. |

| • |

|

You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority—Under the U.K. Banking Act 2009, as recently amended, the relevant U.K. resolution

authority may exercise a U.K. Bail-in Power under certain conditions which, in summary, include that such authority determines that: (i) a relevant entity (such as the Issuer) is failing or is likely to fail, (ii) it is not reasonably

likely that (ignoring the other stabilization powers under the U.K. Banking Act) any other action will be taken to avoid the entity’s failure, (iii) the exercise of the stabilization powers are necessary taking into account certain public

interest considerations such as the stability of the U.K. financial system, public confidence in the U.K. banking system and the protection of depositors and (iv) the objectives of the resolution measures would not be met to the same extent by

the winding up of the entity. Notwithstanding these conditions, there remains uncertainty regarding how the relevant U.K. resolution authority would assess these conditions in deciding whether to exercise any U.K. Bail-in Power. The U.K. Bail-in

Power includes any statutory write-down and conversion power which allows for the cancellation of all, or a portion, of any amounts payable on the Notes, including any repayment of principal and/or the conversion of all, or a portion, of any amounts

payable on the Notes, including the repayment of principal, into shares or other securities or other obligations of ours or another person, including by means of a variation to the terms of the Notes. Accordingly, if any U.K. Bail-in Power is

exercised you may lose all or a part of the value of your investment in the Notes or receive a different security, which may be worth significantly less than the Notes and which may have significantly fewer protections than those typically afforded

to debt securities. Moreover, the relevant U.K. resolution authority may exercise its authority to implement the U.K. Bail-in Power without providing any advance notice to the holders of the Notes. |

By your acquisition of the Notes, you acknowledge, agree to be bound by, and consent to the exercise of any U.K. Bail-in Power by the

relevant U.K. resolution authority. The exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes will not be a default or an Event of Default (as each term is defined in the indenture relating to the

Notes) and the trustee will not be liable for any action that the trustee takes, or abstains from taking, in either case, in accordance with the exercise of the U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes.

Accordingly, your rights as a holder of the Notes are subject to, and will be varied, if necessary, so as to give effect to, the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. Please see “Consent to U.K.

Bail-in Power” in this preliminary pricing supplement and the risk factors in the accompanying prospectus addendum for more information.

| • |

|

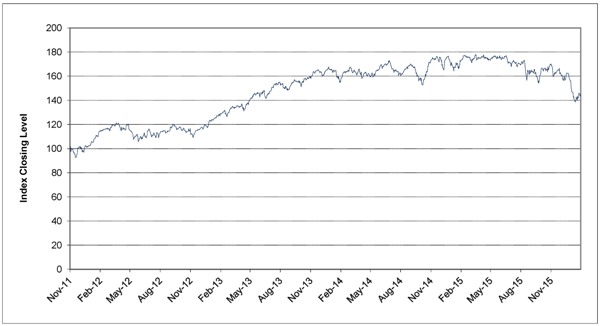

The Index Has Limited Historical Information—The Index was created in November 2011. Because limited historical performance data exists, your investment in the Notes may involve a greater risk than investing

in alternate securities linked to one or more indices with a more established record of performance. A longer history of actual performance may be helpful in providing more reliable information on which to evaluate the validity of the EquityCompass

Share Buyback Strategy and the methodology utilized by the Index to select the index components. |

PPS–13

| • |

|

Historical Levels of the Index Should not be Taken as an Indication of the Future Performance or Volatility of the Index during the Term of the Notes—It is impossible to predict whether the Index will rise

or fall. The level of the Index reflects the performance of a limited number of shares, relative to a broad market indicator. The performance of these shares may be influenced by many unpredictable factors. The actual volatility and performance of

the Index over the term of the Notes, as well as the amount payable at maturity or upon early redemption, may bear little relation to historical levels of the Index. |

| • |

|

The Index is not Actively Managed—The Index operates by pre-determined rules, as described in this preliminary pricing supplement under “Description of the Index”. There will be no active

management of the Index to enhance returns beyond those embedded in the Index. An actively managed investment may potentially respond more directly and appropriately to immediate market, political, financial or other factors than the non-actively

managed Index, which may adversely affect the level of the Index and the value of the Notes. |

| • |

|

The Index Sponsor and the Index Selection Agent Rely on Information over which they Have no Control—The index sponsor and the Index Selection Agent rely on information from various third party independent

and public sources in selecting the index components and calculating the Index level, including earnings and other financial reports published by individual companies. Neither the index sponsor nor the Index Selection Agent independently verify the

information extracted from these sources, which may be inaccurate or subject to later correction or restatement. Furthermore, if the market for any Index component is disrupted, publicly available information regarding the Index component may be

based on the last-reported levels and may be based on non-current information. |

| • |

|

The Notes Will be Automatically Redeemed if, on any Valuation Date Prior to the Final Valuation Date, the Closing Indicative Note Value per $1,000 principal amount Note is Less Than or Equal to 25% of the principal

amount per Note, or $250.00—An Automatic Call Trigger Event will occur if, on any Valuation Date prior to the Final Valuation Date, the Closing Indicative Note Value per $1,000 principal amount Note is less than or equal to $250.00. If an

Automatic Call Trigger Event occurs, the Notes will be automatically called on the applicable Automatic Call Date. Because the Closing Indicative Note Value on any Valuation Date reflects the Investor Fee Percentage for such day, it is possible that

the effect of the Investor Fee Percentage particular Valuation Date might result in the occurrence of an Automatic Call Trigger Event on such Valuation Date and, accordingly, an early redemption of your Notes. Because the Automatic Call Amount

Calculation Date will not occur until the Valuation Date following the Automatic Call Trigger Date, it is possible that the Closing Indicative Note Value will decline from the Automatic Call Trigger Date to the Automatic Call Amount Calculation Date

and the Automatic Call Amount that you will receive on the Automatic Call Date will be less than it would have been had the Automatic Call Amount been linked to the Closing Indicative Note Value per $1,000 principal amount Note on the Automatic Call

Trigger Date. In the event that an Automatic Call Trigger Event occurs, the Automatic Call Amount that you receive on the Automatic Call Date is likely to be significantly less than the principal amount of your Notes. Accordingly, you must be

willing to accept the risk that you will lose a significant amount (up to 100%) of your investment in the Notes upon the occurrence of an Automatic Call Trigger Event. |

| • |

|

The Notes Will be Automatically Redeemed Upon the Occurrence of a Termination Event—If the index sponsor determines, on or prior to the Final Valuation Date, that it will not be able to calculate and publish

the Index as a result of a Termination Event, we, in our capacity as Issuer, may redeem the Notes (in whole but not in part) on the applicable Issuer Redemption Date at the applicable Issuer Redemption Price. If a Termination Event occurs, the

Issuer Redemption Price that you will receive on the Issuer Redemption Date may be significantly less than the amount you would have received for your Notes on the Maturity Date had the Termination Event not occurred. Because the Issuer Redemption

Price will not occur until the Valuation Date following the date on which a Termination Event occurs, it is possible that the Closing Indicative Note Value will decline from the date on which a Termination Event occurs to the Issuer Redemption Price

Calculation Date and the Issuer Redemption Price that you will receive on the Issuer Redemption Date will be less than it would have been had the Issuer Redemption Price been linked to the Closing Indicative Note Value per $1,000 principal amount

Note on the date on which the Termination Event occurred. Because the Closing Indicative Note Value on an Issuer Redemption Price Calculation Date may be less than the principal amount of your Notes, the Issuer Redemption Price that you receive on

an Issuer Redemption Date may be less, and may be significantly less, than the principal amount of your Notes. Accordingly, you must be willing to accept the risk that you will lose a significant amount of your investment in the Notes upon the

occurrence of a Termination Event. |

Because Barclays Bank PLC is the owner of the intellectual property and licensing rights

relating to the Index and because the issuer of the Notes and the index sponsor is our wholly-owned subsidiary, we may have conflicts of interest that may affect your Notes in various ways, including the occurrence of a Termination Event. You are

urged to read carefully “As Index Sponsor, We Will Have the Authority to Make Determinations That Could Materially Affect Your Notes in Various Ways and Create Conflicts of Interest” below. As noted elsewhere in this preliminary pricing

supplement, you are urged to consult with your own advisors prior to investing in the Notes.

| • |

|

Potential Early Exit—Your Notes are subject to early redemption upon the occurrence of a Termination Event or an Automatic Call Trigger Event, as described under the “Issuer Redemption” and

“Automatic Call” provisions on the cover page of this preliminary pricing supplement. You may not be able to reinvest any amounts received on an Automatic Call Date or Issuer Redemption Date, as the case may be, in a comparable investment

with similar risk and appreciation potential as the Notes. The “Automatic Call” and “Issuer Redemption” features may also adversely impact your ability to sell your Notes and the price at which they may be sold. Furthermore,

as noted elsewhere in this preliminary pricing supplement, the Automatic Call Amount or the Issuer Redemption Price, as the case may be, may be substantially less than the principal amount of your Notes, and you may some or all of the principal

amount of your Notes upon the occurrence of a Termination Event or an Automatic Call Trigger Event, as the case may be. |

PPS–14

| • |

|

Postponement of a Valuation Date May Result in a Reduced Amount Payable at Maturity or Upon Redemption—As the payment at maturity or upon redemption is a function of, among other things, the Closing

Indicative Note Value on the Final Valuation Date or an Automatic Call Amount Calculation Date or Issuer Redemption Price Calculation Date, as the case may be, the postponement of any Valuation Date may result in the application of a different

Closing Indicative Note Value and, accordingly, decrease the payment you receive at maturity or upon redemption. For the avoidance of doubt, if a Valuation Date (including the Final Valuation Date, Automatic Call Amount Calculation Date or Issuer

Redemption Price Calculation Date, as the case may be) is postponed, the Closing Indicative Note Value on such date, as postponed, will reflect the subtraction of the Investor Fee Percentage calculated as of such date, as postponed.

|

Also as noted on the cover page of this preliminary pricing supplement, if a Market Disruption Event occurs on any Valuation

Date, such date will be disregarded for purposes of determining whether an Automatic Call Trigger Event occurs. In such an event, your may suffer losses on your Notes in an amount greater than you would have suffered had an Automatic Call Trigger

Event been deemed to occur on the Valuation Date on which such event would have occurred but for the relevant Market Disruption Event.

| • |

|

No Interest or Dividend Payments or Voting Rights—As a holder of the Notes, you will not receive any periodical interest payments under the Notes, and you will not have voting rights or rights to receive

cash dividends or other distributions or other rights that holders of securities comprising the Index would have. |

| • |

|

The Estimated Value of the Notes Is Not a Prediction of the Prices at Which the Notes May Trade in the Secondary Market, If Any Such Market Exists, and Such Secondary Market Prices, If Any, May Be Lower Than the

Principal Amount of the Notes and May Be Lower Than Such Estimated Value of the Notes—The estimated value of the Notes will not be a prediction of the prices at which the Notes may trade in secondary market transactions, if any such market

exists, nor will it be a prediction of the Closing Indicative Note Value on any day or the Optional Redemption Amount that you will receive upon an optional redemption of your Notes. The price at which you may be able to sell your Notes in the

secondary market at any time will be influenced by many factors that cannot be predicted, such as market conditions, and any bid and ask spread for similar sized trades, and may be substantially less than our estimated value of the Notes on the

cover page of this preliminary pricing supplement. The Optional Redemption Amount that you will receive upon an optional redemption of your Notes will depend on the path taken by the Notes from the Initial Valuation Date to the Optional Redemption

Amount Calculation Date, and will be limited by the Participation Rate of 97.50% and will be adversely affected by the effect of the Investor Fee Percentage. Similarly, the Issuer Redemption Price or Automatic Call Amount that you may receive on the

Notes, as described on the cover page of this preliminary pricing supplement, will be limited by the Participation Rate of 97.50%, will be adversely affected by the effect of the Investor Fee Percentage and may be substantially less than our

estimated value of the Notes on the cover page of this preliminary pricing supplement. |

| • |

|

Certain Built-In Costs Are Likely to Adversely Affect the Value of the Notes Prior to Maturity—While the payment at maturity described in this preliminary pricing supplement is based on the full principal

amount of your Notes, the original issue price of the Notes includes the agent’s commission and the cost of hedging our obligations under the Notes through one or more of our affiliates. As a result, the price, if any, at which Barclays Capital

Inc. And other affiliates of Barclays Bank PLC will be willing to purchase Notes from you in secondary market transactions will likely be lower than the price you paid for your Notes, and any sale prior to the Maturity Date could result in a

substantial loss to you. |

| • |

|

The Index Sponsor, Our Wholly-Owned Subsidiary, Will Have the Authority to Make Determinations That Could Materially Affect Your Notes in Various Ways and Create Conflicts of Interest—We are the owner of the

intellectual property and licensing rights relating to the Index and the index sponsor of the Index is our wholly-owned subsidiary. The index sponsor is responsible for the composition, calculation and maintenance of the Index. As discussed under

“Description of the Index” in this preliminary pricing supplement, the index sponsor has the discretion in a number of circumstances, including upon the occurrence of an index market disruption event or force majeure event, to make

judgments and take actions in connection with the composition, calculation and maintenance of the Index, and any such judgments or actions may adversely affect the value of the Notes. For example, if there is a lack of liquidity or material decline

in the liquidity of an index component, the index sponsor could determine that this is an index market disruption event and take any action as set forth under “Description of the Index—Market Disruption and Force Majeure Events.”

|

The role played by the index sponsor, and the exercise by the index sponsor of the kinds of discretion described above and

in “Description of the Index”, could present it with significant conflicts of interest in light of the fact that Barclays Bank PLC, the issuer of the Notes, is its parent company and the index owner. The index sponsor, in its capacity as

such, has no obligation to take the needs of any buyer, seller or holder of the Notes into consideration at any time.

PPS–15

| • |

|

Our Business Activities May Create Conflicts of Interest—In addition to the role of Barclays Risk Analytics and Index Solutions Limited, our wholly-owned subsidiary, as index sponsor, our wholly-owned

subsidiary (as described in this preliminary pricing supplement), our affiliates expect to play a variety of roles in connection with the issuance of the Notes. |

We and our affiliates establish the offering price of the Notes for initial sale to the public, and the offering price is not based upon any

independent verification or valuation. Additionally, the role played by Barclays Capital Inc., as a dealer in the Notes, could present it with significant conflicts of interest with the role of Barclays Bank PLC, as issuer of the Notes. For example,

Barclays Capital Inc. or its representatives may derive compensation or financial benefit from the distribution of the Notes and such compensation or financial benefit may serve as an incentive to sell these Notes instead of other investments. We

may pay dealer compensation to any of our affiliates acting as agents or dealers in connection with the distribution of the Notes. Furthermore, we and our affiliates make markets in and trade various financial instruments or products for their own

accounts and for the account of their clients and otherwise provide investment banking and other financial services with respect to these financial instruments and products. These financial instruments and products may include securities,

instruments or assets that may serve as the underliers, basket underliers or constituents of the underliers of the Notes. Such market making, trading activities, other investment banking and financial services may negatively impact the value of the

Notes. Furthermore, in any such market making, trading activities, and other services, we or our affiliates may take positions or take actions that are inconsistent with, or adverse to, the investment objectives of the holders of the Notes. We and

our affiliates have no obligation to take the needs of any buyer, seller or holder of the Notes into account in conducting these activities

| • |

|

There May be Conflicts of Interest Involving the Calculation Agent—In addition to the variety of roles that we and our affiliates play in connection with the issuance of the Notes described above, we also

act as calculation agent and may enter into transactions to hedge our obligations under the Notes. In performing these varied duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your

interests as an investor in the Notes. |

| • |

|

There May Be Conflicts of Interest With Respect to the Notes Involving Our Affiliates and the Index Selection Agent and its Affiliates; One or More Affiliates of the Index Selection Agent May Act as a Dealer in the