Filed

Pursuant to Rule 424(b)(2)

Registration No. 333-272447

Pricing Supplement dated May 8, 2024

(To Equity Index Underlying Supplement dated September

5, 2023,

Prospectus Supplement dated September 5, 2023, and

Prospectus dated September 5, 2023)

STRUCTURED INVESTMENTS

Opportunities in U.S. Equities

$3,594,000 Contingent Income Auto-Callable Securities

due May 13, 2027

Based on the Worst Performing of the S&P 500®

Index, the Nasdaq-100 Index® and the Russell 2000® Index

Principal at Risk Securities

The Contingent Income Auto-Callable Securities (the “securities”)

are unsecured debt obligations of Canadian Imperial Bank of Commerce (“CIBC” or the “Bank”). The securities have

the terms described in the accompanying underlying supplement, prospectus supplement and prospectus, as supplemented or modified by this

document. The securities do not guarantee the payment of interest or the repayment of any principal. Instead, the securities will pay

a Contingent Quarterly Coupon at an annual rate of 8.60% but only if the Closing Level of each of the S&P 500®

Index, the Nasdaq-100 Index® and the Russell 2000® Index on the related Observation Date is at

or above 70.00% of its respective Initial Index Value, which we refer to as the respective Coupon Barrier Level. However,

if the Closing Level of any Underlying Index is less than its Coupon Barrier Level on any Observation Date, we will

pay no interest for the related quarterly period. In addition, the securities will be automatically redeemed if the Closing Level of

each Underlying Index is greater than or equal to its respective Initial Index Value on any quarterly Observation

Date, beginning on May 8, 2025 and ending on February 8, 2027, for the Early Redemption Payment equal to the sum of the Stated Principal

Amount plus the related Contingent Quarterly Coupon. No further payments will be made on the securities once they have been redeemed.

At maturity, if the securities have not previously been redeemed and the Final Index Value of each Underlying Index is greater

than or equal to 70.00% of its respective Initial Index Value, which we refer to as the respective Downside Threshold Level, the

Payment at Maturity will be the Stated Principal Amount and the related Contingent Quarterly Coupon. If, however, the Final Index Value

of any Underlying Index is less than its Downside Threshold Level, investors will be fully exposed to the decline in the

Worst Performing Underlying Index on a 1-to-1 basis and will receive a Payment at Maturity that is less than 70.00% of the Stated

Principal Amount of the securities and could be zero. Accordingly, investors in the securities must be willing to accept the risk

of losing their entire initial investment based on the performance of the Worst Performing Underlying Index and also the risk of not

receiving any quarterly coupons during the entire term of the securities. Because all payments on the securities are based on the

worst performing of the Underlying Indices, a decline beyond the respective Coupon Barrier Level on any Observation Date and/or beyond

the respective Downside Threshold Level on the final Observation Date, as applicable, of any Underlying Index will result in the

forfeiture of Contingent Quarterly Coupons and/or a significant loss of your investment, as applicable, even if one or both of the other

Underlying Indices have appreciated or have not declined as much. Investors will not participate in any appreciation in any Underlying

Index. The securities are for investors who are willing to risk their principal based on the worst performing of three Underlying Indices

and who seek an opportunity to earn interest at a potentially above-market rate in exchange for the risk of receiving no quarterly interest

if any Underlying Index closes below its Coupon Barrier Level on any Observation Date, and the risk of an early redemption of

the securities.

All payments are subject to our credit risk. If

we default on our obligations, you could lose some or all of your investment. These securities are not secured obligations and you will

not have any security interest in, or otherwise have any access to, any Underlying Index or any securities included in any Underlying

Index. The securities will not constitute deposits insured by the Canada Deposit Insurance Corporation, the U.S. Federal Deposit Insurance

Corporation, or any other government agency or instrumentality of Canada, the United States or any other jurisdiction. The securities

are not bail-inable debt securities (as defined on page 6 of the prospectus).

| Final Terms |

| Issuer: |

Canadian Imperial Bank of Commerce |

| Underlying Indices: |

The S&P 500® Index (Bloomberg symbol:

SPX) (the “SPX Index”), the Nasdaq-100 Index® (Bloomberg symbol: NDX) (the “NDX Index”),

and the Russell 2000® Index (Bloomberg symbol: RTY) (the “RTY Index”) |

| Aggregate Principal Amount: |

$3,594,000 |

| Stated Principal Amount: |

$1,000 per security |

| Pricing Date: |

May 8, 2024 |

| Original Issue Date: |

May 13, 2024 (3 Business Days after the Pricing Date) |

| Final Observation Date: |

May 10, 2027, subject to postponement as described under

“Certain Terms of the Notes—Valuation Dates—For Notes Where the Reference Asset Consists of Multiple Indices”

in the accompanying underlying supplement. |

| Maturity Date: |

May 13, 2027, subject to Automatic Early Redemption and

postponement as described under “Certain Terms of the Notes—Interest Payment Dates, Coupon Payment Dates, Call Payment

Dates and Maturity Date” in the underlying supplement. |

| Automatic Early Redemption: |

If, on any quarterly Observation Date beginning on May 8,

2025 and ending on February 8, 2027, the Closing Level of each Underlying Index is greater than or equal to its Initial

Index Value, the securities will be automatically redeemed for an Early Redemption Payment on the related Coupon Payment Date. No

further payments will be made on the securities once they have been redeemed. |

| Early Redemption Payment: |

The Early Redemption Payment will be an amount equal to

(i) the Stated Principal Amount plus (ii) the Contingent Quarterly Coupon with respect to the related Observation Date. |

| CUSIP / ISIN: |

13607XRZ2 / US13607XRZ23 |

| Listing: |

The securities will not be listed on any securities exchange. |

| Commissions and Issue Price: |

|

Price to Public |

Agent’s

Commissions |

Proceeds to Issuer |

| Per Security |

|

$1,000.00 |

$17.50(1) |

|

| |

|

|

$3.90(2) |

$978.60 |

| Total |

|

$3,594,000.00 |

$62,895.00 |

$3,517,088.40 |

| |

|

|

$14,016.60 |

|

(1) CIBC World Markets Corp. (“CIBCWM”), acting as agent

for the Bank, will receive a fee of $21.40 per security and will pay Morgan Stanley Smith Barney LLC (“Morgan Stanley Wealth Management”)

a fixed sales commission of $17.50 for each security they sell. See “Additional Information About the Securities — Supplemental

Plan of Distribution (Conflicts of Interest)” below.

(2) Of the $21.40 per security

received by CIBCWM, CIBCWM will pay Morgan Stanley Wealth Management a structuring fee of $3.90 for each security.

The initial estimated value of the securities on the Pricing Date as

determined by CIBC is $962.60 per security, which is less than the price to public. See “Risk Factors—General Risks” beginning

on page 13 of this pricing supplement and “Additional Information About the Securities—The Bank’s Estimated Value of

the Securities” beginning on page 25 of this pricing supplement for additional information.

Neither the U.S. Securities

and Exchange Commission (the “SEC”) nor any state or provincial securities commission has approved or disapproved the securities

or determined if this pricing supplement or the accompanying underlying supplement, prospectus supplement or prospectus is truthful or

complete. Any representation to the contrary is a criminal offense.

Investing in the securities involves risks not associated with

an investment in ordinary debt securities. See “Risk Factors” beginning on page 11 of this pricing supplement, and “Risk

Factors” beginning on page S-1 of the accompanying underlying supplement, page S-1 of the prospectus supplement and page 1 of the

prospectus.

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Terms continued from previous page:

| Contingent

Quarterly Coupon: |

·

If, on any Observation Date, the Closing Level of each Underlying

Index is greater than or equal to its Coupon Barrier Level, we will pay a Contingent Quarterly Coupon of $21.50 per security

(equivalent to an annual rate of 8.60%) on the related Coupon Payment Date.

· If,

on any Observation Date, the Closing Level of any Underlying Index is less than its Coupon Barrier Level, no Contingent

Quarterly Coupon will be paid with respect to that Observation Date. |

| Observation

Dates: |

Quarterly,

on August 8, 2024, November 8, 2024, February 10, 2025, May 8, 2025, August 8, 2025, November 10, 2025, February 9, 2026, May 8,

2026, August 10, 2026, November 9, 2026, February 8, 2027 and May 10, 2027 (the “final Observation Date”). Each Observation

Date is subject to postponement for non-Trading Days and certain Market Disruption Events as described under “Certain Terms

of the Notes—Valuation Dates—For Notes Where the Reference Asset Consists of Multiple Indices” in the underlying

supplement. |

| Coupon

Payment Dates: |

With respect

to each Observation Date other than the final Observation Date, the third Business Day after the related Observation Date. The payment

of the Contingent Quarterly Coupon, if any, with respect to the final Observation Date will be made on the Maturity Date. Each Coupon

Payment Date is subject to postponement as described under “Certain Terms of the Notes—Interest Payment Dates, Coupon

Payment Dates, Call Payment Dates and Maturity Date” in the underlying supplement. |

| Payment

at Maturity: |

If the

securities have not been previously redeemed, investors will receive on the Maturity Date a Payment at Maturity determined as follows: |

·

If the Final Index Value of each

Underlying Index is greater than or equal to its respective Downside Threshold Level: the Stated Principal Amount plus

the Contingent Quarterly Coupon with respect to the final Observation Date

·

If the Final Index Value of any

Underlying Index is less than its Downside Threshold Level: (i) the Stated Principal Amount multiplied by (ii) the

Index Performance Factor of the Worst Performing Underlying Index.

Under these circumstances, the

Payment at Maturity will be less than 70.00% of the Stated Principal Amount of the securities and could be zero. Even with any Contingent

Quarterly Coupons, the return on the securities could be negative. |

| Coupon

Barrier Level: |

3,631.369

with respect to the SPX, 12,659.507 with respect to the NDX and 1,438.5945 with respect to the RTY, each of which is 70.00% of its

Initial Index Value |

| Downside

Threshold Level: |

3,631.369

with respect to the SPX, 12,659.507 with respect to the NDX and 1,438.5945 with respect to the RTY, each of which is 70.00% of its

Initial Index Value |

| Index

Performance Factor of the Worst Performing Underlying Index: |

With respect

to the Worst Performing Underlying Index, its Final Index Value divided by its Initial Index Value |

| Worst

Performing Underlying Index: |

The Underlying

Index with the lowest Final Index Value as compared to the respective Initial Index Value |

| Initial

Index Value: |

5,187.67

with respect to the SPX, 18,085.01 with respect to the NDX and 2,055.135 with respect to the RTY, each of which was its Closing Level

on the Pricing Date. |

| Final

Index Value: |

With respect

to each Underlying Index, its Closing Level on the final Observation Date. |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Investment Summary

Contingent Income Auto-Callable Securities

Principal at Risk Securities

Contingent Income Auto-Callable Securities due May 13,

2027 Based on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index (the “securities”) do not guarantee the repayment of any principal and do not provide for the regular payment

of interest. Instead, the securities will pay a Contingent Quarterly Coupon but only if the Closing Level of each Underlying

Index is at or above its respective Coupon Barrier Level on the related Observation Date. However, if the Closing Level

of any Underlying Index is less than its Coupon Barrier Level on any Observation Date, we will pay no interest for

the related quarterly period. If the Closing Level of at least one Underlying Index is less than its respective Coupon

Barrier Level on each Observation Date, you will not receive any Contingent Quarterly Coupon for the entire term of the securities.

In addition, if the Closing Level of each Underlying Index is greater than or equal to its Initial Index Value on any quarterly

Observation Date beginning on May 8, 2025 and ending on February 8, 2027, the securities will be automatically redeemed for an Early

Redemption Payment equal to the Stated Principal Amount plus the Contingent Quarterly Coupon with respect to the related Observation

Date. If the securities have not been automatically called prior to maturity and the Final Index Value of any Underlying Index

is less than its Downside Threshold Level, investors will be fully exposed to the decline in the Worst Performing Underlying Index

on a 1-to-1 basis, and will receive a Payment at Maturity that is less than 70.00% of the Stated Principal Amount of the securities and

could be zero. Accordingly, investors in the securities must be willing to accept the risk of losing their entire initial investment

based on the performance of the Worst Performing Underlying Index and also the risk of not receiving any quarterly coupons throughout

the entire term of the securities. In addition, investors will not participate in any appreciation of any Underlying Index.

| Maturity: |

Three years,

unless redeemed earlier |

| Contingent Quarterly Coupon: |

If the Closing Level of each Underlying Index

is greater than or equal to its respective Coupon Barrier Level on an Observation Date, we will pay a Contingent Quarterly

Coupon of $21.50 per security (equivalent to an annual rate of 8.60%) on the related Coupon Payment Date.

If the Closing Level of any Underlying Index

is less than its Coupon Barrier Level, no Contingent Quarterly Coupon will be paid with respect to that quarterly period.

It is possible that one or more Underlying Indices will close below the respective Coupon Barrier Level(s) on most or all of the

Observation Dates so that you will receive few or no Contingent Quarterly Coupons throughout the entire term of the securities. |

| Automatic Early Redemption: |

If the Closing Level of each Underlying

Index is greater than or equal to its Initial Index Value on any quarterly Observation Date beginning on May 8, 2025 and ending

on February 8, 2027, the securities will be automatically redeemed for an Early Redemption Payment equal to the Stated Principal

Amount plus the Contingent Quarterly Coupon with respect to the related Observation Date. No further payments will be made on the

securities once they have been redeemed. |

| Payment at Maturity: |

If the securities have not been automatically redeemed

prior to maturity, the Payment at Maturity will be determined as follows:

If the Final Index Value of each Underlying

Index is greater than or equal to its respective Downside Threshold Level: the Stated Principal Amount and the Contingent

Quarterly Coupon with respect to the final Observation Date.

If the Final Index Value of any Underlying

Index is less than its Downside Threshold Level: the Stated Principal Amount times the Index Performance Factor of

the Worst Performing Underlying Index. Under these circumstances, the Payment at Maturity will be less than 70.00% of the Stated

Principal Amount of the securities and could be zero. No quarterly coupon will be payable at maturity. Accordingly, investors

in the securities must be willing to accept the risk of losing their entire initial investment.

|

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Key Investment Rationale

The securities do not guarantee the repayment of any principal

at maturity and do not provide for the regular payment of interest. Instead, the securities will pay a Contingent Quarterly Coupon but

only if the Closing Level of each Underlying Index is at or above its respective Coupon Barrier Level on the

related Observation Date. However, if the Closing Level of any Underlying Index is less than its Coupon Barrier Level

on any Observation Date, we will pay no interest for the related quarterly period. These securities are for investors who are willing

to risk their principal and seek an opportunity to earn interest at a potentially above-market rate in exchange for the risk of receiving

no quarterly interest if any Underlying Index closes below its Coupon Barrier Level on any Observation Date, and the risk of an

early redemption of the securities.

The following scenarios are for illustration purposes only to demonstrate

how the Contingent Quarterly Coupon and the Payment at Maturity (if the securities have not been previously redeemed) are determined,

and do not attempt to demonstrate every situation that may occur. Accordingly, the securities may or may not be redeemed prior to maturity,

the Contingent Quarterly Coupon may not be payable with respect to some or all of the quarterly periods during the term of the securities,

and the Payment at Maturity may be less than 70.00% of the Stated Principal Amount of the securities and may be zero. Investors will

not participate in any appreciation in any Underlying Index. Even with any Contingent Quarterly Coupons, the return on the securities

could be negative.

| Scenario

1: The securities are redeemed prior to maturity |

This scenario assumes that, prior to early redemption,

each Underlying Index closes at or above its Coupon Barrier Level on some quarterly Observation Dates, but one or more

Underlying Indices close below the respective Coupon Barrier Level(s) on the others. Investors receive the Contingent Quarterly Coupon,

corresponding to a return of 8.60% per annum, for the quarterly periods for which the Closing Level of each Underlying

Index is at or above the respective Coupon Barrier Level on the related Observation Date, but not for the quarterly periods for which

the Closing Level of any Underlying Index is below its Coupon Barrier Level on the related Observation Date.

When each Underlying Index closes at or above

its respective Initial Index Value on a quarterly Observation Date, the securities will be automatically redeemed for the

Stated Principal Amount plus the Contingent Quarterly Coupon with respect to the related Observation Date.

|

| Scenario

2: The securities are not redeemed prior to maturity, and investors receive principal

back at maturity |

This scenario assumes that each Underlying Index closes

at or above the respective Coupon Barrier Level on some quarterly Observation Dates, but one or more Underlying Indices close below

the respective Coupon Barrier Level(s) on the others, and each Underlying Index closes below its respective Initial Index Value on

every quarterly Observation Date. Consequently, the securities are not automatically redeemed, and investors receive the Contingent

Quarterly Coupon, corresponding to a return of 8.60% per annum, for the quarterly periods for which the Closing Level of each

Underlying Index is at or above the respective Coupon Barrier Level on the related Observation Date, but not for the quarterly

periods for which the Closing Level of any Underlying Index is below its Coupon Barrier Level on the related Observation Date.

On the final Observation Date, each

Underlying Index closes at or above its Downside Threshold Level. At maturity, investors will receive the Stated Principal Amount

and the Contingent Quarterly Coupon with respect to the final Observation Date.

|

| Scenario

3: The securities are not redeemed prior to maturity, and investors suffer a substantial

loss of principal at maturity |

This scenario assumes that each Underlying Index closes at or above

its respective Coupon Barrier Level on some quarterly Observation Dates, but one or more Underlying Indices close below the respective

Coupon Barrier Level(s) on the others, and each Underlying Index closes below its respective Initial Index Value on every quarterly

Observation Date. Consequently, the securities are not automatically redeemed, and investors receive the Contingent Quarterly Coupon,

corresponding to a return of 8.60% per annum, for the quarterly periods for which the Closing Level of each Underlying

Index is at or above the respective Coupon Barrier Level on the related Observation Date, but not for the quarterly periods for which

the Closing Level of any Underlying Index is below its Coupon Barrier Level on the related Observation Date.

On the final Observation Date, one or more Underlying

Indices close below the respective Downside Threshold Level(s). At maturity, investors will receive an amount equal to the Stated

Principal Amount multiplied by the Index Performance Factor of the Worst Performing Underlying Index. Under these circumstances,

the Payment at Maturity will be less than 70.00% of the Stated Principal Amount and could be zero. No coupon will be paid at maturity

in this scenario.

|

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

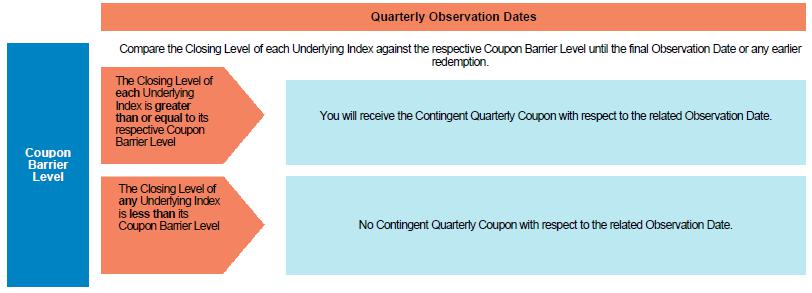

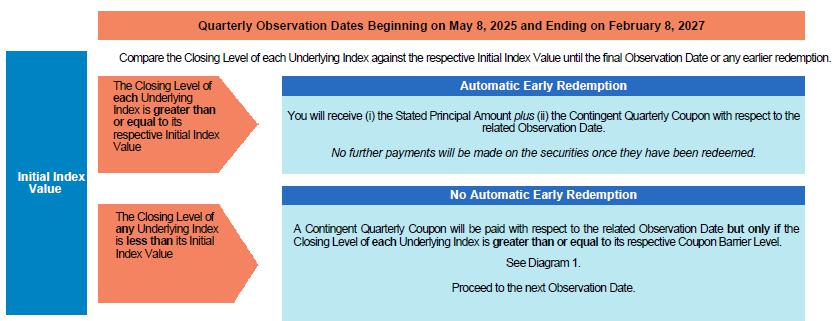

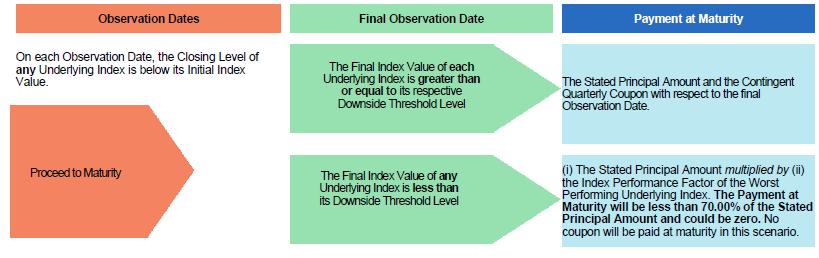

How the Securities Work

The following diagrams illustrate the potential outcomes for the securities

depending on (1) the Closing Level of each Underlying Index on each quarterly Observation Date, and (2) the Final Index Value of each

Underlying Index. Please see “Hypothetical Examples” beginning on page 7 for illustration of hypothetical payouts on the

securities.

Diagram #1: Contingent Quarterly Coupons (Beginning

on the First Coupon Payment Date until Automatic Early Redemption or Maturity)

Diagram #2: Automatic Early Redemption

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Diagram #3: Payment at Maturity if No Automatic Early

Redemption Occurs

For more information about the payout upon an early redemption or

at maturity in different hypothetical scenarios, see “Hypothetical Examples” starting on page 7.

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Hypothetical Examples

The following hypothetical examples illustrate how to determine whether

a Contingent Quarterly Coupon is payable with respect to an Observation Date and how to calculate the Payment at Maturity, if any, if

the securities have not been automatically redeemed early. The following examples are for illustrative purposes only. Whether you receive

a Contingent Quarterly Coupon will be determined by reference to the Closing Level of each Underlying Index on each quarterly Observation

Date, and the amount you will receive at maturity, if any, will be determined by reference to the Final Index Value of the Worst Performing

Underlying Index on the final Observation Date. The actual Initial Index Value, Coupon Barrier Level and Downside Threshold Level for

each Underlying Index are set forth on page 2 of this pricing supplement. All payments on the securities, if any, are subject to our

credit risk. The numbers in the hypothetical examples below may have been rounded for the ease of analysis. The below examples are based

on the following terms:

| Stated Principal Amount: |

$1,000 per security |

| Hypothetical Initial Index Values: |

1,000 for each Underlying Index |

| Contingent Quarterly Coupon: |

$21.50 per quarter (8.60% per annum or 2.15% per quarter) |

| Observation Dates: |

Quarterly, commencing on August 8, 2024 |

| Hypothetical Coupon Barrier Levels: |

700.00 for each Underlying Index (70.00% of its hypothetical Initial

Index Value) |

| Hypothetical Downside Threshold Levels: |

700.00 for each Underlying Index (70.00% of its hypothetical Initial

Index Value) |

How to determine whether a Contingent Quarterly

Coupon is payable with respect to an Observation Date:

| |

Closing

Level |

Contingent

Quarterly

Coupon |

| |

SPX

Index |

NDX

Index |

RTY

Index |

|

| Hypothetical

Observation Date 1 |

800 (at or above Coupon

Barrier Level)

|

950 (at or above Coupon

Barrier Level) |

1,050 (at or above Coupon

Barrier Level) |

$21.50 |

| Hypothetical Observation

Date 2 |

800

(at or above Coupon

Barrier Level) |

1,200 (at or above Coupon

Barrier Level) |

500 (below Coupon Barrier

Level) |

$0 |

| Hypothetical Observation

Date 3 |

600

(below Coupon Barrier

Level) |

500 (below Coupon Barrier

Level) |

1,150 (at or above Coupon

Barrier Level) |

$0 |

| Hypothetical Observation

Date 4 |

500

(below Coupon Barrier

Level) |

400

(below Coupon

Barrier Level) |

550 (below Coupon

Barrier Level) |

$0 |

On hypothetical Observation Date 1, each Underlying Index closes at

or above its respective Coupon Barrier Level. Therefore, a Contingent Quarterly Coupon of $21.50 is paid on the relevant Coupon Payment

Date.

On each of hypothetical Observation Dates 2 and 3, at least one Underlying

Index closes at or above its respective Coupon Barrier Level, but one or both of the other Underlying Indices close below their respective

Coupon Barrier Levels. Therefore, no Contingent Quarterly Coupon is paid on the relevant Coupon Payment Date.

On hypothetical Observation Date 4, each Underlying Index closes below

its respective Coupon Barrier Level, and, accordingly, no Contingent Quarterly Coupon is paid on the relevant Coupon Payment Date.

If the Closing Level of at least one Underlying Index is less than

its Coupon Barrier Level on each Observation Date, you will not receive any Contingent Quarterly Coupons for the entire term of the securities.

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

How to calculate the Payment at Maturity (if the securities

have not been automatically redeemed):

If the Closing Level of each Underlying Index is greater than

or equal to its Initial Index Value on any quarterly Observation Date beginning on May 8, 2025 and ending on February 8, 2027, the securities

will be automatically redeemed for an Early Redemption Payment equal to the Stated Principal Amount for each security you hold plus

the Contingent Quarterly Coupon with respect to the related Observation Date.

The examples below illustrate how to calculate the Payment

at Maturity if the securities have not been automatically redeemed prior to maturity.

| |

Final

Index Value |

Payment

at Maturity |

| |

SPX

Index |

NDX

Index |

RTY

Index |

| Example

1: |

400

(below the Downside Threshold Level) |

500

(below the Downside Threshold Level) |

750

(at or above the Downside Threshold Level) |

$1,000 × Index Performance Factor of the

Worst Performing Underlying Index =

$1,000 × (400 / 1,000) = $400 |

| Example

2: |

800

(at or above the Downside Threshold Level) |

750

(at or above the Downside Threshold Level) |

500

(below the Downside Threshold Level) |

$1,000

× (500 / 1,000) = $500 |

| Example

3: |

400

(below the Downside Threshold Level) |

300

(below the Downside Threshold Level) |

450

(below the Downside Threshold Level) |

$1,000 × (300

/ 1,000) = $300 |

| Example

4: |

400

(below the Downside Threshold Level) |

400

(below the Downside Threshold Level) |

300

(below the Downside Threshold Level) |

$1,000 × (300

/ 1,000) = $300 |

| Example

5: |

1,100

(at or above the

Downside Threshold Level) |

800

(at or above the Downside Threshold Level) |

750

(at or above the Downside Threshold Level) |

The Stated Principal Amount + the Contingent Quarterly Coupon with

respect to the final Observation Date.

|

| Example

6: |

1,300

(at or above the

Downside Threshold Level) |

1,200

(at or above the Downside Threshold Level) |

1,600

(at or above the Downside Threshold Level) |

The Stated Principal Amount + the Contingent Quarterly Coupon with

respect to the final Observation Date.

For more information, please see above under “How to determine

whether a Contingent Quarterly Coupon is payable with respect to an Observation Date.” |

In examples 1 and 2, the Final Index Value(s) of one or two

of the Underlying Indices are at or above the respective Downside Threshold Level(s), but the Final Index Value(s) of one or both of

the other Underlying Indices are below the respective Downside Threshold Level(s). Therefore, investors are exposed to the downside performance

of the Worst Performing Underlying Index at maturity and receive at maturity an amount equal to the Stated Principal Amount multiplied

by the Index Performance Factor of the Worst Performing Underlying Index. Moreover, investors do not receive any Contingent Quarterly

Coupon for the final quarterly period.

Similarly, in examples 3 and 4, the Final Index Value of

each Underlying Index is below its respective Downside Threshold Level, and investors receive at maturity an amount equal to the Stated

Principal Amount times the Index Performance Factor of the Worst Performing Underlying Index. In example 3, the SPX Index has

declined 60% from its Initial Index Value to its Final Index Value, the NDX Index has declined 70% from its Initial Index Value to its

Final Index Value, and the RTY Index has declined 55% from its Initial Index Value to its Final Index Value. Therefore, the Payment at

Maturity equals the Stated Principal Amount multiplied by the Index Performance Factor of the NDX Index, which is the Worst Performing

Underlying Index in this example. In example 4, the SPX Index has declined 60% from its Initial Index Value to its Final Index Value,

the NDX Index has declined 60% from its Initial Index Value, and the RTY Index has declined 70% from its Initial Index Value to its Final

Index Value. Therefore, the Payment at Maturity equals the Stated Principal Amount times the Index Performance Factor of the RTY

Index, which is the Worst Performing Underlying Index in this example. Moreover, investors do not receive the Contingent Quarterly Coupon

for the final quarterly period.

In examples 5 and 6, the Final Index Value of each Underlying

Index is at or above its respective Downside Threshold Level and its respective Coupon Barrier Level. Therefore, investors receive at

maturity the Stated Principal Amount of the securities plus the

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Contingent Quarterly Coupon with respect to the final Observation

Date. However, investors do not participate in any appreciation of the Underlying Indices.

If the securities have not been redeemed prior to maturity

and the Final Index Value of ANY Underlying Index is below its Downside Threshold Level, you will be exposed to the downside performance

of the Worst Performing Underlying Index at maturity, and your Payment at Maturity will be less than 70% of the stated principal amount

per security and could be zero.

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Supplemental Terms of the Securities

For purposes of the securities offered by this pricing supplement, all

references to each of the following terms used in the accompanying underlying supplement will be deemed to refer to the corresponding

term used in this pricing supplement, as set forth in the table below:

Underlying Supplement Term

Coupon Determination Date/ Call Observation Date

Final Valuation Date

Reference Asset / Index

|

Pricing Supplement Term

Observation Date

final Observation Date

Underlying Index

|

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Risk Factors

An investment in the securities involves significant risks. This

section describes the material risks relating to the securities. For further discussion of these and other risks, you should read the

section entitled “Risk Factors” beginning on page S-1 of the accompanying underlying supplement, page S-1 of the prospectus

supplement and page 1 of the prospectus. We also urge you to consult with your investment, legal, tax, accounting and other advisers

in connection with your investment in the securities.

Risks Relating to the Structure of the Securities

| · | The securities do not

guarantee the return of any principal. The terms of the securities differ from those

of ordinary debt securities in that the securities do not provide the regular interest payments

or guarantee the return of any of the Stated Principal Amount at maturity. Instead, if the

securities have not been automatically redeemed prior to maturity and if the Final Index

Value of the Worst Performing Underlying Index is less than its Downside Threshold Level,

you will lose 1% for every 1% decline in the Final Index Value of the Worst Performing Underlying

Index from its Initial Index Value. In this case, the Payment at Maturity will be less than

70.00% of the Stated Principal Amount and could be zero. |

| · | The securities do not

provide for regular interest payments, and you may receive no Contingent Quarterly Coupons

on most or all of the Coupon Payment Dates. The terms of the securities differ from those

of conventional debt securities in that they do not provide for the regular interest payments.

Instead, the securities will pay a Contingent Quarterly Coupon only if the Closing

Level of each Underlying Index on the related Observation Date is at or above

its respective Coupon Barrier Level. If the Closing Level of any Underlying Index

is below its Coupon Barrier Level on each Observation Date, you will not receive any

Contingent Quarterly Coupons over the entire term of the securities, and you will not receive

a positive return on your securities. Generally, this non-payment of the Contingent Quarterly

Coupons coincides with a period of greater risk of principal loss on your securities. If

you do not earn sufficient Contingent Quarterly Coupons over the term of the securities,

the overall return on the securities may be less than the return on a conventional debt security

of ours with comparable maturity. |

| · | The Automatic Early

Redemption feature limits your potential return. If the securities are redeemed, the

Early Redemption Payment is limited to the Stated Principal Amount plus the applicable Contingent

Quarterly Coupon. If the securities are redeemed, you will lose the opportunity to continue

to receive any Contingent Quarterly Coupons from the relevant early redemption date to the

Maturity Date, and the total return on the securities could be minimal. Because of the Automatic

Early Redemption feature, the term of your investment in the securities may be limited to

a period that is shorter than the original term of the securities and may be as short as

approximately 12 months. There is no guarantee that you would be able to reinvest the proceeds

from an investment in the securities at a comparable return for a similar level of risk in

the event the securities are automatically redeemed prior to the Maturity Date. |

| · | Investors will not participate

in any appreciation in the level of any Underlying Index and the return on the securities

will be limited to any Contingent Quarterly Coupons paid on the securities. Payments

on the securities, whether at maturity or upon an early redemption, will not exceed the Stated

Principal Amount plus any Contingent Quarterly Coupons, and any positive return you receive

on the securities will be composed solely of any Contingent Quarterly Coupons. You will not

participate in any appreciation of any Underlying Index. Therefore, if the appreciation of

any Underlying Index exceeds any Contingent Quarterly Coupons paid to you, the securities

will underperform an investment in the securities included in that Underlying Index or the

securities linked to that Underlying Index providing a full participation in the appreciation. |

| · | Higher Contingent Quarterly

Coupon or lower Coupon Barrier Level or Downside Threshold Level are generally associated

with a reference asset with greater expected volatility and therefore can indicate a greater

risk of loss. “Volatility” refers to the frequency and magnitude of changes

in the value of a reference asset. The greater the expected volatility with respect to a

reference asset on the Pricing Date, the higher the expectation as of the Pricing Date that

the value of that reference asset could close below its Downside Threshold Level on the final

Observation Date, indicating a higher expected risk of loss on the securities. This greater

expected risk will generally be reflected in a higher Contingent Quarterly Coupon than the

yield payable on our conventional debt securities with a similar maturity, or in more favorable

terms (such as a lower Coupon Barrier Level or Downside Threshold Level or a higher Contingent

Quarterly Coupon) than for similar securities linked to the performance of a reference asset

with a lower expected volatility as of the Pricing Date. You should therefore understand

that a relatively higher Contingent Quarterly Coupon may indicate an increased risk of loss.

Further, a relatively lower Coupon Barrier Level or Downside Threshold Level may not necessarily

indicate that the securities have a greater likelihood of payments of Contingent Quarterly

Coupons or a repayment of principal at maturity. The volatility of an Underlying Index can

change significantly over the term of the securities. The level of an Underlying Index could

fall sharply, which could result in few or no payment of Contingent Quarterly Coupons during

the term of the securities and a significant or even complete loss of principal at maturity. |

| · | The payments on the

securities are based only on the Closing Levels of the Underlying Indices on the Observation

Dates. The payments on the securities will be based on the Closing Levels of the Underlying

Indices on the Observation Dates, including the final Observation Date. Therefore, for example,

if the Closing Level of any Underlying Index has declined as of each Observation Date below

its Initial Index Value or its Coupon Barrier Level, as applicable, the securities will not

be redeemed and the Contingent Quarterly Coupons will not be payable during the term of the

securities. |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Similarly, if the Final Index Value of any Underlying Index

has declined as of the final Observation Date below its Downside Threshold Level, the Payment at Maturity may be significantly less than

it would otherwise have been had the Payment at Maturity been linked to the Closing Levels of the Underlying Indices other than on the

final Observation Date. Although the actual level of an Underlying Index at other times during the term of the securities may be higher

than its Closing Levels on the Observation Dates, the payments on the securities will not benefit from the Closing Level of any Underlying

Index at any time other than the Observation Dates.

| · | You

are exposed to the price risk of each Underlying Index, with respect to both the Contingent

Quarterly Coupons, if any, and the Payment at Maturity, if any. Your return on the securities

is not linked to a basket consisting of the Underlying Indices. Rather, it will be contingent

upon the independent performance of each Underlying Index. Unlike an instrument with a return

linked to a basket of underlying assets, in which risk is mitigated and diversified among

all the components of the basket, you will be exposed to the risks related to each Underlying

Index. Poor performance by any Underlying Index over the term of the securities may

negatively affect your return and will not be offset or mitigated by any positive performance

by the other Underlying Indices. To receive any Contingent Quarterly Coupons, each Underlying

Index must close at or above its respective Coupon Barrier Level on the applicable Observation

Date. In addition, if any Underlying Index has

declined below its respective Downside Threshold Level as of the final Observation Date,

you will be fully exposed to the decline in the Worst Performing Underlying Index

over the term of the securities on a 1-to-1 basis, even if the other Underlying Indices have

appreciated or not declined as much. Under this scenario, the value of any such payment will

be less than 70.00% of the Stated Principal Amount and could be zero. Accordingly, your investment

is subject to the price risk of each Underlying Index. |

| · | Because

the securities are linked to the performance of the Worst Performing Underlying Index, you

are exposed to greater risks of receiving no Contingent Quarterly Coupons and sustaining

a significant loss on your investment than if the securities were linked to just one index.

The risk that you will not receive any Contingent Quarterly Coupons, or that you will

suffer a significant loss on your investment, is greater if you invest in the securities

as opposed to substantially similar securities that are linked to the performance of just

one Underlying Index. With three Underlying Indices, it is more likely that any Underlying

Index will close below its Coupon Barrier Level on an Observation Date, or below its Downside

Threshold Level on the final Observation Date, than if the securities were linked to only

one Underlying Index. Therefore, it is more likely that you will not receive any Contingent

Quarterly Coupons during the terms of the securities and that you will suffer a significant

loss on your investment at maturity. In addition, because each Underlying Index must close

above its Initial Index Value on an Observation Date in order for the securities to be called

prior to maturity, the securities are less likely to be called on any early redemption date

than if the securities were linked to just one Underlying Index. |

Risks Relating to the Underlying Indices

| · | The

securities are subject to small-capitalization risk. The RTY Index tracks companies that

may be considered small-capitalization companies. These companies often have greater stock

price volatility, lower trading volume and less liquidity than large-capitalization companies

and therefore, the relevant index level may be more volatile than an investment in stocks

issued by larger companies. Stock prices of small-capitalization companies may also be more

vulnerable than those of larger companies to adverse business and economic developments,

and the stocks of small-capitalization companies may be thinly traded, making it difficult

for the RTY Index to track them. In addition, small-capitalization companies are often less

stable financially than large-capitalization companies and may depend on a small number of

key personnel, making them more vulnerable to loss of personnel. Small-capitalization companies

are often subject to less analyst coverage and may be in early, and less predictable, periods

of their corporate existences. These companies tend to have smaller revenues, less diverse

product lines, smaller shares of their product or service markets, fewer financial resources

and competitive strengths than large-capitalization companies, and are more susceptible to

adverse developments related to their products. All these factors may adversely affect the

level of the RTY Index and consequently, the return on the securities. |

| · | There

are risks associated with investments in securities linked to the value of non-U.S. equity

securities. Some of the equity securities composing the NDX Index are issued by non-U.S.

companies. Investments in securities linked to the value of such non-U.S. equity securities,

such as the securities, involve risks associated with the home countries of the issuers of

those non-U.S. equity securities. The prices of securities in non-U.S. markets may be affected

by political, economic, financial and social factors in those countries or global regions,

including changes in government, economic and fiscal policies and currency exchange laws. |

| · | Governmental

regulatory actions, such as sanctions, could adversely affect your investment in the securities.

Governmental regulatory actions, including, without limitation, sanctions-related actions

by the U.S. or a foreign government, could prohibit or otherwise restrict persons from holding

the securities or any securities included in an Underlying Index, or engaging in transactions

therein, and any such action could adversely affect the level of an Underlying Index or the

securities. These regulatory actions could result in restrictions on the securities and could

result in the loss of a significant portion or all of your initial investment in the securities,

including if you are forced to divest the securities due to the government mandates, especially

if such divestment must be made at a time when the value of the securities has declined. |

| · | Adjustments

to the Underlying Indices could adversely affect the value of the securities. The publisher

of each Underlying Index can add, delete or substitute the stocks constituting such Underlying

Index, and can make other methodological changes that could change the value of such Underlying

Index. Any of these actions could adversely affect the value of the securities. The publisher

of each Underlying Index may discontinue or suspend calculation or publication of such Underlying

Index at any time. In these |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

circumstances, we, as the calculation agent, will have the

sole discretion to substitute a successor index that is comparable to the discontinued index. We could have an economic interest that

is different than that of investors in the securities insofar as, for example, we are permitted to consider indices that are calculated

and published by us or any of our affiliates. If we determine that there is no appropriate successor index, the determination

of whether a Contingent Quarterly Coupon will be payable on the securities on the applicable Coupon Payment Date, and/or the payout at

maturity on the securities will be an amount based on the closing prices on each date that the value of such Underlying Index is to be

calculated of the stocks underlying such discontinued index at the time of such discontinuance, without rebalancing or substitution,

computed by us in accordance with the formula for and method of calculating such Underlying Index last in effect prior to the discontinuance,

as compared to the Coupon Barrier Level or Downside Threshold Level, as applicable (depending also on the performance of the other Underlying

Indices).

Conflicts of Interest

| · | Certain business, trading

and hedging activities of us and our affiliates may create conflicts with your interests

and could potentially adversely affect the value of the securities. We and our affiliates

may engage in trading and other business activities related to an Underlying Index or any

securities included in an Underlying Index that are not for your account or on your behalf.

We and our affiliates also may issue or underwrite other financial instruments with returns

based upon an Underlying Index. These activities may present a conflict of interest between

your interest in the securities and the interests that we and our affiliates may have in

our or their proprietary accounts, in facilitating transactions, including block trades,

for our or their other customers, and in accounts under our or their management. In addition,

we and our affiliates may publish research, express opinions or provide recommendations that

are inconsistent with investing in or holding the securities, and which may be revised at

any time without notice to you. Any such research, opinions or recommendations could adversely

affect the level of an Underlying Index, and therefore, the market value of the securities.

These trading and other business activities, if they adversely affect the level of an Underlying

Index or secondary trading in your securities, could be adverse to your interests as a beneficial

owner of the securities. |

Moreover, we and our affiliates play a

variety of roles in connection with the issuance of the securities, including hedging our obligations under the securities and making

the assumptions and inputs used to determine the pricing of the securities and the initial estimated value of the securities when the

terms of the securities were set. We expect to hedge our obligations under the securities through CIBCWM, one of our other affiliates,

and/or another unaffiliated counterparty, which may include any dealer from which you purchase the securities. Any of these hedging activities

may adversely affect the level of an Underlying Index and therefore the market value of the securities and the amount you will receive,

if any, on the securities. In connection with such activities, the economic interests of us and our affiliates may be adverse to your

interests as an investor in the securities. Any of these activities may adversely affect the value of the securities. In addition, because

hedging our obligations entails risk and may be influenced by market forces beyond our control, this hedging activity may result in a

profit that is more or less than expected, or it may result in a loss. We, one or more of our affiliates or any unaffiliated counterparty

will retain any profits realized in hedging our obligations under the securities even if investors do not receive a favorable investment

return under the terms of the securities or in any secondary market transaction. Any profit in connection with such hedging activities

will be in addition to any other compensation that we, our affiliates or any unaffiliated counterparty receive for the sale of the securities,

which creates an additional incentive to sell the securities to you. We, our affiliates or any unaffiliated counterparty will have no

obligation to take, refrain from taking or cease taking any action with respect to these transactions based on the potential effect on

an investor in the securities.

| · | There are potential

conflicts of interest between you and the calculation agent. The calculation agent will

determine, among other things, the amount of payments on the securities. The calculation

agent will exercise its judgment when performing its functions. For example, the calculation

agent will determine whether a Market Disruption Event has occurred on an Observation Date

with respect to any Underlying Index, and determine the level of an Underlying Index if a

scheduled Observation Date is postponed to the last possible day for that Underlying Index.

See “Certain Terms of the Notes—Valuation Dates—For Notes Where the Reference

Asset Consists of Multiple Indices” in the underlying supplement. These determinations

may, in turn, depend on the calculation agent’s judgment as to whether the event has

materially interfered with our ability or the ability of one of our affiliates to unwind

our hedge positions. The calculation agent will be required to carry out its duties in good

faith and use its reasonable judgment. However, because we will be the calculation agent,

potential conflicts of interest could arise. None of us, CIBCWM or any of our other affiliates

will have any obligation to consider your interests as a holder of the securities in taking

any action that might affect the value of your securities. |

General Risks

| · | Payments on the securities

are subject to our credit risk, and actual or perceived changes in our creditworthiness are

expected to affect the value of the securities. The securities are our senior unsecured

debt obligations and are not, either directly or indirectly, an obligation of any third party.

As further described in the accompanying prospectus and prospectus supplement, the securities

will rank on par with all of our other unsecured and unsubordinated debt obligations, except

such obligations as may be preferred by operation of law. Any payments to be made on the

securities depend on our ability to satisfy our obligations as they come due. As a result,

the actual and perceived creditworthiness of us may affect the market value of the securities

and, in the event we were to default on our obligations, you may not receive the amounts

owed to you under the terms of the securities. If we default on our obligations under the

securities, your investment would be at risk and you could lose some or all of your investment.

See “Description of Senior Debt Securities—Events of Default” in the accompanying

prospectus. |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

| · | The Bank’s initial

estimated value of the securities is lower than the initial issue price (price to public)

of the securities. The initial issue price of the securities exceeds the Bank’s

initial estimated value because costs associated with selling and structuring the securities,

as well as hedging the securities, are included in the initial issue price of the securities.

See “Additional Information About the Securities—The Bank’s Estimated Value

of the Securities” beginning on page 25 of this pricing supplement. |

| · | The Bank’s initial

estimated value does not represent future values of the securities and may differ from others’

estimates. The Bank’s initial estimated value of the securities is only an estimate,

which was determined by reference to the Bank’s internal pricing models when the terms

of the securities were set. This estimated value was based on market conditions and other

relevant factors existing at that time, the Bank’s internal funding rate on the Pricing

Date and the Bank’s assumptions about market parameters, which can include volatility,

dividend rates, interest rates and other factors. Different pricing models and assumptions

could provide valuations for the securities that are greater or less than the Bank’s

initial estimated value. In addition, market conditions and other relevant factors in the

future may change, and any assumptions may prove to be incorrect. On future dates, the market

value of the securities could change significantly based on, among other things, changes

in market conditions, including the levels of the Underlying Indices, the Bank’s creditworthiness,

interest rate movements and other relevant factors, which may impact the price at which CIBCWM

or any other party would be willing to buy the securities from you in any secondary market

transactions. The Bank’s initial estimated value does not represent a minimum price

at which CIBCWM or any other party would be willing to buy the securities in any secondary

market (if any exists) at any time. See “Additional Information About the Securities—The

Bank’s Estimated Value of the Securities” beginning on page 25 of this pricing

supplement. |

| · | The Bank’s initial

estimated value of the securities was not determined by reference to credit spreads for our

conventional fixed-rate debt. The internal funding rate used in the determination of

the Bank’s initial estimated value of the securities generally represents a discount

from the credit spreads for our conventional fixed-rate debt. The discount is based on, among

other things, our view of the funding value of the securities as well as the higher issuance,

operational and ongoing liability management costs of the securities in comparison to those

costs for our conventional fixed-rate debt. If the Bank were to have used the interest rate

implied by our conventional fixed-rate debt, we would expect the economic terms of the securities

to be more favorable to you. Consequently, our use of an internal funding rate for market-linked

securities had an adverse effect on the economic terms of the securities and the initial

estimated value of the securities on the Pricing Date, and could have an adverse effect on

any secondary market prices of the securities. See “Additional Information About the

Securities—The Bank’s Estimated Value of the Securities” beginning on page

25 of this pricing supplement. |

| · | If CIBCWM were to repurchase

your securities after the Original Issue Date, the price may be higher than the then-current

estimated value of the securities for a limited time period. While CIBCWM may make markets

in the securities, it is under no obligation to do so and may discontinue any market-making

activities at any time without notice. The price that it makes available from time to time

after the Original Issue Date at which it would be willing to repurchase the securities will

generally reflect its estimate of their value. That estimated value will be based upon a

variety of factors, including then prevailing market conditions, our creditworthiness and

transaction costs. However, for a period of approximately 12 months after the Pricing Date,

the price at which CIBCWM may repurchase the securities is expected to be higher than their

estimated value at that time. This is because, at the beginning of this period, that price

will not include certain costs that were included in the initial issue price, particularly

our hedging costs and profits. As the period continues, these costs are expected to be gradually

included in the price that CIBCWM would be willing to pay, and the difference between that

price and CIBCWM’s estimate of the value of the securities will decrease over time

until the end of this period. After this period, if CIBCWM continues to make a market in

the securities, the prices that it would pay for them are expected to reflect its estimated

value, as well as customary bid-ask spreads for similar trades. In addition, the value of

the securities shown on your account statement may not be identical to the price at which

CIBCWM would be willing to purchase the securities at that time, and could be lower than

CIBCWM’s price. |

| · | Economic and market

factors may adversely affect the terms and market price of the securities prior to maturity

or early redemption. Because structured notes, including the securities, can be thought

of as having a debt and derivative component, factors that influence the values of debt instruments

and options and other derivatives will also affect the terms and features of the securities

at issuance and the market price of the securities prior to maturity or early redemption.

These factors include the levels of the Underlying Indices; the volatility of the Underlying

Indices; the dividend rates paid on the securities included in an Underlying Index; the time

remaining to the maturity or early redemption of the securities; interest rates in the markets

in general; geopolitical conditions and economic, financial, political, regulatory, judicial

or other events; and the creditworthiness of CIBC. These and other factors are unpredictable

and interrelated and may offset or magnify each other. |

| · | The securities will

not be listed on any securities exchange and we do not expect a trading market for the securities

to develop. The securities will not be listed on any securities exchange. Although CIBCWM

and/or its affiliates may purchase the securities from holders, they are not obligated to

do so and are not required to make a market for the securities. There can be no assurance

that a secondary market will develop for the securities. Because we do not expect that any

market makers will participate in a secondary market for the securities, the price at which

you may be able to sell your securities is likely to depend on the price, if any, at which

CIBCWM and/or its affiliates are willing to buy your securities. |

If a secondary market does exist, it may be limited. Accordingly,

there may be a limited number of buyers if you decide to sell your securities prior to maturity or early redemption. This may affect

the price you receive upon such sale. Consequently, you should be willing to hold the securities to maturity or early redemption.

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Tax Risks

| · | The tax treatment of

the securities is uncertain. Significant aspects of the tax treatment of the securities

are uncertain. You should consult your tax advisor about your own tax situation. See “Additional

Information About the Securities — United States Federal Income Tax Considerations”

and “— Certain Canadian Federal Income Tax Considerations” in this pricing

supplement, “Material U.S. Federal Income Tax Consequences” in the underlying

supplement and “Material Income Tax Consequences—Canadian Taxation” in

the prospectus. |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Information About the Underlying Indices

The information below is a brief description of each Underlying Index.

We have derived the following information from publicly available documents. We have not independently verified the accuracy or completeness

of the following information. In addition, information about each Underlying Index may be obtained from other sources, including, but

not limited to, its sponsor’s website. We are not incorporating by reference into this pricing supplement any website or any materials

it includes. None of us, CIBCWM or any of our other affiliates makes any representation that such publicly available information regarding

any Underlying Index is accurate or complete.

S&P 500® Index

The S&P 500® Index (Bloomberg ticker: “SPX

<Index>”) is calculated, maintained and published by S&P Dow Jones Indices LLC. The SPX Index consists of stocks of 500

companies selected to provide a performance benchmark for the U.S. equity markets. See “Index Descriptions—The S&P U.S.

Indices” beginning on page S-43 of the accompanying underlying supplement for additional information about the SPX Index.

Information as of market close on May 8, 2024:

| |

Bloomberg

Ticker Symbol: SPX |

| |

Current

Index Value: 17,596.27 |

| |

Current Index Value: 5,187.67 |

| |

52 Weeks Ago: 4,119.17 |

| |

52 Week High (on March 28, 2024): 5,254.35 |

| |

52 Week Low (on May 16, 2023): 4,109.90 |

Nasdaq-100 Index®

This Nasdaq-100 Index® (Bloomberg ticker: “NDX

<Index>“) is calculated, maintained and published by Nasdaq, Inc. The NDX Index includes 100 of the largest domestic and international

non-financial companies listed on The Nasdaq Stock Market based on market capitalization. The NDX Index reflects companies across major

industry groups including computer hardware and software, telecommunications, retail/wholesale trade and biotechnology. See “Index

Descriptions—The Nasdaq-100 Index®” beginning on page S-26 of the accompanying underlying supplement for additional

information about the NDX Index.

Information as of market close on May 8,

2024:

| |

Bloomberg Ticker Symbol: NDX |

| |

Current Index Value: 18,085.01 |

| |

52 Weeks Ago: 13,201.11 |

| |

52 Week High (on March 22, 2024): 18,339.44 |

| |

52 Week Low (on May 9, 2023): 13,201.11 |

Russell 2000® Index

The Russell 2000® Index (Bloomberg ticker: “RTY

<Index>”) is calculated, maintained and published by FTSE Russell. The RTY Index is designed to track the performance of the

small capitalization segment of the U.S. equity market. The RTY Index is a subset of the Russell 3000® Index and represents

approximately 10% of the total market capitalization of that index. The RTY Index includes approximately 2,000 of the smallest securities

in the U.S. equity market. See “Index Descriptions—The Russell 2000® Index” beginning on page S-31 of

the accompanying underlying supplement for additional information about the RTY Index.

Information as of market close on May 8,

2024:

| |

Bloomberg

Ticker Symbol: RTY |

| |

Current Index Value: 2,055.135 |

| |

52 Weeks

Ago: 1,749.677

|

| |

52 Week High (on March 28, 2024): 2,124.547 |

| |

52 Week Low (on October 27, 2023): 1,636.938 |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

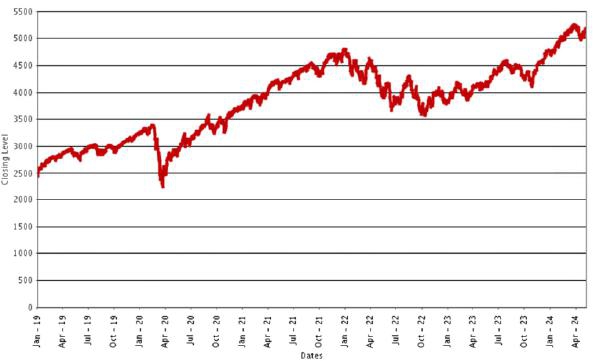

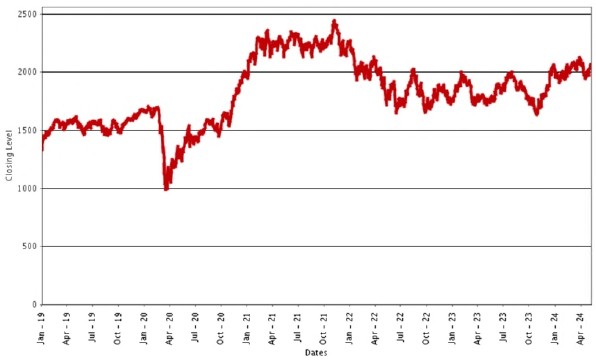

Historical Performance of the Underlying Indices

The following graphs set forth the daily Closing Levels of

each Underlying Index for the period from January 1, 2019 through May 8, 2024. The tables below set forth the published high and low Closing

Levels, as well as end-of-quarter Closing Levels, of each Underlying Index for each quarter in the same period. We obtained the information

in the graphs and the tables below from Bloomberg L.P. (“Bloomberg”) without independent verification. Each Underlying Index

has at times experienced periods of high volatility, and the historical performance of any Underlying Index should not be taken as an

indication of its future performance. No assurance can be given as to the level of any Underlying Index at any time during the term of

the securities, including the Observation Dates. We cannot give you assurance that the performance of any Underlying Index will result

in the return of any of your investment.

S&P 500® Index

|

SPX Index Daily Closing Levels

January 1, 2019 to May 8, 2024 |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

| S&P 500® Index |

High |

Low |

Period End |

| 2019 |

|

|

|

| First Quarter |

2,854.88 |

2,447.89 |

2,834.40 |

| Second Quarter |

2,954.18 |

2,744.45 |

2,941.76 |

| Third Quarter |

3,025.86 |

2,840.60 |

2,976.74 |

| Fourth Quarter |

3,240.02 |

2,887.61 |

3,230.78 |

| 2020 |

|

|

|

| First Quarter |

3,386.15 |

2,237.40 |

2,584.59 |

| Second Quarter |

3,232.39 |

2,470.50 |

3,100.29 |

| Third Quarter |

3,580.84 |

3,115.86 |

3,363.00 |

| Fourth Quarter |

3,756.07 |

3,269.96 |

3,756.07 |

| 2021 |

|

|

|

| First Quarter |

3,974.54 |

3,700.65 |

3,972.89 |

| Second Quarter |

4,297.50 |

4,019.87 |

4,297.50 |

| Third Quarter |

4,536.95 |

4,258.49 |

4,307.54 |

| Fourth Quarter |

4,793.06 |

4,300.46 |

4,766.18 |

| 2022 |

|

|

|

| First Quarter |

4,796.56 |

4,170.70 |

4,530.41 |

| Second Quarter |

4,582.64 |

3,666.77 |

3,785.38 |

| Third Quarter |

4,305.20 |

3,585.62 |

3,585.62 |

| Fourth Quarter |

4,080.11 |

3,577.03 |

3,839.50 |

| 2023 |

|

|

|

| First Quarter |

4,179.76 |

3,808.1 |

4,109.31 |

| Second Quarter |

4,450.38 |

4,055.99 |

4,450.38 |

| Third Quarter |

4,588.96 |

4,273.53 |

4,288.05 |

| Fourth Quarter |

4,783.35 |

4,117.37 |

4,769.83 |

| 2024 |

|

|

|

| First Quarter |

5,254.35 |

4,688.68 |

5,254.35 |

| Second Quarter (through May 8, 2024) |

5,243.77 |

4,967.23 |

5,187.67 |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Nasdaq-100 Index®

|

NDX Index Daily Closing Levels

January 1, 2019 to May 8, 2024 |

| |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

| Nasdaq-100 Index® |

High |

Low |

Period End |

| 2019 |

|

|

|

| First Quarter |

7,493.27 |

6,147.13 |

7,378.77 |

| Second Quarter |

7,845.73 |

6,978.02 |

7,671.08 |

| Third Quarter |

8,016.95 |

7,415.69 |

7,749.45 |

| Fourth Quarter |

8,778.31 |

7,550.79 |

8,733.07 |

| 2020 |

|

|

|

| First Quarter |

9,718.73 |

6,994.29 |

7,813.50 |

| Second Quarter |

10,209.82 |

7,486.29 |

10,156.85 |

| Third Quarter |

12,420.54 |

10,279.25 |

11,418.06 |

| Fourth Quarter |

12,888.28 |

11,052.95 |

12,888.28 |

| 2021 |

|

|

|

| First Quarter |

13,807.70 |

12,299.08 |

13,091.44 |

| Second Quarter |

14,572.75 |

13,001.63 |

14,554.80 |

| Third Quarter |

15,675.76 |

14,549.09 |

14,689.62 |

| Fourth Quarter |

16,573.34 |

14,472.12 |

16,320.08 |

| 2022 |

|

|

|

| First Quarter |

16,501.77 |

13,046.64 |

14,838.49 |

| Second Quarter |

15,159.58 |

11,127.57 |

11,503.72 |

| Third Quarter |

13,667.18 |

10,971.22 |

10,971.22 |

| Fourth Quarter |

12,041.89 |

10,679.34 |

10,939.76 |

| 2023 |

|

|

|

| First Quarter |

13,181.35 |

10,741.22 |

13,181.35 |

| Second Quarter |

15,185.48 |

12,725.11 |

15,179.21 |

| Third Quarter |

15,841.35 |

14,545.83 |

14,715.24 |

| Fourth Quarter |

16,906.80 |

14,109.57 |

16,825.93 |

| 2024 |

|

|

|

| First Quarter |

18,339.44 |

16,282.01 |

18,254.69 |

| Second Quarter (through May 8, 2024) |

18,307.98 |

17,037.65 |

18,085.01 |

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

Russell 2000® Index

RTY Index Daily Closing Levels

January 1, 2019 to May 8, 2024 |

|

|

Contingent

Income Auto-Callable Securities due May 13, 2027

Based

on the Worst Performing of the S&P 500® Index, the Nasdaq-100 Index® and the Russell 2000®

Index

Principal

at Risk Securities

| Russell 2000® Index |

High |

Low |

Period End |

| 2019 |

|

|

|

| First Quarter |

1,590.062 |

1,330.831 |

1,539.739 |

| Second Quarter |

1,614.976 |

1,465.487 |

1,566.572 |

| Third Quarter |

1,585.599 |

1,456.039 |

1,523.373 |

| Fourth Quarter |

1,678.010 |

1,472.598 |

1,668.469 |

| 2020 |

|

|

|

| First Quarter |

1,705.215 |

991.160 |

1,153.103 |

| Second Quarter |

1,536.895 |

1,052.053 |

1,441.365 |

| Third Quarter |

1,592.287 |

1,398.920 |

1,507.692 |

| Fourth Quarter |

2,007.104 |

1,531.202 |

1,974.855 |

| 2021 |

|

|

|

| First Quarter |

2,360.168 |

1,945.914 |

2,220.519 |

| Second Quarter |

2,343.758 |

2,135.139 |

2,310.549 |

| Third Quarter |

2,329.359 |

2,130.680 |

2,204.372 |

| Fourth Quarter |

2,442.742 |

2,139.875 |

2,245.313 |

| 2022 |

|

|

|

| First Quarter |

2,272.557 |