UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23247

(Investment Company Act File Number)

XAI Octagon Floating Rate & Alternative

Income Term Trust

(Exact Name of Registrant as Specified in Charter)

321 North Clark Street, Suite 2430

Chicago, IL 60654

(Address of Principal Executive Offices)

Benjamin D. McCulloch, Esq.

XA Investments LLC

321 North Clark Street, Suite 2430

Chicago, IL 60654

(Name and Address of Agent for Service)

(312) 374-6930

(Registrant’s Telephone Number)

Date of Fiscal Year End: September 30

Date of Reporting Period: September 30, 2023

Item 1. Reports to Stockholders.

| TABLE OF CONTENTS |

|

| |

|

| Shareholder Letter |

3 |

| Questions & Answers |

4 |

| Trust Portfolio Information |

9 |

| Schedule of Investments |

11 |

| Statement of Assets and Liabilities |

24 |

| Statement of Operations |

25 |

| Statements of Changes in Net Assets |

26 |

| Statement of Cash Flows |

27 |

| Financial Highlights |

28 |

| Notes to Financial Statements |

30 |

| Report of Independent Registered Public Accounting Firm |

41 |

| Certain Changes Occurring During the Prior Fiscal Year |

42 |

| Fees and Expenses |

43 |

| Market and Net Asset Value Information |

44 |

| Investment Objective and Policies |

45 |

| Risks |

55 |

| Use of Leverage |

74 |

| Limited Term and Eligible Tender Offer |

76 |

| Dividend Reinvestment Plan |

77 |

| Net Asset Value |

78 |

| Management of the Trust |

79 |

| Additional Information |

83 |

| Approval of Advisory Agreements |

86 |

XAI Octagon Floating Rate

& Alternative Income Term Trust

SHAREHOLDER

LETTER

September 30,

2023 (Unaudited)

Dear Shareholder:

We thank you for your investment

in the XAI Octagon Floating Rate & Alternative Income Term Trust (the “Trust”). This report covers the fiscal year ended

September 30, 2023 (the “Period”). During the Period, we observed elevated, but tapering inflation levels, continued rate

hikes by the U.S. Federal Reserve (the “Fed”), and regional bank failures. Despite these headwinds, economic data have indicated

a resilient U.S. economy, as demonstrated by strong corporate earnings and employment. The Consumer Price Index started the Period at

8.2% and ended the Period at 3.7%.1 The Fed raised interest rates six times during

the Period for a cumulative increase of 2.25%. These dynamics are important to consider as the Trust primarily invests in floating-rate

securities including loans, collateralized loan obligation (“CLO”) debt tranches and CLO equity.

Amidst the backdrop of

rising interest rates, the loan market returned 6.48% over the first half of 2023—the strongest period of first half performance

since 2009— and the rally continued in the third quarter of 2023.2 Broadly,

loans’ strong performance over the Period has been driven by rising rates, economic data indicating resilient growth, better-than-expected

corporate earnings results, and higher secondary prices. The trailing 12-month

loan default rate rose to 1.75% by July month-end but has since reversed course. September marked a default-free month for the Morningstar

LSTA US Leveraged Loan Index for the first time this year.3

There has been a steady pace of CLO

origination throughout 2023, precipitating persistent bids for loans and broad tightening in CLO liability spreads, as compared to late-2022

levels. With meaningful performance dispersion across both the CLO and underlying loan markets, we believe it is important to focus on

fundamentally strong CLOs that offer compelling yields and the potential for price appreciation.

For the Period, the S&P

500 Index, the Bloomberg Barclays U.S. High Yield 1% Issuer Capped Index and the Trust’s benchmark, the Morningstar LSTA US Leveraged

Loan 100 Index, generated total returns of 21.62%, 10.31%, and 13.74%, respectively.4

The Trust’s net asset

value (“NAV”) increased during the Period by 4.38% from $6.39 per common share to $6.67 per common share as of September

30, 2023, reflecting valuation increases for the Trust’s investments.

During the Period, the Trust declared

monthly distributions totaling an aggregated $0.936 per common share. The monthly distribution of $0.085 per common share declared on

September 1, 2023 represented an annualized distribution rate of 14.68% based on the Trust’s closing market price of $6.95 per common

share on September 30, 2023.

The market price per common share

of $6.95 on September 30, 2023 represented a 4.20% premium to NAV of $6.67 per common share. During the Period, the Trust’s common

shares traded on average at a 2.14% premium to NAV. From the Trust’s IPO on September 27, 2017 through September 30, 2023 the Trust’s

common shares have traded on average at a 3.30% premium to NAV.

We continue to seek operational

scale by increasing the Trust’s common assets. During the Period, the Trust issued an additional 7,247,127 common shares pursuant to an

at-the-market

(“ATM”) offering program, resulting in $48,265,936 of net proceeds to the Trust which may result in incremental expense efficiencies

for shareholders. In addition to the ATM program, $10,000,000 of the Trust’s 6.00% Series 2029 Convertible Preferred Shares were

converted to common shares in three separate conversions at respective conversion prices above NAV, resulting in the issuance of an additional

1,579,188 common shares.

On October 26, 2023, the Trust announced

that the Trust’s Board of Trustees (the “Board”) has unanimously approved a proposal to eliminate the Trust’s

termination date of December 31, 2029. The proposal, if approved by shareholders, will amend the Trust’s Second Amended and Restated

Declaration of Trust and make the Trust perpetual (the “Term Amendment”). The Board also approved a new sub-advisory agreement

among the Trust, the investment adviser and the Trust’s sub-adviser, to become effective upon the closing of a transaction by the

sub-adviser’s parent company that will result in the automatic termination of the current sub-advisory agreement. The terms of the

new sub-advisory agreement are substantially identical to the current sub-advisory agreement. The Term Amendment and the new sub-advisory

agreement (together, the “Proposals”) are subject to approval by the Trust’s shareholders. The Board approved submitting

each Proposal to the Trust’s shareholders for approval at a special meeting of shareholders, to be held on December 19, 2023. Shareholders

of record at the close of business on October 25, 2023 are entitled to vote at the meeting. This

letter and the accompanying shareholder report is not a solicitation of any vote, consent or proxy from any Trust shareholder,

which will be made only pursuant to separate proxy materials filed by the Trust with the Securities and Exchange Commission (“SEC”).

Because the proxy statement contains important information about the Proposals, the Trust’s shareholders are urged to read the proxy

statement and accompanying materials carefully. Shareholders can obtain, free of charge, copies of these documents at the SEC’s

website at www.sec.gov and can obtain copies by calling (800) 431-9645 or by writing the Trust at 321

North Clark Street, Suite 2430, Chicago, Illinois 60654.

We appreciate your investment and

look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the

Trust’s website at www.xainvestments.com/XFLT.

Sincerely,

Kimberly Flynn

Managing Director

XA Investments LLC

November 15, 2023

| 1 |

Source: U.S. Bureau of Labor Statistics, “12-month percentage change, Consumer Price Index, all items, not seasonally adjusted.” |

| 2 |

Sources: PitchBook

Leveraged Commentary & Data (“PitchBook LCD”), Morningstar LSTA (“Loan Syndications and Trading Association”)

US Leveraged Loan Index. |

| 3 |

Source: PitchBook LCD, “In first damage-free month of 2023, loan default rate falls to 1.27%,” (October 2, 2023). |

| 4 |

Source: Bloomberg. See “Index Definitions” in Questions & Answers for additional information. |

XAI Octagon Floating Rate & Alternative Income Term

Trust

QUESTIONS & ANSWERS

September 30, 2023 (Unaudited)

XA Investments LLC (“XAI”)

serves as the investment adviser to the XAI Octagon Floating Rate & Alternative Income Term Trust (the “Trust”). Octagon

Credit Investors, LLC (“Octagon”) serves as the Trust’s investment sub-adviser and is responsible for the management

of the Trust’s portfolio of investments.

Gretchen M. Lam, Senior Portfolio

Manager at Octagon and a member of Octagon’s Investment Committee serves as lead portfolio manager of Trust. Ms. Lam is supported

by a team of Octagon investment professionals in the day-to-day management of the Trust’s portfolio, including the following members

of Octagon’s Investment Committee: Andrew D. Gordon (Octagon’s co-founder and Chief Executive Officer), Michael B. Nechamkin

(Chief Investment Officer and Senior Portfolio Manager), Lauren B. Law (Portfolio Manager), and Sean M. Gleason (Portfolio Manager). In

addition, Maegan Gallagher (Head of Trading and Capital Markets) is a member of the Octagon Investment Committee. Octagon has announced

that Ms. Lam will succeed Mr. Gordon as Chief Executive Officer of Octagon, effective January 1, 2024. At that time, Mr. Gordon will assume

the role of Executive Chair of the Board of Managers and will also continue to serve as a member of the firm’s Investment Committee.

What is the Trust’s investment

objective and how is it pursued?

The Trust’s investment objective

is to seek attractive total return with an emphasis on income generation across multiple stages of the credit cycle. The Trust seeks to

achieve its investment objective by investing in a dynamically managed portfolio of opportunities primarily within the private credit

markets. The Trust invests primarily in below investment grade credit instruments that are regarded as having predominantly speculative

characteristics with respect to capacity to pay interest and to repay principal. The Trust may invest without limitation in credit instruments

that are illiquid. Under normal market conditions, the Trust will invest at least 80% of its Managed Assets in floating-rate credit instruments

and other structured credit investments. “Managed Assets” means the total assets of the Trust, including assets attributable

to the Trust’s use of leverage, minus the sum of its accrued liabilities (other than liabilities incurred for the purpose of creating

leverage).

The Trust’s investments may

include (i) structured credit investments, including collateralized loan obligation (“CLO”) debt and subordinated (i.e., residual

or equity) securities; (ii) traditional corporate credit investments, including leveraged loans and high yield bonds; (iii) opportunistic

credit investments, including stressed and distressed credit situations and long/short credit investments; and (iv) other credit-related

instruments.

Leveraged loans are debt obligations

(also commonly referred to as “senior loans” or “floating-rate loans”) issued by a bank to a corporation that

generally holds legal claim to the borrower’s assets above all other debt obligations. Leveraged loans and CLO debt securities have

historically used the one-month LIBOR as an interest rate benchmark, which was phased out on June 30, 2023, although one- three- and six-month

U.S. dollar LIBOR will continue to be published under a representative “synthetic” methodology until September 30, 2024 to

assist in transitioning existing instruments tied to LIBOR to an alternative rate. These “synthetic” rates are not permitted

for use in new products. “LIBOR” stands for London Interbank Offered Rate and was the benchmark rate that most of the world’s

leading banks charged each other for short-term loans. On July 29, 2021, the Alternative Reference Rates Committee, a group of private

market participants formed by the Federal Reserve Board and Federal Bank of New York, formally recommended CME Group’s forward-looking

Term Standard Overnight Financing Rate (“SOFR”) as the replacement rate for LIBOR. New instruments are now being issued with

an alternative rate – typically SOFR. Replacement of LIBOR could adversely affect the market value or liquidity of CLO securities

and/or loans, and pose tangential risk for markets and assets that do not rely directly on LIBOR. There is uncertainty with respect to

replacement of LIBOR with proposed alternative reference rates, and it is possible that different markets might adopt different rates,

resulting in multiple rates at the same time and a potential mismatch between CLO securities and underlying collateral, the effects of

which are uncertain at this time, and could include increased volatility or illiquidity. In addition, operational and technology challenges

during the transition from LIBOR as well as inconsistent communication from issuers could result in delayed investment analyses and reduced

investment opportunities.

CLOs are a type of structured credit

vehicle that typically invest in a diverse portfolio of broadly syndicated leveraged loans. CLOs finance this pool of loans with a capital

structure that consists of debt and equity. CLO debt includes senior and mezzanine debt (collectively, “liabilities”) of a

CLO structure with tranches rated from AAA down to BB or B. Interest earned from the underlying loan collateral pool of a CLO is used

to pay the coupon interest on the CLO liabilities. CLO debt investors earn returns based on spreads above 3-month LIBOR or SOFR, as applicable.

CLO equity represents a residual stake in the CLO structure and is the first loss position in the event of defaults and credit losses.

CLO equity investors receive the excess spread between the CLO assets and liabilities and expenses. CLO equity is junior in priority of

payment and is subject to certain payment restrictions generally set forth in an indenture governing the notes.

The Trust uses leverage to seek to

enhance total return and income. Although leverage may create an opportunity for increased return and income for shareholders, it also

results in additional risks and can magnify the effect of any losses. There is no assurance that the leverage strategy will be successful.

If income and gains on securities purchased with leverage proceeds are greater than the cost of the leverage, common shareholders’

return will be greater than if leverage had not been used. Conversely, if the income or gains from the securities purchased with the proceeds

of leverage are less than the cost of leverage, common shareholders’ return will be less than if leverage had not been used.

Describe the market conditions for

leveraged loans during the fiscal year ended September 30, 2023, and Octagon’s outlook.

Leveraged loans returned

13.05% during the fiscal year ended September 30, 2023 (the “Period”), as measured by the Morningstar LSTA US Leveraged Loan

Index (the “Morningstar LLI”).1 Loans’ strong performance over

the Period was driven by rising LIBOR/SOFR reference rates, economic data indicating resilient growth, better-than-expected corporate

earnings results, and generally supportive technical market factors. Despite fluctuating throughout the first half of 2023 against the

backdrop of rising rates, loan prices trended higher as the Period progressed. After reaching an intra-year peak of 94.71 in early February

(from 92.44 as of December 31, 2022), the average bid price of the Morningstar LLI declined to 92.56 in late March, amid broader market

volatility from bank failures, financial contagion concerns, and monetary tightening. The average bid price of the Morningstar LLI increased

modestly in April before retreating to 92.89 by May month-end amid elevated rate volatility.1

As markets broadly rallied in response to resilient labor market data and hawkish rhetoric from the U.S. Federal Reserve

(the “Fed”) that precipitated a reassessment of Fed policy expectations, the average bid price for the Morningstar LLI rebounded

to 94.24 by June 30, 2023.1

Overall, the loan market

returned 6.48% over the first half of 2023—the strongest period of first half performance since 2009—and the momentum continued

in the third quarter of 2023.1 The loan market returned 3.46% in the third quarter,

reflecting a sustained secondary market rally during which the average Morningstar LLI bid price reached 95.91 on September 18, 2023,

the highest level since May 2022.1 Higher base rates have propelled the floating

rate asset class’s outsized gains, with interest income accounting for 7.18% of the Morningstar LLI’s 10.16% year-to-date

return as of September 30, 2023.1 Notably, leveraged loans are one of the only

major asset classes to produce a positive cumulative return since the U.S. Federal Reserve (the “Fed”) began increasing rates

in March 2022, which we believe underscores loans’ ability to outperform in a rising rate environment.2

XAI Octagon Floating Rate & Alternative Income Term

Trust

QUESTIONS & ANSWERS

September 30, 2023 (Continued) (Unaudited)

In the wake of a flight-to-quality

that drove significant performance dispersion in the loan market throughout 2022, lower-rated

loans have outperformed their higher quality cohorts over the course of 2023.1

Year-to-date as of September 30, 2023, CCC-rated loans have returned 15.03%, outpacing B (+11.31%) and BB-rated loans (+7.27%).1

In the context of firmer market conditions, the share of performing loans priced below 80 in the Morningstar LLI (as

opposed to the par amount of 100) has gradually declined year-to-date amid firmer market conditions. As of September 2023, loans priced

below 80 accounted for 4.4% of the total outstanding loans in the Morningstar LLI, which is lower than the 7.4% observed at the end of

2022.1

Loan downgrades have outpaced

upgrades throughout 2023, thereby contributing to increased performance dispersion among loan borrowers. The pace of ratings downgrades

has recently eased; the rolling three-month downgrade-to-upgrade ratio, which is calculated as the number of loans downgraded divided

by the number of loans upgraded, was 1.73x as of September 30, 2023—the lowest level in 14 months.3

After a default-free fourth quarter 2022, eight loan

issuers defaulted in the first quarter of 2023. As a result, the trailing 12-month

(“LTM”) default rate of the Morningstar LLI increased to 1.32% as of March 31, 2023, up from 0.72% as of December 31, 2022.3

Further, the LTM loan default rate rose to 1.75% by July month-end but has since reversed course. September marked a default-free month

for the Morningstar LLI for the first time this year.3 As of September 30, 2023,

the LTM default rate of the Morningstar LLI was 1.27%, nearly 0.50% lower than July’s peak of 1.75%, and comfortably inside the

low end of the range of 2023 default rate forecasts of 2-6%.3 Looking ahead, we

expect loan defaults to increase from the September 2023 level. However, based on our assessment of the current loan borrower universe

and broader market dynamics, we do not foresee a near-term spike in default rates.

Interest coverage and leverage

ratios for publicly reporting borrowers within the Morningstar LLI have remained healthy by historical standards.4

Still, we expect a higher-for-longer interest rate environment to pressure credit fundamentals—especially interest

coverage ratios—though many borrowers entered the current Fed rate hike cycle with very strong interest coverage levels that should

buffer the impact of declining ratios. Our internal analyses indicate that certain borrowers may be better positioned than others due

to interest rate hedging and fixed rate debt in their capital structures. We believe continued performance dispersion among issuers underscores

the importance of prudent credit selection and active portfolio management.

The primary loan market

started off strong in 2023, before activity stalled in March amid turmoil in the banking sector. Of the $52.4 billion of institutional

loans issued in the first quarter of 2023, $41.8 billion were priced in January and February.5

New issuance remained relatively subdued in the second quarter ($50.1 billion total primary institutional loan volume5)

but increased in the third quarter of 2023, amid improving risk sentiment and a rally in the secondary market. Third quarter new issue

loan volume of $76.3 billion represented a 51% quarter-over-quarter increase, bringing total year-to-date primary issuance to $179.0

billion as of September 30, 2023.5 While M&A-backed loan volume sequentially

increased in each quarter of 2023, refinancing activity accounted for the lion’s share of year-to-date loan supply through September

30, 2023 (nearly 60%, or $105.3 billion5), as borrowers took advantage of opportunities

to address near-term debt maturities. Inclusive of $61.0 billion of amend-and-extend

transactions executed year-to-date, the amount of loans coming due between 2023-2025

decreased to $143.9 billion as of September 30, 2023, versus $280.4 billion at calendar year-end

2022.6

The steady pace of CLO

origination throughout 2023 precipitated persistent bids for loans and broad tightening in CLO liability spreads compared to late-2022

levels. Year-to-date new US CLO issuance totaled $83.9 billion as of September 30, 2023; in addition to stable institutional demand,

retail loan funds have reported modest net inflows in August and September 2023, following several consecutive months of outflows.5

For the first time all year, in September 2023, loan market supply and demand were nearly balanced.7

The current forward calendar is signaling light new loan issuance in the near-term, which we believe should provide

continued support to the loan market’s favorable technical dynamics.

All-in yields for loans have been

benefiting from higher LIBOR and SOFR base rates; given high levels of current income with price convexity, we believe that loans currently

present a compelling total return opportunity with the potential for mitigated downside volatility. Though we expect credit stress to

remain elevated, we expect relatively balanced market technicals to provide support for loan prices, notwithstanding issuer-specific price

movement driven by earnings results and company outlook.

Describe the current market conditions

for the CLO market and Octagon’s outlook.

In tandem with strong performance

for loans, CLO debt tranches generated healthy returns over the Period that ranged from 9.06% for AAA-rated tranches to 23.48% for BB

tranches, as measured by the J.P. Morgan Collateralized Loan Obligation Index (“CLOIE”).8

CLOs generally performed well in 2022 versus comparably rated assets and have outpaced other comparably rated assets

on a year-to-date basis as of September 30, 2023. Year-to-date as of September 30, 2023, CLO AAA tranches have returned 6.36% versus

-1.43% for AAA-rated corporate bonds8,9; meanwhile, CLO BB tranches have returned 16.02% compared to 4.40% for BB-rated high

yield bonds.8,9 Notably, CLO mezzanine tranches (rated BB and B), which comprise the majority

of the Trust’s CLO debt holdings, have posted the strongest year-to-date performance of credit assets.8,9,10

New CLO issuance has been steady

year-to-date,

despite the challenges of macro headwinds, muted loan supply, and comparatively wide AAA spreads (versus the historical median) amid a

limited CLO AAA investor base. With $83.9 billion of new deals priced year-to-date as of September 30, 2023, primary CLO market activity

is running 22% behind last year’s pace.5 Tightening liability spreads supported a rebound

in CLO refinancing and reset activity in the third quarter of 2023—$9.1 billion of deals were refinanced or reset during the third

quarter versus only $0.4B in the second quarter.6 Meanwhile, secondary CLO trading activity

has remained elevated, reflecting attractive relative value opportunities in the secondary market compared to the primary market (primary

CLO liability spreads have generally lagged secondary spread levels year-to-date). Of the approximately $41.5 billion in year-to-date

US CLO bid wanted in competition volume (as of September 30, 2023), investment grade debt tranches (rated AAA-A)

accounted for 70%.11

Primary CLO spreads tightened

in the first quarter of 2023 from the fourth quarter of 2022, despite marginal widening in spreads in mid-March

2023 from banking sector driven market volatility. The spread basis between larger, top-tier managers and smaller, lower tier managers

widened in the second quarter of 2023 to roughly 0.31%, amid more challenging issuance conditions.12

As the pace of CLO formation picked up in the third quarter, primary liability spreads broadly tightened. The average

AAA coupon for broadly syndicated loan CLOs that priced in the third quarter was SOFR + 1.89%, down from the second quarter average of

SOFR + 1.98%, and the fourth quarter 2022 average spread of SOFR + 2.31%.6

While primary AAA spreads for top-tier

managers narrowed to year-to-date tights (less than SOFR + 1.70%) during the third quarter of 2023,6 spreads have since widened. Year-to-date,

deal origination has been driven by CLO managers’ internal investments/captive equity funds,6 and we expect new CLO issuance will

continue to be focused among higher tier managers, particularly in the context of limited CLO AAA investor demand (which may constrain

new deal issuance over the near-term). Absent an uptick

in new issue loan supply, CLO liability spread compression, or a decline in secondary loan prices, CLO arbitrage is likely to remain challenged.

XAI Octagon Floating Rate & Alternative Income Term

Trust

QUESTIONS & ANSWERS

September 30, 2023 (Continued) (Unaudited)

CLO managers remain focused

on managing portfolio risk in underlying collateral pools amid loan downgrades. The median CCC concentration in US broadly-syndicated

loan (“BSL”) CLO portfolios increased by 1.1% and 3.9% on a trailing three-month and 12-month basis, respectively, as of

September 2023, although many CLO managers have reduced CCC exposure in reinvesting BSL CLOs by 0.4% and 2.1% over the same respective

periods.13 CLO exposure to CCC/Caa-rated assets of more than 7.5% negatively impacts

overcollateralization cushions. Junior overcollateralization ratio test cushions for reinvesting BSL CLOs generally remain healthy at

a median level of 4.6% as of September 30, 2023,13 though overcollateralization

cushions may face pressure amid accelerating rating agency downgrade activity.

For reinvesting CLOs, the

median third quarter 2023 equity distribution was 4.0% of notional value (or roughly 17% annualized), in line with the prior quarter

median and 1.5% higher than the first quarter 2023 median of 2.5%.14 The recent

improvement in quarterly equity payments partially reflects declining three-month/one-month reference rate basis; the basis between

one-month and three-month

SOFR declined roughly 0.60% between November 2022 and July 2023.14 Third quarter

equity distributions reported thus far have been generally in line with the levels from the prior two quarters.15

Though challenges remain, we believe

CLO tranches present compelling investment opportunities, and that the Trust’s portfolio has the potential for further upside. At

current levels, we believe BB-rated CLO tranches (which comprise the majority of the Trust’s CLO debt holdings) are attractive given

double-digit average current yields, and that “higher-for-longer” reference rate expectations should support above-average

returns for CLO tranches over the intermediate term. At the same time, risks remain throughout the corporate credit space, and CLO collateral

portfolios are likely to be challenged by idiosyncratic headwinds, ratings agency downgrades, and increased defaults among loan issuers.

With continued performance dispersion across both the CLO and underlying loan markets, the Trust will endeavor to invest in fundamentally

strong CLOs that offer compelling yields and the potential for price appreciation.

How did the Trust perform for the period?

During the Period, the Trust’s

total return based on market price was 35.05% and total return based on net asset value (“NAV”) was 20.48%. NAV return includes

the deduction of management fees, operating expenses, and all other Trust expenses. All Trust total returns cited whether based on NAV

or market price assume the reinvestment of all distributions. As of September 30, 2023, the Trust’s market price of $6.95 represented

a premium of 4.20% to its NAV of $6.67. The market value of the Trust’s common shares fluctuates from time to time and may be higher

or lower than the Trust’s NAV. Performance data quoted represents past performance. Past performance does not guarantee future results.

Current performance may be lower or higher than the performance data quoted.

What were the distributions over the

period?

During the Period, the Trust increased

its monthly distribution from $0.073 per share to $0.085 per share. The increase in the monthly distribution was declared on May 1, 2023

and remained at this level through the end of the Period. The Trust’s distribution of $0.085 per share declared on September 1,

2023 represented an annualized distribution rate of 14.68% based on the Trust’s closing market price of $6.95 per common share on

September 30, 2023. The Trust’s distribution rate is not constant, and the amount of distributions, when and if declared by the

Trust’s Board of Trustees, is subject to change based on the performance of the Trust.

The Trust intends to pay substantially

all of its net investment income, if any, to common shareholders through monthly distributions and to distribute any net realized long-term

capital gains to common shareholders at least annually. The Trust’s net investment income and capital gain can vary significantly

over time; however, the Trust seeks to maintain stable common share monthly distributions over time. There is no assurance the Trust will

pay regular monthly distributions or that it will do so at a particular rate. Distributions may be paid by the Trust from any permitted

source and, from time to time, all or a portion of a distribution may be a return of capital.

Please see Note 4 of the Notes to the Financial

Statements for more information on distributions for the Period.

What influenced the Trust’s performance over the Period?

The Trust generated positive returns

across its main portfolio segments during the Period. CLO equity represented the largest contributor to performance, with a net gain of

$0.73 per share for the Period, followed by the Trust’s performing loan investments, which produced a net gain of $0.65 per share.

During the Period, the Trust’s CLO equity positions collected quarterly distribution payments totaling $33,413,102 or $0.87 per

share, which were offset by unrealized market value losses of $5,159,071 or $0.13 per share. It bears noting that CLO equity pricing can

be volatile. The Trust’s CLO debt portfolio segment and performing high yield bond portfolio segment posted net gains of $0.33 per

share and $0.04 per share, respectively, for the Period.

Relevant indices for the markets

in which the Trust invests include the Trust’s benchmark, the Morningstar 100, which returned 13.74% for the Period, Bloomberg Barclays

U.S. High Yield 1% Issuer Capped Index, which returned 10.31% for the Period, and the JP Morgan BB/B CLO Debt Index, which returned 23.48%

for the Period. There is no representative benchmark index for CLO equity in the marketplace.

Discuss the Trust’s secondary market performance and

issuance of additional common shares.

During the Period, the Trust issued

7,247,127 common shares pursuant to an at-the-market (“ATM”) offering program resulting in $48,265,936 of net proceeds to

the Trust. The ATM program is a form of continuous offering of the Trust’s common shares. The goal of the Trust’s ATM program

is to enhance secondary market liquidity for shareholders by increasing the size of the Trust over time and reducing operating expenses

per share. In an ATM offering, newly issued shares are sold incrementally into the secondary trading market through a placement agent

at prevailing market prices, but always at or above the Trust’s NAV per common share. The placement agent sells the common shares

in the open market and the Trust receives cash proceeds from the transaction to be invested pursuant to the Trust’s investment objective.

The Trust issues common

shares pursuant to the ATM program only if the common shares are trading at a sufficient premium such that the issuance price, less

the placement fee, exceeds the Trust’s NAV per common share. For the Period, the Trust’s common shares traded at an

average 2.14% premium to NAV and had an average daily trading volume of

209,761 common shares. ATM program daily issuance totals depend on the common shares’ average daily trading volume and market price’s

relative premium or discount to NAV.

XAI Octagon Floating Rate & Alternative Income Term

Trust

QUESTIONS & ANSWERS

September 30, 2023 (Continued) (Unaudited)

In addition to the ATM program,

$10,000,000 of the Trust’s 6.00% Series 2029 Convertible Preferred Shares were converted to common shares in three separate conversions

at an average conversion price above NAV per common share, resulting in the issuance of an additional 1,579,188 common shares. This share

issuance was accretive for shareholders.

Discuss the Trust’s use of leverage.

The Trust uses leverage as part

of its investment strategy to finance the purchase of additional securities that may provide increased income and greater appreciation

potential to common shareholders than could be achieved from a portfolio that is unlevered. Given the average cost of leverage during

the Period of 6.12%, the leverage employed by the Trust is expected to be accretive to income generation. The Trust currently employs

leverage through the combination of a bank borrowing facility and preferred shares outstanding. As of September 30, 2023, the amount of

outstanding borrowings under the facility was $150,350,000, which represented approximately 29.57% of the Trust’s Managed Assets

(including the proceeds from borrowing). As of September 30, 2023, the purchasers of the 6.00% Series 2029 Convertible Preferred Shares

had purchased 800,000 additional 6.00% Series 2029 Convertible Preferred Shares, representing an aggregate liquidation preference of $20,000,000.

The Trust also had 6.50% Series 2026 Preferred Shares outstanding with a total liquidation preference of $39,900,000. Total leverage was

$210,250,000 as of September 30, 2023, representing 41.34% of the Trust’s Managed Assets.

The Trust may use leverage through

(i) the issuance of senior securities representing indebtedness, including through borrowing from financial institutions or issuance of

debt securities, including notes or commercial paper, (ii) the issuance of preferred shares and/or (iii) reverse repurchase agreements,

securities lending, short sales or derivatives, such as swaps, futures or forward contracts, that have the effect of leverage. The Trust

may utilize leverage, to the maximum extent permitted under the Investment Company Act of 1940, as amended. Because a portion of the Trust’s

assets may consist of illiquid investments, to the extent that the Trust must dispose of portfolio holdings to meet its regulatory asset

coverage ratio, the Trust may be required to dispose of more liquid holdings at times or on terms that the Trust would otherwise consider

undesirable, which may pose particular risks during adverse or volatile market conditions. While leverage may increase the income of the

Trust in yield terms, it also amplifies the effects of changing market prices in the portfolio and can cause the Trust’s NAV to

change to a greater degree than the market as a whole. This change in NAV can create volatility in Trust pricing.

Index Definitions

The Trust is actively managed and

does not seek to track any index. Index returns are stated for illustrative purposes only, do not reflect the deduction of fees and expenses,

and do not represent the performance of the Trust. Past performance is not a predictor of future market performance. It is not possible

to invest directly in an index.

The Bloomberg Barclays U.S. High

Yield 1% Issuer Capped Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond markets. Securities are classified

as high yield if the middle rating of the Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. Issuers are capped at 1% of the index.

The J.P. Morgan CLO Debt Index represents

the post-crisis J.P. Morgan Collateralized Loan Obligation Index (“CLOIE”). The CLOIE is an index that tracks the market for

U.S. dollar-denominated broadly syndicated, arbitrage CLOs. The CLOIE is divided by origination (pre- versus post-crisis) and is broken

out further into six original rating classes (AAA, AA, A, BBB, BB, B). The sub-index referenced herein tracks BB-rated CLO debt.

The Morningstar LLI is a market-value

weighted index designed to measure the performance of the US leveraged loan market. The index universe comprises syndicated, senior secured,

US-dollar denominated leveraged loans covered by PitchBook Leveraged Commentary & Data (“PitchBook LCD”), a Morningstar

Company. Loan facilities included in the Morningstar LLI must have a one year (at inception) minimum term, an initial minimum spread of

LIBOR/SOFR +1.25%, and a minimum size of $50mm (initially funded). LSTA/Refinitiv Mark-to-Market Pricing is used to price each loan in

the index. LSTA/Refinitiv Mark-to-Market Pricing is based on bid/ask quotes gathered from dealers and is not based upon derived pricing

models. The index uses the average bid for its market value calculation. Please note, the performance information presented herein for

the Morningstar LLI reflects restated returns for the period June 25, 2022 – February 27, 2023, pursuant to a recent notification

issued by PitchBook LCD that a technical error had occurred in the calculation of accrued interest for certain securities dating back

to June 25, 2022. Consequently, previous communications reflected overstated returns.

The Morningstar LSTA US Leveraged

Loan 100 Index (the “Morningstar 100”) is designed to measure the performance of the 100 largest facilities in the US leveraged

loan market. Index constituents are market-value weighted, subject to a single loan facility weight cap of 2%. Loan facilities included

in the Morningstar 100 must have a one year (at inception) minimum term, an initial minimum spread of LIBOR/SOFR + 1.25%, and a minimum

size of $50mm (initially funded). LSTA/Refinitiv Mark-to-Market Pricing is used to price each loan in the index. LSTA/Refinitiv Mark-to-Market

Pricing is based on bid/ask quotes gathered from dealers and is not based upon derived pricing models. The index uses the average bid

for its market value calculation. Please note, the performance information presented herein for the Morningstar 100 reflects restated

returns for the period June 25, 2022 – February 27, 2023, pursuant to a recent notification issued by PitchBook LCD that a technical

error had occurred in the calculation of accrued interest for certain securities dating back to June 25, 2022. Consequently, previous

communications reflected overstated returns.

Risks and Other Considerations

Investing involves risk, including the

possible loss of principal and fluctuation in value.

The views expressed in these Questions

& Answers reflect those of the portfolio managers only through the report period as stated on the cover. These views are expressed

for informational purposes only and are subject to change at any time, based on market and other conditions, and may not come to pass.

These views should not be construed as research, investment advice or a recommendation of any kind regarding the Trust or any issuer or

security, do not constitute a solicitation to buy or sell any security, and should not be considered specific legal, investment or tax

advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific

investor.

XAI Octagon Floating Rate & Alternative Income Term

Trust

QUESTIONS & ANSWERS

September 30, 2023 (Continued) (Unaudited)

The views expressed in this report

may also include forward-looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come

to pass. Actual results or events may differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking

statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking

statements, include general economic conditions such as inflation, recession, and interest rates. Neither XAI nor Octagon has any obligation

to update or otherwise revise any forward-looking statements, including any revision to reflect changes in any circumstances arising after

the date hereof relating to any assumptions or otherwise.

There can be no

assurance that the Trust will achieve its investment objective or that any investment strategies or techniques discussed herein will

be effective. The value of the Trust will fluctuate with the value of the underlying securities. Historically, exchange-listed

closed-end funds often trade at a discount to their NAV.

Performance data quoted represents

past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance

data quoted.

Risk Considerations

Investing in closed-end funds involves

risk; principal loss is possible. There is no guarantee the Trust’s investment objective will be achieved. Exchange-listed closed-end

fund shares may frequently trade at a discount or premium to their NAV. CLOs often involve risks that are different from or more acute

than risks associated with other types of credit instruments and may be difficult to value or be illiquid. The value of CLOs may decrease

if ratings agencies revise their ratings criteria and, as a result, lower the rating of a CLO in which the Trust has invested. Senior

loans may not be fully secured by collateral, generally do not trade on exchanges, and are typically issued by unrated or below-investment

grade companies, and therefore are subject to greater liquidity and credit risk. Lower credit quality debt securities may be more likely

to fail to make timely interest or principal payments. Leverage increases return volatility and magnifies the Trust’s potential

return and its risks; there is no guarantee a trust’s leverage strategy will be successful. The Trust’s shares are not guaranteed

or endorsed by any bank or other insured depository institution and are not federally insured by the Federal Deposit Insurance Corporation.

Please see “Risks” for more information

regarding the Trust’s risks and considerations.

Visit the Trust’s website

(www.xainvestments.com/XFLT) for additional

information regarding the Trust. The Trust regularly updates performance and certain other data and publishes material information as

necessary from time to time on its website. Investors and others are advised to check the website for updated information and the release

of other material information about the Trust. References herein to the Trust’s website are intended to allow investors public access

to information regarding the Trust and do not, and are not intended to, incorporate the Trust’s website in this report.

This material is not intended as

a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material

is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does

not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes

only and is not intended to be, and should not be construed as, legal or tax advice and/or legal opinion. Always consult a financial,

tax, and/or legal professional regarding your specific situation.

| 1 |

Sources: PitchBook Leveraged Commentary

& Data (“PitchBook LCD”), Morningstar LSTA (“Loan Syndications and Trading Association”) US Leveraged

Loan Index. Represents metrics for the Morningstar LSTA US Leveraged Loan Index as of the stated date. |

| 2 |

Source: LSTA, “3Q23 LSTA Trade Data Study Executive Summary: Trade Prices Surge to New Highs on Historically Low Trade Activity,” (October 19, 2023). |

| 3 |

Source: PitchBook LCD, “In first damage-free month of 2023, loan default rate falls to 1.27%,” (October 2, 2023).. |

| 4 |

Source: PitchBook LCD, Morningstar LSTA

US Leveraged Loan Index: Current Credit Statistics, (June 30, 2023). Data for loans represents metrics for 168 issuers within the

Morningstar LSTA US Leveraged Loan Index that file results publicly, or 14% of the total index. For this analysis, PitchBook LCD

draws its performance metrics and total debt levels from S&P Capital IQ. |

| 5 |

Source: PitchBook LCD, “Investor Technicals,” (October 10, 2023). Retrieved from www.lcdcomps.com. |

| 6 |

Source: PitchBook LCD, “US Credit Markets Quarterly – 3Q 2023,” (October 2, 2023). |

| 7 |

Source: PitchBook LCD, “LCD September Wrap: Loans continue to rally despite losses in other asset classes,” (October 2, 2023). |

| 8 |

Source: J.P. Morgan Data Query, as of the stated period/date. J.P. Morgan Collateralized Loan Obligation Index. |

| 9 |

Source: J.P. Morgan Data Query. Represents performance for J.P. Morgan JULI US AAA Index from January 1-September 30, 2023, (October 17, 2023). |

| 10 |

Source: J.P. Morgan High Yield Bond and Leveraged Loan Market Monitor, (October 2, 2023). |

| 11 |

Source: J.P. Morgan CLO Research, (September 2023). |

| 12 |

Source: PitchBook LCD, “US Credit Markets Quarterly Wrap – Second Quarter 2023,” (July 5, 2023). |

| 13 |

Source: BofA Global Research, “CLO Weekly,” (October 16, 2023). |

| 14 |

Source: Barclays Credit Research, “Equity distributions remained strong during July payment cycle,” (August 11, 2023). |

| 15 |

Source: Nomura Global Markets Research,

Securitized Products – North America, “CLO Special Topics: Repayment and default expectations,” (October 19,

2023).

|

XAI Octagon Floating

Rate & Alternative Income Term Trust

TRUST PORTFOLIO INFORMATION

September 30, 2023 (Unaudited)

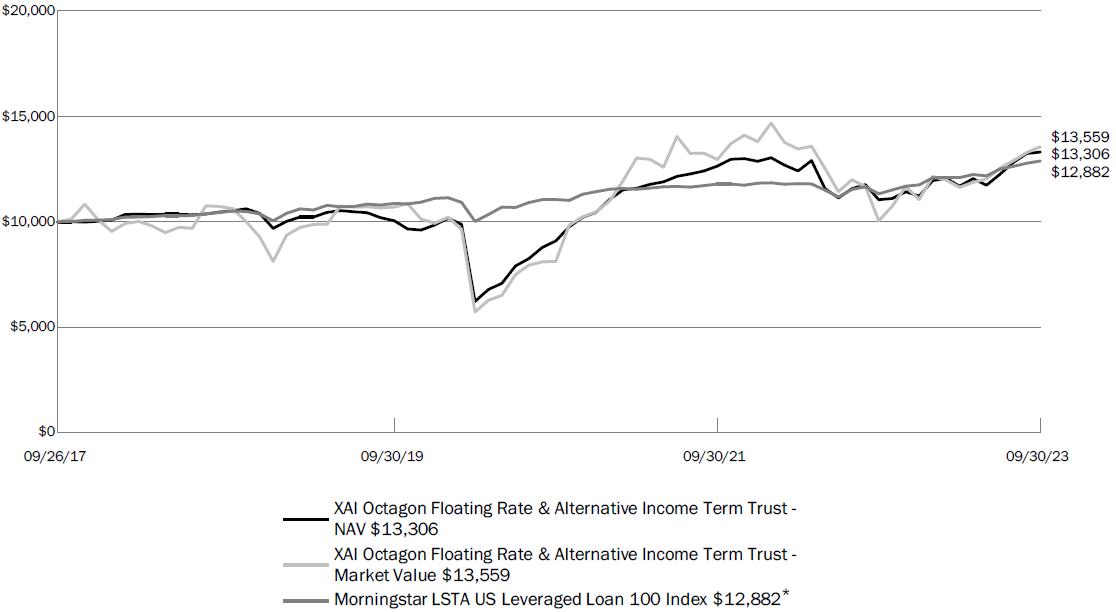

Growth

of a $10,000 Investment (as of September 30, 2023)

The chart above represents

historical performance of a hypothetical investment of $10,000 in the Trust since inception. Past

performance does not guarantee future results. Performance reflects the partial waiver of the Trust’s advisory fees

and/or reimbursement of expenses for certain periods since the inception date. Without these waivers and/or reimbursements, performance

would have been lower. This chart does not reflect the deduction of taxes that a shareholder would pay on Trust distributions or the

redemption of Trust shares. The chart assumes that distributions from the Trust are reinvested.

Summary

Performance (as of September 30, 2023)

| |

1 Month |

3 Months |

6 Months |

1 Year |

3 Years |

5 Years |

Since

Inception

(September 27,

2017)^ |

| XAI Octagon Floating Rate & Alternative Income Term Trust - NAV |

0.52% |

8.60% |

13.86% |

20.48% |

13.56% |

4.81% |

4.87% |

| XAI Octagon Floating Rate & Alternative Income Term Trust - Market Price |

2.01% |

8.07% |

16.61% |

35.05% |

18.67% |

5.02% |

5.20% |

| Morningstar LSTA US Leveraged Loan 100 Index* |

0.80% |

3.09% |

6.53% |

13.77% |

5.25% |

4.17% |

4.30% |

| * | The Morningstar LSTA US Leveraged Loan 100 Index (Loan

Syndications and Trading Association) U.S. Leveraged Loan 100 Index was the first to track the investable senior loan market. This rules-based

index consists of the 100 largest loan facilities in the benchmark S&P/LSTA Leveraged Loan Index (LLI). |

Performance data quoted represents past performance.

Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s

shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than performance

data quoted.

XAI

Octagon Floating Rate & Alternative Income Term Trust

TRUST PORTFOLIO INFORMATION

September 30, 2023 (Continued) (Unaudited)

Top

Ten Portfolio Holdings (as a % of Total Investments)*

| Name |

Type |

|

| Elmwood CLO 14 Ltd. |

Collateralized Loan Obligations Equity |

1.60% |

| CARLYLE US CLO 2019-4 Ltd. |

Collateralized Loan Obligations Equity |

1.39% |

| Elmwood CLO VII Ltd. |

Collateralized Loan Obligations Equity |

1.28% |

| Rockland Park CLO Ltd. |

Collateralized Loan Obligations Equity |

1.08% |

| Regatta XIX Funding Ltd. |

Collateralized Loan Obligations Equity |

1.07% |

| Elmwood CLO II Ltd. |

Collateralized Loan Obligations Equity |

0.97% |

| Regatta XVIII Funding Ltd. |

Collateralized Loan Obligations Equity |

0.95% |

| Anchorage Capital CLO 13 LLC |

Collateralized Loan Obligations Equity |

0.81% |

| Benefit Street Partners CLO XXV Ltd. |

Collateralized Loan Obligations Equity |

0.80% |

| Elmwood CLO I Ltd. |

Collateralized Loan Obligations Equity |

0.80% |

| Total |

|

10.75% |

| * | Holdings

may vary, are subject to change, and exclude Money Market Mutual Funds. |

| Asset Allocation* |

% of Total Investments** |

| Senior Secured First Lien Loans |

45.85% |

| Collateralized Loan Obligations Equity |

29.71% |

| Collateralized Loan Obligations Debt |

17.07% |

| Corporate Bonds |

3.67% |

| Money Market Mutual Funds |

2.10% |

| Secured Second Lien Loans |

1.54% |

| Common Stocks |

0.06% |

| Rights |

–% |

| * | Holdings may vary and are subject to change. |

| ** | Total may not add up to 100% due to rounding. |

XAI

Octagon Floating Rate & Alternative Income Term Trust

SCHEDULE

OF INVESTMENTS

September

30, 2023

| | |

Reference Rate &

Spread | |

Maturity Date | |

Principal Amount | | |

Value | |

| COLLATERALIZED LOAN OBLIGATIONS DEBT - 29.78%(a)(b) |

| Anchorage Capital CLO 13 LLC | |

3M SOFR + 6.96% | |

04/15/2034 | |

$ | 1,500,000 | | |

$ | 1,359,222 | |

| Anchorage Capital CLO 16 Ltd. | |

3M SOFR + 7.61% | |

01/19/2035 | |

| 2,000,000 | | |

| 1,864,897 | |

| Anchorage Capital CLO 17 Ltd. | |

3M SOFR + 7.12% | |

07/15/2034 | |

| 1,250,000 | | |

| 1,144,951 | |

| Anchorage Capital CLO 19 Ltd. | |

3M SOFR + 7.51% | |

10/15/2034 | |

| 1,000,000 | | |

| 764,974 | |

| Anchorage Capital CLO 21 Ltd. | |

3M SOFR + 7.61% | |

10/20/2034 | |

| 500,000 | | |

| 466,686 | |

| Anchorage Capital CLO 4-R Ltd. | |

3M SOFR + 5.76% | |

01/28/2031 | |

| 2,000,000 | | |

| 1,796,254 | |

| Anchorage Capital CLO 9 Ltd. | |

3M SOFR + 7.08% | |

07/15/2032 | |

| 2,000,000 | | |

| 1,840,072 | |

| Apidos CLO XLV Ltd. | |

3M SOFR + 8.40% | |

04/26/2036 | |

| 500,000 | | |

| 492,796 | |

| Apidos CLO XXVII | |

3M SOFR + 6.66% | |

07/17/2030 | |

| 375,000 | | |

| 353,865 | |

| Apidos CLO XXXII | |

3M SOFR + 7.01% | |

01/20/2033 | |

| 250,000 | | |

| 239,761 | |

| ARES LI CLO Ltd. | |

3M SOFR + 7.11% | |

07/15/2034 | |

| 250,000 | | |

| 231,283 | |

| ARES Loan Funding III Ltd. | |

3M SOFR + 7.58% | |

07/25/2035 | |

| 1,000,000 | | |

| 988,996 | |

| ARES LV CLO Ltd. | |

3M SOFR + 6.61% | |

07/15/2034 | |

| 1,525,000 | | |

| 1,447,813 | |

| Atrium IX | |

3M SOFR + 6.71% | |

05/28/2030 | |

| 900,000 | | |

| 852,478 | |

| Atrium XIV LLC | |

3M SOFR + 5.91% | |

08/23/2030 | |

| 500,000 | | |

| 478,713 | |

| Ballyrock CLO 20 Ltd. | |

3M SOFR + 7.25% | |

07/15/2034 | |

| 4,000,000 | | |

| 4,000,000 | |

| Battalion CLO XXI Ltd. | |

3M SOFR + 6.72% | |

07/15/2034 | |

| 1,000,000 | | |

| 878,644 | |

| Benefit Street Partners CLO XVII Ltd. | |

3M SOFR + 6.61% | |

07/15/2032 | |

| 1,100,000 | | |

| 988,132 | |

| Benefit Street Partners CLO XXIV Ltd. | |

3M SOFR + 6.87% | |

10/20/2034 | |

| 1,000,000 | | |

| 943,722 | |

| Benefit Street Partners CLO XXIX | |

3M SOFR + 7.81% | |

01/25/2036 | |

| 1,750,000 | | |

| 1,728,324 | |

| Benefit Street Partners CLO XXVIII Ltd. | |

3M SOFR + 7.59% | |

10/20/2035 | |

| 2,000,000 | | |

| 1,973,890 | |

| CARLYLE US CLO 2022-2 Ltd. | |

3M SOFR + 7.40% | |

04/20/2035 | |

| 800,000 | | |

| 774,281 | |

| Carlyle US CLO 2022-5 Ltd. | |

3M SOFR + 8.46% | |

10/15/2035 | |

| 2,000,000 | | |

| 1,980,331 | |

| CIFC Funding 2015-I Ltd. | |

3M SOFR + 6.26% | |

01/22/2031 | |

| 500,000 | | |

| 448,370 | |

| CIFC Funding 2018-I Ltd. | |

3M SOFR + 5.26% | |

04/18/2031 | |

| 1,750,000 | | |

| 1,568,750 | |

| CIFC Funding 2019-III Ltd. | |

3M SOFR + 7.06% | |

10/16/2034 | |

| 2,750,000 | | |

| 2,643,700 | |

| CIFC Funding 2019-V Ltd. | |

3M SOFR + 7.04% | |

01/15/2035 | |

| 1,000,000 | | |

| 949,880 | |

| CIFC Funding 2019-VI Ltd. | |

3M SOFR + 7.66% | |

01/16/2033 | |

| 500,000 | | |

| 488,413 | |

| CIFC Funding 2022-I Ltd. | |

3M SOFR + 6.40% | |

04/17/2035 | |

| 2,000,000 | | |

| 1,868,054 | |

| CIFC Funding 2022-III Ltd. | |

3M SOFR + 7.27% | |

04/21/2035 | |

| 850,000 | | |

| 817,197 | |

| Clover CLO 2021-3 LLC | |

3M SOFR + 6.72% | |

01/25/2035 | |

| 1,000,000 | | |

| 968,045 | |

| Elmwood CLO II Ltd. | |

3M SOFR + 3.26% | |

04/20/2034 | |

| 1,250,000 | | |

| 1,235,397 | |

| Elmwood CLO VI Ltd. | |

3M SOFR + 6.76% | |

10/20/2034 | |

| 1,750,000 | | |

| 1,736,692 | |

| Elmwood CLO VII Ltd. | |

3M SOFR + 7.50% | |

01/17/2034 | |

| 2,000,000 | | |

| 1,800,000 | |

| Elmwood CLO XI Ltd. | |

3M SOFR + 6.26% | |

10/20/2034 | |

| 750,000 | | |

| 735,871 | |

| GoldenTree Loan Management US CLO 16 Ltd. | |

3M SOFR + 6.75% | |

01/20/2035 | |

| 1,000,000 | | |

| 984,502 | |

| HPS Loan Management 11-2017 Ltd. | |

3M SOFR + 8.11% | |

05/06/2030 | |

| 1,000,000 | | |

| 716,312 | |

| Madison Park Funding LX Ltd. | |

3M SOFR + 8.95% | |

10/25/2035 | |

| 1,250,000 | | |

| 1,250,137 | |

| Madison Park Funding LXIII Ltd. | |

3M SOFR + 8.57% | |

04/21/2035 | |

| 1,250,000 | | |

| 1,242,385 | |

| Madison Park Funding XLVI Ltd. | |

3M SOFR + 6.51% | |

10/15/2034 | |

| 550,000 | | |

| 538,763 | |

| Madison Park Funding XLVIII Ltd. | |

3M SOFR + 6.51% | |

04/19/2033 | |

| 1,500,000 | | |

| 1,470,287 | |

| Madison Park Funding XVII Ltd. | |

3M SOFR + 7.74% | |

07/21/2030 | |

| 1,000,000 | | |

| 739,776 | |

| Madison Park Funding XXVII Ltd. | |

3M SOFR + 5.26% | |

04/20/2030 | |

| 1,500,000 | | |

| 1,385,861 | |

| Madison Park Funding XXXVII Ltd. | |

3M SOFR + 6.41% | |

07/15/2033 | |

| 750,000 | | |

| 734,708 | |

| Magnetite XXIV Ltd. | |

3M SOFR + 6.40% | |

04/15/2035 | |

| 500,000 | | |

| 475,385 | |

| Neuberger Berman Loan Advisers CLO 24 Ltd. | |

3M SOFR + 6.28% | |

04/19/2030 | |

| 1,000,000 | | |

| 929,211 | |

| Neuberger Berman Loan Advisers CLO 32 Ltd. | |

3M SOFR + 6.36% | |

01/20/2032 | |

| 1,500,000 | | |

| 1,421,506 | |

| Neuberger Berman Loan Advisers Clo 40 Ltd. | |

3M SOFR + 6.11% | |

04/16/2033 | |

| 1,670,000 | | |

| 1,580,105 | |

| Neuberger Berman Loan Advisers CLO 47 Ltd. | |

3M SOFR + 6.25% | |

04/14/2035 | |

| 1,000,000 | | |

| 952,422 | |

| OHA Credit Funding 11 Ltd. | |

3M SOFR + 7.25% | |

07/19/2033 | |

| 550,000 | | |

| 549,323 | |

| OHA Credit Funding 12 Ltd. | |

3M SOFR + 8.00% | |

07/20/2036 | |

| 2,000,000 | | |

| 1,972,386 | |

| OHA Credit Funding 2 Ltd. | |

3M SOFR + 6.36% | |

04/21/2034 | |

| 1,000,000 | | |

| 985,261 | |

| OHA Credit Funding 5 Ltd. | |

3M SOFR + 6.51% | |

04/18/2033 | |

| 1,000,000 | | |

| 975,940 | |

| OHA Credit Funding 7 Ltd. | |

3M SOFR + 6.25% | |

02/24/2037 | |

| 900,000 | | |

| 880,767 | |

| OHA Credit Funding 9 Ltd. | |

3M SOFR + 6.51% | |

07/19/2035 | |

| 1,000,000 | | |

| 982,550 | |

| Rad CLO 10 Ltd. | |

3M SOFR + 6.11% | |

04/23/2034 | |

| 2,000,000 | | |

| 1,897,646 | |

| Rad CLO 11 Ltd. | |

3M SOFR + 6.51% | |

04/15/2034 | |

| 1,300,000 | | |

| 1,232,269 | |

| Rad CLO 12 Ltd. | |

3M SOFR + 6.61% | |

10/30/2034 | |

| 2,000,000 | | |

| 1,881,571 | |

| Rad CLO 4 Ltd. | |

3M SOFR + 7.01% | |

04/25/2032 | |

| 2,328,764 | | |

| 2,217,092 | |

| Regatta VII Funding Ltd. | |

3M SOFR + 6.66% | |

06/20/2034 | |

| 1,000,000 | | |

| 927,808 | |

| Regatta VIII Funding Ltd. | |

3M SOFR + 6.36% | |

10/17/2030 | |

| 500,000 | | |

| 478,701 | |

| Regatta XII Funding Ltd. | |

3M SOFR + 6.61% | |

10/15/2032 | |

| 500,000 | | |

| 481,295 | |

See Notes to Financial

Statements.

XAI

Octagon Floating Rate & Alternative Income Term Trust

SCHEDULE

OF INVESTMENTS

September

30, 2023 (Continued)

| | |

Reference Rate &

Spread | |

Maturity Date | |

Principal Amount | | |

Value | |

| COLLATERALIZED LOAN OBLIGATIONS DEBT - 29.78%(a)(b)(Continued) | |

| |

| | |

| |

| Regatta XIV Funding Ltd. | |

3M SOFR + 6.21% | |

10/25/2031 | |

$ | 750,000 | | |

$ | 669,553 | |

| Regatta XIX Funding Ltd. | |

3M SOFR + 6.88% | |

04/20/2035 | |

| 750,000 | | |

| 731,277 | |

| Regatta XVI Funding Ltd. | |

3M SOFR + 7.26% | |

01/15/2033 | |

| 1,400,000 | | |

| 1,365,649 | |

| Regatta XVIII Funding Ltd. | |

3M SOFR + 6.21% | |

01/15/2034 | |

| 2,000,000 | | |

| 1,880,988 | |

| Regatta XXII Funding Ltd. | |

3M SOFR + 7.19% | |

07/20/2035 | |

| 1,350,000 | | |

| 1,338,413 | |

| Regatta XXIII Funding Ltd. | |

3M SOFR + 6.96% | |

01/20/2035 | |

| 2,750,000 | | |

| 2,650,560 | |

| Regatta XXIV Funding Ltd. | |

3M SOFR + 7.06% | |

01/20/2035 | |

| 250,000 | | |

| 241,392 | |

| RR 19 Ltd. | |

3M SOFR + 6.76% | |

10/15/2035 | |

| 500,000 | | |

| 495,882 | |

| Sound Point CLO II Ltd. | |

3M SOFR + 5.76% | |

01/26/2031 | |

| 250,000 | | |

| 153,368 | |

| Sound Point CLO XVIII Ltd. | |

3M SOFR + 5.76% | |

01/21/2031 | |

| 500,000 | | |

| 324,916 | |

| Symphony CLO XXI Ltd. | |

3M SOFR + 6.86% | |

07/15/2032 | |

| 1,000,000 | | |

| 892,078 | |

| Symphony CLO XXIV Ltd. | |

3M SOFR + 7.26% | |

01/23/2032 | |

| 1,000,000 | | |

| 938,325 | |

| THL Credit Wind River 2017-1 CLO Ltd. | |

3M SOFR + 7.32% | |

04/18/2036 | |

| 1,500,000 | | |

| 1,312,819 | |

| THL Credit Wind River 2017-4 CLO Ltd. | |

3M SOFR + 6.06% | |

11/20/2030 | |

| 500,000 | | |

| 443,926 | |

| THL Credit Wind River 2019-1 CLO Ltd. | |

3M SOFR + 6.86% | |

07/20/2034 | |

| 875,000 | | |

| 705,057 | |

| Voya CLO 2020-2 Ltd. | |

3M SOFR + 6.66% | |

07/19/2034 | |

| 1,125,000 | | |

| 1,071,206 | |

| Wind River 2021-3 CLO Ltd. | |

3M SOFR + 6.86% | |

07/20/2033 | |

| 1,000,000 | | |

| 887,972 | |

| | |

| |

| |

| | | |

| 88,837,804 | |

TOTAL COLLATERALIZED LOAN OBLIGATIONS DEBT

(Cost $91,537,635) | |

| |

| |

| | | |

| 88,837,804 | |

| | |

| |

| |

| | | |

| | |

| | |

Estimated Yield | |

Maturity Date | |

| Principal

Amount | | |

| Value | |

| COLLATERALIZED LOAN OBLIGATIONS EQUITY - 51.84%(a)(c) |

| |

| | | |

| | |

| ALM 2020 Ltd. | |

5.75% | |

10/15/2029 | |

| 5,000,000 | | |

| 1,703,310 | |

| Anchorage Capital CLO 13 LLC | |

15.93% | |

04/15/2034 | |

| 7,000,000 | | |

| 4,213,104 | |

| Anchorage Capital CLO 16 Ltd. | |

15.26% | |

01/19/2035 | |

| 2,500,000 | | |

| 1,342,960 | |

| Anchorage Capital CLO 18 Ltd. | |

16.80% | |

04/15/2034 | |

| 850,000 | | |

| 530,539 | |

| Anchorage Capital CLO 19 Ltd. | |

14.32% | |

10/15/2034 | |

| 7,000,000 | | |

| 4,025,077 | |

| Anchorage Capital CLO 1-R Ltd. | |

10.69% | |

04/13/2031 | |

| 4,150,000 | | |

| 1,577,100 | |

| Anchorage Capital CLO 20 Ltd. | |

12.94% | |

01/20/2035 | |

| 1,750,000 | | |

| 1,019,363 | |

| Anchorage Capital CLO 3-R Ltd. | |

10.38% | |

01/28/2031 | |

| 1,400,000 | | |

| 456,148 | |

| Anchorage Capital CLO 7 Ltd. | |

21.72% | |

01/28/2031 | |

| 1,750,000 | | |

| 531,492 | |

| Apidos CLO XXVII | |

8.02% | |

07/17/2030 | |

| 1,300,000 | | |

| 228,436 | |

| ARES LI CLO Ltd. | |

12.98% | |

07/15/2034 | |

| 1,699,959 | | |

| 771,168 | |

| ARES LI CLO Ltd. | |

12.64% | |

07/15/2034 | |

| 2,646,041 | | |

| 1,200,347 | |

| ARES LIX CLO Ltd. | |

25.33% | |

04/25/2034 | |

| 3,500,000 | | |

| 2,188,900 | |

| ARES XLI CLO Ltd. | |

12.27% | |

04/15/2034 | |

| 2,343,500 | | |

| 815,102 | |

| ARES XLIV CLO Ltd. | |

14.20% | |

04/15/2034 | |

| 2,845,572 | | |

| 847,024 | |

| Battalion CLO XV Ltd. | |

15.86% | |

01/17/2033 | |

| 4,500,000 | | |

| 2,439,211 | |

| Battalion CLO XVI Ltd. | |

14.60% | |

12/19/2032 | |

| 3,500,000 | | |

| 1,770,261 | |

| Benefit Street Partners CLO XXV Ltd. | |

47.25% | |

01/15/2035 | |

| 5,250,000 | | |

| 4,180,496 | |

| Carbone Clo Ltd. | |

15.26% | |

01/20/2031 | |

| 7,850,000 | | |

| 3,172,263 | |

| CARLYLE US CLO 2019-4 Ltd. | |

21.42% | |

04/15/2035 | |

| 8,740,000 | | |

| 7,227,001 | |

| CARLYLE US CLO 2021-4 Ltd. | |

22.91% | |

04/20/2034 | |

| 1,000,000 | | |

| 762,285 | |

| CARLYLE US CLO 2021-5 Ltd. | |

15.92% | |

07/20/2034 | |

| 4,000,000 | | |

| 2,699,148 | |

| CIFC Funding 2017-III Ltd. | |

10.53% | |

07/20/2030 | |

| 1,400,000 | | |

| 386,036 | |

| CIFC Funding 2017-V Ltd. | |

7.22% | |

11/16/2030 | |

| 4,500,000 | | |

| 1,517,535 | |

| CIFC Funding 2018-I Ltd. | |

12.11% | |

04/18/2031 | |

| 3,250,000 | | |

| 1,293,958 | |

| CIFC Funding 2018-III Ltd. | |

16.93% | |

07/18/2031 | |

| 3,000,000 | | |

| 1,298,958 | |

| CIFC Funding 2019-III Ltd. | |

19.87% | |

10/16/2034 | |

| 750,000 | | |

| 576,763 | |

| CIFC Funding 2019-V Ltd. | |

19.92% | |

01/15/2035 | |

| 2,500,000 | | |

| 1,909,817 | |

| CIFC Funding 2019-V Ltd. | |

21.30% | |

01/15/2035 | |

| 1,000,000 | | |

| 763,927 | |

| CIFC Funding 2020-II Ltd. | |

27.82% | |

10/20/2034 | |

| 1,000,000 | | |

| 796,159 | |

| CIFC Funding 2020-III Ltd. | |

21.43% | |

10/20/2034 | |

| 150,000 | | |

| 123,039 | |

| CIFC Funding 2021-II | |

18.38% | |

04/15/2034 | |

| 4,000,000 | | |

| 3,132,948 | |

| CIFC Funding 2021-VII Ltd. | |

19.01% | |

01/23/2035 | |

| 1,000,000 | | |

| 785,813 | |

| Clover CLO 2019-1 Ltd. | |

24.60% | |

04/18/2035 | |

| 3,839,200 | | |

| 2,876,885 | |

| Dryden 43 Senior Loan Fund | |

15.37% | |

04/20/2034 | |

| 3,000,000 | | |

| 1,390,500 | |

| Dryden 87 CLO Ltd. | |

17.45% | |

05/20/2034 | |

| 2,000,000 | | |

| 1,305,400 | |

| Dryden 95 CLO Ltd. | |

16.69% | |

08/20/2034 | |

| 1,750,000 | | |

| 1,044,575 | |

| Elmwood CLO 14 Ltd. | |

24.81% | |

04/20/2035 | |

| 10,000,000 | | |

| 8,324,000 | |

| Elmwood CLO I Ltd. | |

16.36% | |

10/20/2033 | |

| 6,000,000 | | |

| 4,156,903 | |

See Notes to Financial

Statements.

XAI

Octagon Floating Rate & Alternative Income Term Trust

SCHEDULE

OF INVESTMENTS

September

30, 2023 (Continued)

| | |

Estimated Yield | |

Maturity Date | |

Principal Amount | | |

Value | |

| COLLATERALIZED LOAN OBLIGATIONS EQUITY - 51.84%(a)(c)(Continued) |

| Elmwood CLO II Ltd. | |

19.33% | |

04/20/2034 | |

$ | 6,500,000 | | |

$ | 5,056,669 | |

| Elmwood CLO III Ltd. | |

20.27% | |

10/20/2034 | |

| 5,250,000 | | |

| 3,958,238 | |

| Elmwood CLO VII Ltd. | |

19.52% | |

01/17/2034 | |

| 8,350,000 | | |

| 6,664,135 | |

| Elmwood CLO VIII Ltd. | |

18.53% | |

01/20/2034 | |

| 5,000,000 | | |

| 4,026,060 | |

| Invesco CLO 2021-1 Ltd. | |

20.95% | |

04/15/2034 | |

| 3,000,000 | | |

| 2,217,000 | |

| Invesco CLO Ltd.(d)(e) | |

N/A | |

07/15/2034 | |

| 500,000 | | |

| 122,480 | |

| Invesco CLO Ltd. | |

17.09% | |

07/15/2034 | |

| 5,000,000 | | |

| 3,144,500 | |

| Madison Park Funding XVIII Ltd. | |

16.26% | |

10/21/2030 | |

| 4,000,000 | | |

| 1,522,200 | |

| Madison Park Funding XX Ltd. | |

22.58% | |

07/27/2030 | |

| 1,740,000 | | |

| 671,466 | |

| Madison Park Funding XXIX Ltd. | |

17.06% | |

10/18/2047 | |

| 3,750,000 | | |

| 1,855,500 | |

| Madison Park Funding XXVIII Ltd. | |

19.69% | |

07/15/2030 | |

| 5,000,000 | | |

| 2,711,600 | |

| Madison Park Funding XXXVII Ltd. | |

24.08% | |

07/15/2049 | |

| 5,500,000 | | |

| 3,642,694 | |

| Magnetite XIX Ltd. | |

29.29% | |

04/17/2034 | |

| 3,200,000 | | |

| 2,135,680 | |

| Niagara Park CLO Ltd. | |

16.77% | |

07/17/2032 | |

| 2,648,000 | | |

| 1,434,228 | |

| NYACK Park CLO Ltd. | |

18.39% | |

10/20/2034 | |

| 1,000,000 | | |

| 764,000 | |

| Oak Hill Credit Partners X-R Ltd. | |

33.48% | |

04/20/2034 | |

| 6,673,000 | | |

| 2,986,168 | |

| OHA Credit Partners XI Ltd. | |

19.19% | |

01/20/2032 | |

| 2,750,000 | | |

| 1,307,611 | |

| OHA Credit Partners XII Ltd. | |

21.76% | |

07/23/2030 | |

| 1,500,000 | | |

| 717,386 | |

| OHA Credit Partners XIII Ltd. | |

24.23% | |

10/21/2034 | |

| 1,600,000 | | |

| 1,104,000 | |

| Point Au Roche Park CLO Ltd. | |

31.27% | |

07/20/2034 | |

| 5,000,000 | | |

| 3,274,700 | |

| Recette CLO Ltd. | |

14.81% | |

04/20/2034 | |

| 10,400,000 | | |

| 3,640,000 | |

| Recette CLO Ltd.(d)(e) | |

N/A | |

04/20/2034 | |

| 10,400,000 | | |

| 14,768 | |

| Regatta XIX Funding Ltd. | |

22.88% | |

04/20/2035 | |

| 6,017,000 | | |

| 5,565,725 | |

| Regatta XVIII Funding Ltd. | |

34.02% | |

01/15/2034 | |

| 7,175,322 | | |

| 4,923,362 | |

| Regatta XXIV Funding Ltd. | |

15.06% | |

01/20/2035 | |

| 5,000,000 | | |

| 3,280,230 | |

| Rockland Park CLO Ltd. | |

16.21% | |

04/20/2034 | |

| 9,000,000 | | |

| 5,645,700 | |

| Rockland Park CLO Ltd.(d)(h) | |

N/A | |

04/20/2034 | |

| 9,000,000 | | |

| 25,740 | |

| Rockland Park CLO Ltd.(d)(h) | |

N/A | |

04/20/2034 | |

| 9,000,000 | | |

| 90,090 | |

| Sixth Street CLO XVII Ltd. | |

16.69% | |

01/20/2034 | |

| 1,100,000 | | |

| 800,037 | |

| THL Credit Wind River 2018-2 CLO Ltd. | |

10.09% | |

07/15/2030 | |

| 3,031,000 | | |

| 1,080,143 | |

| THL Credit Wind River 2018-3 CLO Ltd. | |

16.37% | |

01/20/2031 | |

| 3,000,000 | | |

| 1,569,936 | |

| Thompson Park CLO Ltd. | |

24.18% | |

04/15/2034 | |

| 4,000,000 | | |

| 3,291,036 | |

| Wind River 2016-1 CLO Ltd.(h) | |

N/A | |

12/31/2049 | |

| 4,000,000 | | |

| 400 | |

TOTAL COLLATERALIZED LOAN OBLIGATIONS EQUITY

(Cost $184,292,415) | |

| |

| |

| | | |

| 154,627,433 | |

| | |

| |

| |

| | | |

| | |

| | |

Coupon | |

Maturity Date | |

| Principal

Amount | | |

| Value | |

| CORPORATE BONDS - 6.40% | |

| |

| |

| | | |

| | |

| Automobiles - 0.15% | |

| |

| |

| | | |

| | |

| Ford Motor Credit Co. LLC, Senior Unsecured Bond | |

6.95% | |

03/06/2026 | |

| 455,000 | | |

| 453,863 | |

| Chemicals - 0.35% | |

| |

| |

| | | |

| | |

| Herens Holdco S.a.r.l., Senior Secured Bond(a) | |

4.75% | |

05/15/2028 | |

| 444,000 | | |

| 343,603 | |

| Illuminate Buyer LLC / Illuminate

Holdings IV, Inc., Senior Unsecured Bond(a) | |

9.00% | |

07/01/2028 | |

| 750,000 | | |

| 711,563 | |

| | |

| |

| |

| | | |

| 1,055,166 | |

| Construction & Engineering - 0.22% | |

| |

| |

| | | |

| | |

| Brand Industrial Services, Inc., Senior Secured Bond(a) | |

10.38% | |

08/01/2030 | |

| 652,000 | | |

| 653,819 | |

| Diversified Consumer Services - 0.14% | |

| |

| |

| | | |

| | |

| Sabre GLBL, Inc., Senior Secured Bond(a) | |

11.25% | |

12/15/2027 | |

| 461,000 | | |

| 422,968 | |

| Diversified Telecommunication Services - 0.77% | |

| |

| |

| | | |

| | |

| Altice Financing S.A., Senior Secured Bond(a) | |

5.75% | |

08/15/2029 | |

| 1,197,000 | | |

| 980,104 | |

| Altice France, Senior Secured Bond(a) | |

5.50% | |

10/15/2029 | |

| 667,000 | | |

| 480,240 | |

| Consolidated Communications, Inc.,

Senior Secured Bond(a) | |

5.00% | |

10/01/2028 | |

| 1,125,000 | | |

| 845,297 | |

| | |

| |

| |

| | | |

| 2,305,641 | |

| Electric Utilities - 0.30% | |

| |

| |

| | | |

| | |

| PG&E Corp., Senior Secured Bond | |

5.00% | |

07/01/2028 | |

| 1,000,000 | | |

| 906,020 | |

| Electronic Equipment, Instruments & Components - 0.04% | |

| |

| |

| | | |

| | |

| Coherent Corp., Senior Unsecured Bond(a) | |

5.00% | |

12/15/2029 | |

| 146,000 | | |

| 126,605 | |

| Gas Utilities - 0.30% | |

| |

| |

| | | |

| | |

| Ferrellgas LP / Ferrellgas Finance Corp., Senior Unsecured

Bond(a) | |

5.88% | |

04/01/2029 | |

| 1,000,000 | | |

| 899,120 | |

See Notes to Financial

Statements.

XAI

Octagon Floating Rate & Alternative Income Term Trust

SCHEDULE

OF INVESTMENTS

September

30, 2023 (Continued)

| | |

Coupon | |

Maturity Date | |

Principal Amount | | |

Value | |

| CORPORATE BONDS - 6.40%(Continued) | |

| |

| |

| | |

| |

| Health Care Equipment & Supplies - 0.23% | |

| |

| |

| | |

| |

| Medline Borrower, LP, Senior Secured Bond(a) | |

3.88% | |

04/01/2029 | |

$ | 727,000 | | |

$ | 614,578 | |

| Medline Borrower, LP, Senior Unsecured

Bond(a) | |

5.25% | |

10/01/2029 | |

| 62,000 | | |

| 53,563 | |

| | |

| |

| |

| | | |

| 668,141 | |

| Health Care Providers & Services - 0.18% | |

| |

| |

| | | |

| | |

| LifePoint Health, Inc., Senior Secured Bond(a) | |

9.88% | |

08/15/2030 | |

| 552,000 | | |

| 534,892 | |

| Health Care Technology - 0.40% | |

| |

| |

| | | |

| | |

| AthenaHealth Group, Inc., Senior Unsecured Bond(a) | |

6.50% | |

02/15/2030 | |

| 1,411,000 | | |

| 1,179,428 | |

| Hotels, Restaurants & Leisure - 0.63% | |

| |

| |

| | | |

| | |

| CEC Entertainment, LLC, Senior Secured Bond(a) | |

6.75% | |

05/01/2026 | |

| 470,000 | | |

| 443,252 | |

| Fertitta Entertainment LLC / Fertitta Entertainment Finance

Co, Inc., Senior Unsecured Bond(a) | |

6.75% | |

01/15/2030 | |

| 328,000 | | |

| 267,760 | |

| Hilton Grand Vacations Borrower Escrow LLC / Hilton Grand

Vacations Borrower Esc, Senior Unsecured Bond(a) | |

5.00% | |

06/01/2029 | |

| 529,000 | | |

| 459,844 | |

| Scientific Games Holdings LP/Scientific Games US FinCo,

Inc., Senior Unsecured Bond(a) | |

6.63% | |