0001499494false--12-31FY2023the financial support letter from Hubei New Nature Investment Co., Ltd, a company that is 80.8% owned by the former Chairman and the Chief Executive Officer, Mr. Wei, and from Dunxin Holdings Co., Ltd, a company that is 70% owned by the former Chairman and the Chief Executive Officer, Mr. Wei, which have expressed the willingness and intention to provide the necessary financial support to the Company5372000039230003416000118990009613000144920005500005500001023000913000900090000004798990003840240003835000003400003260003836840003831740009587500095875000479375000104245810022012500.00.20.8082800.0700.000014994942023-01-012023-12-310001499494dxf:MayTherteenTwontyTwontyFourMember2023-01-012023-12-310001499494dxf:WuhanWuchangPeoplesCourtMember2020-08-310001499494dxf:PropertyServicesCoLtdMember2019-05-012020-10-300001499494dxf:PropertyServicesCoLtdMember2020-04-012020-04-300001499494dxf:PropertyServicesCoLtdMember2019-08-012019-08-310001499494dxf:PropertyServicesCoLtdMember2020-10-300001499494dxf:PropertyServicesCoLtdMember2020-04-300001499494dxf:PropertyServicesCoLtdMember2019-08-3100014994942019-09-012019-09-060001499494dxf:MrDengXinxueMrZhangXuanAndMrYangBobiaoMember2019-10-012019-10-140001499494dxf:DunxinHoldingsCoLtdMember2019-09-012019-09-060001499494dxf:HubeiNewNatureInvestmentCoLtdMember2019-09-012019-09-060001499494dxf:MrWeiQizhiWeiMsPengYanAndChutianMember2019-10-1500014994942019-10-140001499494dxf:ChutianMember2019-10-140001499494dxf:HubeiShanyinWealthManagementCoLtdMember2019-10-140001499494dxf:DunxinHoldingsCoLtdMember2019-09-060001499494dxf:HubeiNewNatureInvestmentCoLtdMember2019-09-060001499494ifrs-full:IssuedCapitalMember2019-12-040001499494ifrs-full:IssuedCapitalMember2019-10-012019-10-090001499494ifrs-full:IssuedCapitalMember2019-10-090001499494ifrs-full:IssuedCapitalMember2020-11-100001499494ifrs-full:IssuedCapitalMember2019-07-310001499494ifrs-full:IssuedCapitalMember2019-08-270001499494dxf:HubeiShanyinWealthManagementCoLtdMemberdxf:ChiefExecutiveOfficersMember2022-01-012022-12-310001499494dxf:HubeiShanyinWealthManagementCoLtdMemberdxf:ChiefExecutiveOfficersMember2022-12-310001499494dxf:HubeiShanyinWealthManagementCoLtdMemberdxf:ChiefExecutiveOfficersMember2023-12-310001499494dxf:HubeiShanyinWealthManagementCoLtdMemberdxf:ChiefExecutiveOfficersMember2023-01-012023-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2017-01-012017-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2018-01-012018-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2022-01-012022-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2023-01-012023-12-310001499494dxf:HubeiDailyMediaGroupMemberdxf:LeasecommitmentMember2022-01-012022-12-310001499494dxf:HubeiDailyMediaGroupMemberdxf:LeasecommitmentMember2023-01-012023-12-310001499494dxf:KangChenMember2016-12-310001499494dxf:HubeiBaoliEcologicalConservationMember2016-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2022-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2023-12-310001499494dxf:HubeiDailyMediaGroupMemberdxf:LeasecommitmentMember2023-12-310001499494dxf:HubeiDailyMediaGroupMemberdxf:LeasecommitmentMember2022-12-310001499494dxf:HubeiNewNatureInvestmentCoMember2019-01-012019-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2021-01-012021-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2022-01-012022-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2023-01-012023-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2019-01-012019-12-310001499494dxf:LiLingMember2019-01-012019-12-310001499494dxf:HubeiShanyinWealthManagementCoLtdMemberdxf:ChiefExecutiveOfficersMember2018-12-310001499494dxf:LoanExtensionAgreementSeptemberTwoThounsandTwentyNineMember2023-12-310001499494dxf:ChutianAndMrWeiMember2019-12-040001499494dxf:ChutianAndMrWeiMember2019-10-090001499494dxf:ChutianAndMrWeiMember2023-01-012023-12-310001499494dxf:ChutianAndMrWeiMember2022-01-012022-12-310001499494dxf:ChutianAndMrWeiMember2019-10-012019-10-090001499494dxf:HubeiShanyinWealthManagementCoLtdMemberdxf:ChiefExecutiveOfficersMember2018-01-012018-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2018-01-012018-12-310001499494dxf:LoanExtensionAgreementMember2017-06-300001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2018-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2019-12-310001499494dxf:LiLingMember2019-12-310001499494dxf:WangHailinMember2017-06-300001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2022-12-310001499494dxf:InTwoZeroOneEightMemberdxf:ChiefExecutiveOfficersMember2023-12-310001499494dxf:WangHailinMember2022-12-310001499494dxf:WangHailinMember2023-12-310001499494dxf:ChutianAndMrWeiMember2023-12-310001499494dxf:ChutianAndMrWeiMember2022-12-310001499494dxf:PRCOneMember2023-12-310001499494dxf:PRCOneMember2022-12-310001499494dxf:PRCOneMember2023-01-012023-12-310001499494dxf:PRCMember2022-12-310001499494dxf:MarchOneTwoZeroOneEightMemberdxf:OrdinaryShareMember2023-01-012023-12-310001499494dxf:OrdinarySharesTwoMemberdxf:MarchOneTwoThousandEighteenMember2023-01-012023-12-310001499494dxf:MarchOneTwoZeroOneEightMemberdxf:OrdinaryShareMember2023-12-310001499494dxf:OrdinarySharesOneMemberdxf:MarchOneTwoThousandEighteenMember2023-01-012023-12-310001499494dxf:OrdinarySharesOneMemberdxf:MarchOneTwoThousandEighteenMember2023-12-310001499494dxf:OrdinarySharesTwoMemberdxf:MarchOneTwoThousandEighteenMember2023-12-3100014994942010-06-300001499494dxf:NumberOfShareMember2023-12-310001499494dxf:NumberOfShareMember2023-01-012023-12-310001499494dxf:NumberOfShareMember2022-01-012022-12-310001499494dxf:NumberOfShareMember2022-12-310001499494dxf:NumberOfShareMember2020-12-310001499494dxf:NumberOfShareMember2021-12-310001499494dxf:OrdinaryStockShareMember2023-12-310001499494dxf:OrdinaryStockShareMember2023-01-012023-12-310001499494dxf:OrdinaryStockShareMember2021-01-012021-12-310001499494dxf:OrdinaryStockShareMember2022-01-012022-12-310001499494dxf:OrdinaryStockShareMember2022-12-310001499494dxf:OrdinaryStockShareMember2020-12-310001499494dxf:OrdinaryStockShareMember2021-12-310001499494dxf:TotalEquityMember2023-12-310001499494dxf:TotalEquityMember2023-01-012023-12-310001499494dxf:TotalEquityMember2021-01-012021-12-310001499494dxf:TotalEquityMember2022-01-012022-12-310001499494dxf:TotalEquityMember2022-12-310001499494dxf:TotalEquityMember2020-12-310001499494dxf:TotalEquityMember2021-12-310001499494dxf:InterestPayableToRelatedPartiesMember2022-12-310001499494dxf:InterestPayableToRelatedPartiesMember2023-12-3100014994942023-08-012023-08-0700014994942023-07-012023-07-0700014994942023-07-0700014994942023-08-070001499494dxf:RelatedPartyMember2022-12-310001499494dxf:RelatedPartyMember2023-12-310001499494dxf:ShareholdersMember2022-12-310001499494dxf:ShareholdersMember2023-12-310001499494dxf:ThirdPartiesMember2022-12-310001499494dxf:ThirdPartiesMember2023-12-310001499494dxf:NovemberTherteenTwontyTwontyThreeMemberdxf:OrdinaryShareMember2023-01-012023-12-310001499494dxf:NovemberTherteenTwontyTwontyThreeMemberdxf:OrdinaryShareMember2023-12-310001499494dxf:AcquiredComputerSoftwareMember2022-01-012022-12-310001499494dxf:LandUseRightMember2022-01-012022-12-310001499494dxf:LandUseRightMember2023-12-310001499494dxf:AcquiredComputerSoftwareMember2023-12-310001499494dxf:LandUseRightMember2023-01-012023-12-310001499494dxf:AcquiredComputerSoftwareMember2023-01-012023-12-310001499494dxf:LandUseRightMember2021-12-310001499494dxf:AcquiredComputerSoftwareMember2021-12-310001499494dxf:LandUseRightMember2022-12-310001499494dxf:AcquiredComputerSoftwareMember2022-12-310001499494dxf:LeaseholdImprovementMember2021-12-310001499494dxf:OfficeEquipmentFurnitureMember2021-12-310001499494dxf:MotorVehicleMember2021-12-310001499494dxf:PropertyPlantAndEquipmentsMember2021-12-310001499494dxf:PropertyPlantAndEquipmentsMember2023-12-310001499494dxf:OfficeEquipmentFurnitureMember2023-12-310001499494dxf:MotorVehicleMember2023-12-310001499494dxf:LeaseholdImprovementMember2023-12-310001499494dxf:OfficeEquipmentFurnitureMember2022-01-012022-12-310001499494dxf:PropertyPlantAndEquipmentsMember2022-01-012022-12-310001499494dxf:LeaseholdImprovementMember2022-01-012022-12-310001499494dxf:OfficeEquipmentFurnitureMember2023-01-012023-12-310001499494dxf:MotorVehicleMember2023-01-012023-12-310001499494dxf:MotorVehicleMember2022-01-012022-12-310001499494dxf:LeaseholdImprovementMember2022-12-310001499494dxf:OfficeEquipmentFurnitureMember2022-12-310001499494dxf:MotorVehicleMember2022-12-310001499494dxf:PropertyPlantAndEquipmentsMember2022-12-310001499494dxf:AmericanDepositoryShareMember2017-12-280001499494dxf:AmericanDepositoryShareMember2023-07-250001499494dxf:AmericanDepositoryShareMember2014-12-180001499494dxf:AmericanDepositoryShareMember2014-12-170001499494dxf:IncomeTaxesMember2021-01-012021-12-310001499494dxf:IncomeTaxesMember2023-01-012023-12-310001499494dxf:IncomeTaxesMember2022-01-012022-12-310001499494dxf:FairValuesMember2022-12-310001499494dxf:FairValuesMember2023-12-310001499494dxf:CarryingAmountOthersMember2022-12-310001499494dxf:CarryingAmountOthersMember2023-12-310001499494dxf:HubeiProvinceMember2023-01-012023-12-310001499494dxf:MarketRiskSubjectMember2023-12-310001499494dxf:MarketRiskSubjectMember2022-12-310001499494dxf:Stage3Member2022-12-310001499494dxf:Stage2Member2022-12-310001499494dxf:Stage1Member2022-12-310001499494dxf:Stage3Member2023-12-310001499494dxf:Stage2Member2023-12-310001499494dxf:Stage1Member2023-12-310001499494dxf:PRCMember2023-12-310001499494dxf:EquityIncentivePlanMember2023-12-310001499494dxf:EquityIncentivePlanMember2010-12-310001499494dxf:EquityIncentivePlanMember2020-12-310001499494dxf:EquityIncentivePlanMember2019-12-310001499494dxf:OfficeequipmentandfurnitureMember2023-01-012023-12-310001499494dxf:VehiclesEquipmentMember2023-01-012023-12-310001499494dxf:LeaseholdImprovementMember2023-01-012023-12-310001499494dxf:PropertyPlantAndEquipmentsMember2023-01-012023-12-310001499494dxf:VariableInterestEntityMember2021-12-310001499494dxf:ShareholdersVotingProxyAgreementsMember2023-01-012023-12-310001499494dxf:ExclusivePurchaseOptionAgreementsMember2023-01-012023-12-310001499494dxf:ChutianAndChutianHoldingMemberdxf:ManagementServiceAgreementsMember2023-01-012023-12-310001499494dxf:XiniyaHoldingsLimitedMember2017-12-012017-12-280001499494dxf:TrueSilverLimitedMemberdxf:OrdinaryStockShareMember2017-12-012017-12-280001499494dxf:TrueSilverLimitedMemberdxf:OrdinaryStockShareMember2017-12-280001499494dxf:VariableInterestEntityHubeiChutianMicrofinanceCoLtdMember2017-12-012017-12-280001499494dxf:VariableInterestEntityHubeiChutianMicrofinanceCoLtdMember2017-12-280001499494dxf:TrueSilverLimitedMember2017-12-012017-12-280001499494dxf:HongKongYiYouDigitalTechnologyDevelopmentCoLtdMember2023-01-012023-12-310001499494dxf:HongKongThreeDigitalTechnologyLimitedMember2023-01-012023-12-310001499494dxf:TrueSilverLimitedMember2023-01-012023-12-3100014994942017-12-2800014994942018-05-310001499494dxf:VariableInterestEntityMember2022-01-012022-12-310001499494dxf:VariableInterestEntityMember2023-01-012023-12-310001499494dxf:VariableInterestEntityMember2021-01-012021-12-310001499494dxf:VariableInterestEntityMember2023-12-310001499494dxf:VariableInterestEntityMember2022-12-310001499494dxf:HubeiChutianMicrofinanceCoLtdMember2023-01-012023-12-310001499494dxf:ShenzhenFourDivisionsGlobalIndustrialOperationCoLtdMember2023-01-012023-12-310001499494dxf:WuhanChutianInvestmentHoldingsCoLtdMember2023-01-012023-12-310001499494dxf:HongKongYiyouDigitalTechnologyDevelopmentCoLimitedMember2023-01-012023-12-310001499494dxf:HongKongThreeEntitiesDigitalTechnologyLimitedMember2023-01-012023-12-310001499494dxf:HongKongFourDivisionsInternationalLimitedMember2023-01-012023-12-310001499494dxf:ChutianFinancialHoldingsHongKongLimitedMember2023-01-012023-12-310001499494dxf:HubeiChutianMicrofinanceCoLtdMember2023-12-310001499494dxf:ShenzhenFourDivisionsGlobalIndustrialOperationCoLtdMember2023-12-310001499494dxf:WuhanChutianInvestmentHoldingsCoLtdMember2023-12-310001499494dxf:HongKongYiyouDigitalTechnologyDevelopmentCoLimitedMember2023-12-310001499494dxf:HongKongThreeEntitiesDigitalTechnologyLimitedMember2023-12-310001499494dxf:HongKongFourDivisionsInternationalLimitedMember2023-12-310001499494dxf:ChutianFinancialHoldingsHongKongLimitedMember2023-12-310001499494dxf:TrueSilverLimitedMember2023-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2023-12-310001499494dxf:TotalEquitiesMember2023-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2023-12-310001499494dxf:CurrencyTranslationReserveMember2023-12-310001499494dxf:GereralRiskReserveMember2023-12-310001499494ifrs-full:StatutoryReserveMember2023-12-310001499494dxf:AdditionalPaidInCapitalsMember2023-12-310001499494dxf:ShareCapitalMember2023-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2023-01-012023-12-310001499494dxf:TotalEquitiesMember2023-01-012023-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001499494dxf:CurrencyTranslationReserveMember2023-01-012023-12-310001499494dxf:GereralRiskReserveMember2023-01-012023-12-310001499494ifrs-full:StatutoryReserveMember2023-01-012023-12-310001499494dxf:AdditionalPaidInCapitalsMember2023-01-012023-12-310001499494dxf:ShareCapitalMember2023-01-012023-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2022-12-310001499494dxf:TotalEquitiesMember2022-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2022-12-310001499494dxf:CurrencyTranslationReserveMember2022-12-310001499494dxf:GereralRiskReserveMember2022-12-310001499494ifrs-full:StatutoryReserveMember2022-12-310001499494dxf:AdditionalPaidInCapitalsMember2022-12-310001499494dxf:ShareCapitalMember2022-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2022-01-012022-12-310001499494dxf:TotalEquitiesMember2022-01-012022-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001499494dxf:CurrencyTranslationReserveMember2022-01-012022-12-310001499494dxf:GereralRiskReserveMember2022-01-012022-12-310001499494ifrs-full:StatutoryReserveMember2022-01-012022-12-310001499494dxf:AdditionalPaidInCapitalsMember2022-01-012022-12-310001499494dxf:ShareCapitalMember2022-01-012022-12-3100014994942021-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2021-12-310001499494dxf:TotalEquitiesMember2021-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2021-12-310001499494dxf:CurrencyTranslationReserveMember2021-12-310001499494dxf:GereralRiskReserveMember2021-12-310001499494ifrs-full:StatutoryReserveMember2021-12-310001499494dxf:AdditionalPaidInCapitalsMember2021-12-310001499494dxf:ShareCapitalMember2021-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2021-01-012021-12-310001499494dxf:TotalEquitiesMember2021-01-012021-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001499494dxf:CurrencyTranslationReserveMember2021-01-012021-12-310001499494dxf:GereralRiskReserveMember2021-01-012021-12-310001499494ifrs-full:StatutoryReserveMember2021-01-012021-12-310001499494dxf:AdditionalPaidInCapitalsMember2021-01-012021-12-310001499494dxf:ShareCapitalMember2021-01-012021-12-3100014994942020-12-310001499494dxf:NoncontrollingInterestShareCapitalMember2020-12-310001499494dxf:TotalEquitiesMember2020-12-310001499494ifrs-full:AccumulatedOtherComprehensiveIncomeMember2020-12-310001499494dxf:CurrencyTranslationReserveMember2020-12-310001499494dxf:GereralRiskReserveMember2020-12-310001499494ifrs-full:StatutoryReserveMember2020-12-310001499494dxf:AdditionalPaidInCapitalsMember2020-12-310001499494dxf:ShareCapitalMember2020-12-3100014994942022-12-3100014994942022-01-012022-12-3100014994942021-01-012021-12-3100014994942023-12-310001499494dei:BusinessContactMember2023-01-012023-12-31iso4217:CNYiso4217:USDxbrli:sharesiso4217:CNYxbrli:sharesiso4217:HKDxbrli:pureiso4217:USDxbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 31, 2023

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from _______ to ___

Commission file number: 001-34958

DUNXIN FINANCIAL HOLDINGS LIMITED |

(Exact name of Registrant as specified in its charter) |

Not Applicable | | Cayman Islands |

(Translation of Registrant’s name into English) | | (Jurisdiction of incorporation or organization) |

27th Floor, Lianfa International Building

128 Xudong Road, Wuchang District

Wuhan City, Hubei Province 430063

People’s Republic of China

(Address of principal executive offices)

Mr. Ai (Kosten) Mei

Chief Executive Officer

Tel: +86-27-87303888

E-mail: contact@dunxin.us

27th Floor, Lianfa International Building

128 Xudong Road, Wuchang District

Wuhan City, Hubei Province 430063

People’s Republic of China

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | | Trading Symbol(s) | | Exchange on which registered |

Ordinary shares, par value $0.00005 per share | | DXF | | NYSE American LLC * |

American depositary shares, each representing 480 ordinary shares | | | | NYSE American LLC |

* Not for trading but only in connection with the listing on NYSE American LLC depositary shares.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2023: 10,232,461,723 Class A ordinary shares, par value $0.00005 per share; 512,232,237 Class B ordinary shares, par value US$0.00005 each.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company. See definition of “accelerated filer and large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ | Non-accelerated filer | ☒ |

| | | | Emerging growth company | ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ | | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ☐ No ☒

TABLE OF CONTENTS

CONVENTIONS THAT APPLY TO THIS ANNUAL REPORT

Unless otherwise indicated, references in this annual report to:

| ● | “ADRs” refer to the American depositary receipts that evidence our ADSs; |

| | |

| ● | “ADSs” refer to our American depositary shares, each ADS representing the right to receive four hundred and eighty (480) Class A ordinary shares, par value $0.00005 per share; |

| | |

| ● | “CBRC” refers to the China Banking Regulatory Commission; |

| | |

| ● | “China” or the “PRC” refers to the People’s Republic of China, excluding Taiwan, for the purpose of this annual report only; |

| | |

| ● | “CSRC” refers to the China Securities Regulatory Commission; |

| | |

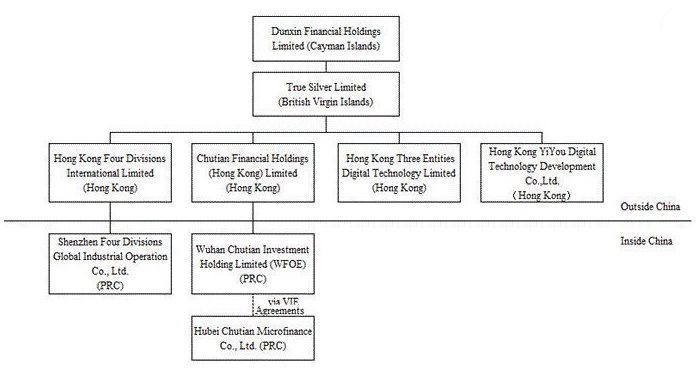

| ● | “Chutian” refers to Hubei Chutian Microfinance Co., Ltd., a PRC company, and a variable interest entity of the Company; |

| | |

| ● | “Chutian Holding” refers to Wuhan Chutian Investment Holding Limited, a PRC company and our wholly foreign owned enterprise with business license No. 91420100MA4KPA0H54; |

| | |

| ● | “Dunxin” refers to Dunxin Financial Holdings Limited, a Cayman Islands exempted company; |

| | |

| ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended; |

| | |

| ● | “Honest Plus” refers to Honest Plus Investments Limited, a British Virgin Islands company; |

| | |

| ● | “HK$” and “HKD” refer to the legal currency of Hong Kong; |

| | |

| ● | “Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China; |

| ● | “Hong Kong Four Divisions” refers to Hong Kong Four Divisions International Limited, a Hong Kong company; |

| | |

| ● | “Hong Kong Three Entities” refers to Hong Kong Three Entities Digital Technology Limited, a Hong Kong company; |

| | |

| ● | “Hong Kong Yiyou” refers to Hong Kong YiYou Digital Technology Development Co., Ltd., a Hong Kong company; |

| | ● | “IFRS” refers to International Financial Reporting Standards are issued by the International Accounting Standards Board (“IASB”); |

| | | |

| | ● | “Microfinance” refers to regulated private lending market for improving financial services to individuals, small and medium-sized enterprises (“SMEs”), expanding financing channels, making efforts to ease the difficulties in financing faced by SMEs and to encourage the innovation of financial products and services; |

| | | |

| | ● | “MOFCOM” refers to the Ministry of Commerce of People’s Republic of China; |

| | | |

| | ● | “PBOC” refers to the People’s Bank of China; |

| | | |

| | ● | “Perfect Lead” refers to Perfect Lead International Limited, a British Virgin Islands company; |

| | | |

| | ● | “RMB” and “Renminbi” refer to the legal currency of the People’s Republic of China; |

| | | |

| | ● | “SAFE” refers to the State Administration of Foreign Exchange; |

| | | |

| | ● | “SEC” refers to the Securities and Exchange Commission; |

| | | |

| | ● | “Securities Act” refers to the Securities Act of 1933, as amended; |

| | | |

| | ● | “Shares” or “ordinary shares” refer to our Class A ordinary shares, par value $0.00005 per share; |

| | |

| | ● | “Shenzhen Four Divisions” refers to Shenzhen Four Divisions Global Industry Management Co., Ltd, a PRC company; |

| | |

| | ● | “True Silver” refers to True Silver Limited, a British Virgin Islands company; |

| | | |

| | ● | “U.S. dollars,” “US$” and “$” refer to the legal currency of the United States; |

| | | |

| | ● | “VIE” refers to variable interest entity, Hubei Chutian Microfinance Co., Ltd., a PRC company and the operating company of Dunxin; and |

| | | |

| | ● | “we,” “us,” “our,” or the “Company” refers to Dunxin Financial Holdings Limited and its subsidiaries, unless the context requires otherwise. When used herein to describe events prior to the CIB Transaction, the terms “Company,” “Xiniya,” “we” and “us” refers to Dunxin Financial Holdings Limited (formerly known as China Xiniya Fashion Limited) and its consolidated subsidiaries before such time. |

Presentation of Our Financial and Operating Data

On December 28, 2017, Honest Plus acquired 91,997,543 Shares and Perfect Lead acquired 22,999,386 Shares for an aggregate purchase price of RMB86,426,660 (or approximately $0.11 per share) pursuant to a Share Purchase Agreement, as amended on October 27, 2016, and on December 10, 2017 (the “Share Purchase Agreement”), by and between Qiming Investment Limited, a British Virgin Islands company (“Qiming Investment”), Qiming Xu, the chairman and chief executive officer of Xiniya (“Mr. Qiming Xu”), Honest Plus, and Perfect Lead. Ricky Qizhi Wei, our former chairman and chief executive officer, is the sole director of Honest Plus and Perfect Lead.

As a condition to the Share Purchase Agreement, on December 10, 2017, Xiniya entered into (1) a Share Transfer Agreement with Qiming Investment pursuant to which Xiniya sold Xiniya Holdings Limited, Xiniya’s wholly-owned subsidiary in Hong Kong, to Mr. Qiming Xu in exchange for a purchase price of RMB228,000,000 (approximately $34,588,428) (“Divestiture”), and (2) a Securities Purchase Agreement with True Silver, a British Virgin Islands company, and Honest Plus pursuant to which Xiniya acquired all of the issued and outstanding shares of True Silver owned by Honest Plus for a purchase price of RMB228,000,000 ($34,588,428) and the issuance of 772,283,308 Shares (the “Acquisition”) at RMB1.00 ($0.15) per share. True Silver, through a VIE structure, operates and consolidates eighty percent (80%) of the financial results of Chutian, a Chinese company that engages in the business of micro lending to customers in China. On December 28, 2017, the Divestiture and the Acquisition closed concurrently with the closing of the Share Purchase Agreement (collectively, the “CIB Transaction”). At the closing of the CIB Transaction, the Company discontinued its apparel business and became a microfinance lender in Hubei Province.

As a result of the CIB Transaction, Honest Plus and Perfect Lead, the former shareholders of True Silver, became the shareholders of the Company. The CIB Transaction was accounted for as a reverse acquisition, wherein True Silver is considered the acquirer for accounting and financial reporting purposes.

Accordingly and except as otherwise provided, the historical financial statement of True Silver are treated as the historical financial statements of the Company.

This annual report includes our audited consolidated statements of profit and other comprehensive income data for the years ended December 31, 2021, 2022 and 2023, and consolidated statements of financial position data as of December 31, 2022 and 2023.

Dunxin’s predecessor, China Xiniya Fashion Limited, completed the initial public offering of 8,000,000 ADSs, each representing the right to receive four (4) ordinary shares, on November 29, 2010. On November 23, 2010, we listed our ADSs on the New York Stock Exchange under the symbol “XNY” and on December 28, 2017, we transitioned to the NYSE American LLC (“NYSE American”) and began trading under our new symbol “DXF” on March 5, 2018. Prior to December 17, 2014, each ADS represented the right to receive four (4) Shares, from December 18, 2014, the right to receive sixteen (16) Shares, from December 28, 2017, the right to receive forty-eight (48) Shares and from July 25, 2023, the right to receive four hundred and eighty (480) Shares..

Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report are made at a rate of RMB7.0999 to $1.00, the exchange rate in effect as of December 31, 2023 as set forth in the H.10 statistical release of The Board of Governors of the Federal Reserve System. Unless otherwise noted, all other financial and other data related to the company in this annual report is presented in U.S. dollars. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade. This annual report contains translations of certain foreign currency amounts into U.S. dollars for the convenience of the reader.

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements, within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act with respect to our business, operating results and financial condition as well as our current expectations, assumptions, estimates and projections about our industry. All statements other than statements of historical fact in this annual report are forward-looking statements. These statements relate to events that involve known and unknown risks, uncertainties and other factors, including those listed under “Risk Factors,” which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements.

In some cases, these forward-looking statements can be identified by words or phrases such as “aim,” “predict,” “anticipate,” “believe,” “continue,” “estimate,” “expect,” “intend,” “is/are likely to,” “could,” “may,” “plan,” “potential,” “will” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, among other things, statements relating to:

| ● | the potential impact of the economic, political and social conditions of the PRC on our business; |

| | |

| ● | any changes in the laws of the PRC or local province that may affect our operation; |

| | |

| ● | the impact of COVID-19 on our operations and business plans; |

| | |

| ● | inflation and fluctuations in foreign currency exchange rates; |

| | |

| ● | our ability to operate as a going concern; |

| | |

| ● | the liquidity of our securities; |

| | |

| ● | our ability to develop and market our microfinance lending business in the future; |

| ● | our exposure to risk associated to the geographic concentration of loans in Hubei Province, China; |

| | |

| ● | our on-going ability to obtain all mandatory and voluntary government and other industry certifications, approvals, and/or licenses to conduct our business; |

| | |

| ● | our ability to collect loan principal and interest timely and effectively and to pay our debt timely; |

| | |

| ● | our ability to maintain effective internal control over financial reporting; |

| | |

| ● | our ability to maintain or increase our market share in the competitive markets in which we do business; |

| | |

| ● | our dependence on the growth in demand for our loan products; |

| | |

| ● | our ability to diversify our product offerings and capture new market opportunities; |

| | |

| ● | the costs and losses we may incur as a result of current ongoing and future litigation and claims; |

| | |

| ● | our estimates of expenses, capital requirements and needs for additional financing and our ability to fund our current and future operations; |

| | |

| ● | the costs we may incur in the future from complying with current and future governmental regulations and the impact of any changes in the regulations on our operations; and |

| | |

| ● | the loss of key members of our senior management. |

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we reference in this annual report and/or file as exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Investing in our securities is highly speculative and involves a significant degree of risk. You should carefully consider the following risks as well as all other information contained in this annual report, including the matters discussed under the headings “Forward-Looking Statements” and “Operating and Financial Review and Prospects” before you decide to make an investment in our securities. Dunxin is a Cayman Islands holding company with substantial operations in China and is subject to a legal and regulatory environment that in many respects differs from the United States. The risks discussed below could materially and adversely affect our business, prospects, financial condition, results of operations, cash flows, ability to pay dividends and the trading price of our ordinary shares. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, prospects, financial condition, results of operations, cash flows and ability to pay dividends, and you may lose all or part of your investment.

RISK FACTORS SUMMARY

Our business is subject to numerous risks described in the section titled “Risk Factors” and elsewhere in this annual report. The main risks set forth below and others you should consider are discussed more fully in the section entitled “Risk Factors” beginning on page 6, which you should read in its entirety.

Risks Related to Doing Business in China

We face risks and uncertainties relating to doing business in China in general, including, but not limited to, the following:

| ● | Changes in China’s economic, political or social conditions or government policies or in relations between China and the United States could have a material adverse effect on our business, financial condition and operations; and may result in our inability to sustain our growth and expansion strategies; |

| | |

| ● | There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations, which could result in a material adverse change in our operations and the value of our ADSs; |

| | |

| ● | The PRC government has increasingly strengthened oversight in offerings conducted overseas or on foreign investment in China-based issuers, which could significantly limit or completely hinder our ability to offer or continue to offer our securities to investors and could cause the value of our securities to significantly decline or become worthless; |

| | |

| ● | The approval and/or other requirements of the CSRC or other PRC governmental authorities may be required in connection with an offering under PRC rules, regulations or policies, and, if required, we cannot predict whether or how soon we will be able to obtain such approval. Any failure to obtain or delay in obtaining the requisite governmental approval for an offering, or a rescission of such approval, would subject us to sanctions imposed by the relevant PRC regulatory authority; |

| | |

| ● | The PRC government’s significant oversight over our business operation could result in a material adverse change in our operations and the value of our ADSs. The Chinese government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or become worthless; and |

| | |

| ● | Our ADSs may be delisted under the Holding Foreign Companies Accountable Act if the PCAOB is unable to inspect auditors who are located in China. The delisting of our ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment. Additionally, the inability of the PCAOB to conduct inspections deprives our investors with the benefits of such inspections. |

| | |

| ● | All of our officers and our Chairman reside within China and substantially all of the assets of those persons are located outside of the United States. It may be difficult for investors to enforce judgments obtained in U.S. courts based on civil liability provisions of the U.S. federal securities laws against us and our officers and directors, as none of them currently resides in the U.S. or has substantial assets in the U.S. |

Risks Factors Related to Our Business

Risks and uncertainties related to our business and industry include, but not limited to, the following:

| ● | Current ongoing litigation and future litigation, administrative proceedings or legal proceedings resulting from our lending business and liquidity issues have had, may continue to have, a material adverse effect on our lending business, financial conditions and operating results; |

| | |

| ● | We have experienced and continue to experience severe liquidity issues resulting from our inability to timely collect payments of loan principal and interest as well as assets and cash being frozen as a result of involvement in various litigation. Our liquidity issues have further severely affected our ability to pay taxes, service providers, employees and others. Due to non-payment of our obligations when due, multiple significant legal proceedings against us were initiated by our shareholders, service providers and others; |

| | |

| ● | COVID-19 pandemic has adversely affected, and may continue to adversely affect, our financial and operating performance; |

| | |

| ● | We have experienced an increase in delinquency rates on loans from borrowers since 2019, which have materially and adversely affected our business and results of operations; |

| ● | Our failure to pay taxes may result in penalties, which may materially and adversely affect our business, financial condition and results of operation; |

| | |

| ● | Our independent auditors have expressed substantial doubt about our ability to continue as a going concern; |

| | |

| ● | If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud; |

| | |

| ● | Our limited operating history makes it difficult to evaluate our business and prospects; |

| | |

| ● | Potential dispute over ownership of our main operating company may adversely affect our business; |

| | |

| ● | We have very limited cash and we need additional capital which, if obtained, could result in dilution or significant debt service obligations. We may not be able to obtain additional capital on commercially reasonable terms, which could adversely affect our liquidity and financial position; |

| | |

| ● | Our microfinance business is subject to extensive regulation and supervision by state, provincial and local government authorities, and we do not strictly adhere to one of the principles under Measures for Administration of Pilot Scheme on Microfinance Companies in Hubei Province, and may be deemed not be in compliance with the provincial local regulatory policies; |

| | |

| ● | Our current operations in China are territorially limited to the Hubei Province and Shenzhen, and we lack product and business diversification; |

Risks Related to Our Corporate Structure

We are also subject to risks and uncertainties related to our corporate structure, including, but not limited to, the following:

| ● | Dunxin is a Cayman Islands holding company with no equity ownership in the VIE and we conduct our operations in China primarily through the VIE with which we have maintained contractual arrangements. Investors in our ADSs thus are not purchasing equity interest in the VIE in China but instead are purchasing equity interest in a Cayman Islands holding company. If the PRC government finds that the a series of contractual arrangements entered into among True Silver, Chutian and certain shareholders of Chutian, which consist of the Exclusive Consigned Management Service Agreement, Exclusive Purchase Option Agreement, Shareholders’ Voting Proxy Agreement, and Share Pledge Agreement (the “VIE Agreements”) that establish the structure for the VIE in China do not comply with PRC laws and regulations, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or we be forced to relinquish our interests in the VIE. Our holding company in the Cayman Islands, our PRC subsidiary, the VIE, and investors of Dunxin face uncertainty about potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIE and, consequently, significantly affect the financial performance of the VIE and the Company as a whole; |

| ● | We rely on contractual arrangements with the VIE and its shareholders for our business operations, and these contractual arrangements may not be as effective as direct ownership in providing control over the VIE. We rely on the performance by the VIE and its shareholders of their obligations under the contracts to exercise control over the VIE. The shareholders of the VIE may not act in the best interests of Dunxin or may not perform their obligations under these contracts. Such risks exist throughout the period in which we intend to operate certain portion of our business through the contractual arrangements with the VIE; |

| | |

| ● | Any failure by the VIE or its shareholders to perform their obligations under the contractual arrangements with them would have a material adverse effect on our business. If the VIE or its shareholders fail to perform their respective obligations under the contractual arrangements, we may have to incur substantial costs and expend additional resources to enforce such arrangements. We may also have to rely on legal remedies under PRC law, including seeking specific performance or injunctive relief, and claiming damages, which we cannot assure you will be effective under PRC law; |

| | |

| ● | The shareholders of the VIE may have actual or potential conflicts of interest with us, which may materially and adversely affect our business and financial condition. The shareholders of the VIE may breach, or cause the VIE to breach, or refuse to renew, the existing contractual arrangements we have with them and the VIE, which would have a material adverse effect on the Company’s ability to effectively control the VIE and receive economic benefits from them. If we cannot resolve any conflict of interest or dispute between us and these shareholders, we would have to rely on legal proceedings, which could result in disruption of our business and subject us to substantial uncertainty as to the outcome of any such legal proceedings; |

| | |

| ● | The Company’s current corporate structure and business operations may be affected by the newly enacted PRC Foreign Investment Law which does not explicitly classify whether VIEs that are controlled through contractual arrangements would be deemed as foreign-invested enterprises if they are ultimately “controlled” by foreign investors; |

| | |

| ● | We rely on contractual arrangements with the VIE and its shareholders to operate our business, which may not be as effective as direct ownership in providing operational control and otherwise have a material adverse effect as to our business; and |

| | |

| ● | Any failure by the VIE or its shareholders to perform their obligations under the Company’s contractual arrangements with them would have a material adverse effect on our business. |

Risks Related to our Ordinary Shares and ADSs

We face risks and uncertainties related to our ordinary shares and ADSs, including, but not limited to, the following:

| ● | The trading prices of our ADSs are likely to be volatile, which could result in substantial losses to investors; |

| | |

| ● | If securities or industry analysts publish negative reports about our business, the price and trading volume of our ADSs could decline; |

| | |

| ● | Our ADSs would be subject to delisting from the NYSE American if we are unable to achieve and maintain compliance with the NYSE American’s continued listing standards; |

| | |

| ● | Substantial future sales or perceived sales of our ADSs in the public market could cause the price of our ADSs to decline; |

| ● | Our articles of association contain anti-takeover provisions that could have a material adverse effect on the rights of holders of our ADSs and ordinary shares; |

| | |

| ● | You may not receive dividends or other distributions on our ordinary shares and you may not receive any value for them, if it is illegal or impractical to make them available to you; and |

| | |

| ● | Your right to participate in any future rights offerings may be limited, which may cause dilution to your holdings and you may not receive distributions with respect to the underlying ordinary shares if it is impractical to make them available to you. |

There are many risks and uncertainties that may affect our operations, performance, development and results. Many of these risks are beyond our control. The following is a description of the important risk factors that may affect our business. If any of these risks were to actually occur, our business, financial condition or results of operations could be materially adversely affected. Additional risks and uncertainties not currently known to us or that we currently consider to be immaterial may also materially adversely affect our business, financial condition or results of operations.

Risks Related to Doing Business in China

Substantial uncertainties and restrictions with respect to the political and economic policies of the PRC government and PRC laws and regulations could have a significant impact upon the business we may be able to conduct in the PRC and accordingly on the results of our operations and financial condition.

Our business operations may be adversely affected by the current and future political environment in the PRC. The Chinese government exerts substantial influence and control over the manner in which we must conduct our business activities. Our ability to operate in China may be adversely affected by changes in Chinese laws and regulations. Under the current government leadership, the government of the PRC has been pursuing economic reform policies that encourage private economic activities and greater economic decentralization. However, the government of the PRC may not continue to pursue these policies, or may significantly alter these policies from time to time without notice.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including, but not limited to, the laws and regulations governing our business, or the enforcement and performance of our arrangements with borrowers in the event of the imposition of statutory liens, death, bankruptcy or criminal proceedings. Only after 1979 did the Chinese government begin to promulgate a comprehensive system of laws that regulate economic affairs in general, deal with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade, as well as encourage foreign investment in China. Although the influence of the law has been increasing, China has not developed a fully integrated legal system and recently enacted laws and regulations may not sufficiently cover all aspects of economic activities in China. Also, because these laws and regulations are relatively new, and because of the limited volume of published cases and judicial interpretation and their lack of force as precedents, interpretation and enforcement of these laws and regulations involve significant uncertainties. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. In addition, there have been constant changes and amendments of laws and regulations over the past 30 years in order to keep up with the rapidly changing society and economy in China. Because government agencies and courts provide interpretations of laws and regulations and decide contractual disputes and issues, their inexperience in adjudicating new business and new polices or regulations in certain less developed areas causes uncertainty and may affect our business. Consequently, we cannot clearly foresee the future direction of Chinese legislative activities with respect to either businesses with foreign investment or the effectiveness on enforcement of laws and regulations in China. The uncertainties, including new laws and regulations and changes of existing laws, as well as judicial interpretation by inexperienced officials in the agencies and courts in certain areas, may cause possible problems to foreign investors.

The Second Session of the Thirteen National People’s Congress of the People’s Republic of China voted to adopt the Foreign Investment Law of the People’s Republic of China (“the Foreign Investment Law”) on March 15, 2019 which came into effective as of January 1, 2020. The current three major foreign investment laws (the Sino-Foreign Equity Joint Venture Law, Sino-Foreign Cooperative Joint Venture Law and Wholly Foreign Owned Enterprise Law) were replaced by the Foreign Investment Law on January 1, 2020.

The Foreign Investment Law expressly stipulated that “the State protects foreign investors’ investment, earnings and other legitimate rights and interests within the territory of China pursuant to the present Law”; “foreign investors may, according to the present Law, freely remit into or out of China, in Renminbi or any other foreign currency, their contributions, profits, capital gains, income from asset proposal, intellectual property royalties, lawfully acquired compensation, indemnity or liquidation income and so on within the territory of China”; “Foreign investors shall not invest in any field with investment prohibited by the negative list for foreign investment access. Foreign investors shall meet the investment conditions stipulated under the negative list for any field with investment restricted by the negative list for foreign investment access”; “In formulating normative documents concerning foreign investment, the people’s governments at all levels and their departments concerned shall comply with laws and regulations, and if there are no laws or administrative regulations to serve as the basis, they shall not impair foreign-funded enterprises’ legitimate rights and interests or increase their obligations, set any market access and exit conditions, or intervene the normal production and operation activities of any foreign-funded enterprise.”

The Foreign Investment Law leaves uncertainty with respect to whether foreign investors-controlled PRC onshore variable interest entities via contractual arrangements will be recognized as “foreign investment”. Although the Foreign Investment Law clearly stipulates: “The state implements the management system of pre-establishment national treatment plus negative list for foreign investment. ... Negative list refers to the quasi-special management measures for foreign investment in specific fields stipulated by the state. The state grants national treatment to foreign investment that is not on the negative list.” The VIE model or VIE structure will continue to exist according to the principle of “access if it is not prohibited”. If our control over the VIE through contractual arrangements are deemed as foreign investment in the future, and any business of the VIE is restricted or prohibited from foreign investment under the “negative list” effective at the time, we may be deemed to be in violation of the Foreign Investment Law, the contractual arrangements that allow us to have control over the VIE may be deemed as invalid and illegal, and we may be required to unwind such contractual arrangements and/or restructure our business operations, any of which may have a material adverse effect on our business operation and financial conditions.

The PRC government exerts substantial influence over the manner in which we conduct our business activities. The PRC government may also intervene or influence our operations at any time, which could result in a material change in our operations and our ADSs could decline in value or become worthless.

We are currently not required to obtain approval from Chinese authorities for the VIE Agreements; however, if the VIE or the holding company were required to obtain approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange, continue to offer securities to investors, and that will materially affect the interest of the investors and cause significantly depreciation of our price of ADSs.

The Chinese government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to taxation, environmental regulations, land use rights, property and other matters. The central or local governments of these jurisdictions may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations. Accordingly, government actions in the future, including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy or regional or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular regions thereof, and could require us to divest ourselves of any interest we then hold in our operations in China.

For example, the Chinese cybersecurity regulator announced on July 2, 2021, that it had begun an investigation of Didi Global Inc. (NYSE: DIDI) and two days later ordered that the company’s app be removed from smartphone app stores. Similarly, our business segments may be subject to various government and regulatory interference in the regions in which we operate. We could be subject to regulation by various political and regulatory entities, including various local and municipal agencies and government sub-divisions. We may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply.

Furthermore, it is uncertain when and whether we will be required to obtain permission from the PRC government for any securities offerings that are conducted in the United States or enter into VIE Agreements in the future, and even when such permission is obtained, whether it will be denied or rescinded. Although we are currently not required to obtain permission from any of the PRC federal or local government to obtain such permission and has not received any denial for or entering into VIE Agreements, our operations could be adversely affected, directly or indirectly, by existing or future laws and regulations relating to our business or industry. Recent statements by the Chinese government indicating an intent, and the PRC government may take actions to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. On February 17, 2023, China Securities Regulatory Commission issued the “Trial Measures for the Management of Overseas Issuance and Listing of Securities by Domestic Enterprises” and supporting regulatory guidelines, marking the formal shift to the filing system of overseas listing of domestic enterprises. Filing is only to increase supervision, does not represent serious restrictions or obstacles to Chinese enterprises in overseas listed investment business. These actions could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or become worthless.

Our microfinance business is subject to extensive regulation and supervision by state, provincial and local government authorities, which may interfere with the way we conduct our business and may negatively impact our financial results.

We are subject to extensive and complex state, provincial and local laws, rules and regulations with regard to our loan operations, capital structure, and allowance for loan losses, among other things. These laws, rules and regulations are issued by different central government ministries and departments, provincial and local governments while enforced by different local authorities.

In addition, it is not clear whether microfinance companies are subject to certain banking regulations that the state-owned and commercial banks are subject to, including the regulation with regard to loan loss reserves. Therefore the interpretation and implementation of such laws, rules and regulations may not be clear and occasionally we have to depend on oral inquiries with local government authorities. As a result of the complexity, uncertainties and constant changes in these laws, rules and regulations, including changes in interpretation and implementation of such, our business activities and growth may be adversely affected if we do not respond to the changes in a timely manner or are found to be in violation of the applicable laws, regulations and policies as a result of a different position from ours taken by the competent authority in the interpretation of such applicable laws, regulations and policies. If we were found not to be in compliance with these laws and regulations, we may be subject to sanctions by regulatory authorities, monetary penalties and/or reputation damage, which could have a material adverse effect on our business operation and profitability.

Fluctuations in the foreign currency exchange rate between U.S. Dollars and Renminbi could adversely affect our financial condition.

The value of the RMB against the U.S. dollar and other currencies may fluctuate. Exchange rates are affected by, among other things, changes in political and economic conditions and the foreign exchange policy adopted by the PRC government. On July 21, 2005, the PRC government changed its policy of pegging the value of the RMB to the U.S. dollar. Under the new policy, the RMB is permitted to fluctuate within a narrow and managed band against a basket of foreign currencies. Following the removal of the U.S. dollar peg, the RMB appreciated more than 20% against the U.S. dollar over three years. From July 2008 until June 2010, however, the RMB traded stably within a narrow range against the U.S. dollar. There remains significant international pressure on the PRC government to adopt a more flexible currency policy, which could result in a further and more significant appreciation of the RMB against foreign currencies. On June 20, 2010, the PBOC announced that the PRC government would reform the RMB exchange rate regime and increase the flexibility of the exchange rate. On August 11, 2015, the PBOC led central parity quoting banks to further improve the formation mechanism of the RMB against the US dollar, indicating that the central parity quoting price shall be decided with reference to the closing price on the previous trading day. On December 11, 2015, the China Foreign Exchange Trade System launched the RMB exchange-rate index, which strengthened the reference to a currency basket to better maintain the stability of the RMB exchange rate against the currencies in the basket. As a result, the CNY/USD central parity formation mechanism of “closing rate + exchange-rate movements of a basket of currencies” was developed. In June 2016, the Foreign Exchange Self-Disciplinary Mechanism was established, allowing financial institutions to play a more important role in maintaining orderly operations in the foreign-exchange market and in an environment for fair competition. In February 2017, the Foreign Exchange Self-Disciplinary Mechanism adjusted the reference period for the central parity against the currency basket from 24 hours ahead of submitting the quotes to 15 hours between the closing on the previous trading day and the submission of the quotes, which avoided repeated references to the daily movements of the USD exchange rate in the central parity of the following day. According to the Annual Report on Exchange Rate Arrangements and Exchange Restrictions (2019), which was published in August 2020 by the International Monetary Fund China’s exchange rate regime was classified as “other management floating arrangements” (comparing to prior to June 2018, which was classified as “crawl-like arrangements”). This exchange rate arrangement has medium to high intensive elasticity. In fact, the current daily fluctuation range of the RMB exchange rate against the US dollar limits to 2% up and down, and the formation mechanism of the intermediate exchange rate is not completely marketized. The flexibility of the RMB exchange rate against the US dollar may exhibit farther two-way fluctuations. We cannot predict how this new policy and mechanism will affect the RMB exchange rate.

Our revenues and costs are mostly denominated in the RMB, and substantially all of our financial assets are also denominated in the RMB. Any significant fluctuations in the exchange rate between the RMB and the U.S. dollar may materially adversely affect our cash flows, revenues, earnings and financial position, and the amount of and any dividends we may pay on our ordinary shares in U.S. dollars. In addition, any fluctuations in the exchange rate between the RMB and the U.S. dollar could result in foreign currency translation losses for financial reporting purposes.

You may face difficulties in protecting your interests and exercising your rights as a shareholder since we conduct all of our operations in China, and all of our officers and our Chairman reside outside the United States. It may also be difficult for you or overseas regulators to conduct investigations or collect evidence within China.

Dunxin was incorporated in the Cayman Islands and we conduct most of our operations in China through Chutian, the VIE in China. In addition, all of our officers and our chairman reside outside the United States and substantially all of the assets of those persons are located outside of the United States. As a result, it may be difficult for you to conduct due diligence on the business or attend shareholders meetings if such meetings are held in China, and it may be difficult for you to effect service of process upon those persons inside mainland China. It may be difficult for you to enforce judgments obtained in U.S. courts based on civil liability provisions of the U.S. federal securities laws against us and our officers and directors, as none of them currently resides in the U.S. or has substantial assets in the U.S. As a result of all of the above, our public shareholders may have more difficulty in protecting their interests through actions against our management, or major shareholders than would shareholders of a corporation doing business entirely or predominantly within the United States. In addition, there is uncertainty as to whether the courts of the Cayman Islands or the PRC would recognize or enforce judgments of U.S. courts against us or such persons predicated upon the civil liability provisions of the securities laws of the United States or any state.

The recognition and enforcement of foreign judgments are provided for under the PRC Civil Procedures Law. PRC courts may recognize and enforce foreign judgments in accordance with the requirements of the PRC Civil Procedures Law based either on treaties between China and the country where the judgment is made or on principles of reciprocity between jurisdictions. China does not have any treaties or other forms of written arrangement with the United States that provide for the reciprocal recognition and enforcement of foreign judgments. In addition, according to the PRC Civil Procedures Law, the PRC courts will not enforce a foreign judgment against us or our directors and officers if they decide that the judgment violates the basic principles of PRC laws or national sovereignty, security, or public interest. As a result, it is uncertain whether and on what basis a PRC court would enforce a judgment rendered by a court in the United States.

In 2017, Wuhan Intermediate People's Court in Wuhan, where the city Chutian, the VIE in China located, recognized for the first time the validity of a commercial judgment made by an American court in accordance with the principle of reciprocity.

It may also be difficult for you or overseas regulators to conduct investigations or collect evidence within China. For example, in China, there are significant legal and other obstacles to obtaining information needed for shareholder investigations or litigation outside China or otherwise with respect to foreign entities. Although the authorities in China may establish a regulatory cooperation mechanism with its counterparts of another country or region to monitor and oversee cross-border securities activities, such regulatory cooperation with the securities regulatory authorities in the United States may not be efficient in the absence of a practical cooperation mechanism. Furthermore, according to Article 177 of the PRC Securities Law, or “Article 177,” which became effective in March 2020, no overseas securities regulator is allowed to directly conduct investigations or evidence collection activities within the territory of the PRC. Article 177 further provides that Chinese entities and individuals are not allowed to provide documents or materials related to securities business activities to foreign agencies without prior consent from the securities regulatory authority of the State Council and the competent departments of the State Council. While detailed interpretation of or implementing rules under Article 177 have yet to be promulgated, the inability for an overseas securities regulator to directly conduct investigation or evidence collection activities within China may further increase difficulties faced by you in protecting your interests.

A severe and prolonged global financial crisis, or economic recession and the slowdown in the Chinese economy may adversely affect our business, results of operations and financial condition.

We operate our business in the PRC. The growth of the Chinese economy has slowed down since 2012 compared to the previous decade and the trend may continue. According to the National Bureau of Statistics of China, China’s gross domestic product (GDP) growth was 5.2% in 2023. There is considerable uncertainty over the long-term effects of the monetary and fiscal policies adopted by the central banks and financial authorities of some of the world’s leading economies, including the United States and China. In addition, there have also been concerns on the relationship between China and the U.S. following rounds of tariffs imposed by the U.S and retaliatory tariffs imposed by China. It is unclear whether these challenges and uncertainties will be contained or resolved, and what effects they may have on the global political and economic conditions in the long term. Economic conditions in China are sensitive to global economic conditions, as well as changes in domestic economic and political policies and the expected or perceived overall economic growth rate in China. Any prolonged slowdown in the global or Chinese economy may have a negative impact on our business, results of operations and financial condition, and continued turbulence in the international markets may adversely affect our ability to access the capital markets to meet liquidity needs in a number of ways, including:

| ● | we may face severe challenges, loss of customers and other operation risks during the global financial crisis and economic downturn; |

| | |

| ● | under difficult economic conditions, borrowers may seek to reduce the loan size or discontinue borrowings; and |

| | |

| ● | financing and other sources of liquidity may not be available on reasonable terms or at all. |

These risks may be exacerbated in the event of a prolonged economic downturn or financial crisis. Our customers may reduce or delay their borrowings, while we may have difficulty expanding our borrowers fast enough, or at all, to offset the impact of decreased loans. In addition, to the extent borrowers’ experiences financial difficulties due to the economic slowdown, we could have difficulty collecting payment from the borrower.

Any adverse changes in political policies of the PRC government could negatively impact China’s overall economic growth, which could materially adversely affect our business.

Dunxin is a holding company with substantial operations in the PRC. China’s economy differs from the economies of most other countries in many respects, including the amount of government involvement in the economy, the general level of economic development, growth rates and government control of foreign exchange and the allocation of resources. The PRC government exercises significant control over China’s economic growth by allocating resources, controlling the payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies. Any actions and policies adopted by the PRC government could negatively impact the Chinese economy, which could materially adversely affect our business.

China moves to liberalize interest rates and deposit rates may create more competition.

China has been slowly liberalizing its interest rate and deposit rate policies to a market driven policy to try to move away from a policy based on artificially imposed ceiling or floor to a market system policy-based market demands for financial services. This marketization of interest rates and deposit rates may result in increased competition from banks and competitors and the narrowing of the interest rate spread for loan products which may materially adversely affect our business and results of operations.

Future inflation in China may inhibit economic activity and adversely affect our operations.

The Chinese economy has experienced periods of rapid expansion in recent years which can lead to high rates of inflation or deflation. This has caused the PRC government to, from time to time, enact various corrective measures designed to restrict the availability of credit or regulate growth and contain inflation. High inflation may in the future cause the PRC government to once again impose controls on credit and/or prices, or to take other action, which could inhibit economic activity in China. Any action on the part of the PRC government that seeks to control credit and/or prices may materially adversely affect our business operations.

PRC regulation of loans to, and direct investments in, PRC entities by offshore holding companies may delay or prevent Dunxin from using proceeds from future financing activities to make loans or additional capital contributions to its PRC operating subsidiary.

As an offshore holding company with PRC subsidiary, Dunxin may transfer funds to its PRC subsidiary or finance its operating entity by means of shareholder loans or capital contributions. Any loans to Dunxin’s PRC subsidiary, which are foreign-invested enterprises, shall be limited to within the margin between the total investment and registered capital approved by the examination and approval authorities. Within the scope of the aforementioned margin foreign-invested enterprises may voluntarily contract foreign debts. Where the margin is exceeded, the original examination and approval authorities shall re-conduct appraisal and determination of total investment. Such loan shall be registered with SAFE, or its local counterparts. Furthermore, any capital increase contributions we make to the Company’s PRC subsidiary, which are foreign-invested enterprises, shall be subject to record-filing via the Comprehensive Management System of the MOFCOM. We may not be able to obtain these government registrations or approvals on a timely basis, if at all. If we fail to receive such registrations or approvals, our ability to provide loans or capital increase contributions to the Company’s PRC subsidiary may be negatively affected, which could adversely affect our liquidity and our ability to fund and expand our business.

In addition, SAFE promulgated a Notice on Further Improving and Adjusting the Foreign Exchange Administration Policies on Direct Investments on November 19, 2012, or Circular 59, as amended on May 4, 2015, which requires the authenticity of settlement of net proceeds from offshore offerings to be closely examined and the net proceeds to be settled in the manner described in the offering documents. Furthermore, SAFE promulgated a Notice on Reforming the Administrative Approach Regarding the Settlement of the Foreign Exchange Capitals of Foreign-invested Enterprises, or Circular 19 (partially invalid on December 30, 2019), promulgated on March 30, 2015 and taken effect from June 1, 2015, pursuant to which the foreign-invested enterprises shall be allowed to settle their foreign exchange capitals on a discretionary basis, the RMB funds obtained by foreign-invested enterprises from the discretionary settlement of their foreign exchange capitals shall be managed under the accounts for foreign exchange settlement pending payment, and a foreign-invested enterprise shall truthfully use its capital for its own operational purposes within the scope of business and it shall not, unless otherwise prescribed by laws and regulations use the foregoing funds for investment in securities etc. Besides, SAFE further promulgated a Notice on Reforming and Standardizing the Administrative Provisions on Capital Account Foreign Exchange Settlement, or Circular 16, on June 9, 2016, according to which a domestic institution shall use foreign exchange earnings under capital account within its business scope and in a truthful manner for proprietary purposes and a bank shall not process foreign exchange settlement or payment formalities for a domestic institution that applies for the payment and settlement of all of its foreign exchange earnings under capital account in one lump-sum or the payment of all RMB funds in its Account for Foreign Exchange Settlement Pending Payment, if the domestic institution is unable to provide relevant materials in proof of transaction authenticity.

Circular 59, Circular 19 and Circular 16 may significantly limit our ability to effectively use the proceeds from future financing activities as the Wholly Foreign Owned Enterprise (“WFOE”) may not convert the funds received from us in foreign currencies into RMB or may not use the RMB funds obtained from foreign exchange settlement for certain purposes, which may materially adversely affect our liquidity and our ability to fund and expand our business in the PRC.

The disclosures in our reports and other filings with the SEC and our other public pronouncements are not subject to the scrutiny of any regulatory bodies in the PRC.