false

2024

FY

--12-31

0001460235

0001460235

2024-01-01

2024-12-31

0001460235

2024-06-30

0001460235

2025-02-26

0001460235

2024-12-31

0001460235

2023-12-31

0001460235

2023-01-01

2023-12-31

0001460235

pplt:PlatinumMember

2024-12-31

0001460235

pplt:PlatinumMember

2023-12-31

0001460235

2022-01-01

2022-12-31

0001460235

2022-12-31

0001460235

2021-12-31

0001460235

us-gaap:FairValueInputsLevel1Member

2024-12-31

0001460235

us-gaap:FairValueInputsLevel1Member

2023-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

utr:oz

xbrli:pure

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form

10-K

| ☒ |

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2024 |

or

| ☐ |

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the Transition Period from

to

|

Commission

File Number: 001-34590

abrdn

Platinum ETF Trust

(Exact

name of registrant as specified in its charter)

| New

York |

|

26-4732885 |

(State

or other jurisdiction of incorporation or organization) |

|

(I.R.S.

Employer Identification No.) |

| c/o

abrdn ETFs Sponsor LLC |

|

|

1900

Market Street, Suite 200

Philadelphia,

PA

|

|

19103

|

(Address

of principal executive offices) |

|

(Zip

Code) |

(844)

383-7289

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| abrdn

Physical Platinum Shares ETF |

|

PPLT |

|

NYSE

Arca |

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant

to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit such files). Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller

reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange

Act.

| Large

Accelerated Filer |

☒ |

|

Accelerated

Filer |

☐ |

| Non-Accelerated

Filer |

☐ |

|

Smaller

Reporting Company |

☐ |

| |

|

|

Emerging

Growth Company |

☐ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the

registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒

No

Aggregate

market value of the registrant’s Shares outstanding based upon the closing price of a Share on June 30, 2024 as reported

by the NYSE Arca, Inc. on that date: $1,015,317,000.

As

of February 26, 2025, abrdn Platinum ETF Trust had 11,900,000 abrdn Physical Platinum Shares ETF outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE: None

FORWARD

LOOKING STATEMENTS

This

Annual Report on Form 10-K contains various “forward-looking statements” within the meaning of Section 27A of the

Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and within the Private

Securities Litigation Reform Act of 1995, as amended. Forward-looking statements usually include the words, “anticipates,”

“believes,” “estimates,” “expects,” “intends,” “plans,” “projects,”

“understands” and other words suggesting uncertainty. We remind readers that forward-looking statements are merely

predictions and therefore inherently subject to uncertainties and other factors and involve known and unknown risks that could

cause the actual results, performance, levels of activity, or our achievements, or industry results, to be materially different

from any future results, performance, levels of activity, or our achievements expressed or implied by such forward-looking statements.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof.

The Trust undertakes no obligation to publicly release any revisions to these forward-looking statements to reflect events or

circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Additional

significant uncertainties and other factors affecting forward-looking statements are presented in the Risk Factors section herein.

TABLE

OF CONTENTS

PART

I

Item

1. Business

The

purpose of the abrdn Platinum ETF Trust (the “Trust”) is to own platinum transferred to the Trust in exchange

for shares issued by the Trust (“Shares”). Each Share represents a fractional undivided beneficial interest in and

ownership of the Trust. The assets of the Trust consist solely of platinum bullion. The Trust was formed on December 30,

2009 when an initial deposit of platinum was made in exchange for the issuance of two Baskets (a “Basket” consists

of 50,000 Shares).

The

sponsor of the Trust is abrdn ETFs Sponsor LLC (the “Sponsor”). The trustee of the Trust is The Bank of New York Mellon

(the “Trustee”) and the custodian is ICBC Standard Bank Plc (the “Custodian” or “ICBC”).

The

Trust’s Shares at redeemable value increased from $997,445,666 at December 31, 2023 to $1,018,947,768 at December 31, 2024,

the Trust’s fiscal year end. Outstanding Shares in the Trust increased from 10,850,000 at December 31, 2023 to 12,200,000

at December 31, 2024.

The

Trust is not managed like a corporation or an active investment vehicle. The Trust has no directors, officers or employees. It

does not engage in any activities designed to obtain a profit from or to improve the losses caused by changes in the price of platinum.

The platinum held by the Trust will only be delivered to pay the remuneration due to the Sponsor (the “Sponsor’s

Fee”), distributed to Authorized Participants (defined below) in connection with the redemption of Baskets or sold (1) on

an as-needed basis to pay Trust expenses not assumed by the Sponsor, (2) in the event the Trust terminates and liquidates its

assets, or (3) as otherwise required by law or regulation.

The

Trust is not registered as an investment company under the Investment Company Act of 1940 and is not required to register under

such act. The Trust does not and will not hold or trade in commodities futures contracts, “commodity interests” or

any other instruments regulated by the Commodity Exchange Act (the “CEA”), as administered by the Commodity Futures

Trading Commission (the “CFTC”) and the National Futures Association (“NFA”). The Trust is not a commodity

pool for purposes of the CEA and the Shares are not “commodity interests,” and neither the Sponsor nor the Trustee

is subject to regulation as a commodity pool operator or a commodity trading advisor in connection with the Shares. The Trust

has no fixed termination date.

The

Sponsor of the registrant maintains an Internet website at www.abrdn.com/us/etf through which the registrant’s annual reports

on Form 10-K, quarterly reports on Form 10-Q, and amendments to those reports filed or furnished pursuant to Section 13(a) or

15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, are made available free of charge as soon as reasonably

practicable after they have been filed or furnished to the Securities and Exchange Commission (the “SEC”). The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically at www.sec.gov.

Trust

Objective

The

investment objective of the Trust is for the Shares to reflect the performance of the price of physical platinum, less the

Trust’s expenses. The Shares are intended to constitute a simple and cost-effective means of making an investment similar

to an investment in physical platinum. An investment in physical platinum requires expensive and sometimes complicated arrangements

in connection with the assay, transportation, warehousing and insurance of the metal. Traditionally, such expense and complications

have resulted in investments in physical platinum being efficient only in amounts beyond the reach of many investors.

The

Shares are intended to provide institutional and retail investors with a simple and cost-efficient means, with minimal credit

risk, of gaining investment benefits similar to those of holding platinum bullion. The Shares offer an investment that:

| ● | Easily

Accessible and Relatively Cost Effective. Investors can access the platinum bullion market through a traditional

brokerage account. The Sponsor believes that investors will be able to more effectively implement strategic and tactical asset

allocation strategies that use platinum bullion by using the Shares instead of using the traditional means of purchasing,

trading and holding platinum bullion and for many investors, transaction costs related to the Shares will be lower than those

associated with the purchase, storage and insurance of physical platinum bullion. |

| ● | Exchange

Traded and Transparent. The Shares trade on the NYSE Arca, providing investors with an efficient means to implement various

investment strategies. The Shares are eligible for margin accounts and are backed by the assets of the Trust and the Trust does

not hold or employ any derivative securities. Furthermore, the value of the Trust’s holdings are reported on the Trust’s

website daily. |

| ● | Minimal Credit Risk. The Shares represent an interest in physical platinum owned by the Trust (other than an amount

held in unallocated form which is not sufficient to make up a whole plate of which is held temporarily to effect a creation

or redemption of Shares). Physical platinum of the Trust in the Custodian’s possession is not subject to borrowing

arrangements with third parties. Other than the platinum temporarily being held in an unallocated platinum account with

the Custodian, the physical platinum of the Trust is not subject to counterparty or credit risks. See “Risk Factors—Platinum

held in the Trust’s unallocated platinum account and any Authorized Participant’s unallocated platinum account

is not segregated from the Custodian’s assets...” This contrasts with most other financial products that gain

exposure to platinum through the use of derivatives that are subject to counterparty and credit risks. |

Investing

in the Shares does not insulate the investor from certain risks, including price volatility. See “Risk Factors.”

Overview

of the Platinum Industry

This

section provides a brief introduction to the platinum industry by looking at some of the key participants, detailing the primary

sources of demand and supply.

In

this annual report, the term “ounces” refers to troy ounces.

Platinum Group

Metals

Platinum

and palladium are the two best known metals of the six platinum group metals (“PGMs”). Platinum and palladium have

the greatest economic importance and are found in the largest quantities. The other four—iridium, rhodium, ruthenium and

osmium—are produced only as co-products of platinum and palladium. PGMs are known for their purity, high melting points

and unique catalytic properties. In addition to their oxidation and reduction properties, they are also extremely resistant to

corrosion. PGMs are utilized in a number of industrial processes, technologies and commercial applications. Their unique chemical

and physical properties make PGMs an excellent raw material, catalyst and ingredient for manufacturing processes. Consumer and

industrial products made with platinum and other PGMs include flat panel monitors, glass fiber, medical tools, computer hard drives,

nylon and razors, among others. PGMs play a critical role in autocatalysis and pollution control in the automotive sector.

PGM

mining is heavily concentrated in southern Africa (South Africa and Zimbabwe), with smaller percentages coming from the United

States, Russia and other locations. South Africa is the world’s leading platinum producer and one of the largest palladium

producers. Russia is the second largest producer of platinum. All of South Africa’s production is sourced from the Bushveld

Igneous Complex, which hosts the world’s largest resource of PGMs. Together, South Africa and Russia accounted for over

83% of platinum supply in 2023.

World

Platinum Supply and Demand 2014-2023

The

following table sets forth a summary of the world platinum supply and demand over the past 10 years (from 2014 to 2023) and is

based on information reported by Johnson Matthey, PGM Market Reports (2015 – 2024).

| (thousands of ounces) |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

| Supply |

|

|

|

|

|

|

|

|

|

|

| South Africa |

3,546 |

4,572 |

4,392 |

4,450 |

4,467 |

4,344 |

3,243 |

4,609 |

3,965 |

4,001 |

| Russia |

700 |

670 |

714 |

720 |

687 |

721 |

699 |

638 |

450 |

780 |

| North America |

340 |

339 |

370 |

368 |

370 |

367 |

334 |

279 |

280 |

288 |

| Zimbabwe |

401 |

400 |

489 |

466 |

474 |

451 |

482 |

465 |

488 |

515 |

| Others |

167 |

158 |

162 |

157 |

152 |

154 |

205 |

222 |

203 |

207 |

| Total primary supply |

5,154 |

6,139 |

6,127 |

6,161 |

6,150 |

6,037 |

4,963 |

6,213 |

5,386 |

5,791 |

| |

|

|

|

|

|

|

|

|

|

|

| Recycling |

|

|

|

|

|

|

|

|

|

|

| Autocatalyst |

1,255 |

1,136 |

1,132 |

1,249 |

1,332 |

1,389 |

1,157 |

1,236 |

1,205 |

1,036 |

| Electrical |

28 |

30 |

32 |

35 |

38 |

40 |

37 |

43 |

39 |

37 |

| Jewellery |

762 |

574 |

738 |

746 |

699 |

663 |

506 |

367 |

273 |

227 |

| Total secondary supply |

2,045 |

1,740 |

1,902 |

2,030 |

2,069 |

2,092 |

1,700 |

1,646 |

1,517 |

1,300 |

| |

|

|

|

|

|

|

|

|

|

|

| Total combined supply |

7,199 |

7,879 |

8,029 |

8,191 |

8,219 |

8,129 |

6,663 |

7,859 |

6,903 |

7,091 |

| |

|

|

|

|

|

|

|

|

|

|

| Demand by Application |

|

|

|

|

|

|

|

|

|

|

| Auto |

3,062 |

3,273 |

3,339 |

3,061 |

2,815 |

2,589 |

2,024 |

2,410 |

2,747 |

3,342 |

| Chemical |

576 |

502 |

477 |

453 |

654 |

662 |

614 |

670 |

695 |

647 |

| Dental & Biomedical |

214 |

215 |

218 |

238 |

241 |

254 |

218 |

224 |

251 |

264 |

| Electrical & Electronics |

225 |

228 |

232 |

224 |

228 |

216 |

227 |

263 |

247 |

195 |

| Glass |

143 |

227 |

247 |

314 |

501 |

490 |

560 |

836 |

708 |

776 |

| Investment |

277 |

451 |

620 |

361 |

67 |

1,131 |

1,022 |

(28) |

(565) |

46 |

| Jewelry |

2,839 |

2,746 |

2,413 |

2,385 |

2,258 |

2,073 |

1,657 |

1,468 |

1,391 |

1,361 |

| Petroleum |

172 |

140 |

186 |

228 |

380 |

262 |

285 |

223 |

240 |

174 |

| Pollution Control |

— |

— |

— |

184 |

193 |

190 |

181 |

214 |

234 |

275 |

| Other |

468 |

494 |

535 |

530 |

531 |

542 |

417 |

444 |

483 |

529 |

| Total demand |

7,976 |

8,276 |

8,267 |

7,978 |

7,868 |

8,409 |

7,205 |

6,724 |

6,431 |

7,609 |

| |

|

|

|

|

|

|

|

|

|

|

| Movements in Stocks |

(777) |

(397) |

(238) |

213 |

351 |

(280) |

(542) |

1,135 |

472 |

(518) |

Source:

Johnson Matthey PGM Market Report (2015-2024).

| 1 |

Primary supply: Supply figures represent sales of primary

PGM by producers and are allocated to the region where mining took place, rather than the region of subsequent processing. |

| 2 |

Secondary supply: Secondary supply is the quantity of

metal recovered from open-loop recycling (i.e. where the original purchaser does not retain ownership of the PGM). Outside the automotive,

jewelry and electronics markets, open-loop recycling is negligible. |

| 3 |

Automotive recycling represents the weight of metal recovered

from end-of-life vehicles and aftermarket scrap. It does not include warranty or production scrap. |

| 4 |

Demand: Demand figures for any given application represent

the sum of industry demand for new metal in that application, net of any closed-loop recycling (i.e. where industry participants retain

ownership of the metal: an example would be recycling of spent chemical catalysts where the metal is retained to be used on fresh catalyst

that replaces the spent charge). |

| 5 |

Automotive demand is allocated to the region where the

vehicle is manufactured and is accounted for at the time of vehicle production. It includes emissions catalysts on vehicles, motorcycles

and three-wheelers, as well as fuel cell vehicles. Non-road mobile machinery is counted as industrial demand, in the pollution control

category.

|

| 6 |

Jewelry demand is allocated to the region where the finished

jewelry is manufactured, not sold. |

| 7 |

Movements in stocks: This figure gives the overall market

balance in any one year and reflects the extent of stocks that must be mobilized to balance the market in that year. It is thus a proxy

for changes in stocks held by fabricators, dealers, banks and depositories, but excludes stocks held by primary and secondary refiners

and final consumers. A positive figure (market surplus) thus reflects an increase in global market stocks. A negative value (market deficit)

indicates a decrease in global market stocks. |

The

following are some of the main characteristics of the platinum market illustrated by the table:

The

main supplier of platinum is South Africa, providing approximately 71.4% of total mine supply over the past 10 years (2014-2023).

Russia is the second largest supplier of platinum. Its share of world mine production has averaged around 11.7% of total mine supply

over the past ten years ended 2023. Scrap supply from recycling of autocatalyst and other sources have accounted for about 24%

of total supply over the last 10 years.

Over

the ten years ended December 2023, jewelry demand for platinum peaked at approximately 36% of total demand in 2014. Jewelry demand has

since declined to 18% total demand in 2023, following a consistent downward trend. Automotive demand for platinum, which accounted for

around 36% of total demand at the end of 2014, has increased to roughly 44% of total demand as of the end of 2023. Following two consecutive

years of growth, investment demand fell from a high of 14% in 2020 into negative territory in 2022 at (9%) but improved to 1% in 2023.

Pollution control demand, which captures the production demand of non-road vehicles such as agricultural equipment and industrial machinery

as well as small engines and stationary source emissions controls in factories that use technology that is similar to autocatalysts,

increased to 4% of total demand in 2023.

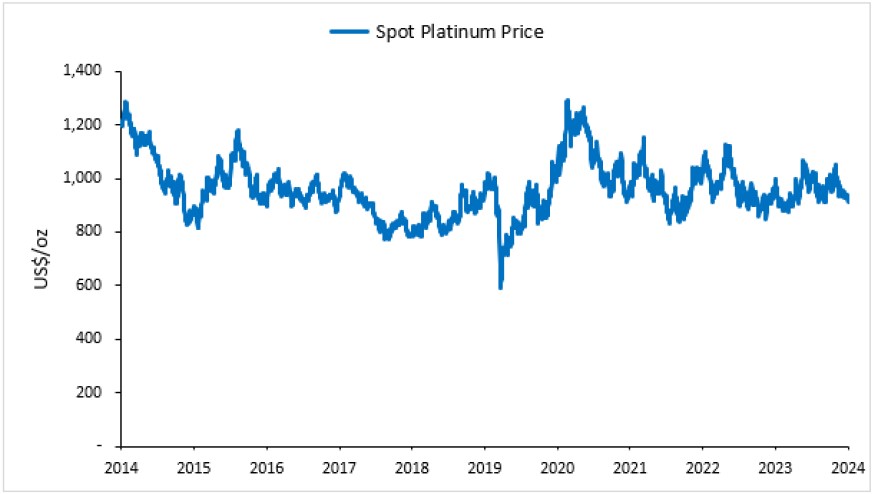

Historical

Chart of the Price of Platinum

The

price of platinum is volatile and fluctuations are expected to have a direct impact on the value of the Shares. However, movements

in the price of platinum in the past are not a reliable indicator of future movements. The following chart illustrates the

movements in the price of an ounce of platinum in U.S. Dollars from December 31, 2014 to December 31, 2024 and is based on information provided by Bloomberg:

Source:

Bloomberg, abrdn. Chart data from 12/31/2014 to 12/31/2024. Spo Platinum Price = PLTMLNPM Index.

The following is a discussion of the movements in the price of platinum illustrated by the table:

In

2012, platinum prices rose on the back of supply disruptions in South Africa, which accounts for more than 72% of the world’s

supply of platinum. A strike at one of South Africa’s biggest platinum mines caused the price of platinum to rise from $1,387

to $1,709 per ounce in August 2012. At the beginning of 2013, Anglo American Platinum, the world’s biggest producer of the

metal, announced its intention to close four mine shafts and its consideration of selling another mine complex as part of a radical

overhaul of its South African operations. This statement prompted a strong reaction on platinum prices, which rose from $1,656

to $1,736 per ounce in the days following the announcement, on fears of a further tightening in platinum supply. However, platinum’s

correlation to gold weighed on platinum prices in 2013 overall. Prolonged strikes at South African mines in 2014 led to the deepest

supply deficit in platinum since 1975 (the earliest date we have supply and demand data). However, that failed to arrest the price

slide which saw prices fall 11% in 2014, highlighting the extent of negative sentiment towards industrially-exposed precious metals.

Despite autocatalyst demand for platinum increasing in 2015, tightening nitrogen oxide emission standards have led to pessimism

about the future demand for platinum-heavy diesel autocatalysts relative to palladium-heavy gasoline autocatalysts. Further pessimistic

outlook for South Africa’s economy and its currency the South African Rand weighed on platinum prices throughout 2017, and

platinum continued to fall in 2018 driven by lackluster investor sentiment, a stronger US dollar, weaker diesel demand and rising

mine supply. Platinum prices bounced back, rising 19.9% to $952 per ounce at the end of 2019. After seeing the price fall as low

as $593 per ounce on March 19, 2020, platinum rebounded from pandemic lows and finished the year at $1,068 per ounce. The steep

climb in palladium price has led some investors to conclude that platinum appears under-valued, in view of its potential to substitute

for palladium in automotive applications in the future. Additionally, the outlook for mining in South Africa is increasingly uncertain,

with producers facing steep increases in electricity prices, periodic disruption to power supplies and a risk of industrial action

during anticipated wage negotiations. In 2021, platinum took a back seat to risky assets, similarly to other precious metals,

as it returned -10% (as of December 31, 2021). Follow through from auto production disruptions during the pandemic were a major

contributor to the price performance in 2021. The price of platinum reached as high as $1,151 per ounce on March 8, 2022, as Russia’s

invasion of Ukraine and the threat of sanctions on Russian exports, including platinum, pushed prices higher. However, while other

precious metals (gold, silver, palladium) saw prices fluctuate throughout the year, platinum’s volatility was much more

pronounced within the first quarter of 2022, as the price fell roughly 15% by March 31, 2022, to close the first quarter at $983

per ounce. Aggressive interest rate hikes by the U.S. Federal Reserve, a strong U.S. Dollar and risks of diminishing global economic

growth exerted additional pressure on prices, as the price of platinum fell as low as $831 per ounce on July 14, 2022. Through

the end of 2022, increasing autocatalyst demand and a growing substitution of platinum for palladium contributed to ongoing physical

market tightness, despite a global surplus, which saw the price of platinum increase roughly 24% from July 14, 2022 through December

31, 2022 to $1,031 per ounce.

In

2023, a decrease in platinum production in South Africa, the world’s leading producer, has continued to impact global supply (see

“World Platinum Supply and Demand in 2023” above for additional discussion). While industry analysis groups see potential

for a nearly 1-million-ounce deficit in platinum in 2023, the price performance has not reflected this sentiment over the course

of the year as the market remains well supplied pulling from existing above ground stockpiles. Despite a positive outlook at the

beginning of the year, fueled by China’s loosening of Covid-related restrictions, that drove the price as high as $1,128

per ounce on April 21, 2023, the Chinese economic rebound disappointed investors and led the price of platinum to fall as low

as $850 per ounce on November 13, 2023. While an end-of-year rally saw the price of platinum increase roughly 18% off the yearly

low to $1,000 per ounce, platinum ended the year approximately 3% below its 2022 closing price.

In 2024, mining production in South Africa has continued to impact global supply, as the country experiences some remaining power supply

disruptions, although at a far lower pace than in 2023. Political instability, inflation and volatile market prices have compressed profit margins and subsequently led to a decrease in expected supply from the world's leading producer. As a result, platinum

markets remained volatile throughout the year while prices have not responded to the existing supply side deficit as above ground stocks

are being worked through. An increase in expected automotive demand provided some tailwinds during the first half of the year sent the

spot price of platinum as high as $1,065 per ounce on May 17, 2024. However, the lackluster Chinese economic rebound and disappointing

level of stimulus turned to headwinds as the price retreated to $910 per ounce. The risk of additional sanctions on Russian metal exports

in October provided some temporary price support, however market fears over supply restrictions quickly dissipated, and prices retreated

once more. Headwinds grew as the US election resulted in an increased potential of tariffs that are large enough to slow global economic

growth and the spot price of platinum ended the year down -8.6%, at $914 per ounce.

Operation

of the Platinum Market

The

global trade in platinum consists of Over-the-Counter (“OTC”) transactions in spot, forwards, and options and

other derivatives, together with exchange-traded futures and options.

Global

Over-The-Counter Market

The

OTC market trades on a 24-hour per day continuous basis and accounts for most global platinum trading. Market makers, as well

as others in the OTC market, trade with each other and with their clients on a principal-to-principal basis. All risks and issues

of credit are between the parties directly involved in the transaction. Market makers include the market making members of the

London Platinum and Palladium Market (“LPPM”), the trade association that acts as the coordinator for activities conducted

on behalf of its members and other participants in the LPPM. Five member participants of the LPPM are currently participating

in the electronic LBMA Platinum Price PM (as described below) process administered by the London Metal Exchange (“LME”). The OTC

market provides a relatively flexible market in terms of quotes, price, size, destinations for delivery and other factors. Bullion

dealers customize transactions to meet clients’ requirements. The OTC market has no formal structure and no open outcry

meeting place.

The

main centers of the OTC market for platinum are London, New York, Hong Kong and Zurich. Mining companies, manufacturers of jewelry

and industrial products, together with investors and speculators, tend to transact their business through one of these market

centers. Centers such as Dubai and several cities in the Far East also transact substantial OTC market business, typically involving

jewelry and small plates or ingots of platinum (1 kilogram or less) and will hedge their exposure by selling into one of these

main OTC centers. Precious metals dealers have offices around the world and most of the world’s major bullion dealers are

either members or associate members of the London Bullion Market Association (“LBMA”) and/or the LPPM. In the OTC

market for platinum, the standard size of trades between market makers is 1,000 ounces.

Liquidity

in the OTC market can vary from time to time during the course of the 24-hour trading day. Fluctuations in liquidity are reflected

in adjustments to dealing spreads—the differential between a dealer’s “buy” and “sell” prices.

The period of greatest liquidity in the platinum market generally occurs at the time of day when trading in the European time

zones overlaps with trading in the United States, which is when OTC market trading in London, New York, and other centers

coincides with futures and options trading on the Commodity Exchange, Inc. (“COMEX”), a designated contract market

within the CME Group. This period lasts for approximately four hours each New York business day morning.

The

Platinum Market

The

Zurich and London Platinum Bullion Markets

Although the market for physical platinum is distributed globally, most platinum is stored and most OTC market trades are cleared through London and Zurich. In addition to coordinating market activities, the LPPM acts as the principal point of contact between the market and its regulators. A primary function of the LPPM is its involvement in the promotion of refining standards by maintenance of the “London/Zurich Good Delivery Lists,” which are the lists of LPPM accredited refiners of platinum. The LPPM also coordinates market clearing and vaulting, promotes good trading practices and develops standard documentation.

Platinum is traded generally on a “loco London” or “loco Zurich” basis, meaning the precious metal is physically held in vaults in London or Zurich or is transferred into accounts established in London or Zurich. Delivery of the platinum can either be by physical delivery or through the clearing systems to an unallocated account.

The

unit of trade in London and Zurich is the troy ounce, whose conversion between grams is: 1,000 grams equals to 32.1507465 troy

ounces, and one troy ounce is equivalent to 31.1034768 grams. A good delivery platinum plate or ingot on the LPPM approved list

is acceptable for delivery in settlement of a transaction on the OTC market (a “Good Delivery Platinum Plate or Ingot”).

A Good Delivery Platinum Plate or Ingot must contain between 32 and 192 troy ounces of platinum with a minimum fineness (or purity)

of 999.5 parts per 1,000 (99.95%), be of good appearance, and be easy to handle and stack. The platinum content of a platinum

Good Delivery Platinum Plate or Ingot is calculated by multiplying the gross weight by the fineness of the plate or ingot. A Good

Delivery Platinum Plate or Ingot must also bear the stamp of one of the refiners who are on the LPPM approved list. Unless otherwise

specified, the platinum spot price always refers to the “Good Delivery Standards” set by the LPPM. Business is generally

conducted over the phone and through electronic dealing systems.

Since

December 1, 2014, the LME has been administering the operation of an electronic platinum bullion price fixing system (“LMEbullion”)

that replicates electronically the manual London platinum fix processes previously employed by the London Platinum and Palladium

Fixing Company Ltd (“LPPFCL”), as well as providing electronic market clearing processes for platinum bullion transactions

at the fixed prices established by the LME pricing mechanism. The LME’s electronic price fixing processes, like the previous

London platinum fix processes, establishes and publishes fixed prices for troy ounces of platinum twice each London trading day

during fixing sessions beginning at 9:45 a.m. London time (the “LBMA Platinum Price AM”) and 2:00 p.m. London time (the “LBMA Platinum Price PM”). In addition to utilizing the same London platinum fix standards and methods, the LME also supervises the platinum

electronic price fixing processes through its market operations, compliance, internal audit and third-party complaint handling

capabilities in order to support the integrity of the LBMA Platinum Price PM. The LME, in administering LMEbullion, uses a pricing methodology

that meets the administrative and regulatory needs of platinum market participants, including the International Organization of

Securities Commission’s (IOSCO) Principles for Financial Benchmarks, (the “IOSCO Principles”).

Daily

during London trading hours the LBMA Platinum Price AM and the LBMA Platinum Price PM each provide reference platinum prices for that day’s trading.

Many long-term contracts will be priced on the basis of either the LBMA Platinum Price AM or the LBMA Platinum Price PM, and market participants will

usually refer to one or the other of these prices when looking for a basis for valuations. The Trust values its platinum on the

basis of the LBMA Platinum Price PM. If on a day when the Trust’s NAV is being calculated, the LBMA Platinum Price PM is not available or has not been announced by 4:00 p.m. New York time, the Trustee is authorized to use the LBMA Platinum Price AM announced on that day. If neither price is available for that day, the Trustee will value the Trust’s platinum based on the most recently announced LBMA Platinum Price PM or LBMA Platinum Price AM.

Formal

participation in the LBMA Platinum Price PM is limited to participating LPPM members. Five LPPM members are currently participating in establishing

the LBMA Platinum Price PM (Goldman Sachs International, HSBC Bank USA NA, ICBC Standard Bank plc, Johnson Matthey plc and BASF Metals Ltd.).

Any other market participant wishing to participate in the trading on the LBMA Platinum Price PM is required to do so through one of the participating

LPPM members.

Orders

are placed either with one of the participating LPPM member participants or with another precious metals dealer who will then

be in contact with a participating LPPM member during the fixing. The fix begins with the chair reflecting the market price and

other data, prevailing at the opening of the fix. This is relayed by the LPPM member participants to their dealing rooms which

have direct communication with all interested parties. Any member participant may enter the fixing process at any time, or adjust

or withdraw his order. The platinum price is adjusted up or down until all the buy and sell orders are electronically matched,

at which time the price is declared fixed. All orders are transacted on the basis of this fixed price, which is instantly relayed

to the market through various media.

The

LBMA and the LME have asserted that the LME’s electronic price fixing processes are similar to the non-electronic processes

previously used to establish the applicable London platinum fix where the London platinum fix process adjusted the platinum price

up or down until all the buy and sell orders entered by the participating LPPM members are matched, at which time the price was

declared fixed. Nevertheless, the LBMA Platinum Price PM has several advantages over the previous London platinum fix. The LME’s electronic

price fixing processes are intended to be transparent. The LME asserts that its electronic price fixing processes are fully auditable

by third parties since an audit trail exists from the beginning of each fixing session. The LME also asserts that the market operation,

compliance, internal audit and third-party complaint handling capabilities of the LME supports the integrity of the LBMA Platinum Price PM.

Since

December 1, 2014, the Sponsor determined that the London platinum fix, which has been revised based on the new LME method and

is now known as the LBMA Platinum Price (PM), which we refer to herein as the LBMA Platinum Price PM, is an appropriate basis for valuing

platinum bullion received upon purchase of the Trust’s Shares, delivered upon redemption of the Trust’s Shares and

for determining the value of the Trust’s platinum bullion each trading day. The Sponsor also determined that the LME PM Fix fairly represents the commercial value of platinum bullion held by the Trust and the “Benchmark Price” (as defined in Trust Agreement) as of any day is such day’s LBMA Platinum Price PM or such day’s LBMA Platinum Price AM if such day’s LBMA Platinum Price PM is not available.

As

of December 1, 2014, the LPPFCL transferred ownership of the historic and future intellectual property of the twice daily “fix”

for platinum and palladium bullion to a subsidiary company of the LBMA.

Futures

Exchanges

The

most significant platinum futures exchanges are the COMEX, a designated contract market within the CME Group, and the Tokyo

Commodity Exchange, Inc. (“TOCOM”). The COMEX is the largest exchange in the world for trading precious metals futures

and options and launched platinum futures in 1956, followed with options in 1990. The TOCOM has been trading platinum since 1984.

Trading on these exchanges is based on fixed delivery dates and transaction sizes for the futures and options contracts traded.

Trading costs are negotiable. As a matter of practice, only a small percentage of the futures market turnover ever comes to physical

delivery of the platinum represented by the contracts traded. Both exchanges permit trading on margin. Margin trading can add

to the speculative risk involved given the potential for margin calls if the price moves against the contract holder. The COMEX

trades platinum futures almost continuously (with one short break in the evening) through its CME Globex electronic trading system

and clears through its central clearing system. On June 6, 2003, the TOCOM adopted a similar clearing system. In each case, the

exchange acts as a counterparty for each member for clearing purposes.

Market

Regulation

The

global platinum markets are overseen and regulated by both governmental and self-regulatory organizations. In addition, certain

trade associations have established rules and protocols for market practices and participants. In the United Kingdom, responsibility

for the regulation of the financial market participants, including the major participating members of the LPPM falls under

the authority of the Financial Conduct Authority (“FCA”) as provided by the Financial Services and Markets

Act 2000 (“FSM Act”). Under this act, all U.K.-based banks, together with other investment firms, are subject to a

range of requirements, including fitness and properness, capital adequacy, liquidity, and systems and controls.

The

FCA is responsible for regulating investment products, including derivatives, and those who deal in investment products. Regulation

of spot, commercial forwards, and deposits of platinum not covered by the FSM Act is provided for by The London Code of Conduct

for Non-Investment Products, which was established by market participants in conjunction with the Bank of England.

The

TOCOM has authority to perform financial and operational surveillance on its members’ trading activities, scrutinize positions

held by members and large-scale customers, and monitor the price movements of futures markets by comparing them with cash and

other derivative markets’ prices. To act as a Futures Commission Merchant Broker on the TOCOM, a broker must obtain a license

from Japan’s Ministry of Economy, Trade and Industry, the regulatory authority that oversees the operations of the TOCOM.

The

CFTC regulates trading in commodity contracts, such as futures, options and swaps. In addition, under the CEA, the CFTC has jurisdiction

to prosecute manipulation and fraud in any commodity (including precious metals) traded in interstate commerce as spot as well

as deliverable forwards. The CFTC is the exclusive regulator of U.S. commodity exchanges and clearing houses.

Secondary

Market Trading

While

the Trust’s investment objective is for the Shares to reflect the performance of the price of physical platinum, less

the Trust’s expenses, the Shares may trade in the secondary market on the NYSE Arca at prices that are lower or higher relative

to their net asset value (the value of the Trust’s assets less its liabilities (“NAV”)) per Share. The amount

of the discount or premium in the trading price relative to the NAV per Share may be influenced by non-concurrent trading hours

between the NYSE Arca, COMEX and the London and Zurich platinum markets. While the Shares trade on the NYSE Arca until

4:00 PM New York time, liquidity in the global platinum market is reduced after the close of the COMEX at 1:30 PM New York

time. As a result, during this time, trading spreads, and the resulting premium or discount, on the Shares may widen.

Valuation

of Platinum and Computation of Net Asset Value

On

each day that the NYSE Arca is open for regular trading, as promptly as practicable after 4:00 PM New York time, on such day (“Evaluation

Time”), the Trustee evaluates the platinum held by the Trust and determines both the average net asset value (“ANAV”)

and the NAV of the Trust.

At the Evaluation Time, the Trustee values the Trust’s platinum on the basis of that day’s LBMA Platinum Price PM or, if no

LBMA Platinum Price PM is made on such day or has not been announced by the Evaluation Time, the LBMA Platinum Price AM announced on that

day will be used. If neither price is available for that day, the Trust will value its palladium based on the most recently announced

LBMA Platinum Price PM or LBMA Platinum Price AM, unless the Sponsor determines that such price is inappropriate as a basis for evaluation.

In the event the Sponsor determines that the applicable LBMA Platinum Price PM or such other publicly available price as the Sponsor may

deem fairly represents the commercial value of the Trust’s platinum is not an appropriate basis for evaluation of the Trust’s

platinum, it shall identify an alternative basis for such evaluation to be employed by the Trustee. Neither the Trustee nor the Sponsor

shall be liable to any person for the determination that the LME PM Fix or such other publicly available price is not appropriate as a

basis for evaluation of the Trust’s platinum or for any determination as to the alternative basis for such evaluation provided that

such determination is made in good faith. See “Operation of the Platinum Market—the Platinum Market”for a description

of the LBMA Platinum Price PM.

Once

the value of the platinum has been determined, the Trustee subtracts all estimated accrued fees (other than the fees accruing

for such day on which the valuation takes place which are computed by reference to the value of the Trust or its assets),

expenses and other liabilities of the Trust from the total value of the platinum and any other assets of the Trust.

The resulting figure is the ANAV of the Trust. The ANAV of the Trust is used to compute the Sponsor’s Fee.

All

fees accruing for the day on which the valuation takes place which are computed by reference to the value of the Trust or

its assets are calculated using the ANAV calculated for such day. The Trustee subtracts from the ANAV the amount of accrued fees

so computed for such day and the resulting figure is the NAV of the Trust. The Trustee also determines the NAV per Share

by dividing the NAV of the Trust by the number of the Shares outstanding as of the close of trading on the NYSE Arca (which includes

the net number of any Shares created or redeemed on such evaluation day).

Any

estimate of the accrued but unpaid fees, expenses and liabilities of the Trust for purposes of computing the NAV of the Trust

and ANAV made by the Trustee in good faith shall be conclusive upon all persons interested in the Trust and no revision or correction

in any computation made under the Trust Agreement will be required by reason of any difference in amounts estimated from those

actually paid.

The

Sponsor and the Shareholders may rely on any evaluation furnished by the Trustee, and the Sponsor has no responsibility for the

evaluation’s accuracy. The determinations the Trustee makes will be made in good faith upon the basis of, and the Trustee

will not be liable for any errors contained in, information reasonably available to it. The Trustee will not be liable to the

Sponsor, The Depository Trust Company (“DTC”). Authorized Participants, the Shareholders or any other person for errors in judgment. However, the preceding liability

exclusion will not protect the Trustee against any liability resulting from bad faith or gross negligence in the performance of

its duties.

On May 23, 2024, the Sponsor entered into an Amendment (the “Trust Amendment”) to the Depositary Trust Agreement (the “Trust Agreement”) with the Trustee. The Trust Amendment reflects the following changes, effective as of June 18, 2024, as approved and directed by the Sponsor on behalf of the Trust: (1) the amendment of the definition of “Benchmark Price” to mean, “as of any day, (i) such day’s LBMA Platinum Price PM or such day’s LBMA Platinum Price AM if such day’s LBMA Platinum Price PM is not available; or (ii) such other publicly available price which is reasonably available to the Trustee at no cost to the Trustee and which the Sponsor may determine fairly represents the commercial value of platinum held by the Trust and instructs the Trustee to use as the Benchmark Price”; (2) the deletion and replacement of the defined term for “London PM Fix” with the defined term “LBMA Platinum Price PM”, which means “the price of a troy ounce of platinum as determined by the LME, the third party administrator of the London platinum price selected by the LBMA, or any successor administrator of the London [platinum price, at or about 2:00 p.m. London, England time”; and (3) the addition of the new definition for “LBMA Platinum Price AM” which means “the price of a troy ounce of platinum as determined by the LME, the third party administrator of the London platinum price selected by the LBMA, or any successor administrator of the London platinum price, at or about 9:45 a.m. London, England time.

Trust

Expenses

The

Trust’s only ordinary recurring expense is the Sponsor’s Fee. In exchange for the Sponsor’s Fee, the Sponsor

has agreed to assume the following administrative and marketing expenses incurred by the Trust: the Trustee’s monthly fee

and out-of-pocket expenses, the Custodian’s fee and reimbursement of the Custodian’s expenses under the Custody Agreements,

Exchange listing fees, SEC registration fees, printing and mailing costs, audit fees and up to $100,000 per annum in legal expenses.

The

Sponsor’s Fee accrues daily at an annualized rate equal to 0.60% of the ANAV of the Trust and is payable monthly in arrears.

The Sponsor, from time to time, may temporarily waive all or a portion of the Sponsor’s Fee at its discretion for a stated

period of time. Presently, the Sponsor does not intend to waive any of its fee.

Furthermore,

the Sponsor may, in its sole discretion, agree to rebate all or a portion of the Sponsor’s Fee attributable to Shares held

by certain institutional investors subject to minimum shareholding and lock up requirements as determined by the Sponsor to foster

stability in the Trust’s asset levels. Any such rebate will be subject to negotiation and written agreement between the

Sponsor and the investor on a case by case basis. The Sponsor is under no obligation to provide any rebates of the Sponsor’s

Fee. Neither the Trust nor the Trustee will be a party to any Sponsor’s Fee rebate arrangements negotiated by the Sponsor.

Any Sponsor’s Fee rebate shall be paid from the funds of the Sponsor and not from the assets of the Trust.

The

Sponsor’s Fee is paid by delivery of platinum to an account maintained by the Custodian for the Sponsor on an unallocated

basis, monthly on the first business day of the month in respect of fees payable for the prior month. The delivery is of that

number of ounces of platinum which equals the daily accrual of the Sponsor’s Fee for such prior month calculated at the

LBMA Platinum Price PM.

The

Trustee will, when directed by the Sponsor, and, in the absence of such direction, may, in its discretion, sell platinum in such

quantity and at such times as may be necessary to permit payment in cash of Trust expenses not assumed by the Sponsor. The Trustee

is authorized to sell platinum at such times and in the smallest amounts required to permit such payments as they become due,

it being the intention to avoid or minimize the Trust’s holdings of assets other than platinum. Accordingly, the amount

of platinum to be sold will vary from time to time depending on the level of the Trust’s expenses and the market price of platinum.

The Custodian is authorized to purchase from the Trust, at the request of the Trustee, platinum needed to cover Trust expenses

not assumed by the Sponsor at the price used by the Trustee to determine the value of the platinum held by the Trust on the date

of the sale.

The

Sponsor’s Fee for the year ended December 31, 2024 was $5,968,067 (December 31, 2023: $5,772,056; December 31, 2022: $6,556,049).

Cash

held by the Trustee pending payment of the Trust’s expenses will not bear any interest. Each delivery or sale of platinum

by the Trust to pay the Sponsor’s Fee or other Trust expenses will be a taxable event to Shareholders.

Creation

and Redemption of Shares

The

Trust creates and redeems Shares from time to time, but only in one or more Baskets of 50,000 Shares. The creation and redemption

of Baskets is only made in exchange for the delivery to the Trust or the distribution by the Trust of the amount of physical

platinum represented by the Baskets being created or redeemed, the amount of which is based on the combined NAV of the number

of Shares included in the Baskets being created or redeemed determined on the day the order to create or redeem Baskets is properly

received.

Authorized

Participants are the only persons that may place orders to create and redeem Baskets. Authorized Participants must be (1) registered

broker-dealers or other securities market participants, such as banks and other financial institutions, which are not required

to register as broker-dealers to engage in securities transactions, and (2) participants in DTC. To become an Authorized Participant,

a person must enter into an Authorized Participant Agreement with the Sponsor and the Trustee. The Authorized Participant Agreement

provides the procedures for the creation and redemption of Baskets and for the delivery of the platinum and any cash required

for such creations and redemptions. The Authorized Participant Agreement and the related procedures attached thereto may be amended

by the Trustee and the Sponsor, without the consent of any Shareholder or Authorized Participant. Authorized Participants pay

a transaction fee of $500 to the Trustee for each order they place to create or redeem one or more Baskets. Authorized Participants

who make deposits with the Trust in exchange for Baskets receive no fees, commissions or other form of compensation or inducement

of any kind from either the Sponsor or the Trust for serving as an Authorized Participant, and no such person has any obligation

or responsibility to the Sponsor or the Trust to effect any sale or resale of Shares.

Authorized

Participants are cautioned that some of their activities will result in their being deemed participants in a distribution in a

manner which would render them statutory underwriters and subject them to the prospectus-delivery and liability provisions of

the Securities Act, as described in “Plan of Distribution”.

Prior

to initiating any creation or redemption order, an Authorized Participant must have entered into an agreement with the Custodian

or a platinum clearing bank to establish an Authorized Participant Unallocated Account in London (Authorized Participant

Unallocated Bullion Account Agreement). Authorized Participant Unallocated Accounts may only be used for transactions with the Trust. Platinum held in Authorized Participant Unallocated Accounts is typically not segregated

from the Custodian’s or other platinum clearing bank’s assets, as a consequence of which an Authorized Participant

will have no proprietary interest in any specific plates or ingots of platinum held by the Custodian or the platinum

clearing bank. Credits to its Authorized Participant Unallocated Account are therefore at risk of the Custodian’s or other platinum

clearing bank’s insolvency. No fees will be charged by the Custodian for the use of the Authorized Participant Unallocated

Account as long as the Authorized Participant Unallocated Account is used solely for platinum transfers to and from the Trust

Unallocated Account and the Custodian (or one of its affiliates) receives compensation for maintaining the Trust Allocated Account.

Authorized Participants should be aware that the Custodian’s liability threshold under the Authorized Participant Unallocated

Bullion Account Agreement is generally gross negligence, not negligence, which is the Custodian’s liability threshold under

the Trust’s Custody Agreements.

As

the terms of the Authorized Participant Unallocated Bullion Account Agreement differ in certain respects from the terms of the

Trust Unallocated Account Agreement, potential Authorized Participants should review the terms of the Authorized Participant Unallocated

Bullion Account Agreement carefully. A copy of the Authorized Participant Agreement may be obtained by potential Authorized Participants

from the Trustee.

Certain

Authorized Participants are expected to have the facility to participate directly in the physical platinum market and the

platinum futures market. In some cases, an Authorized Participant may from time to time acquire platinum from or sell platinum

to its affiliated platinum trading desk, which may profit in these instances. Each Authorized Participant must be registered

as a broker-dealer under the Securities Exchange Act of 1934 (Exchange Act) and regulated by FINRA or be exempt from being or

otherwise not be required to be so regulated or registered, and be qualified to act as a broker or dealer in the states or

other jurisdictions where the nature of its business so requires. Certain Authorized Participants are regulated under federal

and state banking laws and regulations. Each Authorized Participant has its own set of rules and procedures, internal controls

and information barriers as it determines is appropriate in light of its own regulatory regime.

Authorized

Participants may act for their own accounts or as agents for broker-dealers, custodians and other securities market participants

that wish to create or redeem Baskets. An order for one or more Baskets may be placed by an Authorized Participant on behalf of

multiple clients. As of the date of this report, Goldman Sachs & Co., HSBC Securities (USA) LLC, J.P. Morgan Securities LLC,

Merrill Lynch Professional Clearing Corp., Mizuho Securities USA LLC, Morgan Stanley & Co. Inc., Scotia Capital (USA)

Inc., UBS Securities LLC and Virtu Americas, LLC have each signed an Authorized Participant Agreement with the Trust and,

upon the effectiveness of such agreement, may create and redeem Baskets as described above. Persons interested in purchasing Baskets

should contact the Sponsor or the Trustee to obtain the contact information for the Authorized Participants. Shareholders who

are not Authorized Participants will only be able to redeem their Shares through an Authorized Participant.

All

platinum is delivered to the Trust and distributed by the Trust in unallocated form through credits and debits between Authorized

Participant Unallocated Accounts and the Trust Unallocated Account. Platinum transferred from an Authorized Participant Unallocated

Account to the Trust in unallocated form will first be credited to the Trust Unallocated Account. Thereafter, the Custodian will

allocate, specific plates or ingots of platinum, in each case representing

the amount of platinum credited to the Trust Unallocated Account (to the extent such amount is representable by whole platinum

plates or ingots) to the Trust Allocated Account. The movement of platinum is reversed for the distribution of platinum to an

Authorized Participant in connection with the redemption of Baskets.

All

physical platinum represented by a credit to any Authorized Participant Unallocated Account and to the Trust Unallocated Account

and all physical platinum held in the Trust Allocated Account with the Custodian must be of at least a minimum fineness (or purity) of 999.5 parts per 1,000 (99.95%) and otherwise conform to the rules, regulations

practices and customs of the LPPM, including the specifications for a Good Delivery Platinum Plate or Ingot.

Under

the Authorized Participant Agreement, the Sponsor has agreed to indemnify the Authorized Participants against certain liabilities,

including liabilities under the Securities Act.

The

following description of the procedures for the creation and redemption of Baskets is only a summary and an investor should

refer to the relevant provisions of the Trust Agreement and the form of Authorized Participant Agreement for more

detail.

Creation

Procedures

On

any business day, an Authorized Participant may place an order with the Trustee to create one or more Baskets. Creation and redemption

orders are accepted on “business days” the NYSE Arca is open for regular trading. Settlements of such orders requiring

receipt or delivery, or confirmation of receipt or delivery, of platinum in the United Kingdom, or another jurisdiction

will occur on “business days” when (1) banks in the United Kingdom or other jurisdiction and (2) the

London platinum markets are regularly open for business. If such banks or the London platinum markets are

not open for regular business for a full day, such a day will only be a “business day” for settlement purposes if

the settlement procedures can be completed by the end of such day. Redemption settlements including platinum deliveries loco London

may be delayed longer than two, but no more than five, business days following the redemption order date. Settlement of orders

requiring receipt or delivery, or confirmation of receipt or delivery, of Shares will occur, after confirmation of the applicable

platinum delivery, on “business days” when the NYSE Arca is open for regular trading. In the event of a level 3 market-wide

circuit breaker resulting in a trading halt for the remainder of the trading day, the time of the market-wide trading halt is

considered the close of regular trading and no creation orders for the current trade date will be accepted after that time (the

“cutoff”). Orders placed after the cutoff will be deemed to be rejected and will not be processed. Orders should be

placed in proper form on the following business day. Purchase orders must be placed no later than 3:59:59 p.m. on each business

day the NYSE Arca is open for regular trading.

By

placing a purchase order, an Authorized Participant agrees to deposit platinum with the Trust. Prior to the delivery of Baskets

for a purchase order, the Authorized Participant must also have wired to the Trustee the non-refundable transaction fee due for

the purchase order.

Determination

of required deposits

The

amount of the required platinum deposit is determined by dividing the number of ounces of platinum held by the Trust by the number

of Baskets outstanding, as adjusted for the amount of platinum constituting estimated accrued but unpaid fees and expenses of

the Trust.

Fractions

of a fine ounce of platinum smaller than 0.001 of a fine ounce which are included in the platinum deposit amount are disregarded

in the foregoing calculation. All questions as to the composition of a Creation Basket Deposit will be finally determined by the

Trustee. The Trustee’s determination of the Creation Basket Deposit shall be final and binding on all persons interested

in the Trust.

Delivery

of required deposits

An

Authorized Participant who places a purchase order is responsible for crediting its Authorized Participant Unallocated Account

with the required platinum deposit amount by the prescribed settlement date in London. Upon receipt of the platinum deposit amount,

the Custodian, after receiving appropriate instructions from the Authorized Participant and the Trustee, will transfer on the

prescribed settlement date the platinum deposit amount from the Authorized Participant Unallocated Account to the Trust Unallocated

Account and the Trustee will direct DTC to credit the number of Baskets ordered to the Authorized Participant’s DTC account. The

expense and risk of delivery, ownership and safekeeping of platinum until such platinum has been received by the Trust shall be

borne solely by the Authorized Participant. The Trustee may accept delivery of platinum by such other means as the Sponsor, from

time to time, may determine with the Trustee to be acceptable for the Trust, provided that the same is disclosed in a prospectus

relating to the Trust filed with the SEC pursuant to Rule 424 under the Securities Act. If platinum is to be delivered other than

as described above, the Sponsor is authorized to establish such procedures and to appoint such custodians and establish such custody

accounts in addition to those described in this report, as the Sponsor determines to be desirable.

Acting

on standing instructions given by the Trustee, the Custodian will transfer the platinum deposit amount from the Trust Unallocated

Account to the Trust Allocated Account by transferring platinum plates and ingots from its inventory to the Trust Allocated Account.

The Custodian uses commercially reasonable efforts to complete the transfer of platinum to the Trust Allocated Account prior to

the time by which the Trustee is to credit the Basket to the Authorized Participant’s DTC account; if, however, such transfers

have not been completed by such time, the number of Baskets ordered will be delivered against receipt of the platinum deposit

amount in the Trust Unallocated Account, and all Shareholders will be exposed to the risks of unallocated platinum to the extent

of that platinum deposit amount until the Custodian completes the allocation process. See “Risk Factors—Platinum held

in the Trust’s unallocated platinum account and any Authorized Participant’s unallocated platinum account is not segregated

from the Custodian’s assets.....”

Because

platinum is only allocated in multiples of whole plates or ingots, the amount of platinum allocated from the Trust Unallocated

Account to the Trust Allocated Account may be less than the total fine ounces of platinum credited to the Trust Unallocated Account.

Any balance will be held in the Trust Unallocated Account. The Custodian uses commercially reasonable efforts to minimize the

amount of platinum held in the Trust Unallocated Account; no more than 192 ounces of platinum (maximum weight to make one Good

Delivery Platinum Plate or Ingot) is expected to be held in the Trust Unallocated Account at the close of each business day.

Rejection

of purchase orders

The

Trustee may reject a purchase order or a Creation Basket Deposit if such order or Creation Basket Deposit is not presented in

proper form as described in the Authorized Participant Agreement or if the fulfillment of the order, in the opinion of counsel,

might be unlawful. None of the Trustee, the Sponsor or the Custodian will be liable for the rejection of any purchase order or

Creation Basket Deposit.

Redemption

Procedures

The

procedures by which an Authorized Participant can redeem one or more Baskets mirror the procedures for the creation of Baskets.

On any business day, an Authorized Participant may place an order with the Trustee to redeem one or more Baskets. Redemption orders

must be placed no later than 3:59:59 p.m. on each business day the NYSE Arca is open for regular trading. In the event of a level

3 market-wide circuit breaker resulting in a trading halt for the remainder of the trading day, the time of the market-wide trading

halt is considered the close of regular trading and no redemption orders for the current trade date will be accepted after that

time (the “cutoff”). Orders placed after the cutoff will be deemed to be rejected and will not be processed. Orders

should be placed in proper form on the following business day. A redemption order so received is effective on the date it is received

in satisfactory form by the Trustee. The redemption procedures allow Authorized Participants to redeem Baskets and do not entitle

an individual Shareholder to redeem any Shares in an amount less than a Basket, or to redeem Baskets other than through an Authorized

Participant.

By

placing a redemption order, an Authorized Participant agrees to deliver the Baskets to be redeemed through DTC’s book-entry system

to the Trust by the prescribed settlement date. Prior to the delivery of the redemption distribution for a redemption order, the

Authorized Participant must also have wired to the Trustee the non-refundable transaction fee due for the redemption order.

Determination

of redemption distribution

The

redemption distribution from the Trust consists of a credit to the redeeming Authorized Participant’s Authorized Participant

Unallocated Account representing the amount of the platinum held by the Trust evidenced by the Shares being redeemed. Fractions

of a fine ounce of platinum included in the redemption distribution smaller than 0.001 of a fine ounce are disregarded. Redemption

distributions will be subject to the deduction of any applicable tax or other governmental charges which may be due.

Delivery

of redemption distribution

The

redemption distribution due from the Trust will be delivered to the Authorized Participant on the prescribed settlement date following

a loco London redemption order date if, by 10:00 a.m. New York time on the settlement date, the Trustee’s DTC account has been

credited with the Baskets to be redeemed. If a loco swap or physical transfer is necessary to effect a loco London redemption,

the redemption distribution due from the Trust will be delivered to the Authorized Participant on or before the prescribed settlement

date if, by 10:00 a.m. New York time on the first business day after the loco London redemption order date, the Trustee’s DTC account has been credited with the Baskets

to be redeemed. In the event that, by 10:00 a.m. New York time on the prescribed settlement date, the Trustee’s DTC account has

not been credited with the total number of Shares corresponding to the total number of Baskets to be redeemed pursuant to such

redemption order, the Trustee shall send to the Authorized Participant and the Custodian via fax or electronic mail message notice

of such fact and the Authorized Participant shall have one business day following receipt of such notice to correct such failure.

If such failure is not cured within such one business day period, the Trustee (in consultation with the Sponsor) will cancel such

redemption order and will send via fax or electronic mail message notice of such cancellation to the Authorized Participant and

the Custodian, and the Authorized Participant will be solely responsible for all costs incurred by the Trust, the Trustee or the

Custodian related to the cancelled order. The Trustee is also authorized to deliver the redemption distribution notwithstanding

that the Baskets to be redeemed are not credited to the Trustee’s DTC account by 10:00 a.m. New York time on the prescribed settlement

date if the Authorized Participant has collateralized its obligation to deliver the Baskets through DTC’s book entry system on

such terms as the Sponsor and the Trustee may from time to time agree upon.

The

Custodian transfers the redemption platinum amount from the Trust Allocated Account to the Trust Unallocated Account and, thereafter,

to the redeeming Authorized Participant’s Authorized Participant Unallocated Account. The Authorized Participant and the

Trust are each at risk in respect of platinum credited to their respective unallocated accounts in the event of the Custodian’s

insolvency. See “Risk Factors—Platinum held in the Trust’s unallocated platinum account and any Authorized Participant’s

unallocated platinum account is not segregated from the Custodian’s assets.....”

As

with the allocation of platinum to the Trust Allocated Account which occurs upon a purchase order, if in transferring platinum

from the Trust Allocated Account to the Trust Unallocated Account in connection with a redemption order there is an excess amount

of platinum transferred to the Trust Unallocated Account, the excess over the platinum redemption amount will be held in the Trust

Unallocated Account. The Custodian uses commercially reasonable efforts to minimize the amount of platinum held in the Trust Unallocated

Account; no more than 192 ounces of platinum (maximum weight to make one Good Delivery Platinum Plate or Ingot) is expected to

be held in the Trust Unallocated Account at the close of each business day.

Suspension

or rejection of redemption orders

The

Trustee may, in its discretion, and will, when directed by the Sponsor, suspend the right of redemption, or postpone the redemption

settlement date, (1) for any period during which the NYSE Arca is closed other than customary weekend or holiday closings, or

trading on the NYSE Arca is suspended or restricted or (2) for any period during which an emergency exists as a result of which

delivery, disposal or evaluation of platinum is not reasonably practicable. None of the Sponsor, the Trustee or the Custodian

are liable to any person or in any way for any loss or damages that may result from any such suspension or postponement.

The

Trustee will reject a redemption order if the order is not in proper form as described in the Authorized Participant Agreement

or if the fulfillment of the order, in the opinion of its counsel, might be unlawful.

Creation

and Redemption Transaction Fee

To

compensate the Trustee for services in processing the creation and redemption of Baskets, an Authorized Participant is required

to pay a transaction fee to the Trustee of $500 per order to create or redeem Baskets. An order may include multiple Baskets.

The transaction fee may be reduced, increased or otherwise changed by the Trustee with the consent of the Sponsor. From time to

time, the Trustee, with the consent of the Sponsor, may waive all or a portion of the applicable transaction fee. The Trustee

shall notify DTC of any agreement to change the transaction fee and will not implement any increase in the fee for the redemption

of Baskets until 30 days after the date of the notice.

The

Sponsor

The

Trust’s Sponsor is abrdn ETFs Sponsor LLC, a Delaware limited liability company formed on June 17, 2009.

The

Sponsor’s office is located at c/o abrdn ETFs Sponsor LLC, 1900 Market Street, Suite 200, Philadelphia, PA 19103.

Prior to April 27, 2018, the Sponsor was wholly-owned by ETF Securities Limited, a Jersey, Channel Islands based company.

Effective April 27, 2018, ETF Securities Limited sold its membership interest in the Sponsor to abrdn Inc. (known as Aberdeen

Standard Investments Inc. prior to January 1, 2022) a Delaware corporation. As a result of the sale, abrdn Inc. became the

sole member of the Sponsor. abrdn Inc. is a wholly-owned indirect subsidiary of abrdn plc, which together with its affiliates

and subsidiaries, is collectively referred to as “abrdn.” Under the Delaware Limited Liability Company Act and

the governing documents of the Sponsor, the sole member of the Sponsor, abrdn Inc., is not responsible for the debts,

obligations and liabilities of the Sponsor solely by reason of being the sole member of the Sponsor.

The

Sponsor’s Role

The

Sponsor arranged for the creation of the Trust, and is generally responsible for the ongoing registration of the Shares for their

public offering in the United States and the listing of the Shares on the NYSE Arca. The Sponsor has agreed to assume the

organizational expenses of the Trust and the following administrative and marketing expenses incurred by the Trust: the

Trustee’s monthly fee and out-of-pocket expenses, the Custodian’s fee and the reimbursement of the Custodian’s

expenses under the Custody Agreements, exchange listing fees, SEC registration fees, printing and mailing costs, audit fees and up