false

2024-10-16

0001385849

Energy Fuels Inc.

0001385849

2024-10-16

2024-10-16

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

October 16, 2024

ENERGY FUELS INC.

(Exact name of registrant as specified in its charter)

|

Ontario

|

001-36204

|

98-1067994

|

| (State or other jurisdiction |

(Commission |

(IRS Employer |

| of incorporation) |

File Number) |

Identification No.) |

225 Union Blvd., Suite 600

Lakewood, Colorado, United States

80228

(Address of principal executive offices) (ZIP Code)

Registrant’s telephone number, including area code: (303) 974-2140

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading Symbols |

|

Name of each exchange on which registered |

|

Common shares, no par value

|

|

UUUU

|

|

NYSE American LLC

|

| |

|

EFR |

|

Toronto Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§ 230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§ 240.12b -2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

EXPLANATORY NOTE

As previously reported in a Current Report on Form 8-K dated October 3, 2024 (the "Closing Form 8-K"), EFR Australia Pty Ltd ("EFR"), a wholly owned subsidiary of Energy Fuels Inc. (the "Company" or "Energy Fuels" or "we" or "us" or "our"), completed the acquisition of all of the fully paid ordinary shares (the "Transaction") of Base Resources Limited ("Base Resources") on October 2, 2024 (the "Implementation Date") pursuant to a Scheme Implementation Deed dated April 21, 2024 by and among the Company, EFR and Base Resources (the "Deed").

In a Form 8-K dated October 3, 2024, the Company provided details of the completion of the acquisition of Base Resources required by Item 2.01 of Form 8-K and filed the financial statements and pro forma financial information required by Regulation S-X. Then, in a Form 8-K dated October 8, 2024, the Company provided additional details of the completion of the acquisition of Base Resources required by Items 3.02 and 5.02 of Form 8-K (together with the October 3, 2024 Form 8-K, the “Closing Forms 8-K”). This Form 8-K should be read in conjunction with the Closing Forms 8-K.

The purpose of this Form 8-K is to supplement the Company's material disclosure for its post-Transaction business operations.

Item 8.01. Other Events.

The disclosure contained in this Item 8.01 has not previously been filed by the Company. This disclosure is intended to supplement rather than replace the Company's previous disclosures, except to the extent explicitly amended by this Form 8-K. Accordingly, the disclosure in this Item 8.01 should be read in conjunction with the Company's previous disclosure, including the disclosure contained in the Company's Annual Report on Form 10-K for the year ended December 31, 2023, as amended (the "FY23 Form 10-K"), and the Company's quarterly reports for the quarters ended March 31, 2024 and June 30, 2024.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Form 8-K contains "forward-looking statements" and "forward-looking information" within the meaning of applicable United States ("U.S.") and Canadian securities laws (collectively, "forward-looking statements"), which may include, but are not limited to, statements with respect to the Company's: anticipated results and progress of our operations in future periods; planned exploration; development of our properties; plans related to our business, such as the ramp-up of our uranium business in response to improved uranium prices, our rare earth element ("REE") line of business, including work on our Kwale heavy mineral sands ("HMS") project in Kenya (the "Kwale Project"), Toliara HMS and REE project in Madagascar (the "Toliara Project"), Donald HMS and REE joint venture project in Australia (the "Donald Project") and South Bahia HMS and REE project in Brazil (the "Bahia Project") and our planned development of capabilities for the commercial separation of REEs at our White Mesa Mill (the "White Mesa Mill" or the "Mill") in Utah; plans related to our potential recovery of radioisotopes at the Mill for use in the production of targeted alpha therapy ("TAT") medical treatments; any plans related to the acquisition of additional mineral properties; any plans relating to the ramp-up of production or ongoing operations at any of our uranium, uranium/vanadium and/or HMS properties; historic estimates of resources and reserves; production estimates; maintenance and renewal of permits; expectations to enter into binding agreements with the Government of Madagascar as it relates to the Toliara Project; and expectations for the outcome of pending litigation. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, schedules, assumptions, future events, or performance (often, but not always, using words or phrases such as "expects" or "does not expect," "is expected," "is likely," "budgets," "scheduled," "forecasts," "intends," "anticipates" or "does not anticipate," "continues," "plans," "estimates," or "believes," and similar expressions or variations of such words and phrases or statements stating that certain actions, events or results "may," "could," "would," "might," or "will" be taken, occur or be achieved) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made. We believe that the expectations reflected in these forward-looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct, and such forward-looking statements included in, or incorporated by reference into, this Annual Report should not be unduly relied upon.

Readers are cautioned that it would be unreasonable to rely on any such forward-looking statements as creating any legal rights, and that the forward-looking statements are not guarantees and may involve known and unknown risks and uncertainties, and that actual results are likely to differ (and may differ materially), and objectives and strategies may differ or change, from those expressed or implied in the forward-looking statements as a result of various factors. Such risks and uncertainties include, but are not limited to: global economic risks, such as the occurrence of a pandemic, political unrest or wars; cybersecurity risks associated with critical and other highly sensitive minerals of international interest, which are key to national security; risks associated with the restart and subsequent operation of any of our uranium, uranium/vanadium and HMS mines; risks associated with our commercial production of an REE carbonate ("RE Carbonate") or separated REE oxides and the planned expansion of such production, and risks associated with the exploration and development of our Bahia Project in Brazil; risks associated with the potential recovery of radioisotopes for use in the Company's TAT initiatives; risks associated with potential mineral acquisitions internationally, including geopolitical considerations; risks associated with increased regulatory requirements applicable to our operations in response to pressure from special interest groups or otherwise; and risks generally encountered in the exploration, development, operation, closure and reclamation of mineral properties and processing and recovery facilities. Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors which could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation the following risks which are in addition and supplementary to the risk factor disclosed in the Company's FY23 Form 10-K:

• failure to complete and integrate proposed acquisitions, and/or to incorrectly assess the value of or risks associated with completed acquisitions, including our acquisition of mineral concessions at the Bahia Project, the Donald Project and Base Resources (which owns the Toliara Project) and any future acquisitions; and

• risks associated with fluctuations in price levels for HMS concentrate ("HMC") and its components, including the prices for ilmenite, rutile, titanium and zircon, which could impact planned production levels or the feasibility of production of HMC and monazite from our Bahia Project, Toliara Project, the Donald Project and any other HMS project the Company may acquire or participate in, which could impact monazite supply for our RE Carbonate, separated REE oxide and any other REE value-added product production.

The following information pertains to the outlook and conditions currently known to the Company that could have a material impact on its financial condition. Other factors may arise in the future that are currently not foreseen by management of the Company that may present additional risks, including risks that the Company currently believes are immaterial. Current and prospective shareholders of the Company should carefully consider these risk factors in conjunction with the risk factors contained in the FY23 Form 10-K when making investment decisions.

Our failure to successfully address any of the risks and uncertainties described below could have a material adverse effect on our business, financial condition and/or results of operations, and the trading price of our common shares may fluctuate widely. We cannot assure you that we have or will successfully or fully address these risks or other unknown risks that may affect our business.

Market, Industry and Other Data

This Form 8-K contains estimates, projections and other information concerning our industry, our business and the markets for our products. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances that are assumed in this information. Unless otherwise expressly stated, we obtained this industry, business, market and other data from our own internal estimates and research, as well as from reports, research surveys, studies and similar data prepared by market research firms and other third parties, industry and general publications, government data, and similar sources.

RISK FACTORS

Risks Related to our Business

Mining, extraction, recovery, processing, construction, development and exploration activities depend, to a substantial degree, on adequate infrastructure.

Reliable roads, bridges, power sources and water supply are important determinants affecting capital and operating costs for existing and planned operations. For the Toliara Project, the Donald Project and the Bahia Project, new infrastructure will need to be built to support activities. However, unusual or infrequent weather phenomena, including drought, flooding, sabotage, government and/or other interference in the maintenance or provision of such infrastructure could adversely affect our operations and activities, financial condition and results of operations.

Risks associated with our REE business.

There are a number of risks inherent to our REE activities, which include the following revised risk:

The risk of achieving and maintaining an adequate supply of monazite feed for processing at the Mill. Although the Company has acquired the Bahia Project, it is currently at the exploration and permitting stage and is not an operating mine. The same consideration applies to the Toliara Project and the Donald Project, although the Toliara Project is at a more advanced stage. As a result, the Company does not currently own its own operating monazite-bearing mine(s) and is completely dependent on contractual arrangements for its REE feed sources at this time. There can be no guarantee that the Company will be able to secure adequate monazite supply over the long-term at suitable prices or that the Bahia Project, Toliara Project or the Donald Project will be developed into operating monazite-producing mines. In addition, the price the Company may be required to pay for monazite sands is subject not only to commercial factors but also to the risk of influence by foreign policy and/or foreign state-owned enterprises. We will evaluate potential acquisitions of additional mines or resource properties and joint ventures with mine or resource property owners, but there can be no guarantee that any such acquisitions or joint ventures can be realized on acceptable terms. Further, to the extent the Company is required to purchase monazite ore sources and rely on REE separation facilities located outside the U.S., we may be at a transportation cost disadvantage compared to processing facilities in China or elsewhere that may be closer to potential ore sources and/or REE separation facilities.

We may need additional financing in connection with the implementation of our business and strategic plans from time to time.

The exploration, construction, development and acquisition of mineral properties and the ongoing operation of mines and other facilities, including the Toliara Project, the Donald Project and the Bahia Project, requires a substantial amount of capital and may depend on our ability to obtain financing through joint ventures, debt financing, equity financing and/or other means. We may accordingly need further capital in order to take advantage of further opportunities or acquisitions. Our financial condition, general market conditions, volatile REEs, HMC, uranium and vanadium markets, volatile interest rates, legal claims against us, a significant disruption to our business or operations, or other factors may make it difficult to secure financing necessary for the expansion of mining activities or to take advantage of opportunities for acquisitions. Further, volatility in the credit markets may increase costs associated with debt instruments due to increased spreads over relevant interest rate benchmarks, or may affect our ability, or the ability of third parties we seek to do business with, to access those markets. Continued volatility in equity markets, specifically including energy and commodity markets, may increase the costs associated with equity financings due to a low share price and may create the potential need for us to offer higher discounts and other value (e.g., warrants). There is no assurance that we will be successful in obtaining required financing as and when needed on acceptable terms, if at all.

We are subject to costs associated with decommissioning and reclamation of our properties.

For so long as we are and remain the owner and operator of the Mill, Kwale Operations, the Nichols Ranch Project and numerous REEs, HMC, uranium, uranium/vanadium, REE and HMS projects and other facilities located in the U.S., Brazil, Africa and elsewhere, and certain other permitting, construction, development and exploration properties, we are obligated to ultimately reclaim or participate in the reclamation of our properties upon the occurrence of certain predetermined criteria using closely monitored and carefully developed, approved methods. Our reclamation obligations in the U.S. are bonded, and cash and other assets have been reserved to secure a portion, but not all, of the bonded amounts. Although our financial statements will record a liability for the asset retirement obligation, and the bonding requirements are generally periodically reviewed by applicable regulatory authorities, there can be no assurance or guarantee that the ultimate cost of such reclamation obligations will not exceed the estimated liability to be provided on our financial statements. Further, to the extent the bonded amounts are not fully collateralized, we will be required to come up with additional cash to perform our reclamation obligations when they occur.

Decommissioning plans for our properties in the U.S. have been filed with applicable regulatory authorities. These regulatory authorities have accepted the decommissioning plans in concept, not upon a detailed performance forecast, which has yet to be generated. Over time, further regulatory review of the decommissioning plans may result in additional decommissioning requirements, associated costs and the requirement to provide additional financial assurances, including as our properties approach or go into decommissioning. It is not possible to predict what level of decommissioning and reclamation (and financial assurances relating thereto) may be required in the future by regulatory authorities. The decommissioning and rehabilitation plan for Kwale Operations has been filed with the Kenyan National Environment Management Authority with approval to proceed granted on September, 25 2024. While the financial statements of Base Resources provide for the estimated costs of this decommissioning and rehabilitation for Kwale Operations, there can be no assurance or guarantee that the ultimate cost of such decommissioning and rehabilitation will not exceed the estimated liability provided in the financial statements.

We face heightened risks relating to the business we conduct in foreign jurisdictions which could have a material adverse effect on our operations, liquidity and/or financial condition.

The Company faces a number of risks related to conducting business operations in foreign jurisdictions (including Brazil, Australia and Africa), such as heightened risks of political instability, expropriation of assets, business interruption, increased taxation, import/export controls, unilateral modification of concessions and contracts. We also face the typical risks associated with doing business in foreign countries, including: different market and economic forces, resulting from new business environments with new competitors and different consumer preferences; dealing with local suppliers who may have a strong foothold in the area; the need to build up brand awareness and trust in a new market; different customer and supplier demographics; language and cultural barriers; extreme weather events and natural disasters that can present a sustained business risk relating to supply logistics and other factors; the additional requirements of foreign legal systems; the impacts of foreign tax requirements; the need to comply with foreign regulations and operations compliance; the need to comply with foreign legal systems, including as they relate to contract enforceability; the requirement to stay abreast of and remain in compliance with changing laws and regulations; inconsistent application of existing laws; social unrest; and the lack of purchasing power parity compared to domestic competitors. Any number of these risks could have a material adverse effect on our operations, liquidity and/or financial condition.

Our operations outside the United States and Canada require us to comply with a number of United States, Canadian and international regulations, violations of which could have a material adverse effect on our business, consolidated results of operations, and consolidated financial condition.

Our operations outside the United States and Canada require us to comply with a number of United States, Canadian, Australian, African and other international regulations. For example, our operations in countries outside the United States and Canada are subject to the United States Foreign Corrupt Practices Act ("FCPA"), which prohibits United States companies and their agents and employees from providing anything of value to a foreign official for the purposes of influencing any act or decision of these individuals in their official capacity to help obtain or retain business, direct business to any person or corporate entity, or obtain any unfair advantage, as well as to the Corruption of Foreign Public Officials Act ("CFPOA"), which is the Canadian equivalent of the FCPA. Our activities create the risk of unauthorized payments or offers of payments by our employees, agents, or joint venture partners that could be in violation of anti-corruption laws, even though some of these parties are not subject to our control. We have internal control policies and procedures and are implementing additional training and compliance programs for our employees and agents with respect to the FCPA and CFPOA. However, we cannot assure that our policies, procedures, and programs will always protect us from reckless or criminal acts committed by our employees or agents. We are also subject to the risks that our employees, joint venture partners, and agents outside of the U.S. may fail to comply with other applicable laws. Allegations of violations of applicable anti-corruption laws may result in internal, independent, or government investigations. Violations of anti-corruption laws may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could have a material adverse effect on our business, consolidated results of operations and consolidated financial condition.

The Company may face tax risks in certain operating foreign jurisdictions and unexpected taxes could be imposed on us which could have a material and adverse effect on our financial position.

Our operations and business in foreign jurisdictions, including Brazil, Australia and Africa, may increase our susceptibility to sudden tax changes. Taxation laws in these jurisdictions are complex, subject to varying interpretations and applications by the relevant tax authorities and subject to changes and revisions in the ordinary course. Any unexpected taxes imposed on us could have a material and adverse impact on our financial position.

We face risks associated with a Brazilian federal or state government enacting or managing a conservation unit or environmental protection area which could have a material adverse effect on our operations, liquidity and/or financial condition.

In respect of the Company's Bahia Project in Brazil, there is a risk of a Brazilian federal or state government enacting or managing a conservation unit or environmental protection area or implementing a management plan in connection therewith that could impact planned production at or restrict the Company's ability to or prevent the Company from mining the Company's Bahia Project, or portions thereof. Such an action could have a material adverse effect on our operations, liquidity and/or financial condition.

Our operations in Africa expose us to regional-specific social, political, economic and/or other risks.

The Company's operations in Africa may expose us to uncertain social, political or economic conditions and/or other risks. Government agencies or other counterparties could seek to assert rights of expropriation, renegotiation or nullification of existing concessions, contracts and pricing benchmarks, challenges to title to properties or mineral rights or delays renewing licenses and permits. Such government agencies or other counterparties may also seek to impose onerous fiscal policy, onerous regulation, changes in law or policy governing existing operations, financial constraints and unreasonable taxation.

There is also a risk that foreign public officials or government agencies will act unreasonably towards us. There can be no assurance that these foreign public officials or government agencies or other counterparties will not take the steps noted above in respect of the Company's operations and, if any such steps are taken, there can be no assurance that sufficient remedies will be available to recoup the investments that have been made to date in such areas. The occurrence of any such events in respect of the Company's operations in such foreign nations could adversely affect the Company's business and results of operations.

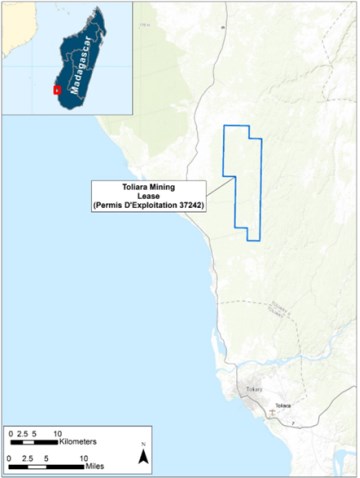

The development of the Toliara Project requires certain actions of the Government of Madagascar and the Company entering into binding agreements, neither of which may occur on a timely basis, at all or on acceptable terms. Further, the development of the Toliara Project is dependent on several factors beyond our control.

Development of the Toliara Project is dependent on lifting the current suspension of on-ground activities imposed by the Government of Madagascar and an agreement on the fiscal terms applicable to the project. There is no certainty that binding fiscal terms for the Toliara Project will be agreed and that the suspension will be lifted or that these milestones will be achieved on a timely basis.

Once the suspension is lifted, development of the Toliara Project will be dependent on several factors including, but not limited to:

- securing requisite fiscal and legal stability (e.g. through eligibility certification under the Law No. 2001-031 on large scale mining investments dated 8 October 2002 as amended by law No. 2005-022 dated 27 July 2005 and put into effect by Decree no 2003-784 dated 8 January 2003);

- entering into an acceptable investment agreement (or similar agreement) addressing fiscal and other key terms governing the Project and also providing necessary legal clarifications in relation to applicable law;

- ratification by the Malagasy Parliament of an acceptable investment agreement (or similar agreement);

- having monazite included as a mineral for exploitation on the Toliara exploitation permit on a timely basis or at all;

- securing requisite land access for the Toliara exploitation permit and the Toliara Project's associated infrastructure;

- access to adequate capital to fund development;

- obtaining regulatory consents and approvals necessary for, or exemptions beneficial to, development and production on a timely basis or at all;

- commodity prices and securing necessary offtakes on reasonable terms;

- geotechnical conditions;

- recruitment and retention of appropriately skilled and experienced employees, contractors and consultants; and

- maintaining positive relations with host communities and regional and national governments/officials.

Risk associated with the closure of Kwale Operations.

The closure of Kwale Operations and conclusion of mining and processing activities is subject to several risks for the Company including, but not limited to:

- adequate financial provisioning for closure and rehabilitation;

- environmental contamination, including soil erosion and water pollution;

- potential harm to personnel on site during closure, including employees and contractors;

- meeting and adherence to evolving regulations and standards, as well as international industry good practice;

- managing community and Government relations and expectations and addressing any concerns;

- technical challenges in implementing effective rehabilitation methods;

- long-term monitoring as part of ensuring rehabilitation effectiveness and management of the tailings storage facility;

- maintaining public trust and social license through communication and engagement; and

- resolving current and potential legal disputes on acceptable terms, including with community, government and government related bodies, third party royalty holders and site employees (for example, over contractual obligations, severance packages, and associated employment termination issues).

Risks associated with the Donald Project Joint Venture.

Our ability to earn our 49% interest in the Donald Project is dependent on completion of the joint venture occurring for the purposes of the joint venture agreement dated June 4, 2024 (the "JVA") by and among the Company, our wholly owned subsidiary EFR Donald Ltd and Astron Corporation Limited ("Astron"), and the final investment decision to proceed with the development of phase 1 of the Donald being unanimously passed by the Company and Astron (the "Donald FID"). The development of the Donald Project and the ability of the parties to approve the Donald FID and to develop and operate the project is dependent on a number of factors including, but not limited to:

- the project being fully permitted, including receiving approval of the work authority for the phase 1 mine plan and additional regulatory approvals required for the mining, transport and export of REE concentrate;

- an evaluation of the economics of phase 1 taking into account: the conclusions and recommendations in the Updated Phase 1 Definitive Feasibility Study; expected REE concentrate and HMC recoveries from the planned facilities; the development plan and budget for phase 1, and cash flow forecasts for both the joint venturers;

- the Company having secured commitments for satisfactory offtake and/or sales agreements for the separated REE products expected to be produced at the Mill from the Donald Project REE concentrate;

- Astron and/or the joint-venture entity, Donald Project Pty Ltd, having secured commitments for satisfactory offtake and/or sales agreements for HMC;

- Donald Project Pty Ltd having secured commitments for non-recourse and/or government-backed debt financing for the project development costs required in addition to the Company's A$183 million earn-in amount;

- Donald Project Pty Ltd having secured certain land rights and/or access agreements for the project including its associated infrastructure;

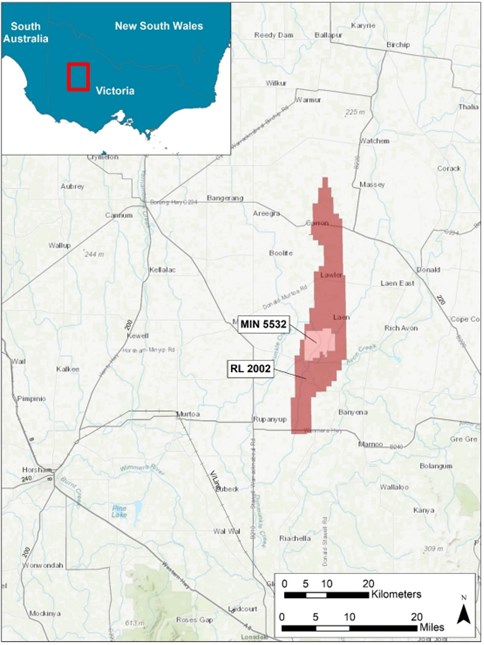

- Donald Project Pty Ltd maintaining and renewing tenements relating to the Donald Project including MIN5532, the current term of which expires in 2030 (and for phase 2 the conversion of RL2002 into a mining lease);

- counter party risk in relation to Astron's ability to perform its obligations under the JVA and related transaction documents;

- obtaining all required local, state and federal consents and approvals required on a timely basis; and

- securing construction and engineering contracts, as well as equipment and spare parts, on acceptable terms and in accordance with project requirements.

We are subject to foreign currency risks which could have a material impact on our cash flows and profitability.

Our operations are subject to foreign currency fluctuations. Our operating expenses and revenues are primarily incurred in U.S. dollars, while some of our cash balances and expenses are measured in Canadian dollars. The operations of Base Resources are also primarily conducted in U.S dollars, but Base Resources conducts some of its business in currencies other than the U.S dollar (including, Australian dollars, Kenyan Shillings and Malagasy Ariary). The fluctuation of the Canadian dollar, Australian dollar, Kenyan Shilling and/or Malagasy Ariary in relation to the U.S. dollar will consequently have an impact on our profitability and may also affect the value of our assets and shareholders' equity. In addition, any strengthening of the U.S. dollar relative to other currencies makes our mineral extraction and recovery less competitive in relation to similar activities in other countries. Any strengthening of the U.S. dollar in relation to the currencies of other countries makes the Company's mineral impact less competitive in relation to similar activities in other countries and could have a material impact on our cash flows and profitability and affect the value of our assets and shareholders' equity.

We may not realize the anticipated benefits of previous acquisitions which could impair our results of operations, profitability and/or financial results.

We may not realize the anticipated benefits of acquiring: the Sheep Mountain Project in 2012; Denison Mines Corp.'s U.S. Mining Division in 2012, including the Mill, certain of the Arizona Strip Properties, the Bullfrog Project and the La Sal Project; Strathmore in 2013, including the Roca Honda Project; Uranerz in 2015, including the Nichols Ranch Project; the Bahia Project in Brazil in 2023; the Donald Project in Australia in 2024; and Base Resources in 2024, which owned the Toliara Project in Africa, due to integration, operational and uranium, REE, HMC, uranium and/or vanadium market challenges. Decreases in commodity prices have required us to place or maintain a number of acquired properties and facilities on standby and to defer permitting and construction and development activities on certain other acquired assets, until market conditions warrant otherwise, and, in some cases, we have elected to sell or abandon certain of these properties at a loss. Our success following those acquisitions will depend in large part on the success of our management in valuing the acquired assets and integrating the acquired assets into the Company. Our failure to properly value the assets and to achieve such integration and to mine or advance such assets could result in our failure to realize the anticipated benefits of those acquisitions and could impair our results of operations, profitability and/or financial results.

Our relationship with our employees may be impacted by changes in labor relations which could have a material adverse impact on our cash flows, earnings, results of operations and/or financial condition.

One of our new subsidiaries, Base Titanium Limited (“Base Titanium”), is a party to a collective bargaining agreement for a significant portion of its Kwale Operations workforce; however, none of our other operations or activities currently directly employ unionized workers who work under collective agreements. There can be no assurance that our employees or the employees of our contractors will not become unionized in the future or, in relation to Base Resources, that it will not become the subject of industrial action in relation to the portion of its Kwale Operations workforce that work under a collective agreement, which may impact our operations and activities. Any lengthy work stoppages may have a material adverse impact on our future cash flows, earnings, results of operations and/or financial condition.

Investors in jurisdictions outside of Canada may have difficulty bringing actions and enforcing judgments under their respective jurisdiction's securities laws against an Ontario corporation.

Although our primary trading market is the NYSE American, a majority of our outstanding voting securities are registered in the names of holders in the U.S. and we are a U.S. domestic issuer for reporting purposes with the United States Securities and Exchange Commission (the "SEC"), and substantially all of our assets, operations and employees are in the U.S., the Company was incorporated in Ontario and, as a result, investors in the U.S. or in other jurisdictions outside of Canada may have difficulty bringing actions and enforcing judgments against us, our directors, our executive officers and some of the experts named in this Form 8-K and the Company’s other SEC filings, including the FY23 Form 10-K, based on civil liabilities provisions of the federal securities laws or other laws of the U.S. or any state thereof or the equivalent laws of other jurisdictions of residence.

General Risk Factors

Russia's Invasion of Ukraine is severely and unpredictably impacting global energy markets and supply chains, and rising concerns over a second severe nuclear accident in Ukraine could seriously hurt public reception to nuclear energy.

Russia's February 2022 invasion of Ukraine continues to severely impact global energy markets and supply chains by causing economic uncertainty, price volatility, supply shortages and national security concerns to such a degree that the International Energy Agency ("IEA") has called it "the first truly global energy crisis, with impacts that will be felt for years to come." As the Company is engaged in a number of energy sectors, including REEs, HMS, uranium and vanadium, it is expected that such global impacts will necessarily impact the Company, though the full extent of any such impacts are not well understood at this time. While supply and shipping impacts could materially interfere with our ability to conduct business, other global responses - such as the U.S. Inflation Reduction Act's provision of funds for energy and climate programs, including the expansion of tax credits and incentives to promote clean energy technologies, and an apparent shift away from global reliance on Russian exports via government sanctions and other means - could materially benefit our business by creating additional market opportunities with utilities providers attempting to lessen their reliance on Russian markets.

The uranium industry also potentially faces renewed skepticism and distrust as a result of Russia's invasion of Ukraine. According to the World Nuclear Association ("WNA"), "In the early hours of 4 March the Zaporizhzhia plant in southeastern Ukraine became the first operating civil nuclear power plant to come under armed attack. Fighting between forces overnight resulted in a projectile hitting a training building within the site of the six-unit plant. Russian forces then took control of the plant. The six reactors were not affected and there was no release of radioactive material. Since late October 2022, Russia has repeatedly targeted Ukraine's civilian infrastructure, including the country's energy system, with missile strikes. Widespread blackouts have resulted, and external power supply to all four of the country's nuclear plants has been affected." (WNA, "Ukraine: Russia-Ukraine War and Nuclear Energy," Feb. 6, 2023). Russia's interference with Ukrainian nuclear plants in violation of Article 56 of the Additional Protocol of 1979 to the Geneva Conventions, which states that nuclear power plants "shall not be made the object of attack, even where these objects are military objectives, if such an attack may cause the release of dangerous forces and consequent severe losses among the civilian population" (WNA, 2023), may result in increased and serious harm to global reception to nuclear energy due to the current war's proximity to Chernobyl, site of the then-Soviet Union's 1986 nuclear accident.

DESCRIPTION OF BUSINESS

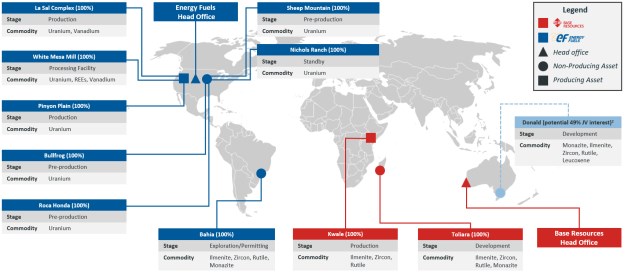

Overview of the Company After Taking into Account the Base Resources Acquisition

Following the acquisition of Base Resources, the Company has the following portfolio of operating and development projects:

Notes:

(1) Non-material mineral properties are not shown; For ease of presentation, U.S. assets have been grouped based on classification, and their location as per the map may not be indicative of their actual location

(2) Energy Fuels has entered a Joint Venture Agreement with Astron Corporation Limited to earn up to a 49% joint venture interest in the Donald Project

(3) The Toliara Exploitation Permit does not presently provide a right to exploit monazite and operations are currently suspended.

The Kwale, Toliara and Donald Project assets are described in more detail in the section entitled "Description of Properties: Additional Material Properties," below.

Expected Synergies Resulting from the Acquisition of Base Resources

Energy Fuels believes the acquisition of Base Resources has the potential to unlock significant value for the Company due to readily identifiable synergies, as outlined below:

- The combination of Base Resources' Toliara Project with Energy Fuels' White Mesa Mill in Utah, the only fully operating, licensed uranium mill in the United States, with existing and planned monazite crack-and-leach processing and rare earth separation capability (combined with Energy Fuels' existing projects), has the potential to position the Company as one of the world's leaders in both REE and HMS production.

- Once the Toliara Project is in production, the project has the potential to be a low-cost and large-scale HMS project. In addition to its ilmenite, rutile (titanium) and zircon (zirconium) production, the Toliara Project also contains large quantities of monazite which is a rich source of the 'magnet' REEs used in electric vehicles and a variety of clean energy and advanced technologies. As this monazite will be a byproduct of the Toliara Project's ilmenite, rutile and zircon production, it is expected to be recovered at a low incremental cost of production and therefore to be globally competitive.

- Once the Toliara Project is in production, the available monazite is expected to provide a large portion of the feed material needed for Energy Fuels' expanding REE production facility at the Mill.

- Processing low-cost Toliara Project monazite at the White Mesa Mill into separated rare earth elements is expected to set a new paradigm for U.S.-REE production and is expected to position the Company as a first-tier REE producer, as well as a first-tier ilmenite, rutile and zircon producer.

- The acquisition of Base Resources is also expected to complement and further strengthen the Company's uranium production capability, as monazite from the Toliara Project would provide sustainable quantities of low-cost uranium production at the Mill, which would supplement the Company's U.S.-sourced uranium production.

- With a strong balance sheet, the Company believes it will be well placed to secure funding for the planned expansion of the Mill, the development of the Company's Toliara, Bahia and Donald projects, as well as take advantage of other integration opportunities in the REE value chain, including potential rare earth metal, metal alloy and magnet making to serve North American and European markets.

- With Energy Fuels currently being the only fully integrated producer of separated REE products from monazite in the U.S. and the Company having the potential to go further downstream, the Company will be positioned to support the U.S. Government's critical minerals and national security objectives.

- Base Resources has a proven mineral sands operations management team with a strong track record of responsible and profitable production at its now winding down Kwale Operations. This team has joined the Company and is expected to continue managing the Toliara Project and enhance the Company's capability to develop its projects in Australia and Brazil.

With the Mill's unique, U.S.-based REE production capability, the Company believes it is well-positioned to unlock significant value from the Toliara Project's potential low-cost monazite production, in a manner that Energy Fuels believes few, if any, other facilities are capable of at this time. This potential addition of a low-cost source of REE raw materials to Energy Fuels' U.S. REE production infrastructure, along with a sustainable low-cost source of uranium production and HMS assets, is expected to deliver significant synergies for the Company.

Energy Fuels' Current Intentions

Corporate Structure

Upon the closing of the Transaction (the "Closing"), Base Resources became a wholly owned indirect subsidiary of Energy Fuels and ceased to be a publicly traded company.

Strategy

Through the combination of Base Resources' proven leadership and mineral sands operations team with Energy Fuels' proven leadership team in uranium and vanadium production, recycling activities and rapidly advancing REE capabilities, the Company believes it is well-positioned to execute its strategy and pursue its initiatives.

Following Closing, the Company's strategy will be to further establish itself as a first tier, globally competitive critical minerals mining company, focused on REE, HMS, uranium, and vanadium production.

To that end, the Company currently intends to pursue the following specific strategic initiatives:

- complete mining and then rehabilitation of Kwale Operations in accordance with all commitments, laws and regulations and in a manner that sets a high standard for rehabilitation of mining projects in Africa and establishes a reputation for excellence in the full life cycle of mining;

- obtain necessary agreements and authorizations to further assess, develop and operate the Toliara Project as one of the world's leaders in HMS and monazite production;

- continue with the exploration, permitting, evaluation and if determined feasible, proceed with development and operation of the Company's Bahia Project;

- complete the activities required to make a phase 1 final investment decision on the Donald Project, and if a positive final investment decision is made, continue with the development of the Donald Project;

- continue with the engineering, design and permitting of the planned phase 2 and phase 3 REE separation circuits at the Mill and development of those facilities;

- continue current uranium production at the Mill, proceed with planned uranium production at the Company's Nichols Ranch ISR Project as market conditions warrant, and continue mining of uranium ore from the Company's Pinyon Plain, La Sal, Pandora and, as market conditions warrant, Whirlwind mines;

- continue with permitting of uranium mining at the Company's Roca Honda, Sheep Mountain and Bullfrog mining projects, as market conditions warrant;continue with current and planned vanadium production at the Mill from ore mined from the Company's La Sal, Pandora and Whirlwind mines, and potentially from the recycling of tailings solutions at the Mill, as market conditions warrant;

- continue to advance the Mill's alternate feed material uranium recycling and abandoned uranium mine clean-up programs, and the evaluation of the recovery of radium at the Mill for use in emerging targeted alpha therapy cancer therapeutics;

- as the only fully integrated producer of separated REE products from monazite in the U.S. (and as a potential producer of critical minerals sourced from Australia), seek available financial and other support from U.S. and Australian government agencies and other stakeholders that provide such support for critical mineral projects;

- evaluate any opportunities for acquisitions of additional HMS, REE, uranium, vanadium or other critical mineral properties that may arise, as well as take advantage of other opportunities in the HMS and rare earth industries as they present, including potential opportunities in rare earth metal-, metal alloy- and magnet-making; and

- perform all activities to leading environmental, social and governance ("ESG") standards and advance the Company's sustainability programs.

Dividend Framework

Energy Fuels has not declared cash dividends on its common shares to date. Energy Fuels anticipates that it will retain any earnings to support operations and to finance the growth of the Company's business (including the pursuit of the strategy outlined above). Therefore, the Company does not expect to pay cash dividends in the foreseeable future. Any future determination to pay cash dividends will be at the discretion of the Company's Board and will be dependent on the financial condition, operating results and capital requirements of the Company, and other factors that the Company's Board deems relevant.

Current Base Resources Employees

Base Resources' workforce is expected to continue in their existing roles following the Closing, noting the planned end of production at the Kwale Operations in 2024 as described in the section entitled "Description of Properties: Additional Material Properties," below.

Headquarters

After Closing the Company's head office will continue to be located at its existing corporate offices in Lakewood, Colorado, USA. Base Resources' existing office in West Perth, Australia, will continue to operate and is intended to be the headquarters of the Company's mineral sands and monazite feedstock division.

Board and Management

Board

Each of the existing Energy Fuels directors will continue as directors of the Company following the Closing. Upon Closing, Mr. Michael Stirzaker, the Non-Executive Chair of Base Resources, was appointed to the Energy Fuels Board.

Management

The Company retained its existing members of the Energy Fuels' senior leadership team following Closing, as well as the existing members of Base Resources' senior leadership team, who are expected to continue managing the development and operation of the Toliara Project and the completion of mining and closure of Kwale Operations, and to enhance the Energy Fuels team's ongoing efforts to further its other mineral sands and rare earths interests.

Acquisition of RadTran LLC.

On August 16, 2024, the Company acquired RadTran LLC ("RadTran"), a private company specializing in the separation of critical radioisotopes, to further the Company's plans for development and production of medical isotopes used in cancer treatments. RadTran's expertise includes separation of radium-226 ("Ra-226") and radium-228 ("Ra-228") from uranium and thorium process streams. This strategic acquisition is expected to significantly enhance Energy Fuels' planned capabilities to address the global shortage of these essential isotopes used in emerging targeted alpha therapies ("TAT") for cancer treatment.

Since July 2021, Energy Fuels and RadTran have been working under a Strategic Alliance Agreement to evaluate the feasibility of recovering Ra-226 and Ra-228 from existing uranium process streams at the Mill. Recovered Ra-226 and Ra-228 would be made available to the pharmaceutical industry and others to enable the production of actinium-225 ("Ac-225"), lead-212 ("Pb-212") and potentially other leading medically attractive TAT isotopes. These isotopes are critical components in the development of targeted alpha therapies, which offer promising new treatments for various cancers. The global shortage of Ra-226 and Ra-228 currently presents itself as a significant barrier to the advancement and commercialization of these therapies.

Energy Fuels received regulatory approval and licensing in 2023 for the concentration of research and development ("R&D") quantities of Ra-226 at the Mill and is currently completing engineering on its R&D pilot facility for Ra-226 production. During 2024, Energy Fuels plans to set up the first stages of the pilot facility and expects to produce R&D quantities of Ra-226 for testing by end-users of the product. Upon successful production of R&D quantities of Ra-226, Energy Fuels plans to develop capabilities at the Mill for the commercial-scale production of Ra-226 and potentially Ra-228 in 2027-2028, conditional on completion of engineering design, securing sufficient offtake agreements for final radium production, and receipt of all required regulatory approvals. The Company's current R&D activities are being conducted using existing Mill facilities without the need for capital improvements of any significance. Capital development for future commercial production capabilities, upon successful production at the R&D level, would be expected to be supported by future offtake agreements for radium production.

In addition, as part of the Acquisition, Saleem Drera, PhD, President and CEO of RadTran, has joined Energy Fuels as Vice President of Radioisotopes, Radiological Systems, and Intellectual Property. In this role, Dr. Drera will lead Energy Fuels' efforts to integrate RadTran's proprietary technology, which includes a number of patents, pending patents, trade secrets and know-how relating to efficient separation of Ra-226 and Ra-228 from process streams, and drive innovation in the production of medical radioisotopes.

Under the Acquisition, the purchase price paid by Energy Fuels to the owners of RadTran consisted of (all dollar amounts in US$): (i) on closing, $1.5 million in cash, $1.5 million in Energy Fuels common shares ("Common Shares") and the grant of a 2% royalty on future revenues from the sale of produced radium, as well as certain other contractual commitments; and up to an additional $14 million in cash and Common Shares based on the satisfaction of a number of performance-based milestones, including achieving initial production, securing suitable offtake agreements to justify commercial production and reaching commercial production.

Competition

The HMS market is highly competitive. The industry is primarily concentrated in Australia, though South Africa, India and China are also major producers. Other countries with significant HMS deposits include the U.S., Brazil and Mozambique. The key industry participants include Iluka Resources, Rio Tinto and Tronox, which are among the largest producers of HMS in the world. Other major players include Kenmare Resources and our newly acquired subsidiary, Base Resources. The market for HMS products is driven by a wide range of factors, including global economic growth, industrial demand and technological innovation. In recent years, the market has faced a number of challenges in line with general economic conditions, including declining demand for certain products, increased competition from alternative materials and the general environmental concerns related to all mining and processing.

Despite these challenges, the HMS market is expected to continue to grow in coming years on the back of forecasted economic growth fueling demand in pigments, ceramics and other mature end-use applications. With this growth, the industry will also need to ensure that its sustainability objectives keep pace, including the need to continue to reduce environmental impacts and improve social and economic outcomes for local communities.

The availability of funds for the acquisition, exploration, evaluation, permitting and construction of HMS and monazite projects and the development of REE separation, metal and metal alloy making and magnet making is limited, and the Company may find it difficult to compete on an international scale with larger and more established and/or subsidized companies for capital. The Company's inability to continue exploration, advancement, the acquisition of new properties and the development of REE separation, metal and metal alloy making and magnet making, due to lack of funding, could have a material adverse effect on the Company's future operations and/or financial position.

However, the Company believes it has a competitive advantage over many of its peers in the U.S. domestic uranium space and in the world REE space, outside of China, to the extent it has diversified business opportunities, including its ability to produce uranium, its ability to recover REE Carbonate, along with uranium, from monazite sand ores and its ability to produce separated REEs oxides at the Mill, its ability to recover vanadium as market conditions may warrant, its existing HMS business, and its potential ability to recover certain radioisotopes for use in TAT medical treatments.

Government Regulation

The Company is subject to extensive laws and regulations which are overseen and enforced by multiple federal, state, regional and local authorities in the jurisdictions where it operates. These laws govern exploration, construction, extraction, recovery, processing, exports, various taxes, labor standards, occupational health and safety, waste disposal, protection and remediation of the environment, protection of endangered and protected species, toxic and hazardous substances and other matters. Uranium minerals and monazite exploration, extraction, recovery and processing are also subject to unique risks and liabilities associated with public perception, potential for impacts to the environment and disposal of waste products occurring as a result of such activities.

Compliance with these laws and regulations may impose substantial costs on the Company and may subject the Company to significant potential liabilities. Changes in these regulations or changes in regulatory attitudes or interpretations could require the Company to expend significant resources to comply with new laws or regulations, attitudes or interpretations relating thereto, or changes to current requirements and could have a material adverse effect on the Company's business operations. However, compliance with government regulations generally, including but not limited to environmental regulations, is an integral part of the Company's day-to-day business and impacts virtually all the Company's capital expenditure and operating decisions at its facilities, as the Company's facilities and operations must comply with this extensive array of environmental, health and safety laws and regulations. The expected costs of compliance with current laws and regulations are assumed by the Company in all its capital budgeting decisions, project analyses and cost and earnings projections.

As monazite is a uranium-bearing ore and is processed through the Mill for the recovery of uranium and REEs, all the regulations applicable to uranium recovery and processing at the Mill apply to the processing of monazite at the Mill, the production of RE Carbonate and the separation of REEs at the Mill.

Environmental Regulations

The Company's projects, exploration, activities, mining and processing operations are subject to the federal, state, regional and local environmental laws and regulations of the jurisdictions in which the Company's activities and facilities are located. For example, in the U.S., the Company is subject to a number of such laws and regulations including, without limitation: the Clean Air Act; the Clean Water Act; the Comprehensive Environmental Response, Compensation and Liability Act; the Atomic Energy Act; the Uranium Mill Tailings Radiation Control Act; the Emergency Planning and Community Right to Know Act; the Endangered Species Act; the Federal Land Policy and Management Act; the National Environmental Policy Act; the Resource Conservation and Recovery Act; and related state laws. The Company is subject to similar laws in other jurisdictions in which it operates. In all jurisdictions in which the Company operates, environmental licenses, permits and other regulatory approvals are required to engage in projects, exploration, mining and processing, and mine closure and reclamation activities. Regulatory approval of a detailed plan of operations and an environmental impact assessment (or equivalent) is required prior to initiating mining or processing activities or for any substantive change to previously approved plans. In all jurisdictions in which the Company operates, specific statutory and regulatory requirements must be met throughout the life of the mining or processing operations regarding air quality, water quality, fisheries, wildlife and biodiversity protection, archaeological and cultural resources, solid and hazardous waste management and disposal, the management and transportation of hazardous chemicals, toxic substances, noise, community right-to-know, land use and reclamation. Such laws and regulations, which may change over time, increase the costs of these activities and may prevent or delay the commencement or continuance of a given operation. Compliance with these laws and regulations has not had a material effect on our operations or financial condition to date, compared to industry norms.

Environmental and Social Efforts and Impacts

Both the newly acquired Kwale Project in Kenya and Toliara Project in Madagascar are located in regions of high conservation value and recognised for their biodiversity richness. They are also areas facing significant anthropogenic pressures, such as deforestation and wide scale land clearing. To support conservation and biodiversity efforts in these areas, a range of programs have been established, including a propagation research program to grow endemic plants, including rare and endangered species.

The Kwale Project's indigenous tree and plant nursery has achieved success since being established in 2012 and is now one of the largest of its kind in Africa, having propagated over 400,000 indigenous plants to date across 307 species. As Kwale approaches the end of its mine life, the use of indigenous grass seed and endemic trees from the nursery has provided the opportunity to restore mined out and disturbed areas to ecologically functioning habitats, which if linked to established forest patches, are expected to result in functioning ecosystems that can support Kenya's broader conservation and biodiversity efforts.

In Madagascar, an endemic indigenous tree and plant nursery has also been established and is in readiness for development of the Toliara Project. Despite limited opportunities to extend our seed collection efforts and collaborate with conservation organizations because of Toliara's suspension of activities, Base Resources has managed to propagate over 75,000 trees and plants from an estimated 206 species, including three of Madagascar's iconic baobab species endemic to the project region.

Employees

The Company and its subsidiaries currently have approximately 1,445 full-time employees. Our operations in the U.S. are in established mining areas where we have found sufficient available personnel for our business plans. While our operations in Kenya and Madagascar are in less developed mining jurisdictions, Base Resources has recruited or trained sufficient personnel to execute on its business plans.

Cybersecurity

The Company maintains a cyber risk management program designed to identify, assess, manage, mitigate and respond to cybersecurity threats. This program is integrated within the Company's enterprise risk management program. The Company regularly assesses the threat landscape and takes a holistic view of cybersecurity risks, with a layered cybersecurity strategy based on prevention, detection and mitigation. The Company has appointed an interdisciplinary team to oversee cybersecurity at the management level, as a part of which it reviews all enterprise-level cybersecurity risks at least annually, or more frequently as needed. Key cybersecurity risks, including cybersecurity threats associated with the use of third-party service providers, are incorporated into the Company's enterprise risk management process as needed. Additionally, the Company has implemented numerous information technology ("IT") policies and procedures concerning cybersecurity matters, which include policies that directly or indirectly relate to encryption standards, antivirus protection, remote access, multi-factor authentication, confidential information and the use of the internet, social media, email and wireless and personal devices for both Company business and personal matters while utilizing Company resources, among other relevant topics. These policies go through an internal review process on a periodic basis and are, if needed, updated and re-approved by the appropriate members of management. In addition, the Company's Cybersecurity Policy, which is maintained on a confidential basis to protect some of the more sensitive aspects of the Company's cybersecurity protections in place, is reviewed and approved annually by both the Audit Committee and the full Board of Directors. Employees receive training, as appropriate, on these policies.

The underlying controls of the cyber risk management program are based on recognized best practices and standards for cybersecurity and information technology, including the National Institute of Standards and Technology ("NIST"), the Center for Internet Security Benchmark ("CIS") and Service Organization Controls Types 1 and 2 of the American Institute of Certified Public Accountants ("SOC") in the Americas, and the International Organization for Standardization ("ISO")/International Electrotechnical Commission ("IEC") 27001 suite of guiding security and process principles in Australia, Kenya and Madagascar. The Company's evaluation and integration efforts across these two existing frameworks have demonstrated very similar information security and risk management elements and a strong alignment of current methods and technologies. The Company is continuing to integrate the two programs to ensure that its company-wide cybersecurity and risk management processes continue to adapt to the ever-changing cybersecurity landscape and to respond to emerging threats in a timely and effective manner in all aspects of the post-Base Resources acquisition business.

Land and Mineral Tenure

Kenya Land Tenure

In Kenya, mining rights are separate from ownership of land surface rights. Under the Kenyan Constitution, all minerals vest in and are held by the national government in trust for the people of Kenya. The Constitutional provisions relating to mineral resources are implemented by the Mining Act No. 12 of 2016 ("Mining Act").

A person shall not search for, prospect or mine any mineral, mineral deposit or tailings in Kenya unless that person has been granted a permit or license under the Mining Act. A mineral right may be granted to, among others, individuals or companies which are registered and established in Kenya that demonstrate the required technical capacity, expertise, experience and financial capacity.

A mineral right means a prospecting license, retention license, mining license, prospecting permit, mining permit or artisanal permit. Practically, of most relevance for large scale operations are the following:

1. Prospecting license: a license relating to large scale operations that authorizes the holder to exclusively carry out prospecting operations pursuant to an approved program for those prospecting operations, the procurement of local goods and services, a plan to employ and train Kenyan citizens and an approved environmental impact assessment report, social heritage impact assessment and environmental management plan. A prospecting license is granted for a maximum term of three years and the area must not exceed 1,500 contiguous blocks. It may be renewed twice for three years each, subject to the area of the license being reduced by not less than one-half each renewal.

2. Mining license: a license relating to large-scale operations that authorizes the holder to exclusively carry out mining operations pursuant to an approved program and a feasibility study demonstrating the feasibility of the project (including evidence of the financial and technical resources available to the applicant), a plan with respect to the employment and training of Kenyan citizens, a plan for the procurement of local goods and services, an applicable environmental impact assessment license, a social heritage impact assessment and environmental management plan, and a plan with respect to socially responsible investments for the local community. A mining license must not exceed 300 contiguous blocks and has a maximum term of 25 years, with a renewal period of 15 years.

Applications for a mineral right are to be considered, processed and determined on a first-come first-served basis. The holder of a mineral right must pay royalties to the State at the prescribed rate. Where a mineral right is granted for a large-scale mining operation, the State must acquire a 10% free carried interest. A holder of a mining license whose planned capital expenditure exceeds the prescribed limit must list at least 20% of its equity on a local stock exchange within three years of commencing production (subject to market conditions).

The Cabinet Secretary, on the recommendation of the Mineral Rights Board, may grant, deny or revoke a mineral right. Mineral rights applications are made to the Cabinet Secretary. Upon receipt, the Cabinet Secretary is required to give notice to the landowner or lawful occupier of the land where the mineral is located, the community and the relevant county Government and to publish notice of the pending application in a newspaper of wide circulation. A person or community may object to the grant of the license within 21 days (in the case of an application for a prospecting license) and within 42 days (in the case of a mining license). The Cabinet Secretary hears and determines any objection to an application through the Mineral Rights Board.

Prospecting and other mining rights may not be granted with respect to private land without the express consent of the registered owner, and such consent shall not be unreasonably withheld. Consent is deemed to be given where the owner of the private land has entered into a legally binding arrangement with the applicant or with the Government which allows for the conduct of prospecting or mining operations, or an agreement with the applicant providing for payment of adequate compensation.

Prospecting and other mining rights may not be granted with respect to community land without the consent of the authority obligated by the law relating to administration and management of community land, or the National Land Commission in relation to land that is unregistered. Consent is deemed to be given where the registered owners of community land have entered into a legally binding arrangement with the applicant or with the Government which allows for the conduct of prospecting or mining operations, or an agreement with the applicant providing for payment of adequate compensation.

The Cabinet Secretary may take steps under the law relating to compulsory acquisition to vest the land or area in the Government or on behalf of Government, where consent is unreasonably withheld or where the Cabinet Secretary considers that withholding of consent is contrary to the national interest.

A mineral right may not be assigned, transferred, mortgaged or traded without the consent of the Cabinet Secretary (not to be unreasonably withheld) on recommendation of the Mineral Rights Board.

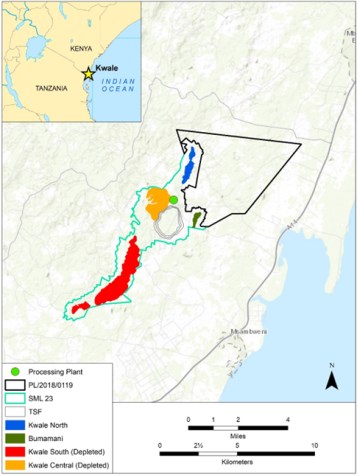

The Kwale Project operates pursuant to the terms of Special Mining Lease 23 ("SML 23"), issued by the Mines and Geological Department on July 6, 2004 under the former Mining Act CAP 306 (now repealed). SML 23 provides Base Titanium with the full and exclusive right, liberty and license to carry out mining operations for ilmenite, rutile and zircon within the defined area of SML 23. Base Titanium's rights under SML 23 were preserved under the transitional provisions of the Mining Act. SML 23 expires on June 30, 2025 and is not renewable. As Base Titanium (a wholly owned subsidiary of Base Resources) will require continued access to the SML 23 area following its expiry to complete its decommissioning and rehabilitation plan, Base Titanium is currently discussing with the Government of Kenya the most appropriate tenure instrument to be granted upon SML 23's expiration. With Kenya's National Environment Management Authority ("NEMA") recently approving Base Titanium's decommissioning and rehabilitation plan, Base Titanium does not anticipate any issues or delays obtaining appropriate replacement tenure from the Government of Kenya that will allow Base Titanium to complete the plan that has been endorsed by NEMA.

Australian Land Tenure

The Company has an indirect interest in mineral tenements in Australia through its ownership interest in Donald Project Pty Ltd and the Donald (Heavy Minerals Sands and Rare Earths) Project based in Victoria, Australia.

In Australia, mining rights are separated from the ownership of the land surface rights and are held by the state. Rights to access the land surface area are regulated both by legislation and by private access and compensation contracts with landholders. Mining rights are obtained by applying to the relevant state or territory government on a first-come, first-served basis, or in some instances, by a tender-based process. Mining rights may also be acquired by entering into a contractual arrangement with the existing holder of the mining right (by way of purchase or farm-in).

Each tenement delineates its area and duration. A holder must comply with the various terms and conditions of the permit, which include: the payment of annual rents, the payment of royalties once the mineral is extracted, meeting minimum annual expenditure obligations, agreeing to future mine rehabilitation plans and annual reporting requirements, as well as the provision of any environmental bond requirements.

Each state's mining legislation governs the grant of exploration licenses and mining leases, with some states also issuing a retention lease which allows an entity to maintain possession of a right to a mineral rich area pending improvement in economic conditions.

Once granted, tenements may be transferred or used as security. Tenements may be cancelled if the holder fails to meet the terms of their issue.

In the State of Victoria, Australia, the types of mineral license for heavy mineral sands and rare earths include exploration licenses, retention licenses and mining leases.

1. Exploration licenses: gives the license holder exclusive rights to explore for specific minerals within the specified license area. However, an exploration license is not an exclusive right to occupy the surface area. It is a right of access only for approved exploration activities, and subject to negotiated land compensation and access arrangements. Holders of an exploration license have a priority right to apply for a mining lease. Exploration licenses may be renewed for new terms, depending on the state legislation.

2. Retention license: is suitable where a mineral resource is identified but the resource is not yet commercially viable to mine but may become so in the future or the resource is required to support an existing mining operation in the future. It is a license between the exploration and mining stages, providing the license holder with tenure over the land as they transition toward obtaining a mining lease.

3. Mining lease: gives the holder the sole right to mine and explore for specific minerals and construct mining facilities related to the mining operation in the land covered by the lease. Mining leases may be subject to existing competing rights such as coal seam gas rights or infrastructure rights.

The Donald project holds retention license RL2002, which progresses to a mining lease. In order to advance this retention license to mining lease, the applicant must satisfy the relevant minister that the applicant is a fit and proper person to hold a license, intends to comply with relevant legislation, genuinely intends to do work, has an appropriate program of work (with a defined mineral resource), and is likely to be able to finance the proposed work and any rehabilitation.

Madagascar Land Tenure

Tenure for mining in Madagascar is governed by Law 2023-007 of July 27, 2023 relating to the New Mining Code (the "New Mining Code"), which has been in force since October 2, 2023 and replaced the former Mining Code, the Law 2005-021 of October 17, 2005 amending Law No. 99-022 of August 19, 1999 (the "Former Mining Code"). Like the Former Mining Code, the New Mining Code provides that all mineralization on the surface and in the subsoil, waters and seabed of the territory of Madagascar, are the property of the Malagasy State.

The New Mining Code covers all aspects of mining, including tenure. Under the New Mining Code, Madagascar is divided into squares of 625 meters a side. Grant of mining permits occurs on the basis of these squares and only one mining permit can exist per square.

Mining permits are administered by the Bureau de Cadastre Minier de Madagascar ("BCMM"), the Madagascar Mining Registry. The BCMM is in charge of the management of mining permits from the filing of the permit application to the expiration of the mining permits. It is a public entity under the supervision of the Ministry in charge of mines. The BCMM processes every mining permit application; however, grant of a mining permit requires issuance of an order duly signed by the Minister in charge of mines.

Like the Former Mining Code, there remain two key mining permits available under the New Mining Code:

1. Permis De Recherche (or Research Permit), which confers on its holder the exclusive right to carry out prospecting and research within the permit area. A Research Permit is valid for an initial period of five years, renewable twice for a further three years (a total of eleven years).

2. Permis D'Exploitation (or Exploitation Permit), which confers on its holder the exclusive right to undertake mining as well as prospecting and research within the permit area. An Exploitation Permit granted under the New Mining Code is valid for twenty-five (25) years and is renewable once for a period of fifteen (15) years. Further renewals (of fifteen (15) years) are possible provided certain conditions are met.

Both Research and Exploitation Permits are real property rights that can be bought, sold, pledged and mortgaged. An environmental authorization is required before exploration activities may be carried out on an area the subject of a Research Permit. This is issued by the Ministry in charge of Mines after completion of an Environmental Commitment Program. Research Permit holders are required to undertake an Environmental Impact Assessment and be issued an environmental permit before their Research Permit is able to be transformed into an Exploitation Permit. The environmental permit is issued by the National Office for Environment (Office National pour l'Environnement or "ONE").