UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of: December 2024

Commission file number: 001-38350

Lithium Americas (Argentina) Corp.

(Translation of Registrant's name into English)

900 West Hastings Street, Suite 300,

Vancouver, British Columbia,

Canada V6C 1E5

(Address of Principal Executive Office)

Indicate by check mark whether the registrant files or will file annual reports under cover:

Form 20-F [ ] Form 40-F [X]

INCORPORATION BY REFERENCE

Exhibits 99.2, 99.7, and 99.8 to this Form 6-K of Lithium Americas (Argentina) Corp. (the "Company") are hereby incorporated by reference as exhibits to the Registration Statement on Form F-10 (File No. 333-269649) of the Company, as amended or supplemented.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Lithium Americas (Argentina) Corp. |

| (Registrant) |

| |

| By: |

"Samuel Pigott" |

| Name: |

Samuel Pigott |

| Title: |

President and Chief Executive Officer |

Dated: December 11, 2024

EXHIBIT INDEX

NOTICE OF SPECIAL MEETING

NOTICE IS HEREBY GIVEN that the special meeting (the "Meeting") of the holders ("Shareholders") of common shares (the "Common Shares") of Lithium Americas (Argentina) Corp. (the "Corporation") will be held virtually at https://meetnow.global/MDAUKRK at 10:00 a.m. (Pacific Time) on January 17, 2025:

At the Meeting, Shareholders will be asked to consider the following matters:

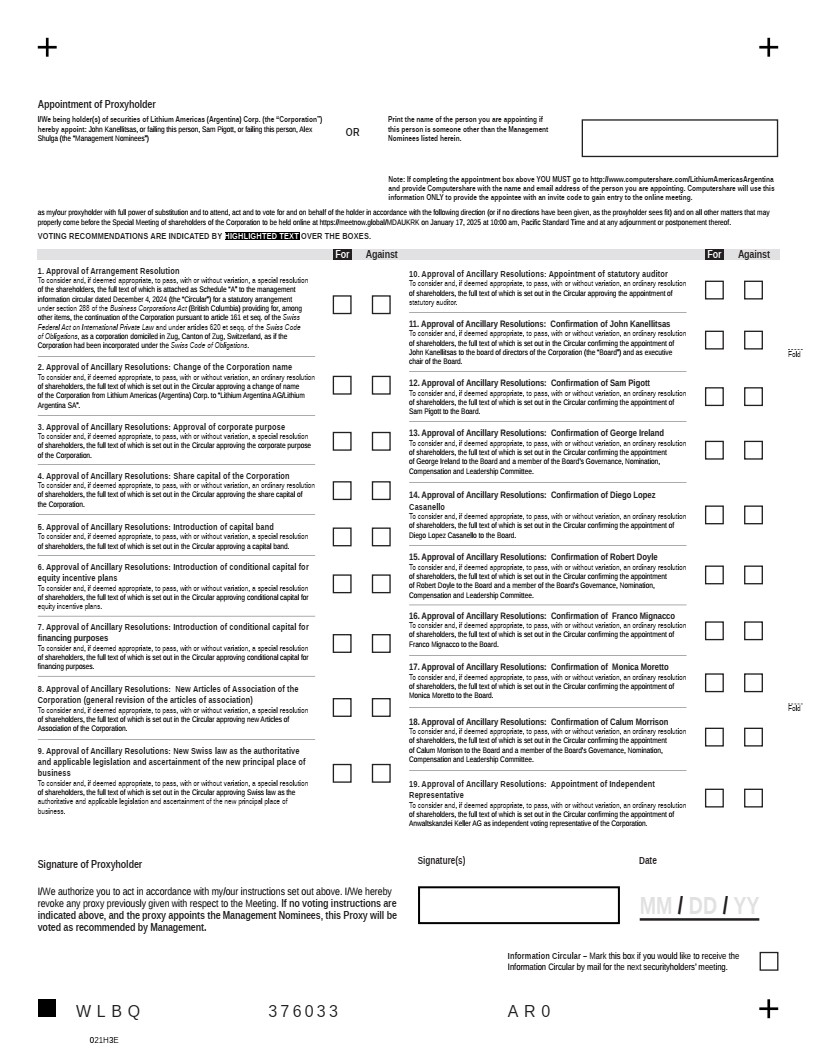

1. to consider and, if deemed appropriate, to pass, with or without variation, a special resolution of the Shareholders (the "Arrangement Resolution"), the full text of which is attached as Schedule "A" to the management information circular (the "Circular") for a statutory arrangement (the "Arrangement") under section 288 of the Business Corporations Act (British Columbia) providing for, among other items, the continuation of the Corporation pursuant to article 161 et seq. of the Swiss Federal Act on International Private Law and under articles 620 et seqq. of the Swiss Code of Obligations, as a corporation domiciled in Zug, Canton of Zug, Switzerland, as if the Corporation had been incorporated under the Swiss Code of Obligations (the "Continuation");

2. if the Arrangement is approved and as required by Swiss law, to pass the following ancillary resolutions (the "Ancillary Resolutions") to be implemented in connection with the Continuation, which shall be subject to receipt of the final order from the Supreme Court of British Columbia and the Arrangement having become effective and shall become effective as per the date of the filing of the application for the Continuation at the commercial register of the Canton of Zug:

(a) approval of the change of the Corporation name;

(b) approval of the corporate purpose of the Corporation;

(c) approval of the share capital of the Corporation;

(d) approval of the introduction of a capital band;

(e) approval of the introduction of conditional capital for equity incentive plans;

(f) approval of the introduction of conditional capital for financing purposes;

(g) approval of the new articles of association (general revision of the articles of association);

(h) approval of Swiss law as the authoritative and applicable legislation and ascertainment of the new principal place of business;

(i) appointment of the statutory auditor;

(j) confirmation of the members of the board of directors, confirmation of the chairman and confirmation of the members of the remuneration committee; and

(k) appointment of the independent representative; and

3. to transact such other business as may properly come before the Meeting or any adjournment thereof.

The specific details of these matters to be put before the Meeting are set forth in the Circular accompanying this notice of special meeting. The Board has approved the contents of the Circular and the distribution of the Circular to Shareholders. All Shareholders are reminded to review the Circular before voting. Registered Shareholders have a right of dissent in respect of the proposed Arrangement and to be paid the fair value of their Common Shares. The dissent rights are described in the accompanying Circular and are attached to the Circular as Schedule "F". Failure to strictly comply with the required procedures may result in the loss of any right of dissent.

Shareholders have the right to vote if they were a Shareholder of the Corporation at the close of business on December 3, 2024, the record date set by the Board for determining the Shareholders entitled to receive notice of and vote at the Meeting or any adjournment(s) or postponement(s) thereof.

In order for the Corporation to proceed with the Continuation, the Arrangement Resolution and Ancillary Resolutions (b), (d), (e), (f), (g) and (h) must be approved by two-thirds of the votes cast by Shareholders voting in person or by proxy at the Meeting and the remaining Ancillary Resolutions must be approved by a majority of the votes cast by Shareholders voting in person or by proxy at the Meeting. The Arrangement must also be approved by the Supreme Court of British Columbia and is subject to the approval of the Toronto Stock Exchange and New York Stock Exchange. The Continuation must be filed and registered with the Commercial Register of the Canton of Zug.

If you have any questions relating to the attached document or with the completion and delivery of your proxy, please contact Laurel Hill Advisory Group, the proxy solicitation agent, by telephone at 1-877-452-7184 (North American Toll Free) or 416-304-0211 (Collect Outside North America), or by email at assistance@laurelhill.com or in person at the 8th Floor, 100 University Avenue, Toronto, Ontario, M5J 2Y1.

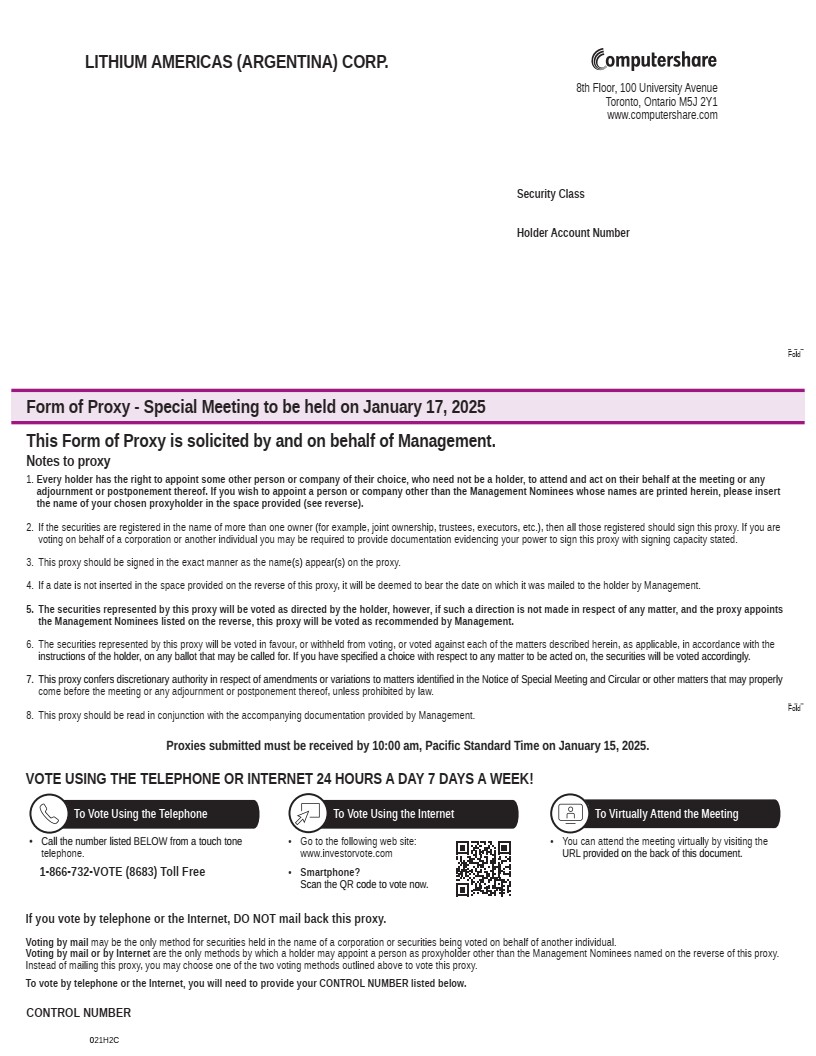

Shareholders who are unable to attend the virtual Meeting are encouraged to vote their proxy by mail, internet or telephone. Shareholders will need the control number contained in the accompanying form of proxy in order to vote. Further information on how to vote at the virtual Meeting can be found in the section "Voting Information - How to Vote" in the Circular. To be valid, a Shareholder's proxy must be received by the Corporation's transfer agent, Computershare Investor Services Inc., no later than 10:00 a.m. (Pacific Time) on January 15, 2025 or no later than 48 hours (excluding Saturdays, Sundays and statutory holidays) prior to the date on which the Meeting or any postponement or adjournment thereof is held.

Non-registered Shareholders who receive these materials through their broker or other intermediary are requested to follow the instructions for voting provided by their broker or intermediary, which may include the completion and delivery of a voting instruction form.

If you have any questions relating to the Meeting, please contact the Corporation by email at ir@lithium-argentina.com.

DATED at Vancouver, British Columbia this 4th day of December, 2024.

| |

On behalf of the Board of Directors

|

| |

|

| |

(signed) "John Kanellitsas"

|

| |

|

| |

Executive Chair

|

LITHIUM AMERICAS (ARGENTINA) CORP.

(FORMERLY LITHIUM AMERICAS CORP.)

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

to be held January 17, 2025

MANAGEMENT INFORMATION CIRCULAR

Dated: December 4, 2024

LETTER TO SHAREHOLDERS

Dear Fellow Lithium Americas (Argentina) Corp. Shareholders,

On behalf of the board of directors (the "Board") of Lithium Americas (Argentina) Corp. ("Lithium Argentina" or the "Corporation"), it is our pleasure to invite you to attend the special meeting of shareholders on January 17, 2025 at 10:00 a.m. (Pacific Time) to be held virtually at https://meetnow.global/MDAUKRK (the "Meeting").

As we announced on November 29, 2024, the Board approved a proposed continuation of the Corporation from the Province of British Columbia into the jurisdiction of Zug, Canton of Zug, Switzerland pursuant to article 161 et seq. of the Swiss Federal Act on International Private Law and under articles 620 et seqq. of the Swiss Code of Obligations, as if the Corporation had been incorporated under the Swiss Code of Obligations (the "Continuation").

Lithium Argentina has performed an extensive review of its business and corporate structure. Switzerland, was determined to be the best jurisdiction from a strategic, commercial and legal perspective. The move is expected to provide expanded financing flexibility and support the Corporation's current business and long-term growth plans through access to various markets, proximity to European customers and an attractive framework for existing shareholders and future investment.

If the Continuation is approved, Lithium Argentina's place of incorporation and its corporate headquarter will be in Zug, Switzerland. The operational headquarters of the Lithium Argentina group of companies will become Buenos Aires, Argentina. The Corporation plans to continue listing its common shares on the Toronto Stock Exchange and the New York Stock Exchange under the new symbol "LAR" which will continue to provide shareholders with the convenience of owning a North American listed stock and avoids any disruption related to changing the listing to other capital markets. By continuing to trade on North American markets, the Corporation will continue to be subject to the public company reporting requirements under Canadian and U.S. securities laws.

The Continuation is to be implemented pursuant to a plan of arrangement under the laws of the Province of British Columbia (the "Arrangement"). The accompanying management information circular (the "Circular") provides you with information for the purposes of voting on a special resolution (the "Arrangement Resolution"), in the form included in the accompanying Circular, to approve the Arrangement.

Assuming the Arrangement Resolution is approved, shareholders will also be asked to approve certain ancillary resolutions required under Swiss law (the "Ancillary Resolutions") to be implemented in connection with the Continuation including, but not limited to, a change of name of the Corporation to "Lithium Argentina AG/Lithium Argentina SA".

Your votes are important to us. In order for the Corporation to proceed with the Continuation, the Arrangement Resolution and Ancillary Resolutions (b), (d), (e), (f), (g) and (h) must be approved by two-thirds of the votes cast by shareholders voting in person or by proxy at the Meeting and the remaining Ancillary Resolutions must be approved by a majority of the votes cast by shareholders voting in person or by proxy at the Meeting. The Arrangement must also be approved by the Supreme Court of British Columbia and is subject to the approval of the Toronto Stock Exchange and New York Stock Exchange. The Continuation must be filed and registered with the Commercial Register of the Canton of Zug.

In view of the importance of the actions to be taken at the Meeting, we urge you to vote FOR the Arrangement Resolution and Ancillary Resolutions and promptly submit your proxy. You are urged to vote in this manner, regardless of the number of shares that you own or whether you will attend the Meeting. Returning the proxy does not deprive you of the right to attend the Meeting and vote your shares in person. To be valid, a shareholder's proxy must be received by the Corporation's transfer agent, Computershare Investor Services Inc., no later than 10:00 a.m. (Pacific Time) on January 15, 2025 or no later than 48 hours (excluding Saturdays, Sundays and statutory holidays) prior to the date on which the Meeting or any postponement or adjournment thereof is held. Proxies received after that time may be accepted by the Chair of the Meeting at such person's sole discretion. The Chair of the Meeting is under no obligation to accept late proxies.

HOW TO VOTE

|

VOTING

METHOD

|

NON-REGISTERED

SHAREHOLDERS

|

REGISTERED SHAREHOLDERS

|

|

Shares held with a broker, bank, or

other intermediary.

|

Shares held in own name and

represented by a physical certificate or

DRS.

|

|

|

www.proxyvote.com

|

www.investorvote.com

|

|

|

Call the toll-free number listed on your voting instruction form (VIF) and vote using the control number provided therein.

|

1-866-732-VOTE (8683)

|

|

|

Complete, date and sign the voting instruction form and return it in the enclosed postage paid envelope.

|

Complete, date and sign management's form of proxy and return it in the enclosed postage paid envelope to:

Computershare Investor Services Inc.

100 University Avenue, 8th Floor, North Tower, Toronto, Ontario, M5J 2Y1

|

If you have any questions relating to the completion and delivery of your proxy, please contact Laurel Hill Advisory Group, the Corporation's proxy solicitation agent, by telephone at 1-877-452-7184 (North American Toll Free) or 416-304-0211 (Collect Outside North America), or by email at assistance@laurelhill.com.

The Corporation's management supports the Continuation and joins with the Board in recommending that you to vote FOR the Arrangement Resolution and the Ancillary Resolutions.

We encourage you to read the Circular in advance to allow meaningful participation in the voting process.

On behalf of everyone at Lithium Argentina, we appreciate your ongoing support of our corporation.

Sincerely,

"John Kanellitsas"

|

"Sam Pigott"

|

| John Kanellitsas |

Sam Pigott |

| Executive Chair |

President and Chief Executive Officer |

NOTICE OF SPECIAL MEETING

NOTICE IS HEREBY GIVEN that the special meeting (the "Meeting") of the holders ("Shareholders") of common shares (the "Common Shares") of Lithium Americas (Argentina) Corp. (the "Corporation") will be held virtually at https://meetnow.global/MDAUKRK at 10:00 a.m. (Pacific Time) on January 17, 2025:

At the Meeting, Shareholders will be asked to consider the following matters:

1. to consider and, if deemed appropriate, to pass, with or without variation, a special resolution of the Shareholders (the "Arrangement Resolution"), the full text of which is attached as Schedule "A" to the management information circular (the "Circular") for a statutory arrangement (the "Arrangement") under section 288 of the Business Corporations Act (British Columbia) providing for, among other items, the continuation of the Corporation pursuant to article 161 et seq. of the Swiss Federal Act on International Private Law and under articles 620 et seqq. of the Swiss Code of Obligations, as a corporation domiciled in Zug, Canton of Zug, Switzerland, as if the Corporation had been incorporated under the Swiss Code of Obligations (the "Continuation");

2. if the Arrangement is approved and as required by Swiss law, to pass the following ancillary resolutions (the "Ancillary Resolutions") to be implemented in connection with the Continuation, which shall be subject to receipt of the final order from the Supreme Court of British Columbia and the Arrangement having become effective and shall become effective as per the date of the filing of the application for the Continuation at the commercial register of the Canton of Zug:

(a) approval of the change of the Corporation name;

(b) approval of the corporate purpose of the Corporation;

(c) approval of the share capital of the Corporation;

(d) approval of the introduction of a capital band;

(e) approval of the introduction of conditional capital for equity incentive plans;

(f) approval of the introduction of conditional capital for financing purposes;

(g) approval of the new articles of association (general revision of the articles of association);

(h) approval of Swiss law as the authoritative and applicable legislation and ascertainment of the new principal place of business;

(i) appointment of the statutory auditor;

(j) confirmation of the members of the board of directors, confirmation of the chairman and confirmation of the members of the remuneration committee; and

(k) appointment of the independent representative; and

3. to transact such other business as may properly come before the Meeting or any adjournment thereof.

The specific details of these matters to be put before the Meeting are set forth in the Circular accompanying this notice of special meeting. The Board has approved the contents of the Circular and the distribution of the Circular to Shareholders. All Shareholders are reminded to review the Circular before voting. Registered Shareholders have a right of dissent in respect of the proposed Arrangement and to be paid the fair value of their Common Shares. The dissent rights are described in the accompanying Circular and are attached to the Circular as Schedule "F". Failure to strictly comply with the required procedures may result in the loss of any right of dissent.

Shareholders have the right to vote if they were a Shareholder of the Corporation at the close of business on December 3, 2024, the record date set by the Board for determining the Shareholders entitled to receive notice of and vote at the Meeting or any adjournment(s) or postponement(s) thereof.

In order for the Corporation to proceed with the Continuation, the Arrangement Resolution and Ancillary Resolutions (b), (d), (e), (f), (g) and (h) must be approved by two-thirds of the votes cast by Shareholders voting in person or by proxy at the Meeting and the remaining Ancillary Resolutions must be approved by a majority of the votes cast by Shareholders voting in person or by proxy at the Meeting. The Arrangement must also be approved by the Supreme Court of British Columbia and is subject to the approval of the Toronto Stock Exchange and New York Stock Exchange. The Continuation must be filed and registered with the Commercial Register of the Canton of Zug.

If you have any questions relating to the attached document or with the completion and delivery of your proxy, please contact Laurel Hill Advisory Group, the proxy solicitation agent, by telephone at 1-877-452-7184 (North American Toll Free) or 416-304-0211 (Collect Outside North America), or by email at assistance@laurelhill.com or in person at the 8th Floor, 100 University Avenue, Toronto, Ontario, M5J 2Y1.

Shareholders who are unable to attend the virtual Meeting are encouraged to vote their proxy by mail, internet or telephone. Shareholders will need the control number contained in the accompanying form of proxy in order to vote. Further information on how to vote at the virtual Meeting can be found in the section "Voting Information - How to Vote" in the Circular. To be valid, a Shareholder's proxy must be received by the Corporation's transfer agent, Computershare Investor Services Inc., no later than 10:00 a.m. (Pacific Time) on January 15, 2025 or no later than 48 hours (excluding Saturdays, Sundays and statutory holidays) prior to the date on which the Meeting or any postponement or adjournment thereof is held.

Non-registered Shareholders who receive these materials through their broker or other intermediary are requested to follow the instructions for voting provided by their broker or intermediary, which may include the completion and delivery of a voting instruction form.

If you have any questions relating to the Meeting, please contact the Corporation by email at ir@lithium-argentina.com.

DATED at Vancouver, British Columbia this 4th day of December, 2024.

| |

On behalf of the Board of Directors

|

| |

|

| |

(signed) "John Kanellitsas"

|

| |

|

| |

Executive Chair

|

TABLE OF CONTENTS

GENERAL INFORMATION

DATE OF INFORMATION

All information in this management information circular (the "Circular") of Lithium Americas (Argentina) Corp. (the "Corporation" or "Lithium Argentina") is dated as of December 4, 2024 except as otherwise noted herein.

CURRENCY

This Circular contains references to United States dollars (US$) and Canadian dollars (C$ or $). All dollar amounts referenced, unless otherwise indicated, are expressed in Canadian dollars.

VOTING SECURITIES AND PRINCIPAL HOLDERS OF VOTING SECURITIES

Holders of Common Shares (as defined below) ("Shareholders") as of the close of business on December 3, 2024 (the "Record Date"), are entitled to vote at the Meeting (as defined below) as a Shareholder. Only Shareholders whose names have been entered in the register of Shareholders as of the close of business on the Record Date will be entitled to receive notice of the Meeting and shall have one vote per Common Share at the Meeting. As of the Record Date, the Corporation had 161,929,234 fully paid and non-assessable Common Shares issued and outstanding. The Corporation's authorized capital consists of an unlimited number of common shares without par value (each, a "Common Share").

To the knowledge of the directors and executive officers of the Corporation, no person or company, directly or indirectly, beneficially owns or exercises control or direction over, 10% or more of the Common Shares.

MEETING REPRESENTATIONS

No person is authorized to give any information or to make any representation concerning the Meeting other than those contained in this Circular and, if given or made, such information or representation should not be relied upon as having been authorized.

AUDITOR

The Corporation's auditor is PricewaterhouseCoopers LLP, Chartered Professional Accountants ("PwC"). PwC has served as the Corporation's auditor since August 2015.

See "Appointment of statutory auditor" below for further details on appointing PricewaterhouseCoopers AG as the Corporation's statutory auditor as part of the Ancillary Resolutions.

FORWARD-LOOKING STATEMENTS

This Circular (including the letter attached thereto) and documents referred to or incorporated by reference herein include and incorporate statements that are prospective in nature that constitute forward-looking information and/or forward-looking statements within the meaning of applicable securities laws (collectively, "forward-looking statements"). Forward-looking statements include, but are not limited to, statements concerning the Corporation's future objectives and strategies to achieve those objectives; the Continuation (as defined below), the timing thereof and the anticipated benefits and effects of the Continuation; expected continued listings on the TSX and NYSE (each, as defined below); and other business items at the Meeting, as well as other statements with respect to management's beliefs, outlook, plans, estimates and intentions, and similar statements concerning anticipated future events, results, circumstances, performance or expectations that are not historical facts. Forward-looking statements generally can be identified by the use of forward-looking terminology such as "outlook", "objective", "may", "will", "expect", "intend", "estimate", "anticipate", "believe", "should", "plans" or "continue", or similar expressions suggesting future outcomes or events.

Forward-looking statements reflect management's current beliefs, expectations and assumptions and are based on information currently available to management, management's historical experience, perception of trends and current business conditions, expected future developments and other factors which management considers appropriate. With respect to the forward-looking statements included in or incorporated by reference into this Circular, we have made certain assumptions with respect to, among other things, the Corporation's ability to obtain necessary Shareholder, stock exchange, governmental and Court (as defined below) approvals to proceed with the Continuation; that no unforeseen changes will occur in the legislative and operating framework for the business of the Corporation; that the Corporation will meet its future objectives and priorities; that the Corporation will have access to adequate capital to fund its future projects and plans; that the Corporation's future projects and plans will proceed as anticipated; as well as assumptions concerning general economic and industry growth rates, commodity prices, currency exchange and interest rates and competitive conditions.

Readers are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the future circumstances, outcomes or results anticipated or implied by such forward-looking statements will occur or that plans, intentions or expectations upon which the forward-looking statements are based will occur. By their nature, forward-looking statements involve known and unknown risks and uncertainties and other factors that could cause actual results to differ materially from those contemplated by such statements. Factors that could cause such differences include, but are not limited to: uncertainties in obtaining Shareholder, stock exchange, governmental and Court (as defined below) approvals to proceed with the Continuation; uncertainties with respect to the completion and timing of the Continuation, including the discretion of the Corporation to implement it or not; there being no assurance that the anticipated benefits of the Continuation will be realized; regulatory risks associated with the Continuation and the Corporation being governed under a different corporate legal regime post Continuation; potential tax liabilities associated with the Continuation; uncertainties with respect to the obtaining certain tax rulings; changes in the rights of Shareholders as a result of the Continuation; unforeseen events that could prevent, delay in or increase in cost of completing the Continuation; uncertainties inherent to feasibility studies and mineral resource and reserve estimates; global financial markets, general economic conditions, competitive business environments, and other factors that may negatively impact the Corporation's financial condition; the inability of the Corporation to secure sufficient additional financing to develop the Corporation's mineral projects; and all the other risk factors identified herein and in the Corporation's latest annual information form and other continuous disclosure filings available on SEDAR+ and EDGAR.

All forward-looking statements included in this Circular or incorporated by reference herein are qualified by these cautionary statements. The forward-looking statements are made as of the date of this Circular and, except as required by applicable law, the Corporation does not undertake any obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

Readers are cautioned that the actual results achieved will vary from the information provided herein and that such variations may be material. Consequently, there are no representations by the Corporation that actual results achieved will be the same in whole or in part as those set out in the forward-looking statements.

VOTING INFORMATION

PROXY SOLICITATION

The Corporation is providing this Circular to Shareholders to solicit proxies for use at the special meeting (the "Meeting") of Shareholders to be held virtually at 10:00 a.m. (Pacific Time) on January 17, 2025.

The Corporation's management is primarily soliciting proxies by mail (or alternative means), but may also contact Shareholders by telephone, email, internet or other means of communication. The Corporation will pay the costs of soliciting proxies. The Corporation may also pay reasonable costs incurred by intermediaries who are registered owners of Common Shares (such as brokers, dealers, other registrants under applicable securities laws, nominees and/or custodians) to deliver the notice package to beneficial owners of such Common Shares. The Corporation will provide, without cost to such persons, upon request to the Vice President, Legal and Corporate Secretary of the Corporation, additional copies of the foregoing documents required for this purpose. The cost of solicitation will be borne by the Corporation. In addition, the Corporation has retained the services of Laurel Hill Advisory Group ("Laurel Hill") to provide the following services in connection with the Meeting: review and analysis of the Circular, recommending corporate governance best practices and liaising with proxy advisory firms, as applicable, and assisting the Corporation in connection in its communication with Shareholders. In connection with these services, Laurel Hill will receive a fee of $45,000, plus out-of-pocket expenses. All costs of solicitation will be borne by the Corporation.

The Corporation may also utilize the Broadridge QuickVoteTM service to assist Shareholders with voting their Common Shares. Those Shareholders who have not objected to the Corporation knowing who they are (non-objecting beneficial owners or NOBOs) may be contacted by Laurel Hill to conveniently obtain a vote directly over the phone.

WHO CAN VOTE

Holders of Common Shares as of the close of business on the Record Date, December 3, 2024, are entitled to vote at the Meeting as a Shareholder. Only Shareholders whose names have been entered in the register of Shareholders as of the close of business on the Record Date will be entitled to receive notice of and to vote at the Meeting.

The Corporation's articles (the "Articles") provide that the quorum for the transaction of business at the Meeting is at least two (2) Shareholders who hold in aggregate at least 5% of the issued Common Shares entitled to vote at the Meeting.

The Arrangement Resolution (as defined below) and Ancillary Resolutions (as defined below) (b), (d), (e), (f), (g) and (h) must be approved by at least two-thirds of the votes cast by Shareholders present, whether virtually or by proxy, and entitled to vote at the Meeting and the remaining Ancillary Resolutions must be approved by a majority of the votes cast by Shareholders present, whether virtually or by proxy, and entitled to vote at the Meeting.

VOTER TYPES

Voters fall into two (2) categories:

-

Registered Shareholders, meaning Shareholders whose share certificate is in the name of the holder; or

-

Non-registered Shareholders, meaning beneficial Shareholders whose share certificate is registered in the name of an intermediary such as a brokerage firm, bank, trust company or clearing agency (for example, The Canadian Depository for Securities Limited commonly known as CDS, or Cede & Co.).

HOW TO VOTE

|

VOTING

METHOD

|

NON-REGISTERED

SHAREHOLDERS

|

REGISTERED SHAREHOLDERS

|

|

Shares held with a broker, bank, or

other intermediary.

|

Shares held in own name and

represented by a physical certificate or

DRS.

|

|

|

www.proxyvote.com

|

www.investorvote.com

|

|

|

Call the toll-free number listed on your voting instruction form (VIF) and vote using the control number provided therein.

|

1-866-732-VOTE (8683)

|

|

|

Complete, date and sign the voting instruction form and return it in the enclosed postage paid envelope.

|

Complete, date and sign management's form of proxy and return it in the enclosed postage paid envelope to:

Computershare Investor Services Inc.

100 University Avenue, 8th Floor, North

Tower, Toronto, Ontario, M5J 2Y1

|

Voting occurs in advance of the Meeting by voting a proxy, or at the Meeting by attending online. How a Shareholder votes will vary depending on whether they are a registered Shareholder or a non-registered Shareholder (beneficial Shareholder):

Registered Shareholders

Registered Shareholders may wish to vote by proxy whether or not they are able to attend the Meeting online. Voting by proxy means the Shareholder appoints another individual - either the Corporation's management or any other person of their choice - to attend the Meeting and vote the Shareholder's Common Shares based on their instructions to the person. This person does not need to be a Shareholder of the Corporation to be the Shareholder's proxy. The form of proxy enclosed with this Circular names senior management of the Corporation who will vote the Shareholder's Common Shares as proxy if they do not appoint another person.

Proxies voted by the Corporation's management will be voted FOR the Arrangement Resolution and FOR the Ancillary Resolutions.

To exercise the right of appointing a person other than the Corporation's management as a proxy, a registered Shareholder must fill in the name of the person to be designated proxy in the space provided on the proxy form and return their proxy. The Shareholder must also register their proxyholder with Computershare Investor Services Inc. ("Computershare") at http://www.computershare.com/LithiumAmericasArgentina no later than 10:00 a.m. (Pacific Time) on January 15, 2025. Any registered Shareholder exercising this right must register their non-management proxyholder with Computershare to allow that person to receive a control number from Computershare. Failure to register will result in the proxyholder not receiving a control number to attend, participate or vote at the Meeting. Without a control number, the proxyholder will only be able to attend the Meeting online as a guest. Guests are unable to vote or ask questions.

In the event that the ongoing postal strike in Canada continues, Registered Shareholders are encouraged to contact Laurel Hill to obtain and return their proxies in connection with the Meeting.

Registered Shareholders electing to submit a proxy may do so by:

(a) Internet voting - vote your proxy online at www.investorvote.com using the 15-digit or 16-digit control number located at the bottom of your proxy;

(b) Telephone - vote your proxy by telephone at 1-866-732-VOTE (8683) (North American Toll Free) or 1-312-588-4290 (Collect Outside North America);

(c) Fax - complete, sign, date and fax your proxy to Computershare at (416) 263-9524 or 1-866-249-7775; or

(d) Mail - complete, sign, date and mail your proxy to Computershare Investor Services Inc., Proxy Department at 8th Floor, 100 University Avenue, Toronto, Ontario, M5J 2Y1.

In all cases, the proxy must be received at least 48 hours (excluding Saturdays, Sundays and holidays) before the Meeting or the adjournment thereof at which the proxy is to be used. Proxies received after that time may be accepted by the Chair of the Meeting at such person's sole discretion. The Chair of the Meeting is under no obligation to accept late proxies.

Registered Shareholders may also choose to attend the Meeting virtually and vote their Common Shares at the Meeting through the online meeting platform, rather than voting by proxy. This means attending the Meeting virtually at the time set out on the notice of special meeting and voting at that time.

The Corporation recommends Shareholders consider voting by proxy even if they plan to attend the Meeting virtually, in case they encounter technical difficulties using the online meeting platform.

Registered Shareholders can attend the Meeting virtually by following these steps:

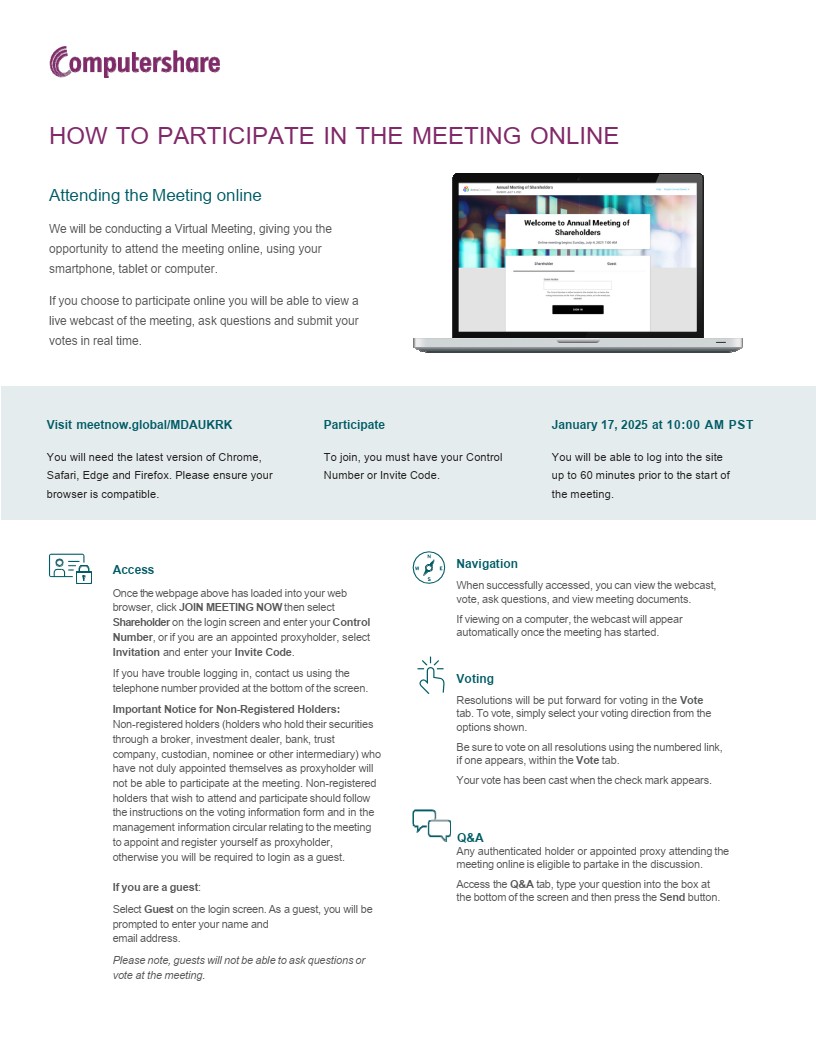

(a) At least a few minutes before the Meeting, go to the Computershare meeting platform website, https://meetnow.global/MDAUKRK

(b) Login by clicking on "I have a Control Number" and entering the 15-digit control number on the proxy form

A "Virtual Meeting User Guide" is available with the Meeting materials on SEDAR+ and EDGAR.

Non-Registered Shareholders

The Corporation sends Meeting materials to intermediaries for delivery to non-registered Shareholders who have not waived the right to receive them and pays for delivery costs to objecting non-registered Shareholders.

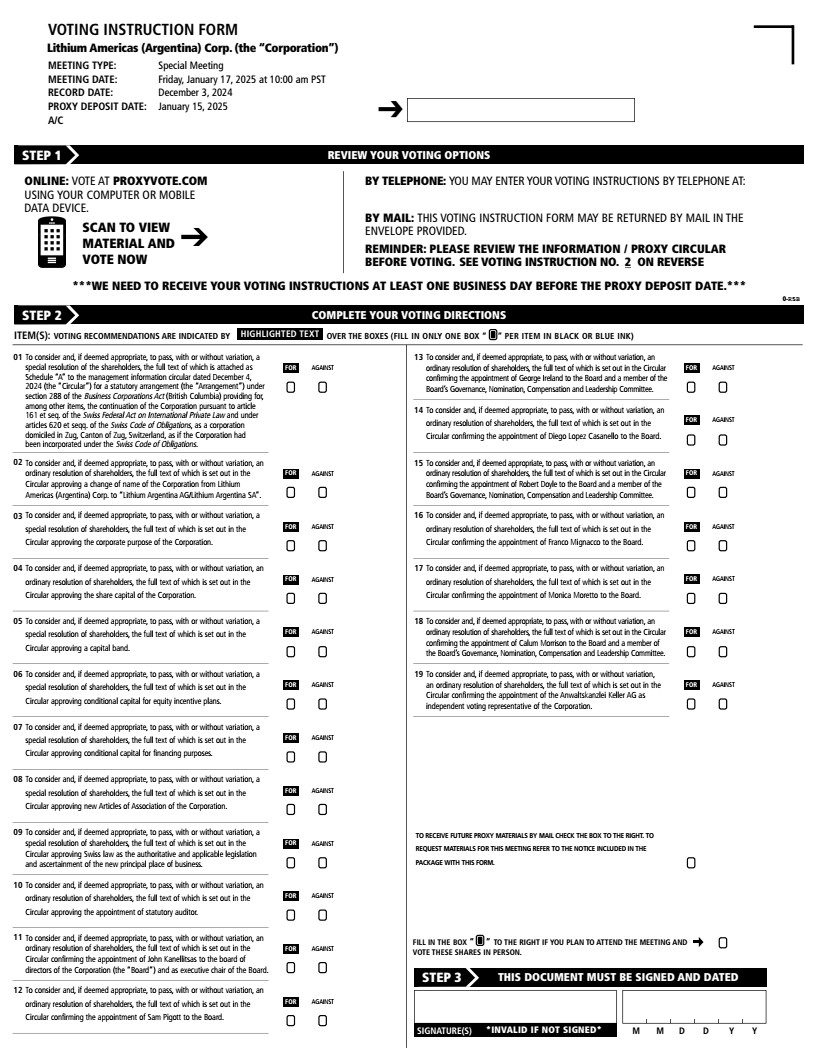

If a non-registered Shareholder has not waived the right to receive Meeting materials, their intermediary is required for the delivery of the Meeting materials. The materials will generally include a voting instruction form ("VIF") that will allow non-registered Shareholders to vote their Common Shares.

The VIF should be completed, signed and returned to the non-registered Shareholder's intermediary. Non-registered Shareholders can also vote by telephone or online per the VIF instructions.

In the event that the ongoing postal strike in Canada continues, non-registered Shareholders are encouraged to contact their intermediary to make arrangements for the return of their VIFs in connection with the Meeting.

Should a non-registered Shareholder who received one of the above forms wish to vote at the Meeting (or have another person attend and vote on behalf of the non-registered Shareholder), the non-registered Shareholder must: (1) follow the instructions on the VIF to indicate that they (or such other person) will virtually attend and vote at the Meeting, and (2) register their appointment at http://www.computershare.com/LithiumAmericasArgentina. If the non-registered Shareholder completes these two steps within the required timeframe, then, prior to the Meeting, Computershare will contact the non-registered Shareholder by email with login details to allow login to the live webcast and voting at the Meeting using the Computershare meeting platform, available online at https://meetnow.global/MDAUKRK. Non-registered Shareholders should carefully follow the instructions contained in the VIF of their intermediaries and contact them directly with any questions regarding the voting of Common Shares owned by them. A "Virtual Meeting User Guide" is available with the meeting materials on SEDAR+ and EDGAR.

Voting instructions must be received in sufficient time (at least one business day before the proxy deposit date) to allow for the VIF to be forwarded by the intermediary to Computershare no later than 10:00 a.m. (Pacific Time) on January 15, 2025.

To attend and vote at the Meeting, U.S. non-registered Shareholders must first obtain a valid legal proxy from their intermediary and then register in advance to attend the Meeting. The U.S. non-registered Shareholder must follow the instructions from their intermediary included with the notice package, or contact their intermediary to request a legal proxy form. After first obtaining a valid legal proxy from their intermediary, to then register to attend the Meeting, U.S. non-registered Shareholders must submit a copy of their valid legal proxy to Computershare. Requests for registration should be directed to Computershare by mail at 100 University Avenue, 8th Floor, Toronto, Ontario, M5J 2Y1, or by email at USLegalProxy@computershare.com.

Requests for registration must be labeled as "Legal Proxy" and be received no later than 10:00 a.m. (Pacific Time) on January 15, 2025. Non-registered Shareholders will receive a confirmation of registration by email after Computershare receives the registration materials. All U.S. non-registered Shareholders must also register their appointment at the following link: http://www.computershare.com/LithiumAmericasArgentina.

VOTING CHANGES

Shareholders can make changes to how they have voted their Common Shares by proxy in advance of the Meeting.

A registered Shareholder who has given a proxy may revoke it at any time not less than 48 hours (excluding Saturdays, Sundays and holidays) before the Meeting time or, if adjourned, any reconvened meeting time by sending written notice of revocation signed by the registered Shareholder of their authorized attorney (or for corporations who are registered Shareholders, by an authorized officer or attorney under the corporate seal) to the Corporation's head office at Lithium Americas (Argentina) Corp., Suite 300, 900 West Hastings Street, Vancouver, British Columbia, V6C 1E5, Attention: Vice President, Legal and Corporate Secretary. A proxy may also be revoked in any other manner permitted by law. A revocation of a proxy does not affect any matter on which a vote has been taken prior to the time of the revocation. A Shareholder attending the Meeting has the right to vote virtually and, if he or she does so, his or her proxy is nullified with respect to the matters such person votes upon and any subsequent matters thereafter to be voted upon at the Meeting.

A non-registered Shareholder wishing to change their vote must, at least seven (7) days before the Meeting, contact their intermediary to change their vote and follow their intermediary's instructions. A revocation of a proxy does not affect any matter on which a vote has been taken prior to the revocation.

EXERCISE OF DISCRETION

Common Shares represented by a properly executed proxy given in favour of the persons designated in the printed portion of the accompanying proxy at the Meeting will be voted or withheld from voting in accordance with the instructions contained therein on any ballot that may be called for and, if a Shareholder specifies a choice with respect to any matter to be acted upon at the Meeting, the Common Shares represented by the proxy shall be voted accordingly. Except with respect to broker non-votes described below where no choice is specified, the proxy will confer discretionary authority and will be voted in favour of each matter for which no choice has been specified.

Except with respect to broker non-votes described below, a proxy when properly completed and delivered and not revoked also confers discretionary authority upon the person appointed as proxy thereunder to vote with respect to any amendments or variations of matters identified in the notice of special meeting and with respect to other matters which may properly come before the Meeting. At the time of posting this Circular in accordance with Notice-and-Access (as defined below), management of the Corporation knows of no such amendments, variations or other matters to come before the Meeting. However, if any other matters which are not known to the management of the Corporation should properly come before the Meeting, the Common Shares represented by proxies given in favour of management nominees will be voted in accordance with the best judgement of the nominee.

Under rules of the New York Stock Exchange ("NYSE"), brokers and other intermediaries holding shares in street name for their customers are generally required to vote these shares in the manner directed by their customers. If their customers do not give any direction, brokers may vote the securities at their discretion on routine matters, but not on non-routine matters. We believe Ancillary Resolutions (a), (b), (c), (d), (i) and (k) are each routine matters and brokers governed by NYSE rules may vote the securities held in street name for their customers in relation to these items of business without direction from their customers. We believe the remaining matters to be voted on at the Meeting are all non-routine matters and brokers governed by NYSE rules may not vote the securities held in street name for their customers in relation to these items of business without direction from their customers. The absence of a vote on a non-routine matter is referred to as a broker non-vote. Any securities represented at the Meeting, but not voted (whether by abstention, broker non-vote or otherwise) will have no impact on any matter to be voted on at the Meeting.

TECHNICAL REQUIREMENTS

Participants attending the Meeting online to vote, should ensure they are entitled to vote and are connected to the internet at all times to allow them to vote on the resolutions during the polling periods for each matter put before the Meeting. Participants are responsible for ensuring they have internet connectivity at all times during the Meeting. Participants will also need to have the latest version of Chrome, Safari, Edge or Firefox. The platform does not support access using Internet Explorer. As internal network security protocols (such as firewalls or VPN connections) may block access to the Computershare meeting platform, participants should use a network that is not restricted by the security settings of any organization or that has disabled any VPN settings. Logging in at least an hour before the start of the Meeting is recommended to ensure participants are able to access the online platform. Participants who are having technical difficulties with access, can contact 1-888-724-2416 for technical assistance.

Non-registered Shareholders who wish to vote at the Meeting are responsible for appointing themselves or a third party as a proxyholder and submitting their proxy form with third party appointment details complete to Computershare and registering the third party appointment online with Computershare in advance of the Meeting at http://www.computershare.com/LithiumAmericasArgentina.

The Corporation believes that Shareholder participation at meetings is important, regardless of the online format for the Meeting. As such, the Meeting platform the Corporation has selected allows for registered Shareholders to ask written questions during the Meeting, and during any subsequent Corporation presentation. This facilitates a similar level of interaction as would be expected at an in-person meeting. Questions will be answered by the Chair of the Meeting, or by the Corporation's senior management in that person's discretion. The Corporation may choose not to answer any question that is asked of them if they determine the question is inappropriate for any reason.

NOTICE TO U.S. SHAREHOLDERS

This Circular is prepared in accordance with applicable disclosure requirements in Canada. As a "foreign private issuer" under the United States Securities Exchange Act of 1934, as amended (the "U.S. Exchange Act"), the Corporation is exempt from proxy solicitation requirements in the United States. This means that the content of this Circular may be different from proxy circulars prepared by domestic issuers in the United States who follow U.S. Exchange Act requirements.

NOTICE-AND-ACCESS

The Corporation is using the notice-and-access provisions ("Notice-and-Access") under National Instrument 54-101 - Communication with Beneficial Owners of Securities of a Reporting Issuer and National Instrument 51-102 - Continuous Disclosure Obligations to distribute the proxy-related materials (including this Circular). This allows the Corporation to post electronic versions of the Meeting materials on SEDAR+ at www.sedarplus.ca and on the Corporation's website at http://lithium-argentina.com/investor-relations/Special-Meeting instead of mailing paper copies to Shareholders. Notice-and-Access is more environmentally friendly, reduces the use of paper and certain physical delivery-related emissions, and is more cost effective for the Corporation, as it reduces print and mailing costs.

Shareholders still have the right to request paper copies of the Meeting materials posted online by the Corporation under Notice-and-Access if they choose. The Corporation will not use the "stratification" procedure for Notice-and-Access, where a paper copy of the Meeting materials is provided along with the notice package. Shareholders may ask the Corporation additional questions about Notice-and-Access by calling 778-653-8092 or emailing ir@lithium-argentina.com.

The Meeting materials are available under the Corporation's profile on SEDAR+ and on the Corporation's website at http://lithium-argentina.com/investor-relations/Special-Meeting. The Corporation will provide paper copies of the Meeting materials including proxy-related materials such as the Circular free of charge for a period of up to one year from the date the Circular is filed on SEDAR+.

For non-registered Shareholders with a 16-digit control number please call 1-877-907-7643 or visit www.proxyvote.com and enter the 16-digit control number located on your voting instruction form. For registered Shareholders, or those Shareholders without a 16-digit control number or who are dialing from outside North America, please call Toll Free Number: 1-844-916-0609 or Direct Dial: 1-303-562-9305 (English) or Toll Free Number: 1-844-973-0593 or Direct Dial: 1-303-562-9306 (French).

Shareholders who wish to receive a paper copy of the Meeting materials in advance of the Meeting should submit their request to the Corporation no later than January 7, 2025, to allow themselves sufficient time to receive and review the materials before the proxy submission deadline of 10:00 a.m. (Pacific Time) on January 15, 2025. The Corporation will send materials within three (3) business days of receiving a request if the request is received before the Meeting date, or within 10 days if received on or after the Meeting date. Shareholders should consider emailing their request to the Corporation and requesting an electronic copy of the materials to ensure they have sufficient time to review the materials, in which case requests should be sent to the Corporation by January 7, 2025.

Shareholders will be sent a paper copy of a notice package under Notice-and-Access by pre-paid mail or courier containing: (i) a notification about the Corporation's use of Notice-and-Access with instructions about how to access the proxy-related materials online, and (ii) for registered Shareholders, a form of proxy, or for non-registered Shareholders, a VIF.

ITEMS OF BUSINESS

At the Meeting, the following items of business will be conducted:

APPROVAL OF ARRANGEMENT RESOLUTION

Shareholders will be asked to consider and, if deemed appropriate, to pass, with or without variation, a special resolution of Shareholders (the "Arrangement Resolution"), the full text of which is attached as Schedule "A" to this Circular to approve a statutory arrangement (the "Arrangement") under section 288 of the Business Corporations Act (British Columbia) (the "BCBCA") providing for the continuation of the Corporation (the "Continuation") under the laws of Switzerland pursuant to article 161 et seq. of the Swiss Federal Act on International Private Law and under articles 620 et seqq. of the Swiss Code of Obligations, as a corporation domiciled in Zug, Canton of Zug, Switzerland, as if the Corporation had been incorporated under the Swiss Code of Obligations. The Arrangement Resolution will authorize the Board to make applicable applications under the BCBCA and pursuant to the Swiss Federal Act on International Private Law and the Swiss Code of Obligations to continue the Corporation from the Province of British Columbia into Zug, Canton of Zug, Switzerland and to adopt, subject to and upon the Continuation, the Articles of Association (as defined below), the full text of which is attached as Schedule "C" to this Circular, and as more fully described below.

The Arrangement Resolution must be approved by at least two-thirds of the votes cast by Shareholders present, whether virtually or by proxy, and entitled to vote at the Meeting. If Shareholder approval for the Continuation is not obtained, the Corporation will remain a British Columbia company, subject to the requirements of the BCBCA and the Corporation will not present the remaining Ancillary Resolutions for a vote at the Meeting. As well as the necessary Shareholder approval, the principal approval required will be that of the Supreme Court of British Columbia (the "Court"), which, under the BCBCA, must approve the Arrangement. It is expected that, assuming the requisite Shareholder approval is received at the Meeting, the hearing of the Court on the Arrangement will be held on January 21, 2025 at 9:45 a.m. (Pacific Time) at the Court house at 800 Smithe Street, Vancouver, British Columbia or at any other date and time as the Court may direct. The Notice of Hearing Petition for the Final Order (the "Notice of Hearing for Final Order") in connection with the Final Order is included as Schedule "E". The "Final Order" means the final order of the Court to be made pursuant to section 291 of the BCBCA in form and substance acceptable to the Corporation, acting reasonably, approving the Arrangement, as such order may be varied, amended or supplemented by the Court with the consent of the Corporation, acting reasonably, at any time prior to the effective date of the Arrangement or, if appealed, then, unless such appeal is withdrawn or denied, as affirmed or varied, amended or supplemented on appeal. The Court will be advised prior to the hearing for the Final Order that if the terms and conditions of the Arrangement are approved by the Court, such approval will be relied upon in seeking an exemption from the registration requirements of the U.S. Securities Act of 1933, as amended (the "U.S. Securities Act"), pursuant to Section 3(a)(10) thereof, with respect to the offer and sale of the securities to be issued or distributed pursuant to the Arrangement.

If the Arrangement Resolution and Ancillary Resolutions are approved at the Meeting and the Court grants the Final Order, the Corporation expects to effect the Continuation by January 23, 2025 or such other time as the Board approves and the Continuation is filed and registered with the Commercial Register of the Canton of Zug. Notwithstanding that the Arrangement Resolution and Ancillary Resolutions are passed or the Court grants the Final Order, the Board may amend the Plan of Arrangement and/or decide to delay or not proceed with the Arrangement and Continuation. There is therefore no guarantee that the Continuation will be effected. Registered Shareholders have certain Dissent Rights (as defined below) in respect of the Arrangement. See "Dissent Rights" below.

Background

The Corporation is currently incorporated under the BCBCA. The Corporation proposes to continue the Corporation from the Province of British Columbia to the jurisdiction of Zug, Canton of Zug, whereby the Corporation would become and be a Swiss share corporation domiciled in Zug, Canton of Zug, Switzerland, whose existence would be governed under articles 620 et seqq. of the Swiss Code of Obligations, as if the Corporation had been incorporated under the Swiss Code of Obligations.

The principal reasons for the Board's proposal to undertake the Continuation, as well as its reasons for recommending that the Shareholders approve the Arrangement Resolution, are discussed below under "Rationale for the Continuation".

Rationale for the Continuation

Lithium Argentina has performed an extensive review of its business and corporate structure. Switzerland, was determined to be the best jurisdiction from a strategic, commercial and legal perspective. The move is expected to provide expanded financing flexibility and support the Corporation's current business and long-term growth plans through access to various markets, proximity to European customers and an attractive framework for existing Shareholders and future investment.

If the Continuation is approved, Lithium Argentina's place of incorporation and its corporate headquarter will be in Zug, Switzerland. The operational headquarters of the Lithium Argentina group of companies will become Buenos Aires, Argentina.

If the Continuation is effected, Lithium Argentina would become and be a Swiss share corporation domiciled in Zug, Canton of Zug, Switzerland, whose existence would be governed under articles 620 et seqq. of the Swiss Code of Obligations, as if the Corporation had been incorporated under the Swiss Code of Obligations.

Upon completion of the Continuation, the Continued Shares (as defined below) will continue to be listed on the Toronto Stock Exchange (the "TSX") and NYSE under the new symbol "LAR", which will continue to provide Shareholders with the convenience of owning a North American listed stock and avoids any disruption related to changing the listing to other capital markets. Continued listing on the TSX and NYSE is subject to satisfying all conditions prescribed by the exchanges. Furthermore, the Continuation will not affect the Corporation's status as a reporting issuer under the securities legislation of any jurisdiction in Canada or as a reporting company in the United States under the U.S. Exchange Act, and the Corporation will remain subject to the requirements of such legislation.

Implementation of the Continuation

In order to effect the Continuation, the following steps will have to be taken:

1. The Corporation must obtain the approval of its Shareholders to the Continuation by approval of the Arrangement Resolution and Ancillary Resolutions;

2. The Final Order will have been obtained in form and substance satisfactory to the Corporation, and will not have been set aside or modified in a manner unacceptable to the Corporation, on appeal or otherwise;

3. All approvals, including from the TSX, the NYSE and applicable third parties, are obtained;

4. The Corporation must obtain authorization from the Registrar of Companies under section 308 of the BCBCA to continue the Corporation under the laws of Switzerland pursuant to article 161 et seq. of the Swiss Federal Act on International Private Law and under articles 620 et seqq. of the Swiss Code of Obligations, as a Swiss share corporation domiciled in Zug, Canton of Zug, Switzerland, as if the Corporation had been incorporated under the Swiss Code of Obligations;

5. The Corporation must obtain an excerpt of the commercial register of the Canton of Zug (the "Commercial Register") evidencing that the Corporation continues as a Swiss share corporation domiciled in Zug, Canton of Zug and is registered under the Swiss Code of Obligations (the "Evidence of Continuation"); and

6. File with the Registrar of Companies a copy of the Evidence of Continuation and request that the Registrar of Companies publish in the prescribed manner a notice that the Corporation has been continued into Zug, Canton of Zug, Switzerland as of the date of the Evidence of Continuation.

In addition, the Corporation has applied for certain tax rulings from Swiss tax authorities in connection with the Continuation with respect to, among other things, applicable corporate income tax, annual capital tax, withholding tax on dividends and on interest payments on the Notes (as defined below) and other matters. Although not a condition of the completion of the Continuation, the Corporation intends to obtain these tax rulings prior to effecting the Continuation.

The TSX has conditionally approved the Continuation and proposed name change subject to fulfilling all of the requirements of the TSX.

The Continuation will be deemed effective upon the issuance of the Evidence of Continuation by the Commercial Register.

The Board will be authorized to implement the Continuation process following the Meeting and to finalize and effect the Continuation at such time as the Board may determine, subject to any intervening events or to the Board becoming aware of any circumstances or effect of the Continuation which would render the Continuation not in the best interests of the Corporation. Notwithstanding that the Arrangement Resolution and Ancillary Resolutions are passed or the Court grants the Final Order, the Board may amend the Plan of Arrangement and/or decide to delay or not proceed with the Arrangement and Continuation. There is therefore no guarantee that the Continuation will be effected.

Vote Required and Recommendation of the Board

The Arrangement Resolution must be approved by at least two-thirds of the votes cast by Shareholders present, whether virtually or by proxy, and entitled to vote at the Meeting.

The Board has concluded that the Arrangement is fair to Shareholders and that it is in the best interest of the Corporation and, as such, has authorized submission of the Arrangement to Shareholders for approval and to the Court for the Final Order.

In coming to its conclusion and recommendations, the Board considered, among other factors, the following factors:

1. the purpose and benefits of the Arrangement and Continuation outlined herein; and

2. that the Shareholders that oppose the Arrangement may, subject to compliance with certain conditions, dissent with respect to the Arrangement Resolution and be entitled, in the event the Arrangement becomes effective, to be paid by the Corporation the fair value of the Common Shares held by such Dissenting Shareholder (as defined below) determined as of the close of business on the last business day before the day on which the Arrangement Resolution is approved by Shareholders at the Meeting. See "Dissent Rights" below.

The Board has unanimously approved the Arrangement and Continuation and recommends that Shareholders vote FOR the Arrangement Resolution.

Management also recommends a vote FOR the Arrangement Resolution. In the absence of instructions to the contrary, the accompanying proxy will be voted FOR the Arrangement Resolution.

Name Change

Under the Swiss Code of Obligations, all companies' names must indicate the legal form of the company. Following the effective time of the Continuation, the Corporation anticipates that its name will, subject to approval by Shareholders and the Commercial Register, be "Lithium Argentina AG/Lithium Argentina SA" rather than "Lithium Americas (Argentina) Corp." See "Approval of Ancillary Resolutions - Change of the Corporation name" below for further details on the name change as part of the Ancillary Resolutions.

Court Approval of the Arrangement

On December 4, 2024, the Corporation obtained the interim order of the Court issued under section 291 of the BCBCA providing, among other things, the calling and holding of the Meeting and other procedural matters, a copy of which is attached as Schedule "D" to this Circular, as such order may be varied, amended or supplemented by the Court with the consent of the Corporation, acting reasonably (the "Interim Order"). It is expected that, assuming the requisite Shareholder approval is received at the Meeting, the hearing of the Court on the Arrangement will be held on January 21, 2025 at 9:45 a.m. (Pacific Time) at the Court house at 800 Smithe Street, Vancouver, British Columbia or at any other date and time as the Court may direct. The Notice of Hearing for Final Order in connection with the Final Order is included as Schedule "E".

At the hearing, any Shareholder or other interested party who wishes to participate or be represented or present arguments or evidence must file and serve a response to petition no later than 4:00 p.m. (Pacific Time) on January 17, 2025 along with any other documents required, all as set out in the Interim Order and Notice of Hearing for Final Order, copies of which are attached as Schedule "D" and Schedule "E", respectively, to this Circular, and satisfy any other requirement of the Court.

The Court has broad discretion under the BCBCA when making orders in respect of arrangements, and the Court may approve the Arrangement as proposed or as amended in any manner the Court may direct, subject to compliance with such terms and conditions, if any, as the Court thinks appropriate. The Court, in hearing the application for the Final Order, will consider, among other things, the fairness of the terms and conditions of the Arrangement to Shareholders. The Court will be advised prior to the hearing for the Final Order that if the terms and conditions of the Arrangement are approved by the Court, such approval will be relied upon in seeking an exemption from the registration requirements of the U.S. Securities Act, pursuant to Section 3(a)(10) thereof, with respect to the offer and sale of the securities to be issued or distributed pursuant to the Arrangement.

For further information regarding the Court hearing and your rights in connection with the Court hearing, see the Notice of Hearing for Final Order attached as Schedule "E" to this Circular. The Notice of Hearing for Final Order constitutes notice of the Court hearing of the application for the Final Order and is your only notice of the Court hearing.

Principal Effects of the Continuation

Upon the issuance of the Evidence of Continuation, the Continuation of the Corporation to Zug, Canton of Zug, Switzerland would result in the Corporation (i) being a Swiss share corporation domiciled in Zug, Canton of Zug registered under the Swiss Code of Obligations (the "Continued Corporation"), (ii) ceasing to be a company governed by the BCBCA and (iii) changing its name to " Lithium Argentina AG/Lithium Argentina SA". The BCBCA will cease to apply to the Corporation and the Corporation will then become subject to applicable Swiss law and in particular the Swiss Code of Obligations. The Continuation will not create a new legal entity, affect the continuity of the Corporation, impact the Corporation's ownership of its properties or result in a change in its business. The persons serving on the Board prior to the Continuation will continue to constitute the Board upon the Continuation becoming effective.

Upon the Continuation being effective, Shareholders will continue to hold Common Shares with a nominal/par value per Common Share of US$0.01 of the Continued Corporation (each, a "Continued Share") with no further action by the Shareholders. Each Continued Share will be in essence the same as, and a continuation of, a Common Share of the Corporation that was issued and outstanding immediately before the Continuation being effective. The number of Common Shares a Shareholder owns (or has rights to acquire) and the percentage ownership such Shareholder has of the Corporation immediately prior to the Continuation will not change as a result of the Continuation. Each pre-Continuation Shareholder will hold that number of Continued Shares in the Continued Corporation that is equal to the number of Common Shares such Shareholder holds in the Corporation immediately prior to the effective time of the Continuation.

Other securities of the Corporation and other rights entitling the holder(s) thereof to acquire securities of the Corporation will automatically become and be rights to acquire an equal number of Continued Shares or other securities, as the case may be. See "Disclosure Regarding the Effect of the Continuation on the Notes".

Upon completion of the Continuation, the Continued Shares will continue to be listed on the TSX and NYSE under the new symbol "LAR" and the transfer agent and registrar for the Continued Shares would continue to be Computershare Investor Services Inc. The TSX has conditionally approved the Continuation and proposed name change subject to fulfilling all of the requirements of the TSX.

For a summary of the principal Canadian, U.S. federal income tax and Swiss tax considerations to Shareholders relative to the Continuation, see the discussion in this Circular under "Certain Canadian Federal Income Tax Consequences", "Certain U.S. Federal Income Tax Consequences" and "Certain Swiss Tax Consequences".

The BCBCA provides that a company must not apply to be continued into another jurisdiction unless the laws of that other jurisdiction provide, in effect, that, after continuation:

(a) the property, rights and interests of the company continue to be the property, rights and interests of the continued corporation;

(b) the continued corporation continues to be liable for the obligations of the company;

(c) an existing cause of action, claim or liability to prosecution is unaffected;

(d) a legal proceeding being prosecuted or pending by or against the company may be prosecuted or its prosecution may be continued, as the case may be, by or against the continued corporation; and

(e) a conviction against, or a ruling, order or judgment in favour of or against, the company may be enforced by or against the continued corporation.

The Corporation is of the view that each such requirement is met in connection with the Continuation. Furthermore, the Continuation will not affect the Corporation's status as a reporting issuer under the securities legislation of any jurisdiction in Canada or as a reporting company in the United States under the U.S. Exchange Act, and the Corporation will remain subject to the requirements of such legislation.

Disclosure Regarding the Effect of the Continuation on the Notes

At the effective time of the Continuation, the Continued Corporation will continue to be liable for all of the Corporation's obligations under the indenture (the "Indenture") dated as of December 6, 2021, as amended by the first supplemental indenture dated October 3, 2023, between the Corporation and Computershare Trust Company, N.A. (the "Trustee") governing the 1.75% Convertible Senior Notes due 2027 (the "Notes"). At and after the effective time of the Continuation, the right to convert each US$1,000 principal amount of Notes into an amount of Common Shares described in the Indenture shall be amended to refer to a right to convert such principal amount of Notes into Continued Shares at a conversion rate equal to the conversion rate then in effect immediately prior to the Continuation.

Following the effective time of the Continuation, the Continued Corporation and the Trustee shall enter into a supplemental indenture to provide that, among other things, the Notes will convert into Continued Shares all in accordance with the terms and conditions of the Indenture.

Pursuant to the Indenture, the holders of Notes, at their election, will be permitted to surrender Notes for conversion (i) into Common Shares during the approximate 30-trading day period prior to the completion of the Continuation and (ii) into Continued Shares during the period from and after the completion of the Continuation until approximately the 35th trading day after the completion of the Continuation.

The Conversion Rate (as defined in the Indenture) for the Notes is currently 52.6019 Common Shares per US$1,000 principal amount of Notes (approximately US$19.01 per Common Share). Pursuant to the terms and conditions of the Indenture, the Corporation does not expect the Conversion Rate for the Notes to be adjusted as a result of the Continuation.

Holders are not required to convert their Notes in connection with the Continuation. Holders electing to convert their Notes prior to the completion of the Continuation as described above will participate in the Continuation as Shareholders. Holders that do not elect to convert their Notes prior to the completion of the Continuation will be entitled to convert their Notes after the completion of the Continuation as described above.

Proposed Timetable for the Arrangement and Continuation

The anticipated timetable for completion of the Arrangement and Continuation and the key dates proposed are as follows:

Meeting: January 17, 2025

Final Order: January 21, 2025

Effective date of the Arrangement and Continuation: Targeted by January 23, 2025

Notice of the actual effective date of the Arrangement and Continuation will be made through one or more news releases issued by the Corporation. The Board will be authorized to implement the Continuation process following the Meeting and to finalize and effect the Continuation at such time as the Board may determine in its sole discretion, subject to any intervening events or to the Board becoming aware of any circumstances or effect of the Continuation which would render the Continuation not in the best interests of the Corporation. Notwithstanding that the Arrangement Resolution and Ancillary Resolutions are passed or the Court grants the Final Order, the Board may amend the Plan of Arrangement and/or decide to delay or not proceed with the Arrangement and Continuation. There is therefore no guarantee that the Continuation will be effected.

Articles of Association

Upon the Commercial Register's approval and registration of the Continuation application, the articles of association (the "Articles of Association"), which amend and restate the Corporation's current constating documents in accordance with the requirements of the Swiss Code of Obligations, will become the official articles of association of the Continued Corporation.

The Articles of Association will be substantially in the form set out in Schedule "C" of this Circular. Accordingly, approval of the Arrangement Resolution and Ancillary Resolution with respect to the adoption of the Articles of Association by Shareholders at the Meeting will have the effect of approving an amendment to the Corporation's constating documents, subject to and upon Continuation, so that the Corporation's charter documents on and from Continuation would comply with the Swiss Code of Obligations. See "Summary Comparison of Material Shareholder Rights under British Columbia Law and Swiss Law" and "Approval of Ancillary Resolutions - New Articles of Association of the Corporation (general revision of the articles of association)" below for further details on the approval of the Articles of Association as part of the Ancillary Resolutions.

Description of Continued Shares

Immediately after the Continuation, the Continued Corporation will continue to have one class of shares outstanding, being the Continued Shares. The Continued Shares will have a nominal/par value per share of US$0.01. See "Summary Comparison of Material Shareholder Rights under British Columbia Law and Swiss Law" below for further details on rights attached to the Continued Shares, including the right to vote at Shareholders' meetings, the entitlement to receive a share of the profit and liquidation proceeds and a subscription right in the event of the issuance of new shares. The Continued Shares will not be convertible into shares of any other class or series or subject to redemption either by the Continued Corporation or by the holder of the Continued Shares.

The capital structure of the Continued Corporation will consist of a share capital of an amount to be defined at the date of the Meeting divided into the issued and outstanding Continued Shares. The precise number of Continued Shares will not be known until immediately prior to approval of the Continuation, such number to be approved at the Meeting. Assuming that the number of Common Shares issued and outstanding on the day of the Meeting is approximately 161,929,234 (the number of Common Shares issued and outstanding as of the Record Date), the Continued Corporation's (nominal) share capital upon completion of the Continuation would be approximately US$1,619,292.34 consisting of 161,929,234 Continued Shares. See "Capitalization" below for further details on the capitalization.

Following the Continuation, the Board may not create any new classes of shares with privileged voting rights unless it receives approval from a special majority of two-thirds of the voting rights represented at a Shareholders' meeting as well as a majority of the aggregate nominal/par value of the shares represented at such meeting, in either case whether in person or by proxy (together, such qualified majority, an "Important Resolution"). Further, following the Continuation, the Board may not create any new classes of shares with special rights or restrictions (other than rights which require an Important Resolution) unless the Shareholders pass a special resolution approved by at least two-thirds of the represented share votes.

See "Share Capital of the Corporation" below for further details on the approval of the share capital of the Continued Corporation in connection with the Continuation as part of the Ancillary Resolutions.

The Continued Corporation has not imposed any restrictions applicable to the transfer of the Continued Shares, subject to Article 7(2) of the Articles of Association with respect to Continued Shares issued in the form of intermediated securities, in which case any transfer of the Continued Shares is effected by a corresponding entry in the securities deposit account of a bank or a depository institution; no Continued Shares in the form of intermediated securities or security interest in any such intermediated securities can be transferred by way of assignment. If uncertificated Continued Shares (not in the form of intermediated securities) are transferred by way of assignment, such assignment must be notified to the Continued Corporation to be valid. Any person who acquires Continued Shares may submit a request to the Continued Corporation to be entered into the share register as a shareholder with voting rights, provided such persons expressly declare that they have acquired the shares in their own name and for their own account, that there is no agreement on the redemption of the shares and that they bear the economic risk associated with the Continued Shares. The Board may record nominees who hold Continued Shares in their own name, but for the account of third parties, as shareholders of record with voting rights in the share register of the Continued Corporation. Beneficial owners of Continued Shares who hold shares through a nominee exercise the shareholders' rights through the intermediation of such nominee. The share register will reflect only record owners, usufructuaries and nominees of Continued Shares. Swiss law does not recognize fractional share interests.

Summary Comparison of Material Shareholder Rights under British Columbia Law and Swiss Law

The rights of Shareholders are currently governed by the BCBCA and the Corporation's constating documents, namely its notice of articles and Articles. Following the issuance of the Evidence of Continuation, the rights of Shareholders of the Continued Corporation would be governed by the Continued Corporation's Articles of Association as well as by the applicable laws and regulations of Switzerland (including, but not limited to, the Swiss Code of Obligations and the Swiss Merger Act).