false

0000890447

0000890447

2024-09-19

2024-09-19

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange

Act of 1934

Date of Report (Date of Earliest Event Reported): September

19, 2024

VERTEX ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Nevada |

|

001-11476 |

|

94-3439569 |

(State or other jurisdiction of

incorporation) |

|

(Commission File Number) |

|

(IRS Employer

Identification No.) |

|

1331 Gemini Street

Suite 250

Houston, Texas |

|

77058 |

| (Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area

code: (866) 660-8156

Check the appropriate box below if the Form 8-K filing

is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Common Stock, $0.001 Par Value Per Share

|

|

VTNR |

|

The NASDAQ

Stock Market LLC

(Nasdaq Capital Market) |

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the

Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by

check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ☐

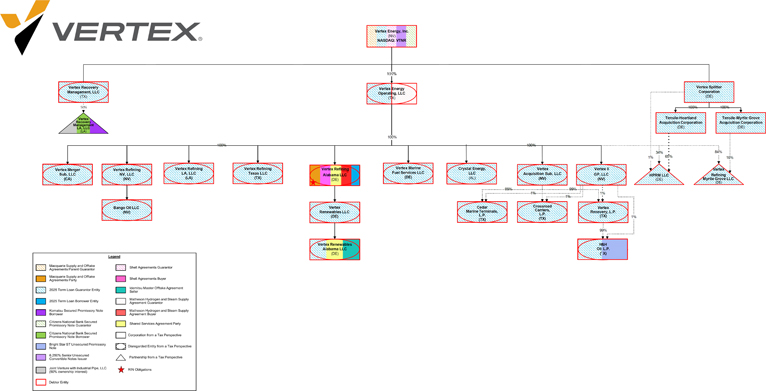

Item 1.01 Entry into a Material Definitive Agreement.

Restructuring Support Agreement

On September 24, 2024, Vertex

Energy, Inc. (the “Company”) and certain of the Company’s subsidiaries (collectively with the Company, the “Company

Parties”) entered into a Restructuring Support Agreement (including all of the exhibits and attachments thereto, the “Restructuring

Support Agreement”), with parties that hold 100% of the claims under the Loan and Security Agreement, dated April 1, 2022 (as

amended from time to time, the “Term Loan”), by and between Vertex Refining Alabama LLC, as borrower, the Company,

as parent and guarantor, Cantor Fitzgerald Securities, as agent, and the lenders party thereto (the “Term Loan Lenders”

or the “Consenting Stakeholders”). The Restructuring Support Agreement contemplates agreed-upon terms for a financial

restructuring of the Company Parties’ capital structure (the “Restructuring”) to be implemented pursuant

to a chapter 11 plan filed by the Company Parties in cases (the “Chapter 11 Cases”) under chapter 11 of title 11 (“Chapter

11”) of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the

Southern District of Texas (the “Bankruptcy Court”). Pursuant to the Restructuring Support Agreement, the Consenting

Stakeholders have agreed, subject to certain terms and conditions, to support the Plan (as defined below).

Restructuring Transactions

The Restructuring Support Agreement

contemplates agreed-upon terms for a financial restructuring of the Company Parties’ capital structure (the “Restructuring”).

Pursuant to the Restructuring Support Agreement, the Debtors expect to effectuate a chapter 11 plan (the “Plan”) through

either (a) a standalone recapitalization of the Company’s balance sheet; or (b) a sale of all, substantially all, or any portion

of the Debtors’ assets through one or more sales (as applicable, a “Recapitalization Transaction”).

Pursuant to the Restructuring

Support Agreement, the Consenting Stakeholders have agreed, subject to certain terms and conditions, to support the Plan, among other

things.

The transactions contemplated

by the Restructuring Support Agreement and the term sheets attached thereto (such transactions, collectively, the “Restructuring

Transactions”) will be consummated pursuant to the Recapitalization Transaction, unless the Company Parties, with the prior

written consent of holders holding at least 80% of the aggregate outstanding principal amount of the Term Loan Claims (as defined below)

(such holders, the “Required Consenting Term Loan Lenders”) determine that pursuit of the highest or otherwise best

asset sale proposal (or proposals), which may include a credit bid submitted by certain debtor-in-possession financing lenders (“DIP

Lenders”) and/or Term Loan Lenders (a “Credit Bid”), is in the best interests of the Company Parties and

their stakeholders (the “Successful Bid”).

If the Company Parties

select a Successful Bid and such Successful Bid is approved by the Bankruptcy Court pursuant to an order, prior to the consummation

of the asset sale, the Company Parties will establish and fund one or more reserves from cash on hand of the Company Parties and

undrawn amounts under the DIP Facility (as defined below), in an amount determined in the Company Parties’ reasonable

discretion and consented to by the Required Consenting Term Loan Lenders, sufficient to (a) fund the estimated fees, costs, and

expenses necessary to fully administer and wind down the estates of the Company Parties, including the fees, costs, and expenses of

the plan administrator selected by the Required Consenting Term Loan Lenders to wind down the Company Parties’ estates (the

“Plan Administrator”), and (b) pay in full in cash all Claims required to be paid under the Bankruptcy Code and

Plan in order for the Plan Effective Date to occur or otherwise be assumed or required to be paid under the terms of the Plan, in

each case to the extent not liquidated and paid in full in cash on the Plan Effective Date (collectively, the “Wind Down

Reserve”); provided, that (x) in no event shall the Wind Down Reserve constitute an increase to the DIP Facility at

any time without the express consent of all of the DIP Lenders and (y) any new money term loans provided for the Wind Down

Reserve shall be funded only in accordance with certain conditions, including, but not limited to, the absence of a default or event

of default under the DIP Facility. Absent such an event of default, the Company Parties will be authorized to maintain the Wind Down

Reserve in an amount and for such time as is necessary, each as determined by the Plan Administrator, to fully reconcile, liquidate,

and pay in full in cash all applicable fees, costs, expenses, claims, and other obligations before distributing any excess

distributable cash to holders of debtor-in-possession financing claims or any other claims and equity interests in accordance with

the priorities and treatment described in the Restructuring Support Agreement.

The Restructuring Support

Agreement also contemplates the cancellation of all existing equity interests of the Company, including the Company’s common stock,

par value $0.001 per share (the “Common Stock”) and any interests arising from the Common Stock, including any options

or warrants, at any time on or after the Plan Effective Date.

DIP Facility

To fund the administration

of the Chapter 11 Cases and the implementation of the Restructuring Transactions, all of the DIP Lenders will provide a $280 million senior

secured super-priority debtor-in-possession loan and security agreement (such agreement, the “DIP Loan Agreement”,

and the financing facility thereunder, the “DIP Facility”), consisting of (a) an $80 million new money term loan

facility and (b) a “roll up” loan facility, whereby $200 million of Term Loan Claims will be converted on a cashless,

dollar-for-dollar basis into DIP Facility loans on the terms and conditions set forth in the DIP Loan Agreement which provides for, among

other things, granting a security interest in all assets of the Company Parties as collateral, and provides for a guarantee by the Company

Parties. The DIP Facility will be used by the Company in accordance with the budget agreed upon between the Company Parties and the Required

DIP Lenders (as defined in the Restructuring Support Agreement).

The Company Parties will

seek approval of the DIP Facility as is consistent with the DIP Loan Agreement, and the transactions contemplated by such DIP Loan Agreement

are subject to approval by the Bankruptcy Court. In addition, the DIP Lenders’ obligations to provide the DIP Facility are subject

to various conditions customary for debtor-in-possession financings of this type.

Additional Terms of the Restructuring

Support Agreement

In

accordance with the Restructuring Support Agreement, the Consenting Stakeholders agreed, among other things, to: (a) support the Restructuring

Transactions as contemplated by, and within the timeframes outlined in, the Restructuring Support Agreement and the definitive documents

governing the Restructuring Transactions; (b) not take action, in respect of each Consenting Stakeholder’s Company Claims/Equity

Interests (as defined in the Restructuring Support Agreement), directly or indirectly, to interfere with acceptance, implementation, or

consummation of the Restructuring Transactions; and (c) vote each of each Consenting Stakeholder’s Company Claims/Equity Interests

owned, held, or otherwise controlled by such Consenting Stakeholder and exercise any powers or rights available to it, in each case, in

favor of any matter requiring approval to the extent necessary to implement the Restructuring Transactions.

In

accordance with the Restructuring Support Agreement, the Company Parties agreed, among other things, to: (a) support and take all steps

reasonably necessary and desirable to consummate the Restructuring Transactions in accordance with the Restructuring Support Agreement;

(b) use commercially reasonable efforts to obtain any and all required regulatory and/or third-party approvals for the Restructuring Transactions;

(c) negotiate in good faith and use commercially reasonable efforts to execute and deliver certain required documents and agreements to

effectuate and consummate the Restructuring Transactions as contemplated by the Restructuring Support Agreement; and (d) not, directly

or indirectly, object to, delay, impede, or take any other action to interfere with acceptance, implementation, or consummation of the

Restructuring Transactions.

The Restructuring

Support Agreement may be terminated upon the occurrence of certain events set forth therein, including, among other things, the failure

to meet specified milestones specified in the Restructuring Term Sheet and in any DIP order.

The Restructuring Transactions

are subject to certain customary conditions, including approval by the Bankruptcy Court. Accordingly, no assurance can be given that the

transactions described in this Current Report on Form 8-K (this “Current Report”) will be consummated.

Amended Intermediation Facility Agreement

Separately, to permit the

Company Parties to continue purchasing crude oil from Macquarie Energy North America Trading Inc. (“Macquarie”) for

the Company Parties’ ordinary course operations and for Macquarie to continue purchasing all Products (as defined in that certain

Supply and Offtake Agreement, dated as of April 1, 2022 (the “Intermediation Facility Agreement”), by and between Vertex

Refining Alabama LLC and Macquarie), Macquarie and the Company Parties agreed to amend and restate the facility existing under the Intermediation

Facility Agreement on the terms and conditions set forth in the Intermediation Facility Term Sheet attached the Restructuring Support

Agreement (the “Amended Intermediation Facility”). Entry into the Amended Intermediation Facility is subject to approval

by the Bankruptcy Court.

The foregoing description of the

Restructuring Support Agreement, DIP Term Sheet, the Intermediation Facility Term Sheet, and the transactions and documents contemplated

thereby does not purport to be complete and is qualified in its entirety by reference to the Restructuring Support Agreement, a copy of

which is filed as Exhibit 10.1 hereto and incorporated herein by reference.

Item 1.03 Bankruptcy or Receivership.

On September 24, 2024 (the “Petition

Date”), the Company Parties filed the Chapter 11 Cases and the Plan in the Bankruptcy Court.

The

Company Parties will continue to operate their businesses as debtors-in-possession under the jurisdiction of the Bankruptcy Court in accordance

with the applicable provisions of the Bankruptcy Code and orders of the Bankruptcy Court. The Company Parties requested approval from

the Bankruptcy Court for a variety of “first day” motions designed to facilitate the administration of the Chapter 11

Cases and minimize disruption to the Company Parties’ operations, including authority to honor trade claims in the ordinary

course of business during the Chapter 11 Cases. The Company Parties anticipate emerging from the

Chapter 11 Cases within 115 days of the Petition Date.

The disclosure statement for the

Plan, which includes a copy of the Plan, is filed as Exhibit 99.1 hereto and incorporated herein by reference.

Item 2.04 Triggering Events that Accelerate or

Increase a Direct Financial Obligation or an Obligation under an Off-Balance Sheet Arrangement.

The filing of the Chapter 11 Cases

described above in this Current Report constituted an event of default that accelerated the Company Parties’ respective obligations

under the following debt instruments (collectively, the “Debt Instruments”):

| |

● |

Indenture, dated as of November 1, 2021, by and among the Company and U.S.

Bank Trust Company, National Association as successor in interest to U.S. Bank National Association, as Trustee, and the approximately

$15.2 million aggregate outstanding principal amount of the 6.25% Convertible Senior Notes due 2027 issued thereunder; and |

| |

● |

Term Loan, consisting of $271.9 million aggregate principal amount outstanding

thereunder and all other amounts due and payable thereunder including but not limited to prepayment premiums, exit fees and accrued and

unpaid interest (collectively, the “Term Loan Claims”). |

The Debt Instruments provide

that, as a result of the Chapter 11 Cases, the principal and interest due thereunder will be immediately due and payable, along with

appliable premiums and fees. Any efforts to enforce such payment obligations under the Debt Instruments are automatically stayed as

a result of the Chapter 11 Cases, and the stakeholders’ rights of enforcement in respect of the Debt Instruments are subject

to the applicable provisions of the Bankruptcy Code. Additionally, in connection with the Chapter 11 Cases, the Company has

incurred, and expects to continue to incur, significant professional fees and other costs in connection with the Chapter 11 Cases.

There can be no assurance that the Company’s current liquidity is sufficient to allow it to satisfy its obligations related to

the Chapter 11 Cases or to pursue confirmation of a Chapter 11 plan.

Item 5.02 Departure of Directors or Certain Officers;

Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers.

Management Retention Bonus

The Company, with the recommendation

of the Compensation Committee of the Board of Directors and the approval of the Board of Directors, entered into a retention letter agreement

with Alvaro Ruiz, the Company’s Chief Strategy Officer, on September 19, 2024, and agreed to pay a retention bonus to Mr. Ruiz of

$154,020. The bonus is subject to the recipient’s obligation to repay the net after-tax bonus in the event that the recipient’s

employment with the Company is terminated by the Company for any reason other than cause, or his death or disability prior to the later

of six months after the date the letter agreement is entered into and the date of a change of control transaction (including an asset

sale of all or substantially all of the Company’s assets). Mr. Ruiz also entered into a waiver and release in favor of the Company

in consideration for the retention bonus, pursuant to which he agreed to release all claims against the Company related to his employment

and certain other employment matters and claims.

Item 7.01 Regulation FD Disclosure.

On September 24, 2024, the Company

issued a press release disclosing the entry into the Restructuring Support Agreement and related matters.

A copy of the press release is

attached as Exhibit 99.2 hereto and incorporated by reference herein.

The information contained

in, or incorporated into, Item 7.01 of this Current Report is furnished under Item 7.01 of Form 8-K and shall

not be deemed “filed” for the purposes of Section 18 of the Exchange Act of 1934, as amended (the “Exchange

Act”) or otherwise subject to the liabilities of that section, and shall not be deemed to be incorporated by reference into

the filings of the Company under the Securities Act of 1933, as amended, or the Exchange Act regardless of any general incorporation language

in such filings.

Item 8.01 Other Events.

Additional Information on the Chapter 11

Cases

Bankruptcy

Court filings and other information related to the Chapter 11 Cases are available at a website administered by the Company’s claims

agent, Kurtzman Carson Consultants, LLC dba Verita Global, at https://www.veritaglobal.net/vertex, or at or the Bankruptcy Court’s

website at www.txs.uscourts.gov/bankruptcy. The documents and other information available via website or elsewhere are not part

of this Current Report and shall not be deemed incorporated herein.

Trading in the Company’s Securities

The Company cautions that trading

in the Company’s securities (including, without limitation, its Common Stock) during the pendency of the Chapter 11 Cases is highly

speculative and poses substantial risks. Trading prices for the Company’s securities may bear little or no relationship to the actual

recovery, if any, by holders of the Company’s securities in the Chapter 11 Cases. The Company expects that its equity holders will

experience a significant or complete loss on their investment, depending on the outcome of the Chapter 11 Cases. Further, the Company

expects to receive a notice of delisting from Nasdaq as a result of the Chapter 11 Cases.

Item 9.01 Financial

Statements and Exhibits.

* Filed herewith.

** Furnished herewith.

Forward-Looking Statements

This

Current Report, including the exhibits attached hereto, contains “forward-looking statements” related to future events. Forward-looking

statements contain words such as “expect,” “anticipate,” “could,” “should,” “intend,”

“plan,” “believe,” “seek,” “see,” “may,” “will,” “would,”

or “target.” Forward-looking statements are based on management’s current expectations, beliefs, assumptions, and estimates

and may include, for example, statements regarding the Chapter 11 Cases, the Company’s ability to complete the Restructuring and

its ability to continue operating in the ordinary course while the Chapter 11 Cases are pending. These statements are subject to significant

risks, uncertainties, and assumptions that are difficult to predict and could cause actual results to differ materially and adversely

from those expressed or implied in the forward-looking statements, including risks and uncertainties regarding the Company’s ability

to successfully complete a restructuring under Chapter 11, including: consummation of the Restructuring; potential adverse effects of

the Chapter 11 Cases on the Company’s liquidity and results of operations; the Company’s ability to obtain timely approval

by the Bankruptcy Court with respect to the motions filed in the Chapter 11 Cases; objections to the Company’s recapitalization

process or other pleadings filed that could protract the Chapter 11 Cases; employee attrition and the Company’s ability to retain

senior management and other key personnel due to distractions and uncertainties; the Company’s ability to comply with financing

arrangements; the Company’s ability to maintain relationships with suppliers, customers, employees, and other third parties and

regulatory authorities as a result of the Chapter 11 Cases; the effects of the Chapter 11 Cases on the Company and on the interests of

various constituents, including holders of Common Stock; the Bankruptcy Court’s rulings in the Chapter 11 Cases, including the approvals

of the terms and conditions of the Restructuring and the outcome of the Chapter 11 Cases generally; the length of time that the Company

will operate under Chapter 11 protection and the continued availability of operating capital during the pendency of the Chapter 11 Cases;

risks associated with third party motions in the Chapter 11 Cases, which may interfere with the Company’s ability to consummate

the Restructuring or an alternative transaction; increased administrative and legal costs related to the Chapter 11 process; and other

litigation and inherent risks involved in a bankruptcy process. Accordingly, readers should not place undue reliance on any forward-looking

statements. Forward-looking statements may include comments as to the Company’s beliefs and expectations as to future financial

performance, events and trends affecting its business and are necessarily subject to uncertainties, many of which are outside the Company’s

control. More information on potential factors that could affect the Company’s financial results is included from time to time in

the “Cautionary Statement Regarding Forward-Looking Statements,” “Risk Factors” and

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the

Company’s most recently filed periodic reports on Form 10-K and Form 10-Q and subsequent filings with the Securities and Exchange

Commission, which are available at www.sec.gov and in the “Investor Relations” – “SEC Filings” section of

the Company’s website at www.vertexenergy.com. Forward-looking statements speak only as of the date they are made. The Company undertakes

no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise

that occur after that date, except as otherwise provided by law.

SIGNATURES

Pursuant to the requirements

of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto

duly authorized.

| |

VERTEX ENERGY, INC. |

|

| |

|

|

| Date: September 26, 2024 |

By: |

/s/ Chris Carlson |

|

| |

|

Chris Carlson |

|

| |

|

Chief Financial Officer |

|

Vertex Energy, Inc. 8-K

Exhibit 10.1

THIS

RESTRUCTURING SUPPORT AGREEMENT IS NOT AN OFFER OR ACCEPTANCE WITH RESPECT TO ANY SECURITIES OR A SOLICITATION OF ACCEPTANCES

OF A CHAPTER 11 PLAN WITHIN THE MEANING OF SECTION 1125 OF THE BANKRUPTCY CODE. ANY SUCH OFFER OR SOLICITATION WILL COMPLY WITH

ALL APPLICABLE SECURITIES LAWS AND/OR PROVISIONS OF THE BANKRUPTCY CODE. NOTHING CONTAINED IN THIS RESTRUCTURING SUPPORT AGREEMENT

SHALL BE AN ADMISSION OF FACT OR LIABILITY OR, UNTIL THE OCCURRENCE OF THE AGREEMENT EFFECTIVE DATE ON THE TERMS DESCRIBED HEREIN,

DEEMED BINDING ON ANY OF THE PARTIES HERETO.

THIS

RESTRUCTURING SUPPORT AGREEMENT IS THE PRODUCT OF SETTLEMENT DISCUSSIONS AMONG THE PARTIES HERETO. ACCORDINGLY, THIS RESTRUCTURING

SUPPORT AGREEMENT IS PROTECTED BY RULE 408 OF THE FEDERAL RULES OF EVIDENCE AND ANY OTHER APPLICABLE STATUTES OR DOCTRINES PROTECTING

THE USE OR DISCLOSURE OF CONFIDENTIAL SETTLEMENT DISCUSSIONS.

THIS

RESTRUCTURING SUPPORT AGREEMENT DOES NOT PURPORT TO SUMMARIZE ALL OF THE TERMS, CONDITIONS, REPRESENTATIONS, WARRANTIES, AND OTHER

PROVISIONS WITH RESPECT TO THE RESTRUCTURING TRANSACTIONS DESCRIBED HEREIN, WHICH TRANSACTIONS WILL BE SUBJECT TO THE COMPLETION

OF THE DEFINITIVE DOCUMENTS INCORPORATING THE TERMS SET FORTH HEREIN AND THE CLOSING OF ANY RESTRUCTURING TRANSACTION SHALL BE

SUBJECT TO THE TERMS AND CONDITIONS SET FORTH IN SUCH DEFINITIVE DOCUMENTS AND THE APPROVAL RIGHTS OF THE PARTIES SET FORTH HEREIN

AND IN SUCH DEFINITIVE DOCUMENTS, IN EACH CASE, SUBJECT TO THE TERMS HEREOF.

RESTRUCTURING

SUPPORT AGREEMENT

This

RESTRUCTURING SUPPORT AGREEMENT (including all exhibits, annexes, and schedules hereto in accordance with Section 14.02, this

“Agreement”) is made and entered into as of September 24, 2024 (the “Execution Date”),

by and among the following parties (each of the following described in sub-clauses (i) through (ii) of this preamble, and any

Entity that subsequently becomes a party hereto by executing and delivering to counsel to the Company Parties and counsel to each

of the Consenting Stakeholders a Joinder, collectively, the “Parties”):1

| i. | Vertex

Energy, Inc., a company incorporated under the Laws of Nevada (“Vertex”),

and each of its Affiliates listed on Exhibit A to this Agreement that have

executed and delivered counterpart signature pages to this Agreement to counsel to the

Consenting Stakeholders (the Entities in this clause (i), collectively, the “Company

Parties”); and |

| 1 | Capitalized

terms used but not defined in the preamble and recitals to this Agreement have the meanings

ascribed to them in Section 1. |

| ii. | the

undersigned holders of, or investment advisors, sub-advisors, or managers of discretionary

accounts that hold Term Loan Claims that have executed and delivered counterpart signature

pages to this Agreement, a Joinder, or a Transfer Agreement to counsel to the Company

Parties (the Entities in this clause (ii), collectively, the “Consenting

Term Loan Lenders,” and together with any person or Entity that subsequently

becomes a Party hereto by executing and delivering a Joinder to counsel to the Company

Parties and counsel to the Consenting Term Loan Lenders, the “Consenting

Stakeholders”). |

RECITALS

WHEREAS,

the Company Parties and the Consenting Stakeholders have in good faith and at arms’ length negotiated or been apprised of

certain restructuring and recapitalization transactions with respect to the Company Parties’ capital structure on the terms

set forth in this Agreement and as specified in the term sheet attached as Exhibit B hereto (together with any exhibits

and appendices annexed thereto, the “Restructuring Term Sheet,” and such transactions, as described

in this Agreement and the Restructuring Term Sheet, the “Restructuring Transactions”);

WHEREAS,

the Company Parties intend to implement the Restructuring Transactions through the commencement by the Debtors of voluntary cases

under chapter 11 of title 11 of the United States Code, 11 U.S.C. §§ 101–1532 (as amended, the “Bankruptcy

Code”) in the United States Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court,”

and the cases commenced, the “Chapter 11 Cases”); and

WHEREAS,

the Parties have agreed to take certain actions in support of the Restructuring Transactions on the terms and conditions set forth

in this Agreement and the Restructuring Term Sheet;

NOW,

THEREFORE, in consideration of the covenants and agreements contained herein, and for other valuable consideration, the receipt

and sufficiency of which are hereby acknowledged, each Party, intending to be legally bound hereby, agrees as follows:

AGREEMENT

| Section

1. | Definitions

and Interpretation. |

| 1.01. | Definitions.

The following terms shall have the following definitions: |

“2027

Convertible Notes” means that certain 6.250% senior unsecured convertible notes due 2027, issued by Vertex Energy,

Inc. pursuant to that certain indenture, dated as of November 1, 2021, by and between Vertex and the Trustee, as may be amended,

modified, amended and restated, or otherwise supplemented from time to time.

“2027

Convertible Notes Claim” means any Claim on account of the 2027 Convertible Notes.

“Affiliate”

has the meaning set forth in section 101(2) of the Bankruptcy Code as if such Entity was a debtor in a case under the Bankruptcy

Code.

“Agent”

means Cantor Fitzgerald Securities, in its capacity as administrative agent and collateral agent under the Term Loan.

“Agreement”

has the meaning set forth in the preamble to this Agreement and, for the avoidance of doubt, includes all the exhibits, annexes,

and schedules hereto in accordance with Section 14.02 (including the Restructuring Term Sheet).

“Agreement

Effective Date” means the date on which the conditions set forth in Section 2.01 have been satisfied or waived by

the appropriate Party or Parties in accordance with this Agreement.

“Agreement

Effective Period” means, with respect to a Party, the period from the Agreement Effective Date to the Termination

Date applicable to that Party.

“Alternative

Restructuring Proposal” means any written or oral plan, inquiry, proposal, offer, bid, term sheet, discussion, or

agreement with respect to (a) a sale, disposition, new-money investment, restructuring, reorganization, merger, amalgamation,

acquisition, consolidation, dissolution, debt investment, equity investment, liquidation, asset sale, share issuance, tender offer,

recapitalization, plan of reorganization, share exchange, business combination, joint venture, partnership, debt incurrence (including,

without limitation, any debtor-in-possession financing, use of cash collateral, or exit financing) or similar transaction or series

of transactions involving any one or more Company Parties or the debt, equity, or other interests in any one or more of the Company

Parties, other than the Restructuring Transactions, or (b) any other transaction involving any one or more of the Company Parties

that is an alternative to one or more of the Restructuring Transactions. For the avoidance of doubt, any inquiry, proposal, offer,

bid, term sheet, discussion, agreement, or sale in connection with and/or pursuant to the Bidding Procedures is not an Alternative

Restructuring Proposal.

“Bankruptcy

Code” has the meaning set forth in the Recitals to this Agreement.

“Bankruptcy

Court” has the meaning set forth in the Recitals to this Agreement.

“Bidding

Procedures” means the procedures governing the submission and evaluation of bids to purchase all, substantially

all, or any portion of the Company’s assets and/or Equity Interests.

“Bidding

Procedures Motion” means the Debtors’ Emergency Motion for Entry of an Order (I) Approving the Bidding

Procedures and Auction, (II) Scheduling Bid Deadlines, an Auction, Objection Deadlines, and a Sale Hearing, (III) Approving the

Assumption and Assignment Procedures, (IV) Approving the Form and Manner of Notice of a Sale Transaction, the Auction, the Sale

Hearings, and Assumption and Assignment Procedures, (V) Authorizing the Sale of the Debtors’ Assets Free and Clear of All

Encumbrances, and (VI) Granting Related Relief.

“Bidding

Procedures Order” means the order of the Bankruptcy Court approving the Bidding Procedures Motion.

“Business

Day” means any day other than a Saturday, Sunday, or other day on which commercial banks are authorized to close

under the Laws of, or are in fact closed in, the state of New York.

“Causes

of Action” means any Claims, interests, damages, remedies, causes of action, demands, rights, actions,

controversies, proceedings, agreements, suits, obligations, liabilities, accounts, defenses, offsets, powers, privileges,

licenses, Liens, indemnities, guaranties, and franchises of any kind or character whatsoever, whether known or unknown,

foreseen or unforeseen, existing or hereinafter arising, contingent or non-contingent, liquidated or unliquidated, secured or

unsecured, assertable, directly or derivatively, matured or unmatured, suspected or unsuspected, whether arising before, on,

or after the Petition Date, in contract, tort, law, equity, or otherwise. Causes of Action also include: (a) all rights of

setoff, counterclaim, or recoupment and claims under contracts or for breaches of duties imposed by law or in equity; (b) the

right to object to or otherwise contest Claims or Equity Interests; (c) claims pursuant to section 362 or chapter 5 of the

Bankruptcy Code; (d) such claims and defenses as fraud, mistake, duress, and usury, and any other defenses set forth in

section 558 of the Bankruptcy Code; and (e) any avoidance actions arising under chapter 5 of the Bankruptcy Code or under

similar local, state, federal, or foreign statutes and common law, including fraudulent transfer Laws.

“Chapter

11 Cases” has the meaning set forth in the Recitals to this Agreement.

“Claim” has

the meaning ascribed to it in section 101(5) of the Bankruptcy Code.

“Company Claims/Equity

Interests” means any Claim against, or Equity Interest in, a Company Party, including, without limitation, the

Term Loan Claims and any Claims and/or Equity Interests held by Consenting Stakeholders.

“Company

Parties” has the meaning set forth in the preamble to this Agreement.

“Confidentiality

Agreement” means an executed confidentiality agreement, including with respect to the issuance of a

“cleansing letter” or other public disclosure of material non-public information agreement, in connection with

any proposed Restructuring Transactions.

“Confirmation

Order” means the conformation order with respect to the Plan.

“Consenting Stakeholders”

has the meaning set forth in the preamble to this Agreement.

“Consenting

Term Loan Lenders” has the meaning set forth in the preamble to this Agreement.

“Debtors”

means the Company Parties that commence Chapter 11 Cases.

“Definitive

Documents” means, collectively, each of the documents listed in Section 3.01 of this Agreement.

“DIP

Agent” means Cantor Fitzgerald Securities, as the administrative agent and collateral agent under the DIP Credit

Agreement, its successors, assigns, or any replacement agent appointed pursuant to the terms of the DIP Credit Agreement.

“DIP

Claim” means any Claim on account of the DIP Facility.

“DIP

Facility” means the new super-senior, secured debtor-in-possession financing facility made in accordance with the

terms of the DIP Loan Agreement.

“DIP

Lenders” has the meaning set forth in the DIP Term Sheet.

“DIP

Loan Agreement” means the Senior Secured Super-Priority Debtor-In-Possession Loan and Security Agreement by and

among certain Company Parties, the DIP Agent, and the lenders party thereto setting forth the terms and conditions of a $280 million

debtor in possession financing facility.

“DIP

Loan Documents” means the DIP Loan Agreement and any other documentation necessary to effectuate the incurrence

of the DIP Facility.

“DIP

Orders” means, as applicable, the interim and final orders of the Bankruptcy Court approving, among other things,

the terms of the debtor-in-possession financing, which shall be consistent with the DIP Loan Agreement.

“DIP

Term Sheet” means the term sheet attached hereto as Exhibit C.

“Disclosure

Statement” means the related disclosure statement with respect to the Plan.

“Disclosure Statement Order”

means an order entered by the Bankruptcy Court approving the adequacy of the Disclosure Statement

“Entity”

shall have the meaning set forth in section 101(15) of the Bankruptcy Code.

“Equity

Interests” means, collectively, the shares (or any class thereof), common stock, preferred stock, limited

liability company interests, partnership interests, and any other equity, ownership, or profits interests of any Company

Party, and options, warrants, rights, or other securities or agreements to acquire or subscribe for, or which are convertible

into the shares (or any class thereof) of, common stock, preferred stock, limited liability company interests, or other

equity, ownership, or profits interests of any Company Party (in each case whether or not arising under or in connection with

any employment agreement).

“Exchange

Act” means the Securities Exchange Act of 1934, as amended.

“Execution Date” has the meaning

set forth in the preamble to this Agreement.

“First

Day Pleadings” means the first-day pleadings that the Company Parties determine are necessary or desirable to file.

“Governmental

Body” means any U.S. or non-U.S. federal, state, municipal, or other government, or other department, commission,

board, bureau, agency, public authority, or instrumentality thereof, or any other U.S. or non-U.S. court or arbitrator.

“Intermediation

Facility Term Sheet” means the term sheet attached hereto as Exhibit D.

“Joinder”

means an executed form of the joinder providing, among other things, that the signing holder of Company Claims/Equity Interests

is bound by the terms of this Agreement, substantially in the form attached hereto as Exhibit F.

“Law”

means any federal, state, local, or foreign law (including common law), statute, code, ordinance, rule, regulation, decree, injunction,

order, ruling, assessment, writ, or other legal requirement or judgment, in each case, that is validly adopted, promulgated, issued,

or entered by a governmental authority of competent jurisdiction (including the Bankruptcy Court).

“Management

Incentive Plan” has the meaning set forth in the Restructuring Term Sheet.

“Milestones”

has the meaning set forth in Section 6.01(b).

“Named

Executive Officers and Directors” has the meaning set forth in the Term Loan Credit Agreement.

“Parties”

has the meaning set forth in the preamble of this Agreement.

“Permitted

Transfer” means a Transfer of any Company Claims/Equity Interests that meets the requirements of Section 8.01.

“Permitted

Transferee” means each transferee of any Company Claims/Equity Interests who meets the requirements of Section 8.01.

“Petition

Date” means the first date any of the Company Parties commences a Chapter 11 Case.

“Plan”

means the joint plan of reorganization filed by the Debtors under chapter 11 of the Bankruptcy Code that embodies the

Restructuring Transactions.

“Plan

Effective Date” means the occurrence of the effective date of the Plan according to its terms.

“Plan

Supplement” means the compilation of documents and forms of documents, schedules, and exhibits to the Plan that

will be filed by the Debtors with the Bankruptcy Court.

“Potential

Purchasers” means a group of potential transaction counterparties participating in the PWP Marketing Process to

be determined by the Company Parties.

“Purchase

Agreement” means any asset or stock purchase agreement to be entered into as part of the Sale Transaction by and

among the Company Parties, as sellers, and the Successful Bidder (if any).

“PWP

Marketing Process” means the marketing process launched on September 3, 2024, by the Company Parties with the assistance

of their investment banker, Perella Weinberg Partners Group, LP.

“Qualified

Marketmaker” means an Entity that (a) holds itself out to the public or the applicable private markets as standing

ready in the ordinary course of business to purchase from customers and sell to customers Company Claims/Equity Interests (or

enter with customers into long and short positions in Company Claims/Equity Interests), in its capacity as a dealer or market

maker in Company Claims/Equity Interests and (b) is, in fact, regularly in the business of making a market in claims against issuers

or borrowers (including debt securities or other debt).

“Remedial

Action” means any action to enforce, request the enforcement of (including any request upon a trustee or agent),

or direct the enforcement of any of the rights and remedies available under any credit agreement, indenture, note, loan agreement,

guaranty, collateral or security agreement, or any agreements or instruments entered into in connection with any of the foregoing

or any amendments or supplements to any of the foregoing (each, a “Debt Document”), including, without

limitation, any action to accelerate or collect any amounts with respect to the obligations under a Debt Document, the sending

of any written notice to the Company Party that a default or event of default has occurred under a Debt Document and is continuing,

the sending of any written request to any trustee or agent under a Debt Document to initiate an action, suit or proceeding such

Debt Document, or any action to exercise any rights or remedies under such Debt Document, which is actually known to the Company

Parties.

“Related

Fund” means, with respect to any Entity, any fund, account or investment vehicle that is controlled, advised or

managed by (a) such Entity, (b) an Affiliate of such Entity, or (c) the same investment manager, advisor, or subadvisor that controls,

advises, or manages such Entity or an Affiliate of such investment manager, advisor, or subadvisor.

“Related

Party” means each of, and in each case in its capacity as such, current and former directors, managers, officers,

committee members, members of any governing body, equity holders (regardless of whether such interests are held directly or indirectly),

affiliated investment funds or investment vehicles, managed accounts or funds, predecessors, participants, successors, assigns,

subsidiaries, Affiliates, partners, limited partners, general partners, principals, members, management companies, fund advisors

or managers, employees, agents, trustees, advisory board members, financial advisors, attorneys (including any other attorneys

or professionals retained by any current or former director or manager in his or her capacity as director or manager of an Entity),

accountants, investment bankers, consultants, representatives, and other professionals and advisors and any such person’s

or Entity’s respective heirs, executors, estates, and nominees.

“Required

Consenting Stakeholders” means the Required Consenting Term Loan Lenders.

“Required

Consenting Term Loan Advisor” means Sidley Austin LLP.

“Required

Consenting Term Loan Lenders” means, as of the relevant date, Consenting Term Loan Lenders holding at least 80%

of the aggregate outstanding principal amount of the Term Loan Claims that are held by Consenting Term Loan Lenders.

“Required

DIP Lenders” has the meaning set forth in the DIP Term Sheet.

“Restructuring

Expenses” means the reasonable and documented fees and expenses incurred by the Agent, any Term Loan Lender, or

any DIP Lender including legal fees and expenses of any legal counsel and fees and expenses of Houlihan Lokey Capital, Inc.,

as financial advisor to the Term Loan Lenders and DIP Lenders.

“Restructuring

Term Sheet” has the meaning set forth in the recitals of this Agreement.

“Restructuring

Transactions” means the transactions described in this Agreement and the Restructuring Term Sheet.

“Rules”

means Rule 501(a)(1), (2), (3), (7), (8), (9), (12), and (13) of the Securities Act.

“Sale

Documents” means all agreements, instruments, pleadings, orders or other related documents utilized to

consummate the Sale Transaction, including, but not limited to, the Bidding Procedures, Bidding Procedures Motion, Bidding

Procedures Order, Sale Order(s), and Purchase Agreement, each of which shall contain terms and conditions that are materially

consistent with this Agreement.

“Sale

Order” means one or more orders of the Bankruptcy Court approving a Sale Transaction.

“Sale

Transaction” means the sale of all, substantially all, or any portion of the Company Parties’ assets and/or

Equity Interests.

“Securities

Act” means the Securities Act of 1933, as amended.

“Shell

Claims” means any Claim on account of transactions by and between Vertex Refining Alabama LLC and the Shell Party.

“Shell

Party” means Shell Energy North America (US), L.P.

“Solicitation

Materials” means all materials to be distributed in connection with solicitation of votes to approve the Plan.

“Successful

Bidder” has the meaning set forth in the Restructuring Term Sheet.

“Term

Loan” means loans outstanding under the credit agreement, dated April 1, 2022, by and between Vertex Refining Alabama

LLC, as borrower, Vertex, as parent and guarantor, Cantor Fitzgerald Securities, as agent, and the lenders party thereto.

“Term

Loan Claims” means any Claim arising from or based upon the Term Loan.

“Term

Loan Credit Agreement” has the meaning set forth in the Restructuring Term Sheet.

“Termination

Date” means the date on which termination of this Agreement as to a Party is effective in accordance with

Sections 12.01, 12.02, 12.03, or 12.04.

“Transfer”

means to sell, resell, reallocate, use, pledge, assign, transfer, hypothecate, participate, donate, or otherwise encumber or dispose

of, directly or indirectly (including through derivatives, options, swaps, pledges, forward sales or other transactions).

“Transfer

Agreement” means an executed form of the transfer agreement providing, among other things, that a transferee is

bound by the terms of this Agreement and substantially in the form attached hereto as Exhibit E.

“Trustee”

means U.S. Bank National Association, in its capacity as trustee under the 2027 Convertible Notes

“U.S.

Trustee” means the Office of the United States Trustee for the Southern District of Texas.

1.02. Interpretation.

For purposes of this Agreement, the following rules of interpretation shall apply:

(a) in

the appropriate context, each term, whether stated in the singular or the plural, shall include both the singular and the plural,

and pronouns stated in the masculine, feminine, or neuter gender shall include the masculine, feminine, and the neuter gender;

(b) capitalized

terms defined only in the plural or singular form shall nonetheless have their defined meanings when used in the opposite form;

(c) unless

otherwise specified, any reference herein to a contract, lease, instrument, release, indenture, or other agreement or document

being in a particular form or on particular terms and conditions means that such document shall be substantially in such form

or substantially on such terms and conditions;

(d) unless

otherwise specified, any reference herein to an existing document, schedule, or exhibit shall mean such document, schedule, or

exhibit, as it may have been or may be amended, restated, amended and restated, supplemented, or otherwise modified or replaced

from time to time; provided that any capitalized terms herein which are defined with reference to another agreement, are

defined with reference to such other agreement as of the date of this Agreement, without giving effect to any termination of such

other agreement or amendments to such capitalized terms in any such other agreement following the date hereof;

(e) unless

otherwise specified, all references herein to “Sections” are references to Sections of this Agreement;

(f) the

words “herein,” “hereof,” “hereinafter,” “hereunder” and “hereto”

refer to this Agreement in its entirety rather than to any particular portion of this Agreement;

(g) captions

and headings to Sections are inserted for convenience of reference only and are not intended to be a part of or to affect the

interpretation of this Agreement;

(h) references

to “shareholders,” “directors,” and/or “officers” shall also include “members”

and/or “managers,” as applicable, as such terms are defined under the applicable limited liability company Laws;

(i) all

exhibits attached hereto or referred to herein are hereby incorporated in and made a part of this Agreement as if set forth in

full herein;

(j) the

use of “include” or “including” is without limitation, whether stated or not and shall not be construed

to limit any general statement that it follows to the specific or similar items or matters immediately following it; and

(k) the

phrase “counsel to the Consenting Stakeholders” refers in this Agreement to each counsel specified in Section 14.10

other than counsel to the Company Parties.

| Section

2. | Effectiveness

of this Agreement. |

2.01.

Agreement Effective Date. This Agreement

shall become effective and binding upon each of the Parties at 12:00 a.m., prevailing Eastern Time, on the Agreement Effective

Date, which is the date on which all of the following conditions have been satisfied or waived in accordance with this Agreement:

(a) each

of the Company Parties shall have executed and delivered counterpart signature pages of this Agreement to counsel to each of the

Consenting Stakeholders;

(b) holders

of at least 80% of the aggregate outstanding principal amount of Term Loan Claims shall have executed and delivered counterpart

signature pages of this Agreement to counsel to the Company Parties; and

(c) counsel

to the Company Parties shall have given notice to counsel to each of the Consenting Stakeholders in the manner set forth in Section

14.10 hereof (by email or otherwise) that the other conditions to the Agreement Effective Date set forth in this Section 2.01

have occurred.

| Section

3. | Definitive

Documents. |

3.01. The

Definitive Documents governing the Restructuring Transactions shall include this Agreement and each of the following:

| (a) | the

Restructuring Term Sheet (and all exhibits thereto); |

| (b) | the

Plan (and all exhibits thereto); |

| (c) | the

Disclosure Statement (and all exhibits thereto); |

| (d) | the

Solicitation Materials; |

(e) any

order of the Bankruptcy Court approving the Disclosure Statement and the other Solicitation Materials (and motion(s) seeking approval

thereof);

| (g) | the

DIP Facility Documents; |

| (h) | the

Confirmation Order; |

| (i) | the

Plan Supplement; and |

(j) the

Sale Documents, if any, including, but not limited to, the Bidding Procedures, the Bidding Procedures Motion, and the Bidding

Procedures Order, Sale Order(s), and Purchase Agreement(s).

3.02. The

Definitive Documents not executed or in a form attached to this Agreement as of the Execution Date remain subject to negotiation

and completion. Upon completion, the Definitive Documents and every other document, deed, agreement, filing, notification, letter,

or instrument related to the Restructuring Transactions shall contain terms, conditions, representations, warranties, and covenants

consistent with the terms of this Agreement, as they may be modified, amended, or supplemented in accordance with Section 13.

Further, the Definitive Documents not executed or in a form attached to this Agreement as of the Execution Date shall otherwise

be in form and substance, including with respect to any amendment, modification, or supplement thereto, reasonably acceptable

to the Company Parties and the Required Consenting Stakeholders.

| Section

4. | Commitments

of the Consenting Stakeholders. |

| 4.01. | General

Commitments, Forbearances, and Waivers. |

(a) During

the Agreement Effective Period, each Consenting Stakeholder agrees, in respect of all of its Company Claims/Equity Interests,

to:

(i) support

the Restructuring Transactions, act in good faith, and vote all Company Claims/Equity Interests owned, held, or otherwise controlled

by such Consenting Stakeholder and exercise any powers or rights available to it (including in any board, shareholders’,

or creditors’ meeting or in any process requiring voting or approval to which they are legally entitled to participate)

in each case in favor of any matter requiring approval to the extent necessary to implement the Restructuring Transactions;

(ii) use

commercially reasonable efforts to cooperate with and assist the Company Parties in obtaining additional support for the Restructuring

Transactions from the Company Parties’ other stakeholders;

(iii) use

commercially reasonable efforts to oppose any party or person from taking any actions contemplated in Section 4.02(b)(ii);

(iv) give

any notice, order, instruction, or direction to the applicable Agent/Trustee necessary to give effect to the Restructuring Transactions;

and

(v) negotiate

in good faith and use commercially reasonable efforts to execute and implement the Definitive Documents that are consistent with

this Agreement to which it is required to be a party.

(b) During

the Agreement Effective Period, each Consenting Stakeholder agrees, in respect of all of its Company Claims/Equity Interests,

that it shall not directly or indirectly:

(i) object

to, delay, impede, or take any other action to interfere with acceptance, implementation, or consummation of the Restructuring

Transactions;

(ii) object

to, delay, impede, or take any other action to interfere with entry of any Sale Document and/or consummation of, if any, Sale

Transaction;

(iii) propose,

file, support, or vote (or allow any proxy appointed by it to vote) for any Alternative Restructuring Proposal;

(iv) execute

or file any motion, objection, pleading, or other document with any court (including any modifications or amendments thereof)

that, in whole or in part, is not materially consistent with this Agreement and/or the Restructuring Term Sheet (nor directly

or indirectly direct any other person or Entity to make such filing);

(v) initiate,

or have initiated on its behalf, any litigation or proceeding of any kind with respect to the Chapter 11 Cases, this Agreement,

the Definitive Documents, or the other Restructuring Transactions contemplated herein against the Company Parties or the other

Parties other than to enforce this Agreement or any Definitive Document or as otherwise permitted under this Agreement (nor directly

or indirectly direct any other person or Entity to make such filing);

(vi) object

to any First Day Pleadings and “second day” pleadings consistent with this Agreement filed by the Debtors in furtherance

of the Restructuring Transactions, including any motion seeking approval of the DIP Facility on the terms set forth herein and

the DIP Credit Agreement;

(vii) object

to or commence any legal proceeding challenging the liens or claims (including the priority thereof) granted or proposed to be

granted to the DIP Commitment Parties under the DIP Orders;

(viii) exercise,

or direct any other person to exercise (either directly or indirectly), any right or remedy for the enforcement, collection, or

recovery of any of its Company Claims/Equity Interests;

(ix) announce publicly their intention

to not support the Restructuring Transactions;

(x) object

to, delay, impede, or take any other action to interfere with the Company Parties’ ownership and possession of their assets,

wherever located, or interfere with the automatic stay arising under section 362 of the Bankruptcy Code; or

(xi) take

any action that is inconsistent in any material respect with the Restructuring Transactions.

| 4.02. | Commitments

with Respect to Chapter 11 Cases. |

(a) During

the Agreement Effective Period, each Consenting Stakeholder that is entitled to vote to accept or reject the Plan pursuant to

its terms agrees that it shall, subject to receipt by such Consenting Stakeholder, whether before or after the commencement of

the Chapter 11 Cases, of the Solicitation Materials;

(i) vote

each of its Company Claims/Equity Interest to accept the Plan by delivering its duly executed and completed ballot accepting the

Plan on a timely basis following the commencement of the solicitation of the Plan and its actual receipt of the Solicitation Materials

and the ballot;

(ii) to

the extent it is permitted to elect whether to opt in to the releases set forth in the Plan, elect to opt in to the releases set

forth in the Plan by timely delivering its duly executed and completed ballot(s) indicating such election;

(iii) not

change, withdraw, amend, or revoke (or cause to be changed, withdrawn, amended, or revoked) any vote or election referred to in

clauses (i) and (ii) above;

(iv) agree

to provide, and opt in to and not object to, the releases set forth in the Plan;

(v) support

all of the debtor and third-party releases, injunctions, discharge, indemnity, and exculpation provisions provided in the

Plan, substantially consistent with those set forth in Annex 1 to the Restructuring Term Sheet;

(vi) not

directly or indirectly, through any person, seek, solicit, propose, support, assist, engage in negotiations in connection with

or participate in the formulation, preparation, filing, or prosecution of any Alternative Restructuring Proposal or object to

or take any other action that would reasonably be expected to prevent, interfere with, delay, or impede the solicitation, approval

of the Disclosure Statement, or the confirmation and consummation of the Plan and the Restructuring Transactions; and

(vii) support

and take all actions reasonably requested by the Company Parties to facilitate the solicitation, approval of the Disclosure Statement,

and confirmation and consummation of the Plan within the timeframes contemplated by this Agreement.

(b) During

the Agreement Effective Period, each Consenting Stakeholder, in respect of each of its Company Claims/Equity Interests, (i) will

support, and (ii) will not directly or indirectly object to, delay, impede, or take any other action to interfere with, in each

case, any motion or

other

pleading or document filed by a Company Party in the Bankruptcy Court that is consistent with this Agreement.

4.03. Commitments

with Respect to PWP Marketing Process. During the Agreement Effective Date, each Consenting Stakeholder and its advisors agree

that they shall:

(a) promptly

inform the Company Parties and/or counsel thereto in the event that they are contacted by a Potential Purchaser regarding the

Company Parties or the PWP Marketing Process; and

(b) not

directly or indirectly communicate with the Potential Purchasers regarding the Company Parties or the PWP Marketing Process without

the Company Parties’ prior written consent, which may be given by email from counsel thereto.

Section

5. Additional Provisions Regarding the

Consenting Stakeholders’ Commitments. Notwithstanding

anything contained in this Agreement, nothing in this Agreement shall: (a) affect the ability of any Consenting Stakeholder to

consult with any other Consenting Stakeholder, the Company Parties, or any other party in interest in the Chapter 11 Cases (including

any official committee and the U.S. Trustee); (b) impair or waive the rights of any Consenting Stakeholder to assert or raise

any objection permitted under this Agreement in connection with the Restructuring Transactions; and (c) prevent any Consenting

Stakeholder from enforcing this Agreement or contesting whether any matter, fact, or thing is a breach of, or is inconsistent

with, this Agreement.

| Section

6. | Commitments

of the Company Parties. |

6.01. Affirmative

Commitments. Except as set forth in Section 7, during the Agreement Effective Period, the Company Parties agree to:

(a) support

and take all steps reasonably necessary and desirable to consummate the Restructuring Transactions in accordance with this Agreement;

(b) comply

with the milestones set forth in the Restructuring Term Sheet and in any DIP Order (collectively, the “Milestones”);

(c) to

the extent any legal or structural impediment arises that would prevent, hinder, or delay the consummation of the Restructuring

Transactions contemplated herein, take all steps reasonably necessary and desirable to address any such impediment;

(d) use

commercially reasonable efforts to obtain any and all required regulatory and/or third-party approvals for the Restructuring Transactions;

(e) negotiate

in good faith and use commercially reasonable efforts to execute and deliver the Definitive Documents and any other required agreements

to effectuate and consummate the Restructuring Transactions as contemplated by this Agreement;

(f) use

commercially reasonable efforts to seek additional support for the Restructuring Transactions from their other material stakeholders;

(g) actively

oppose and object to the efforts of any person seeking to object to, delay, impede, or take any other action to interfere with

the acceptance, implementation, or consummation of the Restructuring Transactions (including, if applicable, the filing of timely

filed objections or written responses) to the extent such opposition or objection is reasonably necessary or desirable to facilitate

implementation of the Restructuring Transactions;

(h) upon

reasonable request of any of the Consenting Stakeholders, inform counsel to the Consenting Stakeholders as to: (i) the status

and progress of the Restructuring Transactions, including progress in relation to the Definitive Documents; and (ii) the status

of obtaining any necessary or reasonably desirable authorizations (including any consents) from each Consenting Stakeholder, any

competent judicial body, governmental authority, banking, taxation, supervisory, or regulatory body or any stock exchange;

(i) notify

counsel to the Consenting Stakeholders in writing (email being sufficient) of any Remedial Action taken by any creditor within

two (2) Business Days of the Company Parties receiving notice or obtaining actual knowledge of such Remedial Action;

(j) notify

counsel to the Consenting Stakeholders in writing (e-mail being sufficient) the commencement of any material governmental or third-party

complaints, litigations, investigations, or hearings (or communications indicating that the same may be contemplated or threatened),

in each case, as soon as reasonable possible, but no later than within two Business Days of the Company Parties receiving notice

or obtaining knowledge of any of the foregoing;

(k) notify

counsel to the Consenting Stakeholders (email being sufficient) within two calendar days of the Company Parties receiving

notice or obtaining actual knowledge of: (i) any event or circumstance that has occurred that would permit any Party to

terminate, or that would result in the termination of, this Agreement; (ii) any matter or circumstance that they know to be a

material impediment to the implementation or consummation of the Restructuring Transactions; (iii) a material breach of this

Agreement (including a material breach by any Company Parties); and (iv) any representation or statement made or deemed to be

made by any of them under this Agreement that is or proves to have been materially incorrect or misleading in any respect

when made or deemed to be made;

(l) use

commercially reasonable efforts to maintain its and its Affiliates’ good standing under the Laws of the state or other jurisdiction

in which they are incorporated or organized;

(m) upon

reasonable request of any of the Consenting Stakeholders, provide the Consenting Stakeholders with reasonable access to the Company

Parties’ books and records during normal business hours on reasonable advance notice to the Company Parties’ representatives

and without disruption to the operation of the Company Parties’ business;

(n) provide

to counsel to the Consenting Stakeholders drafts of: (i) First Day Pleadings and all orders sought pursuant thereto; (ii)

Bidding Procedures Motion; (iii) Sale Order; (iv) the Plan; (v) the Plan Supplement; (vi) the Disclosure Statement; (vii) the

Disclosure Statement Order; (viii) the Solicitation Materials; (ix) the DIP Orders; (x) the Confirmation Order, and (xi) all

other material filings, in each case, at least two calendar days prior to the date on which the Company Party files such

pleading;

(o) use

commercially reasonable efforts to provide to counsel to the Consenting Stakeholders all material draft motions and pleadings

not listed in subsection (n) above that the Company Parties or any of its Affiliates intend to file with the Bankruptcy Court

at least two calendar days prior to the date on which such party files such pleading; and

(p) promptly

pay Restructuring Expenses, subject to appropriate Bankruptcy Court approval.

6.02. Negative

Commitments. Except as set forth in Section 7, during the Agreement Effective Period, each of the Company Parties shall not

directly or indirectly:

(a) object

to, delay, impede, or take any other action to interfere with acceptance, implementation, or consummation of the Restructuring

Transactions;

(b) take

any action that is inconsistent in any material respect with, or is intended to frustrate or impede approval, implementation,

and consummation of the Restructuring Transactions described in, this Agreement or the Plan;

(c) modify

the Plan, in whole or in part, in a manner that is not consistent with this Agreement in all material respects;

(d) file

any motion, pleading, or Definitive Documents with the Bankruptcy Court or any other court (including any modifications or amendments

thereof) that, in whole or in part, is not materially consistent with this Agreement or the Plan;

(e) solicit,

initiate, endorse, propose, file, support, approve, or otherwise promote or advance any Alternative Restructuring Proposal. For

the avoidance of doubt, actions taken by the Company as part of the PWP Marketing Process, or otherwise in accordance with the

Bidding Procedures (which such procedures shall be in form and substance acceptable to the Required Consenting Term Loan Lenders)

shall not be a violation of this Section 6.02(e);

(f) sell,

or file any motion or application seeking to sell, any material assets, other than in the ordinary course of business, without

the prior written consent of the Required Consenting Stakeholders (which may be by email);

(g) other

than as provided in this Agreement and the Restructuring Term Sheet, amend any of their corporate governance or organizational

documents without the prior written consent of the Required Consenting Stakeholders (which may be by email), not to be unreasonably

withheld;

(h) other

than in the ordinary course of business or as required by Law or regulation, (i) enter into or amend, establish, adopt, restate,

supplement, or otherwise modify or accelerate (x) any deferred compensation, incentive, success, retention, bonus, or other compensatory

arrangements, policies, programs, practices, plans, or agreements, including, without limitation, offer letters, employment agreements,

consulting agreements, severance arrangements, or change in control arrangements with or for the benefit of Named Executive Officers

and Directors, or (y) any contracts, arrangements, or commitments that entitle any Named Executive Officers and Directors to indemnification

from the Company Parties, or (ii) amend or terminate any existing

compensation

or benefit plans or arrangements (including employment agreements), in each case without the prior written consent of the Required

Consenting Stakeholders (which may be by email);

(i) other

than in the ordinary course of business, (i) enter into any settlement regarding any Claims or Equity Interests, (ii) enter into

any material agreement that is materially inconsistent with this Agreement, (ii) amend, supplement, modify, or terminate any material

agreement in a way that is materially inconsistent with this Agreement, (iii) knowingly allow any material agreement to expire

if such expiration would frustrate or impede consummation of the Restructuring Transactions, or (iv) knowingly allow any material

permit, license or regulatory approval to lapse, expire, terminate or be revoked, suspended or modified, in each case without

the prior written consent of the Required Consenting Stakeholders (which may be by email);

(j) file

with any court any motion, pleading, or Definitive Document (including any modifications or amendments thereto) that, in whole

or in part, is materially inconsistent with this Agreement;

(k) (i)

operate its business outside the ordinary course, other than the Restructuring Transactions, or (ii) other than in the ordinary

course of business or as contemplated by this Agreement transfer any material asset or right of the Company Parties (or its Affiliates)

or any material asset or right used in the business of the Company Parties (or its Affiliates) to any person or entity;

(l) other

than in the ordinary course of business or as contemplated by this Agreement engage in any material merger, consolidation, disposition,

acquisition, investment, dividend, incurrence of indebtedness, or other similar transaction; or

| Section

7. | Additional

Provisions Regarding Company Parties’ Commitments. |

7.01. Notwithstanding

anything to the contrary in this Agreement, nothing in this Agreement shall require a Company Party or the board of directors,

board of managers, or similar governing body of a Company Party, after consulting with counsel, to take any action or to refrain

from taking any action with respect to the Restructuring Transactions to the extent taking or failing to take such action would

be inconsistent with applicable Law or its fiduciary obligations under applicable Law, and any such action or inaction pursuant

to this Section 7.01 shall not be deemed to constitute a breach of this Agreement. The Company Parties shall give prompt written

notice to counsel to the Consenting Stakeholders within two (2) calendar days of any determination made in accordance with this

Section 7.01 to take any action or refrain from taking any inaction. Notwithstanding anything to the contrary herein, each Consenting

Term Loan Lender reserves its rights to challenge any action taken or not taken by any Company Party in the exercise of its fiduciary

obligations.

7.02. Notwithstanding

anything to the contrary in this Agreement (but subject to Section 7.01), each Company Party and their respective directors, officers,

employees, investment bankers, attorneys, accountants, consultants, and other advisors or representatives shall have the rights

to: (a) consider, respond to, and facilitate Alternative Restructuring Proposals that are unsolicited or received as part of the

PWP Marketing Process; (b) provide access to non-public

information

concerning any Company Party to any Entity or enter into Confidentiality Agreements or nondisclosure agreements with any Entity;

(c) maintain or continue discussions or negotiations with respect to Alternative Restructuring Proposals that are unsolicited

or received as part of the PWP Marketing Process; (d) otherwise cooperate with, assist, participate in, or facilitate any inquiries,

proposals, discussions, or negotiation of Alternative Restructuring Proposals that are unsolicited or received as part of the

PWP Marketing Process; and (e) enter into or continue discussions or negotiations with holders of Claims against or Equity Interests

in a Company Party (including any Consenting Stakeholder), any other party in interest in the Chapter 11 Cases (including any

official committee and the U.S. Trustee), or any other Entity regarding the Restructuring Transactions or Alternative Restructuring

Proposals, provided that (x) if any Company Party receives an Alternative Restructuring Proposal, then such Company Party shall

within two (2) calendar days of receiving such proposal, notify the Required Consenting Term Loan Advisor of the receipt of such

proposal (email being sufficient) (y) provide the Required Consenting Term Loan Advisor with regular updates as to the status

and progress of such Alternative Restructuring Proposal; and (z) use commercially reasonable efforts to respond promptly to reasonable

information requests and questions from the Required Consenting Term Loan Advisor relating to such Alternative Restructuring Proposal.

7.03. Nothing

in this Agreement shall: (a) impair or waive the rights of any Company Party to assert or raise any objection permitted under

this Agreement in connection with the Restructuring Transactions; or (b) prevent any Company Party from enforcing this Agreement

or contesting whether any matter, fact, or thing is a breach of, or is inconsistent with, this Agreement.

| Section

8. | Transfer

of Equity Interests and Securities. |

8.01. During

the Agreement Effective Period, no Consenting Stakeholder shall Transfer any ownership (including any beneficial ownership as

defined in Rule 13d-3 under the Securities Exchange Act of 1934) in any Company Claims/Equity Interests to any affiliated or unaffiliated

party, including any party in which it may hold a direct or indirect beneficial interest, unless:

(a) in

the case of any Company Claims/Equity Interests, the authorized transferee is either (i) a qualified institutional buyer as

defined in Rule 144A of the Securities Act, (ii) a non-U.S. person in an offshore transaction as defined under Regulation S

under the Securities Act, (iii) an institutional accredited investor (as defined in the Rules), or (iv) a Consenting

Stakeholder;

(b) either

(i) the transferee executes and delivers to counsel to the Company Parties, at or before the time of the proposed Transfer, a

Transfer Agreement or (ii) the transferee is a Consenting Stakeholder and the transferee provides notice of such Transfer (including

the amount and type of Company Claim/Equity Interest transferred) to counsel to the Company Parties at or before the time of the

proposed Transfer; and

(c) such

Transfer shall not violate the terms of any order entered by the Bankruptcy Court with respect to preservation of net operating

losses.

8.02. Upon

compliance with the requirements of Section 8.01, the transferor shall be deemed to relinquish its rights (and be released from

its obligations) under this Agreement to the extent of the rights and obligations in respect of such transferred Company Claims/Equity

Interests

and

the transferee shall be deemed to be a Consenting Stakeholder and a Party for all purposes under this Agreement and all of the

Company Claims/Equity Interests then held (and subsequently acquired) by such transferee shall be subject to this Agreement.

8.03. This

Agreement shall in no way be construed to preclude the Consenting Stakeholders from acquiring additional Company Claims/Equity

Interests; provided, however, that (a) such additional Company Claims/Equity Interests shall automatically and immediately

upon acquisition by a Consenting Stakeholder be deemed subject to the terms of this Agreement (regardless of when or whether notice