| Copyright © 2023 First Foundation Inc. All Rights Reserved

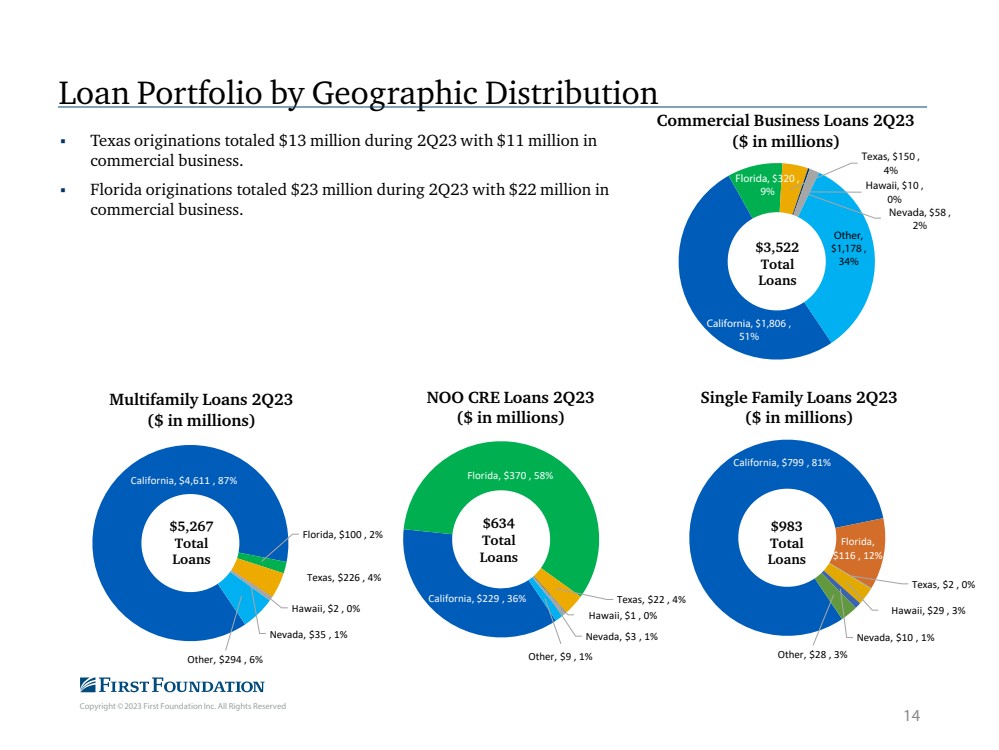

California, $799 , 81%

Florida,

$116 , 12%

Texas, $2 , 0%

Hawaii, $29 , 3%

Nevada, $10 , 1%

Other, $28 , 3%

Single Family Loans 2Q23

($ in millions)

California, $4,611 , 87%

Florida, $100 , 2%

Texas, $226 , 4%

Hawaii, $2 , 0%

Nevada, $35 , 1%

Other, $294 , 6%

Multifamily Loans 2Q23

($ in millions)

California, $229 , 36%

Florida, $370 , 58%

Texas, $22 , 4%

Hawaii, $1 , 0%

Nevada, $3 , 1%

Other, $9 , 1%

NOO CRE Loans 2Q23

($ in millions)

California, $1,806 ,

51%

Florida, $320 ,

9%

Texas, $150 ,

4%

Hawaii, $10 ,

0%

Nevada, $58 ,

2%

Other,

$1,178 ,

34%

Commercial Business Loans 2Q23

($ in millions)

Loan Portfolio by Geographic Distribution

$5,267

Total

Loans

14

$634

Total

Loans

$983

Total

Loans

$3,522

Total

Loans

Texas originations totaled $13 million during 2Q23 with $11 million in

commercial business.

Florida originations totaled $23 million during 2Q23 with $22 million in

commercial business. |