UNITED STATES

SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C.

20549

FORM 6-K

REPORT OF FOREIGN

ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

SECURITIES EXCHANGE

ACT OF 1934

For the month of November,

2024

(Commission File

No. 001-34429),

PAMPA ENERGIA S.A.

(PAMPA ENERGY INC.)

Argentina

(Jurisdiction of

incorporation or organization)

Maipú 1

C1084ABA

City of Buenos Aires

Argentina

(Address of principal

executive offices)

(Indicate by check

mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

Form 20-F ___X___ Form 40-F ______

(Indicate

by check mark whether the registrant by furnishing the

information contained in this form is also thereby furnishing the

information to the Commission pursuant to Rule 12g3-2(b) under

the Securities Exchange Act of 1934.)

Yes ______ No ___X___

(If "Yes"

is marked, indicate below the file number assigned to the

registrant in connection with Rule 12g3-2(b): 82- .)

This Form 6-K

for Pampa Energía S.A. (“Pampa” or the “Company”) contains:

Exhibit

1: Earnings Release Q3 24

SIGNATURE

Pursuant to the requirements of the Securities

Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly

authorized.

Date: November 5, 2024

| Pampa Energía S.A. |

| |

|

|

| |

|

|

| By: |

/s/ Gustavo Mariani

|

|

| |

Name: Gustavo Mariani

Title: Chief Executive Officer |

|

FORWARD-LOOKING

STATEMENTS

This press release may contain

forward-looking statements. These statements are statements that are not historical facts, and are based on management's current

view and estimates offuture economic circumstances, industry conditions, company performance and financial results. The words "anticipates",

"believes", "estimates", "expects", "plans" and similar expressions, as they relate to

the company, are intended to identify forward-looking statements. Statements regarding the declaration or payment of dividends,

the implementation of principal operating and financing strategies and capital expenditure plans, the direction of future operations

and the factors or trends affecting financial condition, liquidity or results of operations are examples of forward-looking statements.

Such statements reflect the current views of management and are subject to a number of risks and uncertainties. There is no guarantee

that the expected events, trends or results will a ctually occur. The statements are based on many assumptions and factors, including

general economic and market conditions, industry conditions, and operating factors. Any changes in such assumptions or factors

could cause actual results to differ materially from current expectations.

Pampa

Energía, an independent company with active participation in the Argentine electricity,

oil and gas value chain, announces the results for the nine-month period and quarter ended

on September 30, 2024. |

Buenos

Aires, November 6, 2024

Stock information

Share capital

as of November 5, 2024

1,363.5 million common shares/

54.5 million ADS

Market capitalization

AR$4,377 billion/

US$3,692 million

Information about the videoconference

Date and time

Thursday November 7

10 AM Eastern Standard Time

12 AM Buenos Aires Time

Access link

bit.ly/Pampa3Q2024VC

For further information

about Pampa

Email

investor@pampa.com

Website for investors

ri.pampa.com

Argentina’s Securities

and Exchange Commission

www.argentina.gob.ar/cnv

Securities and

Exchange Commission

sec.gov

|

|

Basis

of presentation

Pampa’s

financial information adopts US$ as functional currency, converted into AR$ at transactional FX. However, Transener and TGS adjust their

figures for inflation as of September 30, 2024, which are expressed in US$ at the period’s closing FX. The previously reported

figures remain unchanged.

Q3

24 main results[1]

14%

year-on-year sales increase in Q3 24, reaching US$540 million[2],

driven by increased gas production in line with the last Plan Gas round, improved availability, dispatch and prices in power generation,

and higher reforming volumes. These effects were partially offset by lower gas sales to industries and Chile, reforming prices and local

petchem sales.

Operational

KPIs in power generation and

gas production outperformed

during the winter peak demand:

Adjusted

EBITDA[3] was US$279 million in Q3 24, 14% higher than Q3 23, mainly

explained by increased deliveries under Plan Gas, power generation and our stakes at Transener and TGS, offset by petrochemicals and

operating costs.

Net

profit to the Company’s shareholders of US$146 million, a 4% decline from Q3 23,

due to lower gains from financial securities and lesser devaluation over the monetary active position in AR$, partially offset by lesser

financial expenses and income tax, and improvements in the operating margin.

Net

debt decreased US$150 million vs. June 2024, to US$539 million, the lowest amount and ratio in the last 8 years, explained by the operating cash flow of core businesses and improved collections.

|

1

The information is based on FS prepared according to IFRS in force in Argentina.

2 Sales from the affiliates CTBSA, Transener and TGS are excluded, shown as ‘Results for participation in joint businesses

and associates.’

3 Consolidated adjusted EBITDA represents

the flows before financial items, income tax, depreciations and amortizations, extraordinary and non-cash income and expense, equity

income, and includes affiliates’ EBITDA at our ownership. Further information on section 3.1.

| |

| Pampa Energía ● Earnings release Q3 24 ● 1 |

1.

Relevant Events

1.1

Tender offer for 2027 Notes and international placement of 2031 Notes

On

August 26, 2024, Pampa’s Board of Directors approved the repurchase at par value of the 2027 Notes for US$750 million of face value,

7.5% fixed rate and maturing in January 2027. The tender ended on September 5, 2024, participating approximately 53% of the total, equivalent

to US$397 million.

The

funds for the tender came from the successful placement of the 2031 Notes for US$410 million at a 7.95% annual fixed rate and 8.25% yield,

maturing on September 10, 2031. The issuance received offers exceeding US$1.6 billion from international institutional investors. This

transaction strengthens Pampa’s debt profile, paving the way for the upcoming investments in Vaca Muerta, especially in developing

the Rincón de Aranda shale oil block.

1.2

Power generation segment

Partial

commissioning of PEPE 6

In

September 2024, 7 Vestas wind turbines were commissioned, adding 31.5 MW. On October 11, 2024, 4 more were commissioned for 18 MW. Hence,

25 of the 31 wind turbines are commissioned, with a total capacity of 112.5 MW.

All

the wind turbines and civil works were finished in October. PEPE 6 is estimated to be fully online and reach a total capacity of 140

MW by November 2024. With this investment of approximately US$250 million, Pampa has 427 MW of total installed wind power capacity, ranking

as one of the country’s leading renewable power producers.

2024-2026

contingency plan

On

October 1, 2024, the SE established a plan to face the energy system’s critical situation during the seven months of peak demand

(December to March and June to August) (Res. No. 294/24). The plan includes a voluntary participation scheme that recognizes an additional

remuneration, effective from December 2024 to March 2026. Pampa is analyzing participation in the said scheme.

| • |

Fixed

additional remuneration of US$2,000/MW-month for the capacity, adjusted by a criticality factor based on the node where the unit

is located and its availability during peak demand hours[4]. |

| • |

Variable

additional remuneration in US$/MWh for power generation during peak demand periods, based on the type of fuel used, generation

technology, and a criticality factor: |

| Technology |

Natural gas |

Fuel Oil |

Gas Oil |

Biofuel |

Coal |

| GT |

6.4 |

- |

8.6 |

8.7 |

- |

| ST |

3.4 |

6.0 |

- |

8.7 |

10.4 |

| Engines |

8.1 |

15.4 |

10.5 |

8.7 |

- |

4

Ranges between nodes with high (1.25), medium (1.00), and low (0.75) criticality, and between summer and winter.

| |

| Pampa Energía ● Earnings release Q3 24 ● 2 |

Updates

for the spot remuneration scheme

| Effective as of: |

Spot

energy remuneration |

| Increase |

Resolution |

| September |

5% |

SE

No. 233/24 |

| October |

2.7% |

SE

No. 285/24 |

| November |

6% |

SCEyM

No. 20/24 |

License

expiration and transition period at Mendoza hydros

On

October 19, 2024, the HIDISA license concessions were scheduled to expire, one for the assets and water usage granted by the Province

of Mendoza and another for the power generation granted by the National Government. Pampa holds 61% of HIDISA’s share capital.

On

October 18, 2024, the Government of Mendoza set a 12-month transition period starting from the expiration date, appointing the Undersecretary

of Energy and Mining as observer (Decree No. 2,096/24). Additionally, the National Coordination Secretary of Energy and Mining set the

transition period until June 1, 2025, and appointed the SSEE as observer (Res. SCEyM No. 1/24).

The transition period at HINISA expires on November 30,

2024. Pampa sent a letter to the SE seeking guidance on the next steps.

1.3

Increases in regulated tariffs

Natural

gas

On

August 29, 2024, the SE adjusted the PIST values for natural gas from September 2024 (Res. SE No. 232/24). Later, on September 27, 2024,

an additional reduction was applied, effective from October 2024 (Res. SE No. 284/24):

| Demand segment |

September

2024 |

|

As

of October 2024 |

| Subsidized price |

Price

without subsidy |

|

Subsidized price |

Price

without subsidy |

| High-income

residential (N1) and businesses and industries |

n.a. |

US$3.4

per

MBTU |

|

n.a. |

US$3.1

per MBTU |

| Low-income

residential/social tariff (N2) |

US$1.2

per MBTU |

|

US$1.1

per MBTU |

| Middle

income residential (N3) |

US$1.5

per MBTU |

|

US$1.4

per MBTU |

Note:

Consumption exceeding the cap for N2 and N3, which varies according to consumption range, distributor, and zone, will be valued at

N1 price without any discount.

Cost

variations

| Effective as of: |

Transener |

|

TGS |

| Increase |

Resolution |

|

Increase |

Resolution |

| September |

6% |

ENRE

N° 580 y 581/24 |

|

1% |

ENARGAS

N° 491/24 |

| October |

2.7% |

ENRE

N° 692 y 696/24 |

|

2.7% |

ENARGAS

N° 601/24 |

| November |

6% |

ENRE

N° 901 y 902/24 |

|

3.5% |

ENARGAS

N° 735/24 |

| |

| Pampa Energía ● Earnings release Q3 24 ● 3 |

1.4

Acquisition of OCP Ecuador shares and end of concession

On

August 30, 2024, Pampa acquired the remaining 36% of OCP Ecuador, where it already held 64% of the capital, for US$23 million. With this

transaction, Pampa became the sole owner of OCP Ecuador and began consolidating the company in its FS.

OCP

Ecuador operates the country’s main private pipeline, extending 485 kilometers and transporting an average of 150 thousand barrels

of Ecuadorian crude daily, approximately 30% of national production, along with 10 thousand barrels per day of Colombian oil.

The OCP concession has been extended for three months until

November 30, 2024, when the shares must be transferred to the Ecuadorian State. OCP Ecuador is working with the authorities to carry out

the transition per the provisions of the concession contract.

| 1.5 Sale of stake in Gobernador Ayala | |

On October 21, 2024, Pampa transferred its 22.51% stake in the hydrocarbon exploitation license and joint operatorship at the Gobernador Ayala block to Pluspetrol for $23 million.

Public

hearing for the tenure extension of the gas transportation license

On

October 21, 2024, ENARGAS held a public hearing to discuss the tenure extension of TGS’s license for natural gas transportation,

expiring in December 2027. The original contract allowed for a 10-year extension, but the Ley Bases, passed in July 2024, enables

an extension of up to 20 years until December 2047.

Conditioning

capacity expansion at Tratayén

In

October 2024, the construction and commissioning of the first natural gas conditioning module at TGS’s Tratayén Plant was

completed, increasing its capacity by 6.6 million m3 per day. The second module, adding another 6.6 million m3,

is expected to be online by the end of 2024. This investment of approximately US$350 million will enable the plant to reach a total conditioning

capacity of 28 million m3 per day.

| |

| Pampa Energía ● Earnings release Q3 24 ● 4 |

2.

Financial highlights

2.1

Consolidated balance sheet

| Figures in million |

|

As of 09.30.2024 |

|

As of 12.31.2023 |

| |

AR$ |

US$ FX 970.5 |

|

AR$ |

US$ FX 808.45 |

| ASSETS |

|

|

|

|

|

|

| Property, plant and equipment |

|

2,499,436 |

2,575 |

|

2,056,974 |

2,544 |

| Intangible assets |

|

94,114 |

97 |

|

77,898 |

96 |

| Right-of-use assets |

|

12,153 |

13 |

|

17,259 |

21 |

| Deferred tax asset |

|

101,466 |

105 |

|

2 |

0 |

| Investments in joint ventures and associates |

|

918,879 |

947 |

|

542,978 |

672 |

| Financial assets at fair value through profit and loss |

|

26,451 |

27 |

|

28,040 |

35 |

| Other assets |

|

1,722 |

2 |

|

349 |

0 |

| Trade and other receivables |

|

43,103 |

44 |

|

14,524 |

18 |

| Total non-current assets |

|

3,697,324 |

3,810 |

|

2,738,024 |

3,387 |

| |

|

|

|

|

|

|

| Inventories |

|

231,400 |

238 |

|

166,023 |

205 |

| Financial assets at amortized cost |

|

77,881 |

80 |

|

84,749 |

105 |

| Financial assets at fair value through profit and loss |

|

750,900 |

774 |

|

451,883 |

559 |

| Derivative financial instruments |

|

108 |

0 |

|

250 |

0 |

| Trade and other receivables |

|

598,582 |

617 |

|

238,294 |

295 |

| Cash and cash equivalents |

|

322,011 |

332 |

|

137,973 |

171 |

| Total current assets |

|

1,980,882 |

2,041 |

|

1,079,172 |

1,335 |

| |

|

|

|

|

|

|

| Total assets |

|

5,691,563 |

5,865 |

|

3,817,196 |

4,722 |

| |

|

|

|

|

|

|

| EQUITY |

|

|

|

|

|

|

| Equity attributable to owners of the company |

|

3,092,655 |

3,187 |

|

1,943,736 |

2,404 |

| |

|

|

|

|

|

|

| Total equity |

|

3,100,822 |

3,195 |

|

1,950,696 |

2,413 |

| |

|

|

|

|

|

|

| LIABILITIES |

|

|

|

|

|

|

| Provisions |

|

183,254 |

189 |

|

119,863 |

148 |

| Income tax and presumed minimum income tax liabilities |

|

71,282 |

73 |

|

44,614 |

55 |

| Deferred tax liabilities |

|

48,121 |

50 |

|

240,686 |

298 |

| Defined benefit plans |

|

40,976 |

42 |

|

13,172 |

16 |

| Borrowings |

|

1,368,963 |

1,411 |

|

989,182 |

1,224 |

| Trade and other payables |

|

49,286 |

51 |

|

37,301 |

46 |

| Total non-current liabilities |

|

1,761,882 |

1,815 |

|

1,444,818 |

1,787 |

| |

|

|

|

|

|

|

| Provisions |

|

8,720 |

9 |

|

4,649 |

6 |

| Income tax liabilities |

|

199,094 |

205 |

|

14,026 |

17 |

| Taxes payables |

|

47,984 |

49 |

|

11,427 |

14 |

| Defined benefit plans |

|

12,148 |

13 |

|

2,695 |

3 |

| Salaries and social security payable |

|

29,187 |

30 |

|

15,537 |

19 |

| Derivative financial instruments |

|

2 |

0 |

|

191 |

0 |

| Borrowings |

|

305,312 |

315 |

|

181,357 |

224 |

| Trade and other payables |

|

225,170 |

232 |

|

191,800 |

237 |

| Total current liabilities |

|

827,617 |

853 |

|

421,682 |

522 |

| |

|

|

|

|

|

|

| Total liabilities |

|

2,590,741 |

2,669 |

|

1,866,500 |

2,309 |

| |

|

|

|

|

|

|

| Total liabilities and equity |

|

5,691,563 |

5,865 |

|

3,817,196 |

4,722 |

| |

| Pampa Energía ● Earnings release Q3 24 ● 5 |

2.2

Consolidated income statement

| |

|

Nine-month period |

|

Third quarter |

| Figures in million |

|

2024 |

|

2023 |

|

2024 |

|

2023 |

| |

|

AR$ |

US$ |

|

AR$ |

US$ |

|

AR$ |

US$ |

|

AR$ |

US$ |

| Sales revenue |

|

1,294,494 |

1,441 |

|

346,957 |

1,370 |

|

510,706 |

540 |

|

152,701 |

475 |

| Domestic sales |

|

1,086,342 |

1,207 |

|

285,892 |

1,117 |

|

437,156 |

465 |

|

131,583 |

409 |

| Foreign market sales |

|

208,152 |

234 |

|

61,065 |

253 |

|

73,550 |

75 |

|

21,118 |

66 |

| Cost of sales |

|

(831,719) |

(930) |

|

(209,953) |

(850) |

|

(344,291) |

(365) |

|

(92,014) |

(295) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Gross profit |

|

462,775 |

511 |

|

137,004 |

520 |

|

166,415 |

175 |

|

60,687 |

180 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Selling expenses |

|

(51,380) |

(57) |

|

(13,333) |

(51) |

|

(19,798) |

(21) |

|

(5,610) |

(17) |

| Administrative expenses |

|

(124,840) |

(139) |

|

(34,629) |

(133) |

|

(53,166) |

(56) |

|

(14,427) |

(44) |

| Exploration expenses |

|

(256) |

- |

|

(1,772) |

(7) |

|

(89) |

- |

|

(22) |

- |

| Other operating income |

|

102,716 |

116 |

|

31,627 |

115 |

|

31,935 |

33 |

|

17,338 |

54 |

| Other operating expenses |

|

(63,966) |

(72) |

|

(18,079) |

(68) |

|

(20,912) |

(20) |

|

(10,704) |

(33) |

| Impairment of financial assets |

|

(48,912) |

(56) |

|

(415) |

(4) |

|

680 |

- |

|

(116) |

(1) |

| Impairment on PPE, int. assets & inventories |

|

(18,578) |

(19) |

|

(324) |

(1) |

|

(18,436) |

(19) |

|

(1) |

- |

| Results for part. in joint businesses & associates |

|

94,331 |

101 |

|

14,044 |

42 |

|

62,437 |

62 |

|

5,474 |

8 |

| Income from the sale of associates |

|

5,765 |

7 |

|

486 |

1 |

|

- |

- |

|

486 |

1 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Operating income |

|

357,655 |

392 |

|

114,609 |

414 |

|

149,066 |

154 |

|

53,105 |

148 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Financial income |

|

4,095 |

4 |

|

1,090 |

4 |

|

2,086 |

2 |

|

662 |

2 |

| Financial costs |

|

(120,932) |

(137) |

|

(71,096) |

(283) |

|

(39,244) |

(43) |

|

(30,018) |

(95) |

| Other financial results |

|

99,806 |

114 |

|

95,794 |

392 |

|

36,945 |

40 |

|

40,333 |

138 |

| Financial results, net |

|

(17,031) |

(19) |

|

25,788 |

113 |

|

(213) |

(1) |

|

10,977 |

45 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Profit before tax |

|

340,624 |

373 |

|

140,397 |

527 |

|

148,853 |

153 |

|

64,082 |

193 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Income tax |

|

111,715 |

140 |

|

(20,437) |

(69) |

|

(9,451) |

(7) |

|

(13,350) |

(40) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Net income for the period |

|

452,339 |

513 |

|

119,960 |

458 |

|

139,402 |

146 |

|

50,732 |

153 |

| Attributable to the owners of the Company |

|

452,630 |

513 |

|

119,708 |

457 |

|

139,470 |

146 |

|

50,611 |

152 |

| Attributable to the non-controlling interest |

|

(291) |

- |

|

252 |

1 |

|

(68) |

- |

|

121 |

1 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Net income per share to shareholders |

|

332.8 |

0.4 |

|

87.5 |

0.3 |

|

102.6 |

0.1 |

|

37.2 |

0.1 |

| Net income per ADR to shareholders |

|

8,320.4 |

9.4 |

|

2,187.6 |

8.4 |

|

2,563.8 |

2.7 |

|

930.4 |

2.8 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Average outstanding common shares1 |

|

1,360 |

1,360 |

|

1,368 |

1,368 |

|

1,360 |

1,360 |

|

1,360 |

1,360.0 |

| Outstanding shares by the end of period1 |

|

1,360 |

1,360 |

|

1,360 |

1,360 |

|

1,360 |

1,360 |

|

1,360 |

1,360.0 |

Note:

1 It considers the Employee stock-based compensation plan shares, which amounted to 3.9 million common shares as of September 30,

2023 and 2024.

| |

| Pampa Energía ● Earnings release Q3 24 ● 6 |

2.3

Cash and financial borrowings

| |

As of September 30, 2024,

in US$ million |

|

Cash1 |

|

Financial debt |

|

Net debt |

| |

|

Consolidated

in FS |

Ownership adjusted |

|

Consolidated

in FS |

Ownership adjusted |

|

Consolidated

in FS |

Ownership adjusted |

| |

| |

Power generation |

|

963 |

958 |

|

544 |

544 |

|

(419) |

(414) |

| |

Petrochemicals |

|

- |

- |

|

- |

- |

|

- |

- |

| |

Holding and others |

|

82 |

82 |

|

11 |

11 |

|

(71) |

(71) |

| |

Oil and gas |

|

141 |

141 |

|

1,171 |

1,171 |

|

1,029 |

1,029 |

| |

Total under IFRS/Restricted Group |

|

1,186 |

1,181 |

|

1,725 |

1,725 |

|

539 |

544 |

| |

Affiliates at O/S2 |

|

213 |

213 |

|

273 |

273 |

|

60 |

60 |

| |

Total with affiliates |

|

1,399 |

1,394 |

|

1,998 |

1,998 |

|

599 |

604 |

Note:

Financial debt includes accrued interest. 1 It includes cash and cash equivalents, financial assets at fair value with changing

results, and investments at amortized cost. 2 Under IFRS, the affiliates CTBSA, Transener and TGS are not consolidated in Pampa.

Debt

transactions

As

of September 30, 2024, Pampa’s financial debt under IFRS amounted to US$1,725 million, 19% higher than the end of 2023, mainly

due to the international issuance of the 2031 Notes, partially offset by the

repurchase of the 2027 Notes. However, net debt decreased to US$539 million,

the lowest amount in the last 8 years, explained by the contributions of operating cash flow from power and E&P businesses and improved

collections from CAMMESA and ENARSA.

The

table below shows the gross debt principal breakdown:

| Currency |

Type of

issuance |

Amount

in million US$ |

Legislation |

% over

total gross debt |

Avg coupon |

| US$ |

US$1 |

1,255 |

Foreign |

73% |

8.3%, primarily fixed |

| US$ Cable |

215 |

Argentine |

13% |

4.2% |

| US$ MEP |

128 |

Argentine |

7% |

5% |

| AR$ |

AR$ |

23 |

Argentine |

1% |

37.4%, variable |

| US$-link |

98 |

Argentine |

6% |

0% |

With

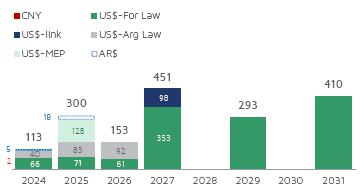

the issuance of the 2031 Notes, the financial debt increased its average life to 3.4 years. The chart below shows the principal maturity

profile, net of repurchases, in US$ million by the end of Q3 24:

|

Note:

The chart only considers Pampa consolidated under IFRS. It does not include affiliates TGS, Transener, and CTBSA. |

| |

| Pampa Energía ● Earnings release Q3 24 ● 7 |

During

Q3 24, Pampa issued the Series 21 CB for US$410 million, at an interest rate of 7.95%, maturing in September 2031, and repurchased in

cash at par value its Series 1 CB for US$397 million, remaining an outstanding amount of US$353 million of face value. After the quarter’s

closing, Pampa issued the Series 22 CB for US$84 million at an interest rate of 5.75%, maturing in October 2028, and canceled US$47 million

from the Series 20 CB, remaining an outstanding amount of US$60 million.

Regarding

our affiliates, in Q3 24, TGS issued its Series 3 CB for US$490 million, at an interest rate of 8.5%, maturing in July 2031, and redeemed

the total outstanding of its 2025 Notes for US$470 million. In addition, TGS took short-term borrowings for US$5 million and paid import

financing equivalent to US$2 million. CTEB paid short-term net bank borrowings for AR$20,496 million and took borrowings for US$10 million.

After the quarter’s closing, CTEB took borrowings for US$57 million and canceled its Series 4 CB for US$96 million.

As

of this report’s issuance date, we comply with the covenants established in our debt agreements.

Summary

of debt securities

Company

In million |

Security |

Maturity |

Amount issued |

Amount

net of repurchases |

Coupon |

| In US$-Foreign Law |

|

|

|

|

|

| Pampa |

CB Series 9 at par & fixed rate |

2026 |

293 |

179 |

9.5% |

| CB Series 1 at discount & fixed rate |

2027 |

750 |

353 |

7.5% |

| CB Series 3 at discount & fixed rate |

2029 |

300 |

293 |

9.125% |

| CB Series 21 at discount & fixed rate |

2031 |

410 |

410 |

7.950% |

| TGS1 |

CB at discount at fixed rate |

2031 |

490 |

490 |

8.50% |

| |

|

|

|

|

|

| In US$-Argentine Law |

|

|

|

|

|

| Pampa |

CB Series 20 |

2026 |

108 |

60 |

6.00% |

| |

|

|

|

|

|

| In US$-link |

|

|

|

|

|

| Pampa |

CB Series 13 |

2027 |

98 |

98 |

0% |

| CTEB1 |

CB Series 6 |

2025 |

84 |

84 |

0% |

| CB Series 9 |

2026 |

50 |

50 |

0% |

| |

|

|

|

|

|

| In US$-MEP |

|

|

|

|

|

| Pampa |

CB Series 16 |

2025 |

56 |

56 |

4.99% |

| CB Series 18 |

2025 |

72 |

72 |

5.00% |

| CB Series 22 |

2028 |

84 |

84 |

5.75% |

| In AR$ |

|

|

|

|

|

| Pampa |

CB Series 19 |

2025 |

17,131 |

17,131 |

Badlar Privada -1% |

Notes:

1 According to IFRS, affiliates are not consolidated in Pampa’s FS. 2 Series 4 CB from CTEB was canceled after Q3

24 closing.

3 Series 22 CB from Pampa was issued after the Q3 24 closing.

| |

| Pampa Energía ● Earnings release Q3 24 ● 8 |

Credit

ratings

| Company |

Agency |

Rating |

| Global |

Local |

| Pampa |

S&P |

b-1 |

na |

| Moody's |

Caa3 |

na |

| FitchRatings2 |

B- |

AA+ (long-term)

A1+ (short-term) |

| TGS |

S&P |

CCC |

na |

| Moody's |

Caa3 |

na |

| FitchRatings |

B- |

na |

| Transener |

FitchRatings2 |

na |

A+ (long-term) |

| CTEB |

FitchRatings2 |

na |

AA- |

Note:

1 Stand-alone. 2 Local ratings issued by FIX SCR.

| |

| Pampa Energía ● Earnings release Q3 24 ● 9 |

3.

Analysis of the Q3 24 results

Breakdown by segment

Figures in US$ million |

Q3 24 |

Q3 23 |

Variation |

| Sales |

Adjusted EBITDA |

Net Income |

Sales |

Adjusted EBITDA |

Net Income |

Sales |

Adjusted EBITDA |

Net Income |

| |

|

|

|

|

|

|

|

|

|

| Power generation |

183 |

112 |

95 |

163 |

91 |

110 |

+12% |

+23% |

-14% |

| Oil and Gas |

228 |

122 |

(4) |

207 |

132 |

2 |

+10% |

-8% |

NA |

| Petrochemicals |

140 |

2 |

7 |

132 |

16 |

15 |

+6% |

-88% |

-53% |

| Holding and Others |

19 |

43 |

48 |

3 |

6 |

25 |

NA |

NA |

+92% |

| Eliminations |

(30) |

- |

- |

(30) |

- |

- |

- |

NA |

NA |

| |

|

|

|

|

|

|

|

|

|

| Total |

540 |

279 |

146 |

475 |

244 |

152 |

+14% |

+14% |

-4% |

Note:

Net income attributable to the Company’s shareholders.

3.1

Reconciliation of consolidated adjusted EBITDA

Reconciliation of adjusted EBITDA,

in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

|

2024 |

2023 |

| Consolidated operating income |

|

392 |

414 |

|

154 |

148 |

| Consolidated depreciations and amortizations |

|

257 |

203 |

|

105 |

77 |

| Reporting EBITDA |

|

649 |

617 |

|

259 |

225 |

| |

|

|

|

|

|

|

| Adjustments from generation segment |

|

80 |

(5) |

|

7 |

1 |

| Adjustments from oil and gas segment |

|

5 |

(0) |

|

14 |

(1) |

| Adjustments from petrochemicals segment |

|

(0) |

3 |

|

(0) |

(0) |

| Adjustments from holding & others segment |

|

20 |

57 |

|

(1) |

20 |

| |

|

|

|

|

|

|

| Consolidated adjusted EBITDA |

|

754 |

672 |

|

279 |

244 |

| At our ownership |

|

753 |

673 |

|

279 |

245 |

| |

| Pampa Energía ● Earnings release Q3 24 ● 10 |

3.2

Analysis of the power generation segment

Power generation segment, consolidated

Figures in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

∆% |

|

2024 |

2023 |

∆% |

| Sales revenue |

|

505 |

507 |

-0% |

|

183 |

163 |

+12% |

| Cost of sales |

|

(260) |

(275) |

-5% |

|

(102) |

(94) |

+9% |

| |

|

|

|

|

|

|

|

|

| Gross profit |

|

245 |

232 |

+6% |

|

81 |

69 |

+17% |

| |

|

|

|

|

|

|

|

|

| Selling expenses |

|

(2) |

(1) |

+100% |

|

(1) |

- |

NA |

| Administrative expenses |

|

(39) |

(38) |

+3% |

|

(14) |

(12) |

+17% |

| Other operating income |

|

34 |

50 |

-32% |

|

2 |

15 |

-87% |

| Other operating expenses |

|

(11) |

(24) |

-54% |

|

(4) |

(10) |

-60% |

| Impairment of financial assets |

|

(46) |

- |

NA |

|

- |

- |

NA |

| Results for participation in joint businesses |

|

(28) |

9 |

NA |

|

10 |

4 |

+150% |

| |

|

|

|

|

|

|

|

|

| Operating income |

|

153 |

228 |

-33% |

|

74 |

66 |

+12% |

| |

|

|

|

|

|

|

|

|

| Finance income |

|

3 |

2 |

+50% |

|

1 |

1 |

- |

| Finance costs |

|

(39) |

(92) |

-58% |

|

(11) |

(26) |

-58% |

| Other financial results |

|

102 |

221 |

-54% |

|

22 |

97 |

-77% |

| Financial results, net |

|

66 |

131 |

-50% |

|

12 |

72 |

-83% |

| |

|

|

|

|

|

|

|

|

| Profit before tax |

|

219 |

359 |

-39% |

|

86 |

138 |

-38% |

| |

|

|

|

|

|

|

|

|

| Income tax |

|

109 |

(48) |

NA |

|

9 |

(27) |

NA |

| |

|

|

|

|

|

|

|

|

| Net income for the period |

|

328 |

311 |

+5% |

|

95 |

111 |

-14% |

| Attributable to owners of the Company |

|

328 |

310 |

+6% |

|

95 |

110 |

-14% |

| Attributable to non-controlling interests |

|

- |

1 |

-100% |

|

- |

1 |

-100% |

| |

|

|

|

|

|

|

|

|

| Adjusted EBITDA |

|

304 |

297 |

+2% |

|

112 |

91 |

+23% |

| Adjusted EBITDA at our share ownership |

|

304 |

298 |

+2% |

|

112 |

91 |

+23% |

| |

|

|

|

|

|

|

|

|

| Increases in PPE |

|

67 |

192 |

-65% |

|

24 |

46 |

-48% |

| Depreciation and amortization |

|

71 |

74 |

-4% |

|

31 |

24 |

+29% |

During

Q3 24, power generation sales increased

12% year-on-year, mainly due to higher legacy or spot energy prices from the AR$ increases that outpaced the devaluation, in addition

to outstanding operating performance with higher availability and load factor in spot and PPAs units. MATER sales also grew, thanks to

the gradual commissioning of PEPE 6. These effects were partially offset by lower Energía Plus demand due to the decline in industrial

activity and the divestment of PEMC in August 2023.

Additionally,

spot energy remuneration increases impacted

the CCGTs capacity payment, which also has a partial income in US$ (US$5.3 thousand per MW-month, +16% year-on-year and +11% vs. Q2 24).

For open cycles (GT and ST), the remuneration was equivalent to US$4.8 thousand per MW-month (+23% vs. Q3 23 and vs. Q2 24) and US$2.3

thousand per MW-month for hydros (+24% vs. Q3 23 and +15% vs. Q2 24).

Compared

to Q2 24, the increase of 9% in sales responds to better spot prices and higher thermal dispatch.

The

operating performance of

Pampa’s operated power generation grew by 19% vs. Q3 23, compared to a 3% year-on-year drop in national generation, because of

the lower availability of the grid’s power plants due to maintenance. This increase was mainly attributed to higher dispatch at

CTGEBA because of improved natural gas supply and overhauls in Q3 23 (+597 GWh), at CTEB (+173 GWh) and CTLL due to an outage in the

GT05 and overhauls in Q3 23 (+159 GWh). Lower water at HPPL (-148 GWh) and PEMC’s divestment (-97 GWh) partially offset these effects.

| |

| Pampa Energía ● Earnings release Q3 24 ● 11 |

The

availability of

Pampa’s operated units reached 96.2% in Q3 24, 244-basis points higher than Q3 23’s 93.7%, due to the outage at CTLL’s

GT05 and programmed overhauls at CTGEBA’s GT03 in Q3 23, that were offset by an outage at CTLL’s GT05 during August 2024.

Therefore, a 96.0% thermal availability rate was reached in Q3 24, 392 basis points higher than 92.1% from Q3 23.

Power generation's

key performance indicators |

|

2024 |

|

2023 |

|

Variation |

| Hydro |

Wind |

Thermal |

Total |

Hydro |

Wind |

Thermal |

Total |

Hydro |

Wind |

Thermal |

Total |

| Installed capacity (MW) |

|

938 |

382 |

4,107 |

5,426 |

|

938 |

287 |

4,107 |

5,332 |

|

- |

+33% |

- |

+2% |

| New capacity (%) |

|

- |

100% |

33% |

32% |

|

- |

100% |

33% |

31% |

|

- |

- |

- |

+1% |

| Market share (%) |

|

2.2% |

0.9% |

9.6% |

12.6% |

|

2.2% |

0.7% |

9.5% |

12.3% |

|

+0% |

+0% |

+0% |

+0% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Nine-month period |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net generation (GWh) |

|

1,641 |

839 |

14,467 |

16,947 |

|

1,249 |

913 |

13,800 |

15,963 |

|

+31% |

-8% |

+5% |

+6% |

| Volume sold (GWh) |

|

1,641 |

844 |

15,054 |

17,539 |

|

1,250 |

913 |

14,655 |

16,818 |

|

+31% |

-8% |

+3% |

+4% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average price (US$/MWh) |

|

15 |

72 |

35 |

35 |

|

19 |

72 |

35 |

35 |

|

-20% |

-1% |

+0% |

-2% |

| Average gross margin (US$/MWh) |

|

6 |

62 |

22 |

22 |

|

5 |

62 |

21 |

22 |

|

+9% |

-0% |

+5% |

+2% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Third quarter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net generation (GWh) |

|

540 |

337 |

5,074 |

5,951 |

|

596 |

316 |

4,073 |

4,985 |

|

-9% |

+7% |

+25% |

+19% |

| Volume sold (GWh) |

|

540 |

340 |

5,280 |

6,161 |

|

596 |

316 |

4,340 |

5,252 |

|

-9% |

+8% |

+22% |

+17% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average price (US$/MWh) |

|

17 |

72 |

35 |

36 |

|

14 |

72 |

39 |

38 |

|

+25% |

-1% |

-9% |

-5% |

| Average gross margin (US$/MWh) |

|

6 |

54 |

22 |

23 |

|

3 |

61 |

23 |

23 |

|

+99% |

-11% |

-3% |

-2% |

Note:

Gross margin before amortization and depreciation. It includes CTEB, operated by Pampa (co-operated by Pampa, 50% equity stake). PEMC

was de-consolidated in August 2023.

Excluding

depreciation and amortizations, net operating costs increased

by 14% to US$88 million vs. Q3 23, mainly explained by lower overdue interests from CAMMESA due to a drop in rates and days of sales

outstanding, and by gas and electricity transportation tariff increases. These effects were partially offset by lower power purchases

to cover contracts. Compared to Q2 24, operating costs rose 42% due to lower overdue interests from CAMMESA and higher maintenance expenses

and power purchases, partially offset by lower labor costs.

Financial

results in Q3 24 reached a net profit of US$12 million, 83% lower than Q3

23, mainly due to lower gains from financial instruments, offset by reduced financial interests because of lower AR$-debt stock and lesser

losses from FX differences, due to minor devaluation impact over AR$ trade receivables.

| Reconciliation of adjusted EBITDA from power generation, in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

|

2024 |

2023 |

| Consolidated operating income |

|

153 |

228 |

|

74 |

66 |

| Consolidated depreciations and amortizations |

|

71 |

74 |

|

31 |

24 |

| Reporting EBITDA |

|

224 |

302 |

|

105 |

90 |

| |

|

|

|

|

|

|

| Deletion of CTEB's equity income |

|

28 |

(9) |

|

(10) |

(4) |

| Deletion of commercial interests to CAMMESA |

|

(28) |

(41) |

|

(2) |

(12) |

| Deletion of CAMMESA's receivable impairment |

|

32 |

- |

|

- |

- |

| Deletion of PPE activation in operating expenses |

|

2 |

2 |

|

1 |

- |

| Deletion of provision in hydros |

|

5 |

6 |

|

2 |

1 |

| CTEB's EBITDA, at our 50% ownership |

|

41 |

37 |

|

16 |

16 |

| |

|

|

|

|

|

|

| Adjusted EBITDA from power generation |

|

304 |

297 |

|

112 |

91 |

Adjusted

EBITDA from the power generation segment was US$112 million, a 23% increase

year-on-year, boosted by the spot energy prices and operational outperformance, offset by higher operating expenses. Adjusted EBITDA

excludes non-operating, non-recurrent and non-cash items and considers CTEB’s 50% ownership, which posted US$16 million in Q3 24,

the same as in Q3 23.

| |

| Pampa Energía ● Earnings release Q3 24 ● 12 |

Finally,

without CTEB, capital expenditures registered

US$24 million in Q3 24 vs. US$46 million in Q3 23, explained by the completion of works in PEPE 4 (commissioned in Q4 23) and partially

offset by the last disbursements for PEPE 6, which is estimated to be fully operating by Q4 24. The PEPE 6 project is detailed below:

| Project |

MW |

Marketing |

Currency |

Awarded price |

|

Estimated capex in

US$ million1 |

Date of

commissioning |

Capacity per

MW-month |

Variable

per MWh |

Total

per MWh |

|

Budget |

% Executed

@09/30/24 |

| Renewable |

|

|

|

|

|

|

|

|

|

|

| Pampa Energía 6 |

139.5 |

MAT ER |

US$ |

na |

na |

62(2) |

|

269 |

72% |

Q4 2024 (est.) |

Note:

1 Without value-added tax. 2 Estimated average.

3.3

Analysis of the oil and gas segment

Oil & gas segment, consolidated

Figures in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

∆% |

|

2024 |

2023 |

∆% |

| Sales revenue |

|

596 |

548 |

+9% |

|

228 |

207 |

+10% |

| Domestic sales |

|

512 |

411 |

+25% |

|

201 |

181 |

+11% |

| Foreign market sales |

|

84 |

137 |

-39% |

|

28 |

26 |

+5% |

| Cost of sales |

|

(387) |

(319) |

+21% |

|

(153) |

(121) |

+26% |

| |

|

|

|

|

|

|

|

|

| Gross profit |

|

209 |

229 |

-9% |

|

75 |

86 |

-13% |

| |

|

|

|

|

|

|

|

|

| Selling expenses |

|

(46) |

(38) |

+21% |

|

(17) |

(13) |

+31% |

| Administrative expenses |

|

(57) |

(56) |

+2% |

|

(21) |

(18) |

+17% |

| Exploration expenses |

|

- |

(7) |

-100% |

|

- |

- |

NA |

| Other operating income |

|

67 |

64 |

+5% |

|

25 |

39 |

-36% |

| Other operating expenses |

|

(22) |

(26) |

-15% |

|

(8) |

(13) |

-38% |

| Impairment of financial assets |

|

(10) |

- |

NA |

|

- |

- |

NA |

| |

|

|

|

|

|

|

|

|

| Operating income |

|

122 |

166 |

-27% |

|

35 |

81 |

-57% |

| |

|

|

|

|

|

|

|

|

| Finance income |

|

1 |

2 |

-50% |

|

1 |

1 |

- |

| Finance costs |

|

(71) |

(157) |

-55% |

|

(22) |

(60) |

-63% |

| Other financial results |

|

(17) |

7 |

NA |

|

(3) |

(18) |

-83% |

| Financial results, net |

|

(87) |

(148) |

-41% |

|

(24) |

(77) |

-69% |

| |

|

|

|

|

|

|

|

|

| Loss before tax |

|

35 |

18 |

+94% |

|

11 |

4 |

+175% |

| |

|

|

|

|

|

|

|

|

| Income tax |

|

36 |

(2) |

NA |

|

(15) |

(2) |

NA |

| |

|

|

|

|

|

|

|

|

| Net loss for the period |

|

71 |

16 |

NA |

|

(4) |

2 |

NA |

| |

|

|

|

|

|

|

|

|

| Adjusted EBITDA |

|

310 |

291 |

+7% |

|

122 |

132 |

-8% |

| |

|

|

|

|

|

|

|

|

| Increases in PPE and right-of-use assets |

|

243 |

385 |

-37% |

|

46 |

169 |

-73% |

| Depreciation and amortization |

|

183 |

125 |

+46% |

|

73 |

52 |

+40% |

In

Q3 24, sales from

the oil and gas segment grew by 10% vs. Q3 23, mainly due to the increased gas deliveries under Plan Gas, thanks to the GPNK commissioned

in August 2023. However, deliveries were limited by transportation constraints due to delays in the commissioning of GPNK’s compressor

stations and higher temperatures in September. Higher gas sales prices to distribution companies, in line with the demand

tariff increases, and better crude oil prices and volumes contributed to the

segment’s sales increase. These effects were partially offset by lower gas sales to large users and exports to Chile, which were

affected by the economic downturn and higher hydrology, respectively.

| |

| Pampa Energía ● Earnings release Q3 24 ● 13 |

Oil and gas'

key performance indicators |

|

2024 |

|

2023 |

|

Variation |

| Oil |

Gas |

Total |

Oil |

Gas |

Total |

Oil |

Gas |

Total |

| Nine-month period |

|

|

|

|

|

|

|

|

|

|

|

|

| Volume |

|

|

|

|

|

|

|

|

|

|

|

|

| Production |

|

|

|

|

|

|

|

|

|

|

|

|

| In thousand m3/day |

|

0.8 |

13,382 |

|

|

0.8 |

10,793 |

|

|

+2% |

+24% |

+22% |

| In million cubic feet/day |

|

|

473 |

|

|

|

381 |

|

|

|

| In thousand boe/day |

|

5.0 |

78.8 |

83.8 |

|

4.9 |

63.5 |

68.5 |

|

|

| Sales |

|

|

|

|

|

|

|

|

|

|

|

|

| In thousand m3/day |

|

0.8 |

13,331 |

|

|

0.8 |

10,827 |

|

|

-10% |

+23% |

+21% |

| In million cubic feet/day |

|

|

471 |

|

|

|

382 |

|

|

|

| In thousand boe/day |

|

4.8 |

78.5 |

83.3 |

|

5.3 |

63.7 |

69.0 |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Average Price |

|

|

|

|

|

|

|

|

|

|

|

|

| In US$/bbl |

|

71.0 |

|

|

|

65.5 |

|

|

|

+8% |

-13% |

|

| In US$/MBTU |

|

|

3.9 |

|

|

|

4.5 |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Third quarter |

|

|

|

|

|

|

|

|

|

|

|

|

| Volume |

|

|

|

|

|

|

|

|

|

|

|

|

| Production |

|

|

|

|

|

|

|

|

|

|

|

|

| In thousand m3/day |

|

0.9 |

13,944 |

|

|

0.7 |

12,860 |

|

|

+16% |

+8% |

+9% |

| In million cubic feet/day |

|

|

492 |

|

|

|

454 |

|

|

|

| In thousand boe/day |

|

5.4 |

82.1 |

87.5 |

|

4.7 |

75.7 |

80.4 |

|

|

| Sales |

|

|

|

|

|

|

|

|

|

|

|

|

| In thousand m3/day |

|

0.9 |

13,632 |

|

|

0.7 |

12,885 |

|

|

+18% |

+6% |

+7% |

| In million cubic feet/day |

|

|

481 |

|

|

|

455 |

|

|

|

| In thousand boe/day |

|

5.5 |

80.2 |

85.7 |

|

4.6 |

75.8 |

80.5 |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Average Price |

|

|

|

|

|

|

|

|

|

|

|

|

| In US$/bbl |

|

71.9 |

|

|

|

63.1 |

|

|

|

+14% |

-6% |

|

| In US$/MBTU |

|

|

4.4 |

|

|

|

4.7 |

|

|

|

Note:

The net production in Argentina. The gas volume is standardized at 9,300 kilocalories (kCal).

Regarding

operating performance,

total production in Q3 24 was 87.5 kboe per day (+9% vs. Q3 23 but -4% vs. Q2 24), with an increase in gas

production to 13.9 million m3 per day (+8% vs. Q3 23 but -4%

vs. Q2 24), boosted by the latest round 4.2 of Plan Gas filling the GPNK, but limited by transportation constraints. Lower gas demand

from Chile and industries and higher temperatures in September partially offset the year-on-year and quarter-on-quarter increases.

Analyzing

the gas output by block, 57% of our total production in Q3 24 came from

El Mangrullo, where we reached 8.0 million m3 per day (+7% vs. Q3 23, but -13% vs. Q2 24). Sierra Chata followed with a 29%

contribution, growing production to 4.0 million m3 per day (+18% vs. Q3 23 and +20% vs. Q2 24). The outstanding productivity

of Sierra Chata’s shale wells hit a production record in July, with 5.0 million m3 per day. At non-operated blocks,

Río Neuquén maintained a steady production at 1.7 million m3 per day (+2% vs. Q3 23 and similar to Q2 24), while

Rincón del Mangrullo continued to deplete, contributing 0.2 million m3 per day (-21% vs. Q3 23 and -9% vs. Q2 24).

Our

gas price in

Q3 24 averaged US$4.4 per MBTU (-6% vs. Q3 23 but +10% vs. Q2 24, due to seasonality), primarily explained by lower exports to Chile

and sales to large users, partially offset by higher prices to retail, in line with the tariff

increases. As a result, Plan Gas compensation decreased 41% vs. Q3 23 to US$18

million.

| |

| Pampa Energía ● Earnings release Q3 24 ● 14 |

Regarding

our gas deliveries,

during Q3 24, 46% was destined for distribution companies and 40% for thermal power generation, both under Plan Gas. 7% supplied the

industrial/spot market, 3% was exported, and the remaining was sold to our petchem plants as raw material. Compared to Q3 23, 41% supplied

the retail segment, 41% the thermal power units, 10% sold to the industrial/spot market, 5% was exported and the remainder to our petchem

plants.

Oil

production reached 5.4 kbbl per day in Q3 24 (+16% vs. Q3 23 and similar

to Q2 24), driven by the start of shale oil production at Rincón de Aranda (+1.2 kbbl per day), partially offset by year-on-year

decreases of 0.2 kbbl per day at El Tordillo and 0.5 kbbl per day at Los Blancos.

Our

oil price in

Q3 24 was 14% higher than Q3 23, reaching US$71.9 per barrel, with domestic and export prices very similar. 54% of our sales were destined

for the domestic market, compared to 85% during Q3 23.

The

lifting cost[5] recorded

US$48 million in Q3 24 (+16% vs. Q3 23 and +9% vs. Q2 24), mainly due to the shale oil development in Rincón de Aranda and, to

a lesser extent, higher gas treatment and transportation costs. The lifting

cost per boe increased to US$6.0 per boe produced in Q3 24, vs. US$5.6

per boe in Q3 23 (+6%) and US$5.3 per boe in Q2 24 (+12%). However, gas

lifting cost decreased by 2% vs. Q3 23 to US$0.8/MBTU, explained by the

growth in production.

Regarding

other operating income and expenses,

higher crude oil stock costs and royalties stand out due to the increased crude oil price and gas production. Plan Gas compensation reached

US$18 million, a 41% year-on-year decrease because of the higher prices charged

to distribution companies, as mentioned before. These effects were partially

offset by higher overdue interests, explained by a year-on-year rise in Plan Gas invoicing.

Financial

results in Q3 24 recorded net losses of US$24 million, a 69% improvement

vs. Q3 23, mainly due to lower financial interests from decreased AR$-debt stock and lesser losses from FX differences due to the minor

devaluation impact over trade receivables in AR$, partially offset by lower gains from holding financial securities.

Reconciliation of adjusted EBITDA from oil & gas,

in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

|

2024 |

2023 |

| Consolidated operating income |

|

122 |

166 |

|

35 |

81 |

| Consolidated depreciations and amortizations |

|

183 |

125 |

|

73 |

52 |

| Reporting EBITDA |

|

305 |

291 |

|

108 |

133 |

| |

|

|

|

|

|

|

| Deletion of PPE & inventories' impairment |

|

19 |

- |

|

19 |

- |

| Deletion of gain from commercial interests |

|

(18) |

(7) |

|

(5) |

(1) |

| Deletion of Río Atuel's reversal losses |

|

- |

7 |

|

- |

- |

| Deletion of CAMMESA's receivable impairment |

|

4 |

- |

|

- |

- |

| |

|

|

|

|

|

|

| Adjusted EBITDA from oil & gas |

|

310 |

291 |

|

122 |

132 |

Our

oil and gas adjusted EBITDA amounted

to US$122 million in Q3 24 (-8% vs. Q3 23), mainly explained by higher operating expenses and lower sales to industries and exports,

partially offset by higher gas deliveries under Plan Gas, thanks to the GPNK. The adjusted EBITDA excludes non-recurring and non-cash

income and expenses, as well as overdue interests, which are mainly charged to CAMMESA.

Finally,

capital expenditures amounted

to US$46 million in Q3 24 (-73% vs. Q3 23), mainly driven by the shale gas deployment during 2023, partially offset by the beginning

of the shale oil pilot plan in Rincón de Aranda.

5

It only considers maintenance, treatment, internal transportation and wellhead staff costs. It does not include amortizations and depreciations.

| |

| Pampa Energía ● Earnings release Q3 24 ● 15 |

3.4

Analysis of the petrochemicals segment

Petrochemicals segment, consolidated

Figures in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

∆% |

|

2024 |

2023 |

∆% |

| Sales revenue |

|

394 |

389 |

+1% |

|

140 |

132 |

+6% |

| Domestic sales |

|

247 |

273 |

-10% |

|

91 |

92 |

-0% |

| Foreign market sales |

|

147 |

116 |

+27% |

|

48 |

40 |

+21% |

| Cost of sales |

|

(361) |

(341) |

+6% |

|

(135) |

(110) |

+23% |

| |

|

|

|

|

|

|

|

|

| Gross profit |

|

33 |

48 |

-31% |

|

5 |

22 |

-77% |

| |

|

|

|

|

|

|

|

|

| Selling expenses |

|

(9) |

(12) |

-25% |

|

(3) |

(4) |

-25% |

| Administrative expenses |

|

(5) |

(5) |

- |

|

(2) |

(2) |

- |

| Other operating income |

|

11 |

- |

NA |

|

3 |

- |

NA |

| Other operating expenses |

|

(5) |

(2) |

+150% |

|

(2) |

(1) |

+100% |

| Impairment of inventories |

|

- |

(3) |

-100% |

|

- |

- |

NA |

| |

|

|

|

|

|

|

|

|

| Operating income |

|

25 |

26 |

-4% |

|

1 |

15 |

-93% |

| |

|

|

|

|

|

|

|

|

| Finance costs |

|

(3) |

(2) |

+50% |

|

(1) |

(1) |

- |

| Other financial results |

|

4 |

7 |

-43% |

|

3 |

4 |

-25% |

| Financial results, net |

|

1 |

5 |

-80% |

|

2 |

3 |

-33% |

| |

|

|

|

|

|

|

|

|

| Profit before tax |

|

26 |

31 |

-16% |

|

3 |

18 |

-83% |

| |

|

|

|

|

|

|

|

|

| Income tax |

|

7 |

(5) |

NA |

|

4 |

(3) |

NA |

| |

|

|

|

|

|

|

|

|

| Net income for the period |

|

33 |

26 |

+27% |

|

7 |

15 |

-53% |

| |

|

|

|

|

|

|

|

|

| Adjusted EBITDA |

|

28 |

33 |

-15% |

|

2 |

16 |

-88% |

| |

|

|

|

|

|

|

|

|

| Increases in PPE |

|

4 |

4 |

- |

|

2 |

1 |

+100% |

| Depreciation and amortization |

|

3 |

4 |

-25% |

|

1 |

1 |

- |

| Reconciliation of adjusted EBITDA from petrochemicals, in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

|

2024 |

2023 |

| Consolidated operating income |

|

25 |

26 |

|

1 |

15 |

| Consolidated depreciations and amortizations |

|

3 |

4 |

|

1 |

1 |

| Reporting EBITDA |

|

28 |

30 |

|

2 |

16 |

| |

|

|

|

|

|

|

| Deletion of inventory impairment |

|

- |

3 |

|

- |

- |

| Deletion of gain from commercial interests |

|

(0) |

(0) |

|

(0) |

(0) |

| |

|

|

|

|

|

|

| Adjusted EBITDA from petrochemicals |

|

28 |

33 |

|

2 |

16 |

The

adjusted EBITDA for

the petrochemicals segment reached US$2 million in Q3 24, an 88% drop compared to Q3 23. This decrease was driven by lower international

spread in reforming products, a drop in domestic polystyrene prices, a decline in domestic volumes of styrenics and higher US$-denominated

operating expenses. These effects were partially offset by higher dispatch of reforming products, both in domestic and foreign markets.

In addition, we recorded a US$3 million profit from the settlement of exports at a differential FX.

Total

volume sold

increased by 25% vs. Q3 23, reaching 128 thousand tons, driven by higher reforming dispatch of octane basis in the local market and isomerized

naphtha and aromatic for export. Lower demand for styrene, polystyrene and SBR partially offset these gains, mainly due to the local

industry activity.

| |

| Pampa Energía ● Earnings release Q3 24 ● 16 |

In

Q3 24, financial results from

the petrochemicals segment reached a profit of US$2 million, similar to Q3 23 US$3 million profit, mainly explained by the lower impact

of the AR$ devaluation over payables.

Petrochemicals'

key performance indicators |

|

Products |

|

Total |

| |

Styrene & polystyrene1 |

SBR |

Reforming & others |

|

| Nine-month period |

|

|

|

|

|

|

| Volume sold 9M24 (thousand ton) |

|

64 |

33 |

251 |

|

348 |

| Volume sold 9M23 (thousand ton) |

|

84 |

32 |

195 |

|

311 |

| Variation 9M24 vs. 9M23 |

|

-24% |

+4% |

+29% |

|

+12% |

| |

|

|

|

|

|

|

| Average price 9M24 (US$/ton) |

|

1,818 |

1,841 |

861 |

|

1,130 |

| Average price 9M23 (US$/ton) |

|

1,860 |

1,813 |

891 |

|

1,248 |

| Variation 9M24 vs. 9M23 |

|

-2% |

+2% |

-3% |

|

-9% |

| |

|

|

|

|

|

|

| Third quarter |

|

|

|

|

|

|

| Volume sold Q3 24 (thousand ton) |

|

22 |

11 |

94 |

|

128 |

| Volume sold Q3 23 (thousand ton) |

|

30 |

12 |

60 |

|

102 |

| Variation Q3 24 vs. Q3 23 |

|

-27% |

-11% |

+59% |

|

+25% |

| |

|

|

|

|

|

|

| Average price Q3 24 (US$/ton) |

|

1,825 |

1,926 |

822 |

|

1,092 |

| Average price Q3 23 (US$/ton) |

|

1,809 |

1,639 |

942 |

|

1,285 |

| Variation Q3 24 vs. Q3 23 |

|

+1% |

+18% |

-13% |

|

-15% |

Note:

1 Includes Propylene.

| |

| Pampa Energía ● Earnings release Q3 24 ● 17 |

3.5

Analysis of the holding and others segment

Holding and others segment, consolidated

Figures in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

∆% |

|

2024 |

2023 |

∆% |

| Sales revenue |

|

29 |

11 |

+164% |

|

19 |

3 |

NA |

| Cost of sales |

|

(5) |

- |

NA |

|

(5) |

- |

NA |

| |

|

|

|

|

|

|

|

|

| Gross profit |

|

24 |

11 |

+118% |

|

14 |

3 |

NA |

| |

|

|

|

|

|

|

|

|

| Administrative expenses |

|

(38) |

(34) |

+12% |

|

(19) |

(12) |

+58% |

| Other operating income |

|

4 |

1 |

+300% |

|

3 |

- |

NA |

| Other operating expenses |

|

(34) |

(16) |

+113% |

|

(6) |

(9) |

-33% |

| Impairment of financial assets |

|

- |

(4) |

-100% |

|

- |

(1) |

-100% |

| Recovery/(accrual) of impairment on intangible assets |

|

- |

2 |

-100% |

|

- |

- |

NA |

| Income from the sale of associates |

|

7 |

1 |

NA |

|

- |

1 |

-100% |

| Results for participation in joint businesses |

|

129 |

33 |

+291% |

|

52 |

4 |

NA |

| |

|

|

|

|

|

|

|

|

| Operating income |

|

92 |

(6) |

NA |

|

44 |

(14) |

NA |

| |

|

|

|

|

|

|

|

|

| Finance income |

|

- |

5 |

-100% |

|

- |

2 |

-100% |

| Finance costs |

|

(24) |

(37) |

-35% |

|

(9) |

(10) |

-10% |

| Other financial results |

|

25 |

157 |

-84% |

|

18 |

55 |

-67% |

| Financial results, net |

|

1 |

125 |

-99% |

|

9 |

47 |

-81% |

| |

|

|

|

|

|

|

|

|

| Profit before tax |

|

93 |

119 |

-22% |

|

53 |

33 |

+61% |

| |

|

|

|

|

|

|

|

|

| Income tax |

|

(12) |

(14) |

-14% |

|

(5) |

(8) |

-38% |

| |

|

|

|

|

|

|

|

|

| Net income for the period |

|

81 |

105 |

-23% |

|

48 |

25 |

+92% |

| |

|

|

|

|

|

|

|

|

| Adjusted EBITDA |

|

112 |

51 |

+118% |

|

43 |

6 |

NA |

| |

|

|

|

|

|

|

|

|

| Increases in PPE |

|

4 |

4 |

- |

|

2 |

1 |

+100% |

| Depreciation and amortization |

|

- |

- |

NA |

|

- |

- |

NA |

The

holding and others segment, excluding the affiliates’ equity income (TGS and Transener), posted a lower loss on operating

margin of US$8 million in Q3 24 vs. US$18 million in Q3 23, mainly explained

by the accounting consolidation of OCP from September 1, 2024,

which contributed US$7 million of operating income, in addition to higher fees, partially offset by higher accrual of executive compensation

due to the share price outperformance.

In

Q3 24, financial results reached

a net profit of US$9 million, US$38 million less than in Q3 23, mainly due to lower earnings from FX difference over tax payables, partially

offset by higher gains from holding financial instruments.

| |

| Pampa Energía ● Earnings release Q3 24 ● 18 |

| Reconciliation of adjusted EBITDA from holding and others, in US$ million |

|

Nine-month period |

|

Third quarter |

| |

2024 |

2023 |

|

2024 |

2023 |

| Consolidated operating income |

|

92 |

(6) |

|

44 |

(14) |

| Consolidated depreciations and amortizations |

|

- |

- |

|

- |

- |

| Reporting EBITDA |

|

92 |

(6) |

|

44 |

(14) |

| |

|

|

|

|

|

|

| Deletion of equity income |

|

(129) |

(33) |

|

(52) |

(4) |

| Deletion of gain from commercial interests |

|

(0) |

(0) |

|

(0) |

0 |

| Deletion of contigencies provision |

|

16 |

- |

|

- |

- |

| Deletion of intang. assets' impairment/(recovery) |

|

- |

(2) |

|

- |

- |

| Deletion of the sale of associates |

|

(7) |

(1) |

|

- |

(1) |

| TGS's EBITDA adjusted by ownership |

|

113 |

73 |

|

40 |

21 |

| Transener's EBITDA adjusted by ownership |

|

26 |

20 |

|

11 |

4 |

| |

|

|

|

|

|

|

| Adjusted EBITDA from holding and others |

|

112 |

51 |

|

43 |

6 |

The

adjusted EBITDA of