true

FY

2023

--12-31

This Amendment No. 4 to Form 10-K (this "Amendment No. 4") amends the Annual Report to Form 10-K of Fintech Scion Limited, a Nevada corporation ("Fintech," the "Company," "we," or "us") for the fiscal year ended December 31, 2023, as filed with the Securities and Exchange Commission (the "SEC") on April 5, 2024 (the "Original Filing"). This Amendment is being filed for the purpose of making clarifications to our disclosure in response to the comment letter received from the staff of the SEC dated June 11, 2024 in connection with the staff's review of the Original Filing and to restate our financial statements as of and for the year ended December 31, 2023 and 2022, and to update related .

0001623590

0

0

0

P5Y

P5Y

P5Y

P5Y

P5Y

0

0

0001623590

2023-01-01

2023-12-31

0001623590

2022-12-31

0001623590

2024-08-15

0001623590

2023-12-31

0001623590

2022-01-01

2022-12-31

0001623590

us-gaap:CommonStockMember

2020-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2020-12-31

0001623590

vxel:MergerReservesMember

2020-12-31

0001623590

us-gaap:RetainedEarningsMember

2020-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2020-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2020-12-31

0001623590

2020-12-31

0001623590

us-gaap:CommonStockMember

2021-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001623590

vxel:MergerReservesMember

2021-12-31

0001623590

us-gaap:RetainedEarningsMember

2021-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2021-12-31

0001623590

2021-12-31

0001623590

us-gaap:CommonStockMember

2022-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001623590

vxel:MergerReservesMember

2022-12-31

0001623590

us-gaap:RetainedEarningsMember

2022-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2022-12-31

0001623590

us-gaap:CommonStockMember

2021-01-01

2021-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2021-01-01

2021-12-31

0001623590

vxel:MergerReservesMember

2021-01-01

2021-12-31

0001623590

us-gaap:RetainedEarningsMember

2021-01-01

2021-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-01-01

2021-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2021-01-01

2021-12-31

0001623590

2021-01-01

2021-12-31

0001623590

us-gaap:CommonStockMember

2022-01-01

2022-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-12-31

0001623590

vxel:MergerReservesMember

2022-01-01

2022-12-31

0001623590

us-gaap:RetainedEarningsMember

2022-01-01

2022-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-01-01

2022-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2022-01-01

2022-12-31

0001623590

us-gaap:CommonStockMember

2023-01-01

2023-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-12-31

0001623590

vxel:MergerReservesMember

2023-01-01

2023-12-31

0001623590

us-gaap:RetainedEarningsMember

2023-01-01

2023-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2023-01-01

2023-12-31

0001623590

us-gaap:CommonStockMember

2023-12-31

0001623590

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001623590

vxel:MergerReservesMember

2023-12-31

0001623590

us-gaap:RetainedEarningsMember

2023-12-31

0001623590

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-12-31

0001623590

us-gaap:NoncontrollingInterestMember

2023-12-31

0001623590

vxel:HWGGCapitalPLCMember

2023-01-01

2023-12-31

0001623590

vxel:HWGGCapitalPLCMember

vxel:OwnershipOneMember

2023-12-31

0001623590

vxel:HWGGCapitalPLCMember

vxel:OwnershipOneMember

2022-12-31

0001623590

vxel:HWGGCapitalPLCMember

vxel:OtherInvesteesOneMember

2023-01-01

2023-12-31

0001623590

vxel:HWGCashSingaporePteLtdMember

2023-01-01

2023-12-31

0001623590

vxel:HWGCashSingaporePteLtdMember

vxel:OwnershipTwoMember

2023-12-31

0001623590

vxel:HWGCashSingaporePteLtdMember

vxel:OwnershipTwoMember

2022-12-31

0001623590

vxel:HWGCashSingaporePteLtdMember

vxel:OtherInvesteesTwoMember

2023-01-01

2023-12-31

0001623590

vxel:HWGCKZLimitedMember

2023-01-01

2023-12-31

0001623590

vxel:HWGCKZLimitedMember

vxel:OwnershipThreeMember

2023-12-31

0001623590

vxel:HWGCKZLimitedMember

vxel:OwnershipThreeMember

2022-12-31

0001623590

vxel:HWGCKZLimitedMember

vxel:OtherInvesteesThreeMember

2023-01-01

2023-12-31

0001623590

vxel:FintechScionLimitedMember

2023-01-01

2023-12-31

0001623590

vxel:FintechDigitalSolutionsLimitedMember

vxel:OwnershipFiveMember

2023-12-31

0001623590

vxel:FintechDigitalSolutionsLimitedMember

vxel:OwnershipFiveMember

2022-12-31

0001623590

vxel:FintechScionLimitedMember

vxel:OtherInvesteesFourMember

2023-01-01

2023-12-31

0001623590

vxel:FintechDigitalSolutionsLimitedMember

2023-01-01

2023-12-31

0001623590

vxel:FintechDigitalSolutionsLimitedMember

vxel:OtherInvesteesFiveMember

2023-01-01

2023-12-31

0001623590

vxel:FintechDigitalConsultingLimitedMember

2023-01-01

2023-12-31

0001623590

vxel:FintechDigitalConsultingLimitedMember

vxel:OwnershipSixMember

2023-12-31

0001623590

vxel:FintechDigitalConsultingLimitedMember

vxel:OwnershipSixMember

2022-12-31

0001623590

vxel:FintechDigitalConsultingLimitedMember

vxel:OtherInvesteesSixMember

2023-01-01

2023-12-31

0001623590

vxel:AeloraSdnBhdPreviouslyKnownAsVitaxelSdnBhdasbMember

2023-01-01

2023-12-31

0001623590

vxel:AeloraSdnBhdPreviouslyKnownAsVitaxelSdnBhdasbMember

vxel:OwnershipSevenMember

2023-12-31

0001623590

vxel:AeloraSdnBhdPreviouslyKnownAsVitaxelSdnBhdasbMember

vxel:OwnershipSevenMember

2022-12-31

0001623590

vxel:AeloraSdnBhdPreviouslyKnownAsVitaxelSdnBhdasbMember

vxel:OtherInvesteesSevenMember

2023-01-01

2023-12-31

0001623590

vxel:VitaxelOnlineMallSdnBhdMember

2023-01-01

2023-12-31

0001623590

vxel:VitaxelOnlineMallSdnBhdMember

vxel:OwnershipEightMember

2023-12-31

0001623590

vxel:VitaxelOnlineMallSdnBhdMember

vxel:OwnershipEightMember

2022-12-31

0001623590

vxel:VitaxelOnlineMallSdnBhdMember

vxel:OtherInvesteesEightMember

2023-01-01

2023-12-31

0001623590

vxel:HWGGCapitalMember

vxel:ExchangeAgreementMember

2022-07-20

2022-07-21

0001623590

vxel:HWGGCapitalMember

vxel:ExchangeAgreementMember

2022-07-21

0001623590

vxel:HWGGCapitalMember

2022-07-20

2022-07-21

0001623590

vxel:HWGGCapitalMember

2022-11-14

2022-11-15

0001623590

vxel:AcquisitionOfFintechMember

vxel:ExchangeAgreementMember

2022-08-08

2022-08-09

0001623590

vxel:AcquisitionOfFintechMember

vxel:ExchangeAgreementMember

2022-08-09

0001623590

vxel:AcquisitionOfFintechMember

2022-08-08

2022-08-09

0001623590

vxel:AcquisitionOfFintechMember

2022-11-29

2022-11-30

0001623590

vxel:ASBAndVOMMember

2022-12-28

2022-12-29

0001623590

vxel:CICODigitalSolutionsLimitedMember

2023-10-09

2023-10-11

0001623590

vxel:CICODigitalSolutionsLimitedMember

2023-10-11

0001623590

vxel:ASBMember

2022-12-31

0001623590

vxel:VOMMember

2022-12-31

0001623590

us-gaap:OfficeEquipmentMember

2023-12-31

0001623590

us-gaap:ComputerEquipmentMember

2023-12-31

0001623590

us-gaap:FurnitureAndFixturesMember

2023-12-31

0001623590

vxel:ElectricalAndFittingMember

2023-12-31

0001623590

us-gaap:SoftwareAndSoftwareDevelopmentCostsMember

2023-12-31

0001623590

us-gaap:OfficeEquipmentMember

2022-12-31

0001623590

us-gaap:ComputerEquipmentMember

2022-12-31

0001623590

us-gaap:FurnitureAndFixturesMember

2022-12-31

0001623590

us-gaap:SoftwareAndSoftwareDevelopmentCostsMember

2022-12-31

0001623590

country:GB

2023-01-01

2023-12-31

0001623590

country:GB

2022-01-01

2022-12-31

0001623590

country:MY

2023-01-01

2023-12-31

0001623590

country:MY

2022-01-01

2022-12-31

0001623590

country:US

2023-01-01

2023-12-31

0001623590

country:US

2022-01-01

2022-12-31

0001623590

vxel:ForeignMember

2023-01-01

2023-12-31

0001623590

vxel:ForeignMember

2022-01-01

2022-12-31

0001623590

vxel:HoWahGentingGroupSdnBhdMember

2023-12-31

0001623590

vxel:HoWahGentingGroupSdnBhdMember

2022-12-31

0001623590

vxel:HWGFintechInternationalLtdMember

2023-12-31

0001623590

vxel:HWGFintechInternationalLtdMember

2022-12-31

0001623590

vxel:GrandeLegacyIncMember

2023-12-31

0001623590

vxel:GrandeLegacyIncMember

2022-12-31

0001623590

vxel:HwgCapitalIncMember

2023-12-31

0001623590

vxel:HwgCapitalIncMember

2022-12-31

0001623590

vxel:HwgDigitalInvestmentBankMalaysiaPLCMember

2023-12-31

0001623590

vxel:HwgDigitalInvestmentBankMalaysiaPLCMember

2022-12-31

0001623590

vxel:AeloraSdnBhdMember

2023-12-31

0001623590

vxel:AeloraSdnBhdMember

2022-12-31

0001623590

vxel:ShalomDodounMember

2022-12-31

0001623590

vxel:NatalieKastbergMember

2023-12-31

0001623590

vxel:NatalieKastbergMember

2022-12-31

0001623590

srt:ChiefExecutiveOfficerMember

2023-12-31

0001623590

vxel:GrandeLegacyIncMember

2023-01-01

2023-12-31

0001623590

vxel:ASBMember

2023-01-01

2023-12-31

0001623590

srt:OfficerMember

2023-12-31

0001623590

vxel:ShalomDodounDirectorChiefExecutiveOfficerOfTheCompanyMember

2023-12-31

0001623590

vxel:ShalomDodounDirectorChiefExecutiveOfficerOfTheCompanyMember

2022-12-31

0001623590

vxel:RichardBermanNonExecutiveDirectorOfTheCompanyMember

2023-12-31

0001623590

vxel:RichardBermanNonExecutiveDirectorOfTheCompanyMember

2022-12-31

0001623590

2022-04-08

0001623590

srt:MaximumMember

2022-04-11

0001623590

srt:MinimumMember

2022-04-11

0001623590

2022-04-11

0001623590

2022-11-15

0001623590

2022-11-30

0001623590

2022-07-21

0001623590

vxel:CICODigitalSolutionsLimitedMember

2023-11-13

2023-11-15

0001623590

vxel:CICODigitalSolutionsLimitedMember

2023-12-25

2023-12-27

0001623590

us-gaap:RedeemableConvertiblePreferredStockMember

2022-03-10

0001623590

vxel:ScenarioPlan30PercentMember

2023-12-31

0001623590

vxel:ScenarioPlan50PercentMember

2023-12-31

0001623590

vxel:ScenarioPlan100PercentMember

2023-12-31

0001623590

vxel:ScenarioPlan30PercentMember

2022-12-31

0001623590

vxel:ScenarioPlan50PercentMember

2022-12-31

0001623590

vxel:ScenarioPlan100PercentMember

2022-12-31

0001623590

vxel:CICODigitalSolutionsLimitedMember

us-gaap:SubsequentEventMember

2024-01-29

2024-01-30

0001623590

srt:ScenarioPreviouslyReportedMember

2022-12-31

0001623590

srt:RestatementAdjustmentMember

2022-12-31

0001623590

vxel:AsRestatedTwoMember

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

2022-01-01

2022-12-31

0001623590

srt:RestatementAdjustmentMember

2022-01-01

2022-12-31

0001623590

vxel:AsRestatedMember

2022-01-01

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

vxel:NetIncomeMember

2022-12-31

0001623590

srt:RestatementAdjustmentMember

vxel:NetIncomeMember

2022-12-31

0001623590

vxel:NetIncomeMember

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

srt:SubsidiariesMember

2022-12-31

0001623590

srt:RestatementAdjustmentMember

srt:SubsidiariesMember

2022-12-31

0001623590

srt:SubsidiariesMember

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

vxel:ReverseMrgerRecapitalizationMember

2022-12-31

0001623590

srt:RestatementAdjustmentMember

vxel:ReverseMrgerRecapitalizationMember

2022-12-31

0001623590

vxel:ReverseMrgerRecapitalizationMember

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

country:GB

2022-01-01

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

country:MY

2022-01-01

2022-12-31

0001623590

srt:RestatementAdjustmentMember

country:MY

2022-01-01

2022-12-31

0001623590

srt:ScenarioPreviouslyReportedMember

2023-01-01

2023-12-31

0001623590

srt:RestatementAdjustmentMember

2023-01-01

2023-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K/A

(Amendment

No. 4)

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF

1934

For

the fiscal year ended December 31, 2023

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT

OF 1934

For

the transition period from ___________________________ to ___________________________

Commission

file number 000-55685

| FINTECH

SCION LIMITED |

| (Exact

name of registrant as specified in its charter) |

| Nevada |

|

30-0803939 |

| (State or other jurisdiction

of incorporation or organization) |

|

(I.R.S. Employer

Identification No.) |

M

Floor & 1st Floor

No.

33 Jalan Maharajalela

50150,

Kuala Lumpur, Malaysia |

|

N/A |

| (Address of principal

executive offices) |

|

(Zip Code) |

+603

9226 0908

(Registrant’s

telephone number, including area code)

Portman

House, 2 Portman Street

London,

W1H 6DU

United

Kingdom

| (Former

name, former address and former fiscal year, if changed since last report) |

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange

on

which registered |

| None |

|

N/A |

|

N/A |

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, $0.001 par value

(Title

of class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

☐ No ☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes

☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days.

☒

Yes ☐ No

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant

to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit and post such files).

☒

Yes ☐ No

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller

reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

| Large

accelerated filer |

☐ |

Accelerated

filer |

☐ |

| |

|

|

|

| Non-accelerated

filer |

☒ |

Smaller reporting

company |

☒ |

| |

|

|

|

| |

|

Emerging growth

company |

☐ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the

registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The

aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at

which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of

the Registrant’s most recently completed fiscal year was $2,628,493 (computed using the closing sales price of $2.25 per

share of common stock on such date).

198,742,643 shares of common stock were issued and outstanding as of August 15, 2024.

Documents

Incorporated by Reference: None.

Explanatory

Note

This Amendment No. 4 to Form 10-K (this

“Amendment No. 4”) amends the Annual Report to Form 10-K of Fintech Scion Limited, a Nevada corporation (“Fintech,”

the “Company,” “we,” or “us”) for the fiscal year ended December 31,

2023, as filed with the Securities and Exchange Commission (the “SEC”) on April 5, 2024 (the “Original Filing”).

This Amendment is being filed for the purpose of making clarifications to our disclosure in response to the comment letter received

from the staff of the SEC dated June 11, 2024 in connection with the staff’s review of the Original Filing and to restate

our financial statements as of and for the year ended December 31, 2023 and 2022.

Except

as otherwise indicated herein, this Form 10-K/A does not reflect events occurring after the date of the Original Filing or modify

or update those disclosures, including the exhibits to the Form 10-K affected by subsequent events. Information not affected by

the restatement is unchanged and reflects the disclosures made at the time of the Original Filing. Accordingly, this Form 10-K/A

should be read in conjunction with our filings made with the Securities and Exchange Commission subsequent to the Original Filing.

For the convenience of the reader, this Form 10-K/A presents the Original Report in its entirety, subject to the changes described

below. The following items have been amended and restated as a result of the restatement:

| |

● |

Part I - Item 1

- Business |

| |

● |

Part I - Item 1A

- Risk Factors |

| |

● |

Part II - Item 7

- Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| |

● |

Part II - Item 8

- Consolidated Financial Statements and Supplementary Data |

| |

● |

Part II - Item 9A

- Controls and Procedures |

| |

● |

Part IV - Item 15(b)

- Exhibits |

In

addition, as required by Rule 12b-15 under the Securities Exchange Act of 1934 as amended (the “Exchange Act”) we

are also filing new certifications by the Company’s Principal Executive Officer and Principal Financial and Accounting Officer

are filed herewith as Exhibit 31.1, 31.2 and 32.1, respectively, pursuant to Rule 13a-14(a) or 15d-14(a) of the Exchange Act.

Description

of Restatement

On June 11,

2024, the staff of the SEC issued a comment letter to our Form 10-K for the fiscal years ended December 31, 2023 and 2022 (the

“SEC Staff Statement”). The SEC Staff Statement addresses certain accounting and reporting considerations related

to the statements of income (loss) and comprehensive income (loss), stockholders’ equity, and cash flows for the period

from January 1, 2022 to November 30, 2022. In the light of this SEC Staff Statement, the Board of Directors, after discussion

with management, has determined that the financial statements previously filed with the SEC should be restated to reflect the

recognition of the results of operation for the acquisition of Fintech.

In

connection with the restatement, management has re-evaluated the effectiveness of our disclosure controls and procedures and internal

control over financial reporting as of December 31, 2023 and 2022. As a result of that assessment, management has concluded that

our disclosure controls and procedures and internal controls over financial reporting were not effective as of December 31, 2023

and 2022, due to a material weakness in our internal control over financial reporting. See Part II, Item 9A, “Controls and

Procedures.”

TABLE

OF CONTENTS

CAUTIONARY

NOTE REGARDING FORWARD-LOOKING STATEMENTS AND INDUSTRY DATA

This

Annual Report on Form 10-K/A contains forward-looking statements which are made pursuant to the safe harbor provisions of Section

27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act

of 1934, as amended (the “Exchange Act”). These statements may be identified by such forward-looking terminology as

“may,” “should,” “expects,” “intends,” “plans,” “anticipates,”

“believes,” “estimates,” “predicts,” “potential,” “continue” or the

negative of these terms or other comparable terminology. Our forward-looking statements are based on a series of expectations,

assumptions, estimates and projections about our company, are not guarantees of future results or performance and involve substantial

risks and uncertainty. We may not actually achieve the plans, intentions or expectations disclosed in these forward-looking statements.

Actual results or events could differ materially from the plans, intentions and expectations disclosed in these forward-looking

statements. Our business and our forward-looking statements involve substantial known and unknown risks and uncertainties, including

the risks and uncertainties inherent in our statements regarding:

| |

● |

our projected financial position and estimated

cash burn rate; |

| |

|

|

| |

● |

our estimates regarding expenses, future revenues

and capital requirements; |

| |

|

|

| |

● |

our ability to continue as a going concern; |

| |

|

|

| |

● |

our need to raise substantial additional capital

to fund our operation; |

| |

|

|

| |

● |

our dependence on third parties in the conduct

of our operations; |

| |

|

|

| |

● |

our ability to obtain the necessary regulatory

approvals to market and commercialize our products; |

| |

|

|

| |

● |

the impact of a health epidemic, on our business,

our operations or the global economy as a whole; |

| |

|

|

| |

● |

the results of market research conducted by

us or others; |

| |

|

|

| |

● |

our ability to obtain and maintain intellectual

property protection for our current and future products; |

| |

|

|

| |

● |

our ability to protect our intellectual property

rights and the potential for us to incur substantial costs from lawsuits to enforce or protect our intellectual property rights; |

| |

|

|

| |

● |

the possibility that a third party may claim

we or our third-party licensors have infringed, misappropriated or otherwise violated their intellectual property rights and

that we may incur substantial costs and be required to devote substantial time defending against claims against us; |

| |

|

|

| |

● |

our reliance on third-party suppliers and manufacturers; |

| |

|

|

| |

● |

the success of competing payment platforms and

products that are or become available; |

| |

● |

our ability to expand our organization to accommodate

potential growth and our ability to retain and attract key personnel; |

| |

|

|

| |

● |

the potential for us to incur substantial costs

resulting from product liability lawsuits against us and the potential for these product liability lawsuits to cause us to

limit our commercialization of our products; and |

| |

|

|

| |

● |

the successful development of our commercialization

capabilities, including sales and marketing capabilities. |

All

of our forward-looking statements are as of the date of this Annual Report on Form 10-K/A only. In each case, actual results may

differ materially from such forward-looking information. We can give no assurance that such expectations or forward-looking statements

will prove to be correct. An occurrence of, or any material adverse change in, one or more of the risk factors or risks and uncertainties

referred to in this Annual Report on Form 10-K/A or included in our other public disclosures or our other periodic reports or other

documents or filings filed with or furnished to the U.S. Securities and Exchange Commission (the “SEC”) could materially

and adversely affect our business, prospects, financial condition and results of operations. Except as required by law, we do

not undertake or plan to update or revise any such forward-looking statements to reflect actual results, changes in plans, assumptions,

estimates or projections or other circumstances affecting such forward-looking statements occurring after the date of this Annual

Report on Form 10-K/A, even if such results, changes or circumstances make it clear that any forward-looking information will not

be realized. Any public statements or disclosures by us following this Annual Report on Form 10-K/A that modify or impact any of

the forward-looking statements contained in this Annual Report on Form 10-K/A will be deemed to modify or supersede such statements

in this Annual Report on Form 10-K/A.

This

Annual Report on Form 10-K/A may include market data and certain industry data and forecasts, which we may obtain from internal

company surveys, market research, consultant surveys, publicly available information, reports of governmental agencies and industry

publications, articles and surveys. Industry surveys, publications, consultant surveys and forecasts generally state that the

information contained therein has been obtained from sources believed to be reliable, but the accuracy and completeness of such

information is not guaranteed. While we believe that such studies and publications are reliable, we have not independently verified

market and industry data from third-party sources.

PART

I.

ITEM

1. Business

Overview

Fintech

Scion Limited (“Fintech Scion”, the “Company”, “we”, “our”, or “us”)

is a fintech enterprise poised to revolutionize the financial landscape through our digital Banking-as-a-Service (BaaS) platform.

Our mission is to empower merchants by furnishing them with an integrated suite of tools, skills, and solutions that streamline

payment services, unlocking a realm of secure, online, and fully managed transactions and settlements. We currently operate through

our wholly-owned subsidiaries based in Malaysia and the United Kingdom.

At

the core of our enterprise lies a sophisticated financial ecosystem, underpinned by a robust technological infrastructure. This

infrastructure has been developed with the mission of empowering financial institutions to offer seamless, consolidated experiences

across diverse verticals encompassing business-to-business, business-to-consumer, and consumer-to-business domains.

In

an era where merchants are leveraging an array of software solutions and digital tools to bolster their competitive edge, our

role has emerged as a pivotal enabler. The intricate challenge of managing disparate software systems sourced from various providers

has become an impediment for merchants of all sizes to seamlessly embrace payments.

Our

current clientele encompasses an array of enterprises and organizations, spanning varied sectors, including, but not limited to

the management consultancy services, development of software and programming activities, e-commerce, tours and entertainment operations,

information technology and investment banking all with a common objective: to minimize the intricacies and costs associated with

fund transfers. We extend our services to online businesses, providing comprehensive solutions encompassing payment collection,

cross-border transactions, FX services, and corporate bank accounts.

Our

cutting-edge payments platform boasts a comprehensive suite of integrated payment products and services tailored to various channels–be

it in-store, online, or through mobile and tablet interfaces. This suite encompasses end-to-end payment processing for an array

of payment types, merchant acquiring and issuing, diverse methods of mobile and contactless payments, and QR code-based solutions.

Complementary software integrations, virtual international bank account numbers (IBAN), integrated mobile point-of-sale (POS)

solutions, risk management tools, and robust reporting and analytics capabilities augment our platform’s offerings.

Our

payment services seamlessly integrating e-money remittance solutions within the global marketplace, spanning open banking and

credit card processing to wire transfers. Our unique Software-as-a-Service (SaaS) model empowers clients to focus on their core

operations and sales while we handle the intricate aspects of payment processing. This streamlined approach facilitates efficient

onboarding, elevates customer retention, and cultivates new revenue streams.

Our

vision transcends boundaries as we aspire to cement our position as a global leader in the payments and banking sphere. Our team,

comprising seasoned experts across operations, technology, sales, legal, compliance, and more, forms the backbone of our enterprise.

The

crux of our vision lies in simplifying and automating global fund transfers while upholding the highest standards of security.

We endeavor to furnish merchants with an all-encompassing Merchant Payment Ecosystem (MPE), a unified platform catering to their

diverse payment needs. Our technology leverages the Gateway Cashier Technology to deliver unparalleled services.

Our

diverse merchant base ranges from small to medium-sized enterprises, or SMEs, to large enterprises, spanning sectors such as hospitality,

e-gaming, consulting, retail, marketing, and e-commerce. While we are rooted in the SaaS framework, our belief in democratizing

technology has led us to offer an initial free platform, generating revenue through value-added services.

Our

revenue streams encompass processing fees based on payment volumes, a hybrid model featuring fixed transaction fees and

monthly charges, and diverse layers that allow us to cross-sell services and nurture lasting client relationships. Currently,

we derive all our revenues from our operating subsidiaries based in Malaysia and the United Kingdom. For the fiscal year

ended December 31, 2023, we recorded revenue of $2,420,184, with 81.9% of such revenue being derived from our operating

subsidiaries in the United Kingdom and the remaining 18.1% from our Malaysian subsidiaries. We also recognized a net loss of

$40,662,716 during the fiscal year ended December 31, 2023, primarily resulting from an impairment loss of $39,136,871 (see

Note 5 to the consolidated financial statements for a discussion of the Company’s Goodwill).

In

the competitive landscape, our distinct layers constitute the heart of our approach, underpinned by a commitment to exemplary

customer service. We understand the nuanced needs of various merchants and have meticulously curated layers tailored to their

requirements, including cutting-edge technology, diverse payment processing and integrated banking. These layers collectively

form the bedrock of our operations, fostering seamless merchant experiences and propelling us to the forefront of the industry.

As

we chart our course, we stand poised to not only cater to our diverse clientele but to exceed their expectations. Our pursuit

of excellence remains unwavering as we continue to innovate, expand our offerings, and forge new partnerships to reshape the payments

and banking landscape.

Corporate

History and Structure

We

were incorporated in the state of Nevada on November 19, 2013 as “Albero, Corp.” On January 8, 2016, we changed our

name to “Vitaxel Group Limited.” On March 2, 2022, we changed our name to “HWGC Holdings Limited.” On

May 16, 2023, we changed our name to “Fintech Scion Limited.”

On

July 21, 2022, we entered into a share exchange agreement with FintechCashier Asia P.L.C. (formerly known as HWGG Capital P.L.C.),

a Labuan company (“FintechAsia”), and all of the shareholders of FintechAsia pursuant to which all shareholders of

FintechAsia irrevocably agreed to transfer and assign to the Company all FintechAsia’s shares held by the shareholders in

exchange for newly issued shares of the Company’s common stock, par value $0.001 per share. Following the closing of the

share exchange on November 15, 2022, FintechAsia became a wholly-owned subsidiary of the Company.

On

August 9, 2022, we entered into another share exchange agreement with Fintech Scion Limited (“Fintech”), a private

limited company incorporated in the United Kingdom, and all of the shareholders of Fintech pursuant to which All shareholders

of Fintech irrevocably agreed to transfer and assign to the Company all of Fintech’s shares held by such shareholders in

exchange for an aggregate of 101,666,667 newly issued shares of the Company’s common stock, par value $0.001 per share.

Following the closing of the share exchange on November 30, 2022, Fintech became a wholly-owned subsidiary of the Company.

On

December 30, 2022, we entered into a stock purchase agreement with Mr. Leong Yee Ming, the previous Chief Executive Officer of

the Company (the “Purchaser”), pursuant to which the Company sold to the Purchaser all issued and outstanding shares

of Aelora Sdn Bhd (“ASB” and formerly known as Vitaxel Sdn Bhd) and Vitaxel Online Mall Sdn Bhd (“Vionmall”,

and together with ASB, the “Former Subsidiaries”). The Company sold the Former Subsidiaries for an aggregate purchase

price of RM4,500,002 (the “Purchase Price”), with RM4,500,000 allocated for the purchase price of ASB and RM2 for

the purchase of Vionmall. The Purchase Price was paid by the Purchaser’s assumption of a certain amount of intercompany

debt owed by the Company to ASB. Pursuant to the terms of the agreement, the Company and ASB assigned, and the Purchaser’s

assumed, that portion of intercompany debt equal to the Purchase Price and in full satisfaction of the Purchase Price. Following

the completion of the disposal of the Former Subsidiaries to the Purchaser on the same day, ASB and Vionmall ceased to be the

subsidiaries of the Company as of December 30, 2022.

On

October 11, 2023, we entered into an Asset Conveyance Agreement (the “Purchase Agreement”) with CICO Digital Solutions

Limited, a British Columbia company (“CICO” and a related party company that has a common control by a major shareholder

of the Company). The Purchase Agreement provided for the acquisition by the Company of substantially all of the assets of CICO

(the “Assets”) related to CICO’s business of providing a service platform and software application for payment

services from CICO. As consideration for the transfer and sale of the Assets, the Company issued CICO 100,000,000 restricted shares

of common stock of the Company, par value $0.001 per share (the “Shares”).

On

December 27, 2023, the Company and CICO mutually and voluntarily agreed to unwind the transaction contemplated by the Purchase

Agreement. Upon termination, each of the parties to the Purchase Agreement were relieved of their respective rights, liabilities,

expenses and other obligations under the Purchase Agreement. In connection therewith, CICO transferred the Shares back to the

Company for cancellation upon receipt. The Shares were cancelled and removed from the Company’s issued and outstanding shares

of common stock on January 30, 2024.

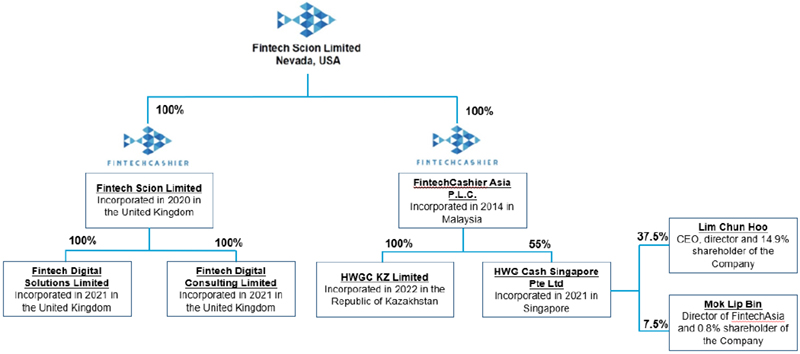

The

diagram below illustrates our corporate structure:

*HWGC

KZ Limited and HWG Cash Singapore Ptd Ltd. are dormant.

Range

of Services

Our

comprehensive suite of services is carefully tailored across six strategic business areas, each designed to cater to the distinct

needs of our diverse clientele. These business areas represent the core of our operations, enabling us to offer a seamless and

integrated payment ecosystem to merchants worldwide.

| |

1. |

Payment Services

Provider (PSP): Operating under the brand name FintechCashier, we excel as a PSP, facilitating international payment solutions

for merchants by collaborating with card acquiring banks and alternative payment solution providers. Our expertise in this

domain empowers merchants to effortlessly navigate the complexities of cross-border transactions. |

Our

PSP service provides an intermediary payment platform to facilitate efficient payment transactions between merchants. Users of

our PSP platform have the ability to initiate payment to a supplier, or collect payment from a customer. These payments are processed

through our banks with all fund movement reflected in the user’s individualized e-wallet. Our PSP service offers both merchant

and supplier users the flexibility to choose their preferred currency when initiating and collecting payment, respectively. We

collect a fee from a user’s e-wallet for each completed transaction. Therefore, users must have sufficient funds to complete

each payment transaction and pay our fee prior to being able to complete the transaction.

Users

have the option of utilizing our PSP services through an already established API operating system, e-mail and mobile messaging

services, or in tandem with our Business Accounts service as more fully described below.

| |

2. |

Business Accounts:

Our specialized business account services extend across diverse industries and currencies, offering tailored solutions

to corporate entities. We assist our clients in establishing and managing corporate accounts, ensuring they can seamlessly

operate on a global scale, irrespective of their sector. |

Our

Business Account services establish the operating system needed to utilize our PSP service platform, including use of our e-wallet

feature allowing users to monitor funds, track payment transactions in real time and review transaction history. Users of our

Business Accounts services experience our full payment service ecosystem to seamlessly integrate our PSP service platform and

operating system to maximize the potential customer experience. We charge an annual fee for our Business Accounts services.

| |

3. |

SEPA & SWIFT

Payments: Our proficient settlement services encompass SEPA and SWIFT payments, enabling swift and secure fund transfers

for merchants and business clients across international banks. Our streamlined process involves efficient inter-account fund

transfers, culminating in the issuance of SWIFT or SEPA payments. |

Our

PSP service platform utilizes SEPA and SWIFT payments through our partner banks to carry out all payment transactions. We do not

currently have direct access to SEPA or SWIFT payments and rely on our bank partners to utilize these services to ensure our customers

experience smooth and secure transfers of funds.

We

do not charge an additional fee for incoming or outgoing SEPA or SWIFT payment services as the fee is included in our PSP service

fees. We absorb all fees charged by our partner bank for use of SEPA or SWIFT payments.

| |

4. |

Foreign Exchange

(FX) Conversion: Through strategic partnerships, we provide foreign exchange payment solutions, facilitating seamless

currency conversion for clients. Whether it’s settling invoices, processing payrolls, or making payments for goods and

services, our FX conversion services ensure seamless and efficient transactions. |

Our

FX conversion services provide foreign currency conversion services for our customers. Through third party brokers, users of our

PSP services or Business Accounts services are able to exchange currency, provided they have the sufficient balance in their e-wallet

of in our designated bank account to fund the conversion transaction.

We

require users of our FX conversion services to inform us of the currency they intend to convert, at which point we determine the

fees associated with such conversion, including the exchange rate fee, our fee and other transaction-related fees such as bank

charges. Upon the user’s agreement to the total fee amount, we instruct our brokers to carry out the exchange. These transactions

typically take 1-2 days, but may take as long as one week depending on the customer requests or a disagreement on the exchange

rate.

Our

customers are not required to register with our brokers to utilize our FX conversion services, as the brokers work with us directly.

Our fees are fixed and do not include mark-up fees on the exchange rate. Any mark-up fees on the exchange rate would be added

by our brokers and passed on to the customers.

| |

5. |

Acquirer Services:

As a global player, we specialize in offering debit and credit card acquiring services to online merchants across the

globe. Our network extends through PSPs and Independent Sales Organizations, ensuring a robust and secure payment acceptance

framework. |

| |

6. |

Whitelabelling:

Our whitelabelling service presents a fully customizable merchant back office platform, complete with comprehensive access

to an array of banking payment methods. This tailored solution empowers merchants to seamlessly integrate their operations

within a unified framework. |

Within

these strategic business areas, we have structured three distinct service layers, all seamlessly integrated within a single platform.

This holistic approach empowers merchants to expand their operational horizons, fueling their growth within a unified payment

ecosystem.

Fintech

Digital Solution Limited is a software technology provider combining hundreds of payment providers and payment methods under one

platform. In response to updated regulatory compliance mandates from the United Kingdom, potentially impacting our operations

as of December 2023, our management has opted to discontinue the EMD agency service. However, our management team remains committed

to collaborating with various firms across multiple jurisdictions where regulatory licenses or registrations are essential for

our operations. We are actively engaging with licensed and regulated entities on a referral basis to ensure seamless continuity

of our services including Business Accounts, SEPA & SWIFT Payments and Foreign Exchange (FX) Conversion services and maintaining

our commitment to delivering reliable payment solutions without any interruption.

Integrated

Solutions and Advanced Capabilities

Our

Merchant Payment Ecosystem (MPE) is grounded in rigorous Know-Your-Customer (KYC) protocols and fortified by robust fraud and

risk management tools. Certified compliance with the European Union’s General Data Protection Regulation (GDPR) and the

Payment Card Industry Data Security Standard (PCI DSS) Level 1 underscores our commitment to safeguarding sensitive data. Operating

at the nexus of multiple currencies and nations, we seamlessly facilitate payment services, encompassing transactions, payouts,

and settlements.

Our

ethos is rooted in agility and innovation, with a steadfast dedication to swift and precise operations. Our service portfolio

extends across the entire end-to-end payment continuum, spanning clients, merchants, PSP providers, affiliates/partners, and harmonious

integration with acquiring banks and solution providers. This inclusive approach ensures seamless interactions across the global

payments landscape.

Powered

by our cutting-edge technology and advanced payment solutions, businesses can manifest their service visions without being constrained

by the intricacies of payment plan budgeting. Our meticulously designed layers cater to diverse merchant needs, ensuring a tailored

fit for every scenario. The FintechCashier onboarding engine serves as a discerning guide, meticulously analyzing applications

and seamlessly aligning merchants with the most pertinent service layer or offering.

| |

a) |

Technology Layer:

At the vanguard of our architecture is the Technology Layer, meticulously engineered to target key verticals within the

market. Anchored by a PCI DSS Level 1 certified payment gateway, recognized by industry titans VISA and MasterCard, this layer

seamlessly integrates a plethora of service providers. From credit card acquirers to issuers, corporate accounts to open banking,

transaction monitoring to Know-Your-Customer and Know Your Business compliance, our technology layer converges diverse functionalities

into a cohesive whole. |

| |

b) |

Payments Layer:

Central to our prowess is the Payments Layer, facilitated through subsidiaries under the FintechCashier umbrella. Endowed

with an array of financial and regulatory licenses, we operate as a Merchant of Record (MOR), vested with the authority and

accountability to oversee a gamut of processing accounts. This dynamic allows us to seamlessly onboard small merchants, expertly

managing their comprehensive payment requisites. Notably, our MOR status holds us responsible for maintaining merchant accounts,

processing payments, managing credit card processing fees, and orchestrating seamless compliance with PCI DSS. Our proactive

stance extends further as we embrace the role of a Payment Initiation Service Provider (PISP) under PSD2. This enables us

to extend direct banking services through an open banking infrastructure, a feat made possible through strategic partnerships

and technological integrations. By deftly incorporating open banking functionality within our payment gateway, we have etched

our place as a leader within the payment stack, a multifaceted assortment of technologies that coalesce to offer a comprehensive

payment solution. |

Our

payment ecosystem comprises essential components that collaborate seamlessly to facilitate secure and efficient electronic transactions.

These integral elements collectively underpin businesses’ ability to accept and process electronic payments from customers.

Whether provided by a Payment Services Provider (PSP) as an integrated solution or crafted in-house by merchants, these components

are essential building blocks within the payment landscape:

| |

1. |

Payment Gateway:

Serving as a crucial bridge, the payment gateway connects a merchant’s website or mobile app to the payment processor.

This pivotal link ensures that customers can make secure transactions using their credit or debit cards, thus enabling seamless

and safe payment experiences. |

| |

2. |

Payment Processor:

The heartbeat of the payment process, the payment processor assumes the pivotal role of orchestrating the actual payment

transactions. It encompasses the full spectrum of tasks, from authorizing the transaction to settling it with the customer’s

bank or financial institution, culminating in the successful completion of the payment. |

| |

3. |

Fraud Detection

and Prevention: These vigilant components stand guard against fraudulent activities, functioning as a protective shield

for both merchants and customers. By meticulously scrutinizing transactions and adhering to industry regulations, these components

ensure the integrity and security of each payment. |

| |

4. |

Risk Management:

A robust risk management framework is integral to navigating the complexities of electronic payments. These components

proactively manage and mitigate risks associated with electronic transactions, including challenges such as chargebacks and

potential fraud. By fostering a secure environment, risk management safeguards the payment ecosystem’s stability. |

| |

5. |

Payment Methods:

Diverse and adaptable, payment methods encompass a spectrum of options that customers can leverage to initiate transactions.

Ranging from credit and debit cards to e-wallets and bank transfers, this versatility empowers customers with convenient choices

for conducting transactions. |

Collectively,

these interwoven elements coalesce to form the foundation of an efficient and secure payment stack. This stack can be seamlessly

delivered as a comprehensive solution by a PSP or meticulously assembled in-house by merchants, utilizing an assortment of specialized

tools. Embracing these core components empowers businesses to confidently engage in electronic payment processing, enhancing their

capacity to provide exceptional service while maintaining robust security measures.

| |

c) |

Banking Layer:

FintechCashier’s technology extends to our Banking Layer, where we seamlessly integrate virtual bank accounts into our

payment offerings. This strategic augmentation encompasses both “pay-in” and “pay-out” solutions,

catering to diverse corporate needs. For “pay-in” scenarios, our system facilitates effortless fund collection

from both individuals and corporate entities, accommodating various payment methods such as traditional bank transfers, credit

or debit card payments, and popular online platforms like PayPal. Conversely, our “pay-out” capabilities empower

businesses to efficiently disburse funds to their clients, whether they are individuals or corporations. Our automated onboarding

process ensures merchants can swiftly access bank accounts and payment processing, streamlining operations and enhancing efficiency. |

These

pivotal layers form the cornerstone of FintechCashier’s holistic approach, aimed at harnessing the full potential of the

market. By offering a comprehensive spectrum of efficient payment services, we empower our customers with a range of benefits,

including:

| |

● |

Currency Support

and Optimized FX Conversion: Seamlessly supporting multiple currencies and optimizing foreign exchange conversion, we

enable businesses to transcend geographic boundaries and operate on a global scale. |

| |

● |

Multilingual

Support: Our platform’s multilingual capabilities create avenues to explore new markets, fostering expansion opportunities

for our clients. |

| |

● |

Always-On Management

Portal: Anchored by high availability, cloud-based architecture, and real-time performance, our user-friendly management

portal ensures uninterrupted service continuity, cultivating customer loyalty. |

| |

● |

Comprehensive

Reporting and Analysis: Clients gain access to robust reporting tools, enabling them to monitor service performance, support

cash flow analysis for various transaction types, and manage chargeback and retrieval disputes. |

| |

● |

Experienced Team

Support: Our seasoned team provides unparalleled support, guiding clients through the intricacies of the payment landscape. |

| |

● |

Efficient Onboarding

and Integration: Through a unified platform, we expedite onboarding and integration processes, enabling swift deployment

of new services without hindrances or budgetary constraints. |

| |

● |

Secured Accessibility:

Clients enjoy secure access to our services through a built-in portal, ensuring the confidentiality and integrity of sensitive

information. |

| |

● |

Hosted Payment

Page (HPP): Our platform’s integration of a hosted payment page streamlines the checkout process, facilitating “one-click-checkout”

simplicity. |

Our

competitive edge as a comprehensive payment hub eliminates the need for customers to seek disparate service providers. We cater

to every facet of merchants’ payment solution requirements, providing an encompassing gateway to manage operations and relationships.

Services like KYC and AML compliance, customer relationship management (CRM), transaction monitoring, and comprehensive reporting

stand testament to our commitment to ensuring seamless, secure, and efficient payment solutions for merchants across diverse industries.

Diverse

Customer Base

We

cater to a wide array of customers, embracing:

| |

● |

Enterprises and Organizations: Our services

resonate with entities across all categories, seeking to optimize fund transfer costs while ensuring swift and secure transactions. |

| |

● |

Online Businesses: For online enterprises,

we present an effective end-to-end solution for the intricate realm of online selling. This encompasses seamless payment collection

and streamlined cross-border transactions, enabling businesses to flourish on a global scale. |

| |

● |

Specialized Online Businesses: A distinctive

facet of our customer spectrum encompasses specialized online businesses facing challenges in establishing and maintaining

physical bank accounts across the diverse territories they operate in. This category is particularly relevant for Small and

Medium-sized Enterprises (SMEs) and online businesses. |

In

stark contrast to relying on a handful of major customers for our revenue stream, our approach emphasizes a diverse customer portfolio.

This strategic stance fortifies our stability and resilience in the market, safeguarding against over-dependence on any single

client.

Operational

Excellence and Support Services

Our

operational infrastructure is meticulously crafted to deliver unparalleled customer experiences across the entire payment ecosystem.

Our suite of operations and support services encompasses:

| |

● |

Merchant Underwriting: Our adept merchant

underwriting team meticulously evaluates applications and assesses risks for new merchants. By focusing on markets with high

card-present volume and minimal fraud and chargeback losses, our underwriting strategy offers low-risk profile merchants an

expedited activation, augmenting their customer journey. |

| |

● |

Merchant Onboarding and Activation: Through

our user-friendly web-based portal, business proprietors can swiftly sign up for a merchant account. For enterprises, our

dedicated merchant onboarding and activation team collaborates closely with partners to facilitate a seamless transition from

sales to implementation and activation. Our streamlined process and automated approvals enable rapid and frictionless onboarding,

empowering us and our partners with accelerated speed-to-market. In fact, even the most intricate and sizable merchants can

be onboarded within a mere 48 hours of application submission. |

| |

● |

Merchant Training: We furnish merchants

with comprehensive training materials through a dedicated department and content delivery platform, ensuring their adept utilization

of our offerings. |

| |

● |

Merchant Risk Management: Our vigilant

risk management operations entail ongoing monitoring of merchant accounts. Supported by dedicated security and regulatory

assistance (including compliance support, vulnerability scanning, system monitoring, and breach aid), our systems are configured

to automatically surveil activities warranting heightened scrutiny. This proactive approach mitigates losses attributed to

fraud and defaults. |

| |

● |

Merchant Support: Operating round the

clock, seven days a week, 365 days a year, our merchant support team is unwavering in its dedication to addressing merchant

inquiries. Whether pertaining to systems integration or technical solutions, our team delivers expert customer support. Additionally,

our cadre of merchant account specialists guides merchants through the entire payment acceptance journey, from onboarding

to settlements and reporting. With a resolute focus on swift issue resolution, we provide unparalleled payment expertise and

support, reducing repeat calls and enhancing operational efficiency. |

| |

● |

Software Integrations and Compliance Management:

A dedicated team of engineers and technical support staff oversees software integrations and ensures full compliance with

security and regulatory requisites. This encompasses support for PCI and Payment Application Data Security Standard compliance,

along with system integration and configuration guidance. |

| |

● |

Partner Support: Our committed support

teams collaborate closely with software providers to address inquiries or issues pertaining to the integration of our products

and solutions into their software suites. We strive for comprehensive issue resolution by harmonizing relevant departments,

optimizing partner support. We also extend assistance in resolving matters encompassing our partners’ entire merchant

portfolio or incidents affecting individual merchants. |

| |

● |

Partner Services: Through our partner-centric

customer relationship management system, partners can track the real-time activation progress of new merchant accounts. This

comprehensive system empowers partners to monitor their merchant portfolio, encompassing commissions, residual payments, and

even support interactions, all in a precise and real-time manner. Automation has been seamlessly woven into these processes

to ensure an impeccable experience and heightened financial efficiency. |

Business

Strategy and Revenue Generation

Over

the forthcoming five years, Fintech Scion and its subsidiaries are resolutely committed to expanding market presence and becoming

a preeminent force in the Banking-as-a-Service realm and a global in payment solutions. This entails broadening our current array

of services and licenses to establish an even more extensive and comprehensive payment ecosystem.

A

pivotal facet of this strategy involves strategic acquisitions and investments within the payment landscape. This approach, as

envisioned by our directors, will foster rapid revenue growth while maintaining prudent control over operating costs.

Our

overarching strategy encompasses the following elements:

| |

● |

Robust Software

Model: We are dedicated to crafting a robust software model that aligns seamlessly with the diverse requirements of businesses

of varying scales. |

| |

● |

Flexibility in

Product Offerings: Flexibility remains at the core of our product offerings, allowing us to tailor custom solutions that

precisely cater to our clients’ unique needs. |

| |

● |

Market Leadership

and Innovation: As a market leader, we are deeply attuned to the evolving marketplace. Continuous research and development

will be an integral part of our approach, allowing us to integrate cutting-edge products into our business portfolio and remain

ahead of industry trends. |

| |

● |

FintechCashier’s

Vision: Our vision for FintechCashier is centered on empowering merchants worldwide to expand their businesses. This will

be achieved through state-of-the-art payment technology coupled with financial services that are transparent and free of hidden

costs. Our motto is encapsulated in the mantra “One Application, One Integration, Pay as You GO.” |

Our

business cases are compelling, with clear value propositions for various segments:

| |

● |

SMEs: Simplifying

global payment acceptance through a single integration, streamlining operations and enhancing their growth prospects. |

| |

● |

Fintechs: Amplifying

the capabilities of fintech companies, enabling them to construct more robust and scalable products. |

| |

● |

PSPs/Card Acquirers:

Elevating these entities into more accessible providers, offering a comprehensive platform with over 280 API integrations

and simplified onboarding processes. |

Value

Addition to Customers

We

augment the value for our customers in the following ways:

| |

● |

SMEs: Simplifying

global payment acceptance through a single integration, reducing operational complexity. |

| |

● |

Fintechs: Enabling

the expansion of their offerings, leading to the creation of more advanced and scalable products. |

| |

● |

PSPs/Card Acquirers:

Transforming these entities into easily accessible providers with a comprehensive platform, streamlined onboarding, and

extensive API integrations. |

Marketing

Approach

Our

marketing initiatives encompass a diverse range of channels, ensuring broad and effective outreach:

| |

● |

Direct Sales:

Our direct sales team employs a multifaceted approach, encompassing techniques like cold calling, networking, and in-person

presentations. They are driven to generate leads and secure sales, while also nurturing customer relationships and collecting

feedback to inform product development. |

| |

● |

Social Media:

Our marketing team fosters brand awareness on prominent social media platforms, including Facebook, Twitter, and LinkedIn,

enabling us to reach a vast audience. |

| |

● |

Website and Mobile

Optimization: A meticulously optimized website and mobile interface are designed to enhance user experience, foster easy

navigation, and improve search engine visibility. |

| |

● |

Adwords and Online

Advertising: We leverage pay-per-click (PPC) advertising, cost-per-thousand advertising, and site-targeted advertising

to effectively promote our offerings through text, banner, and rich-media ads. |

| |

● |

Partnerships:

Collaborations with established banks and financial institutions serve as a conduit to reach a broad spectrum of businesses

annually. |

| |

● |

Affiliate Program:

An affiliate program with a commission-based structure is designed to attract new customers through affiliates, expanding

our customer base. |

Industry

Opportunity

We

believe the fintech industry is attractive for a number of reasons:

| |

● |

Large Total Addressable Market: The

financial services industry represents a significant part of the economy. According to a research report by The Business Research

Company, a global market research and consulting firm, the financial services market has experienced significant growth in

recent years. The firm anticipates that the market will continue to expand, projecting a growth from $31.1 trillion in 2023

to $33.5 trillion in 2024, with a compound annual growth rate (“CAGR”) of 7.7%. Furthermore, it is forecasted

to reach $44.9 trillion by 2028, with a CAGR of 7.6%. |

| |

(1) |

https://www.thebusinessresearchcompany.com/report/financial-services-global-market-report |

Broad

Universe of Potential Targets: The total global fintech market attained a value of more than $140 billion in 2023, and

expected to grow at a CAGR of 12% to reach over $270 billion by 2027(2).

| |

(2) |

https://beinsure.com/ranking/biggest-fintech-unicorn-startups-in-world/ |

| |

● |

Pace of Growth

and Innovation Across Subsectors: In fintech, we believe the pace of innovation in the private and public sectors is accelerating.

There has been significant disruption and change in the delivery of financial services across many subsectors in recent years,

including, among others: |

| |

○ |

APIs, including

open banking and account connectivity; |

| |

○ |

Big data, analytics

and information technology; |

| |

○ |

Digital assets and

blockchain technology; |

| |

○ |

Exchanges and trading

platforms, including capital markets technology; |

| |

○ |

Insurance technology

and services (“insurtech”); |

| |

○ |

Lending and underwriting

technology; |

| |

○ |

Real estate, mortgage

and prop tech services (“proptech”); |

| |

○ |

Regulatory technology

for financial services (“regtech”); |

| |

○ |

Risk technology,

including fraud and identity protection and cyber and data security; and |

| |

○ |

Wealth management

technology (“wealthtech”). |

| |

● |

Accelerated Adoption

Rate for Innovation in Financial Services: Over the last decade, fintech has steadily increased its share of the global

economy, and the financial services industry has become one of the largest consumers of technology worldwide, spending over

$500 billion on technology annually. These adoption levels continue to benefit from robust secular tailwinds including the

growth in digital commerce, the proliferation of mobile technology, the ubiquitous acceptance of digital payments and continuous

technological advancement, positioning the sector for long-term growth. |

| |

● |

Attractive for

Public Markets: Over the past few years, the public market’s demand for high-growth fintech prospects has increased,

as public market investors continue to seek access to private fintech companies that offer disruptive technologies and solutions. |

Market

Opportunity

In

general, FinTech-as-a-Service (FaaS) is gaining attention, leveraging modern technology to aid multiple segments, including Lending,

Credit, and Payments, in resolving long-standing challenges. Businesses are increasingly turning to FaaS to optimize their processes

and increase efficiency. Customer satisfaction and customer retention are two compelling reasons why numerous companies are now

adopting FaaS. Legal compliance and optimal security mechanisms are additional benefits. Using FaaS, financial and non-financial

companies can automate their financial processes and offer customers hassle-free access to credit and services.

FaaS

automates financial processes and makes them efficient, eliminates cumbersome paperwork, and reduces human intervention. Robotic

automation frees up working hours for more valuable tasks. The result—streamlined workflows, thorough document analyses,

and quick results. By integrating FaaS, companies can significantly reduce the turnaround time for the entire financial process

and improve customer experience.

We

believe FaaS has tremendous growth potential with its ability to bridge the gap between traditional legacy structures and next-generation

technology. We predict both financial and non-financial companies will continue to adopt FaaS in effort to improve financial processes,

reduce human intervention and increase personalization.

In

a recently published Financial Services Global Market Report 2024 published by The Business Research Company, it is predicted

that the global financial services market will grow from $31.14 trillion in 2023 to $44.93 trillion in 2028 (CAGR

7.6%).

FinTech-as-a-Service

(FaaS) exhibits immense growth potential and is gaining considerable traction. By harmonizing traditional and modern elements

and bridging the divide between legacy systems and cutting-edge technology, FaaS provides insights into the evolution of the hybrid

future. Furthermore, as businesses strive to enhance financial operations, minimize manual intervention, and enhance personalization,

FaaS is poised for rapid and enduring adoption across financial and non-financial sectors in the foreseeable future.

We

believe our three layer diversified approach in the payment space minimizes our reliance on any one market to to best position

our growth opportunities.

| |

● |

Technology Layer

– Payment Gateway Market – according to an April 2024 report published by MarketandMarkets Research Pvt. Ltd,

there was a market size of$23.3 billion in 2023 and is expected to grow to $28.8 billion by 2029, with a CAGR of 12.9%. |

| |

● |

Banking Layer –

Digital Payment Market – According to an October 2023 report published by MarketandMarkets Research Pvt. Ltd, there

was a market size of $111.2 billion in 2023 and is expected to grow to 193.7 billion by 2028, with a CAGR of 11.8%. |

| |

● |

Payment Layer –

Payment Processing Market – According to an July 2023 report published by MarketandMarkets Research Pvt. Ltd, there

was a market size of $103.2 billion in 2023 and is expected to grow to $160.0 billion by 2028, with a CAGR of 9.2%. |

The

below table summarizes these market opportunities:

| |

2023 |

2028 |

2029 |

CAGR |

| Payment

Gateway Market |

$23.3

billion |

- |

$48.4

billion |

12.96% |

| Digital

Payment Market |

$111.2

billion |

$193.7

billion |

— |

11.80% |

| Payment

Processing Solutions Market |

$103.2

billion |

$160.0

billion |

— |

9.2% |

We

believe we will be able to maintain and even increase our market share revenues over the next two to three years based on the

expected growth of the overall market.

Acquisition

Strategy

We

intend to acquire one or more high-quality businesses that can generate attractive, risk-adjusted returns for shareholders. To

that end, our acquisition and value creation strategy is to identify, acquire and, after our initial business combination, enhance

the growth of a company in the fintech industry that complements our experience and expertise.

We

believe that the following value propositions will allow us to source businesses which will not only bring value to us but also

bring transformative change and exponential growth to them :

| |

● |

Best-in-Class

Sourcing Capabilities: our global network of relationships with financial services and technology company CEOs, founders,

boards of directors and private equity sponsors provides us with a proprietary avenue for sourcing target businesses. |

| |

● |

Deep Insights

Across the Fintech Industry: We believe that our management team’s extensive knowledge of the fintech industry,

understanding of economic and regulatory nuances globally and expertise in technology go-to-market strategies and business

models provide us with a differentiated ability to evaluate promising target businesses. |

| |

● |

Proven Experience

in Consummating Transactions: We believe that our management team’s extensive mergers and acquisitions experience,

with a distinct reputation for navigating transaction complexities, is a significant advantage. Our management team have demonstrated

ability to negotiate and structure transactions, evaluate corporate strategies, access growth capital and develop appropriate

capital structures. |

| |

● |

Significant Financial

Services and Technology Investment Experience: our management team has extensive experience in analyzing attractive financial

services and technology investments in individual equity opportunities. We believe that our proficiency in this area can help

us evaluate compelling business combination opportunities. |

Fintech

Scion will actively pursue mergers and acquisitions to elevate the performance of our portfolio businesses. Our primary aim is

to drive their growth by expanding their size, capabilities, and market presence in their respective industries. These strategic

initiatives are designed to unlock synergies and enhance overall performance. Furthermore, we will allocate resources to develop

scalable platforms that empower our portfolio businesses, enabling them to achieve accelerated growth.

Competitive

Strengths

FintechCashier

competes with a range of providers, each of whom may provide a component of our offering, but do not provide an integrated offering

capable of solving complex business challenges for software partners and merchants. For certain services and solutions, including

end-to-end payments, we compete with third-party payment processors and integrated payment providers.

The

competitive landscape across the three layers are shown in the table:

| Layer |

Market

Sector |

Competitors |

| Technical |

Payment

Gateway Market |

Crassula,

Contis, Mambu, Sblock |

| Payments |

Payment

Processing Market |

Nuvei,

Worldpay, Checkout, Ayden |

| Banking |

Digital

Payment Market |

Solaris