| 19

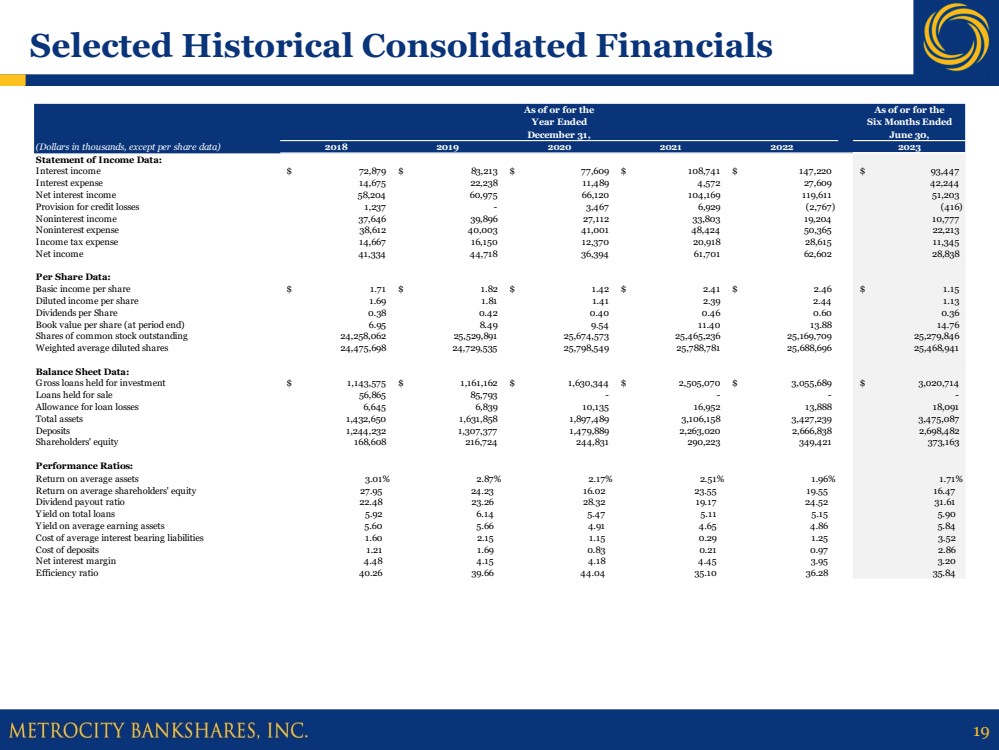

Selected Historical Consolidated Financials

As of or for the As of or for the

Year Ended Six Months Ended

December 31, June 30,

(Dollars in thousands, except per share data) 2018 2019 2020 2021 2022 2023

Statement of Income Data:

Interest income $ 72,879 $ 83,213 $ 77,609 $ 108,741 $ 147,220 $ 93,447

Interest expense 14,675 22,238 11,489 4,572 27,609 42,244

Net interest income 58,204 60,975 66,120 104,169 119,611 51,203

Provision for credit losses 1,237 - 3,467 6,929 (2,767) (416)

Noninterest income 37,646 39,896 27,112 33,803 19,204 10,777

Noninterest expense 38,612 40,003 41,001 48,424 50,365 22,213

Income tax expense 14,667 16,150 12,370 20,918 28,615 11,345

Net income 41,334 44,718 36,394 61,701 62,602 28,838

Per Share Data:

Basic income per share $ 1.71 $ 1.82 $ 1.42 $ 2.41 $ 2.46 $ 1.15

Diluted income per share 1.69 1.81 1.41 2.39 2.44 1.13

Dividends per Share 0.38 0.42 0.40 0.46 0.60 0.36

Book value per share (at period end) 6.95 8.49 9.54 11.40 13.88 14.76

Shares of common stock outstanding 24,258,062 25,529,891 25,674,573 25,465,236 25,169,709 25,279,846

Weighted average diluted shares 24,475,698 24,729,535 25,798,549 25,788,781 25,688,696 25,468,941

Balance Sheet Data:

Gross loans held for investment $ 1,143,575 $ 1,161,162 $ 1,630,344 $ 2,505,070 $ 3,055,689 $ 3,020,714

Loans held for sale 56,865 85,793 - - - -

Allowance for loan losses 6,645 6,839 10,135 16,952 13,888 18,091

Total assets 1,432,650 1,631,858 1,897,489 3,106,158 3,427,239 3,475,087

Deposits 1,244,232 1,307,377 1,479,889 2,263,020 2,666,838 2,698,482

Shareholders' equity 168,608 216,724 244,831 290,223 349,421 373,163

Performance Ratios:

Return on average assets 3.01% 2.87% 2.17% 2.51% 1.96% 1.71%

Return on average shareholders' equity 27.95 24.23 16.02 23.55 19.55 16.47

Dividend payout ratio 22.48 23.26 28.32 19.17 24.52 31.61

Yield on total loans 5.92 6.14 5.47 5.11 5.15 5.90

Yield on average earning assets 5.60 5.66 4.91 4.65 4.86 5.84

Cost of average interest bearing liabilities 1.60 2.15 1.15 0.29 1.25 3.52

Cost of deposits 1.21 1.69 0.83 0.21 0.97 2.86

Net interest margin 4.48 4.15 4.18 4.45 3.95 3.20

Efficiency ratio 40.26 39.66 44.04 35.10 36.28 35.84 |