Filed by Lotus Technology Inc.

Pursuant to Rule 425 under the

Securities Act of 1933,

as amended, and deemed filed pursuant

to Rule 14a-12

under the Securities Exchange Act of

1934, as amended

Subject Company: L Catterton Asia Acquisition

Corp

Commission File No.: 001-40196

|

INVESTOR PRESENTATION JULY 2023 |

|

2 THIS PRESENTATION AND ITS CONTENTS ARE CONFIDENTIAL AND ARE NOT FOR RELEASE, REPRODUCTION, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, TO ANY OTHER PERSON OR IN OR INTO OR FROM ANY JURISDICTION WHERE SUCH RELEASE, REPRODUCTION, PUBLICATION OR DISTRIBUTION IS UNLAWFUL. PERSONS INTO WHOSE POSSESSION THIS PRESENTATION COMES SHOULD INFORM THEMSELVES ABOUT, AND OBSERVE, ANY SUCH RESTRICTIONS. THIS PRESENTATION IS NOT AN OFFER OR AN INVITATION TO BUY, SELL OR SUBSCRIBE FOR SECURITIES. About this Presentation This Presentation has been prepared by L Catterton Asia Acquisition Corp (“SPAC” or “LCAA”) and Lotus Technology Inc. (the “Company” or “Lotus Technology”) in connection with a potential business combination involving SPAC and the Company (the “Transaction”). This Presentation is preliminary in nature and solely for information and discussion purposes and must not be relied upon for any other purpose. For the purpose of this notice, “Presentation” shall mean and include the slides that follow, the oral presentation of the slides by members of SPAC or the Company or any person on their behalf, the question-and-answer session that follows that oral presentation, copies of this document and any materials distributed at, or in connection with, that presentation. By accepting this Presentation, participating in the meeting, or by reading the Presentation slides, you will be deemed to have (i) acknowledged and agreed to the following conditions, limitations and notifications and made the following undertakings, and (ii) acknowledged that you understand the legal and regulatory sanctions attached to the misuse, disclosure or improper circulation of this Presentation. This Presentation does not constitute (i) an offer or invitation for the sale or purchase of the securities, assets or business described herein or a commitment of the Company or SPAC with respect to any of the foregoing, or (ii) a solicitation of proxy, consent or authorisation with respect to any securities or in respect of the Transaction, and this Presentation shall not form the basis of any contract, commitment or investment decision and does not constitute either advice or recommendation regarding any securities. The Company and SPAC expressly reserve the right, at any time and in any respect, to amend or terminate this process, to terminate discussions with any or all potential investors, to accept or reject any proposals and to negotiate with, or cease negotiations with, any party regarding a transaction involving the Company and SPAC. Any offer to sell securities will be made only pursuant to a definitive subscription agreement and will be made in reliance on an exemption from registration under the Securities Act of 1933, as amended, and the rules and regulations promulgated thereunder (collectively, the “Securities Act”), for offers and sales of securities that do not involve a public offering. Furthermore, all or a portion of the information contained in this Presentation may constitute material non-public information of the Company, SPAC and their respective affiliates, and other parties that may be referred to in the context of those discussions. By your receipt of this Presentation, you acknowledge that applicable securities laws restrict a person from purchasing or selling securities of a person with tradeable securities from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities. Except where otherwise indicated, this Presentation speaks as of the date hereof. The information contained in this Presentation replaces and supersedes, in its entirety, information of all prior versions of similar presentations. This Presentation does not purport to contain all information that may be required for or relevant to an evaluation of the Transaction.

Further, this Presentation should not be construed as legal, tax, investment or other advice, and should not be relied upon to form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. You will be responsible for conducting any investigations and analysis that is deemed appropriate and should consult your own legal, regulatory, tax, business, financial and accounting advisors to the extent you deem necessary, and must make your own investment decision and perform your own independent investigation and analysis with respect to the Transaction, any investment in SPAC and the transactions contemplated in this Presentation. SPAC and the Company reserve the right to amend or replace this Presentation at any time but none of SPAC and the Company, their respective subsidiaries, affiliates, legal advisors, financial advisors or agents shall have any obligation to update or supplement any content set forth in this Presentation or otherwise provide any additional information to you in connection with the Transaction should circumstances, management’s estimates or opinions change or any information provided in this Presentation become inaccurate. Confidential Information The information contained in this Presentation is confidential and being provided to you solely for the purpose of assisting you in familiarizing yourself with SPAC and the Company in connection with the Transaction. This Presentation shall remain the property of the Company and the Company reserves the right to require the return of this Presentation (together with any copies or extracts thereof) at any time. Neither this Presentation nor any of its contents may be disclosed or used for any purposes other than information and discussion purposes without the prior written consent of SPAC and the Company. You agree that you will not copy, reproduce or distribute this Presentation, in whole or in part, to other persons or entities at any time without the prior written consent of SPAC and the Company. Any unauthorised distribution or reproduction of any part of this Presentation may result in a violation of the Securities Act. Forward-Looking Statements Certain statements included in this Presentation are forward-looking statements. All statements other than statements of historical fact contained in this Presentation, including statements as to future results of operations and financial position, planned products and services, business strategy and plans, objectives of management for future operations of the Company, market size and growth opportunities, competitive position and technological and market trends, are forward-looking statements. Some of these forward-looking statements can be identified by the use of forward-looking words, including “anticipate,” “expect,” “suggests,” “plan,” “believe,” “intend,” “estimates,” “targets,” “projects,” “should,” “could,” “would,” “may,” “will,” “forecast” or other similar expressions. All forward-looking statements are based upon current estimates and forecasts and reflect the views, assumptions, expectations, and opinions of SPAC and the Company as of the date of this Presentation, and are therefore subject to a number of factors, risks and uncertainties, some of which are not currently known to SPAC or the Company. Some of these factors include, but are not limited to: the company’s success in the highly competitive automotive market, the Company’s reliance on Geely, the Company’s ability to maintain the “Lotus” brand, the Company’s limited number of orders, the Company’s limited number of models, the Company’s dependency on consumers’ demand and willingness for electronic vehicles and passenger vehicles, unforeseen changes of the Company’s industry and technology, the Company’s dependency of suppliers, cost increases

or disruptions of raw materials and other components , and the global shortage in the supply of semiconductor chips.The foregoing list of factors is not exhaustive. You should carefully consider the risks and uncertainties described in the “Risk Factors” section of this Presentation and the “Risk Factors” section of the proxy statement/prospectus on Form F-4 relating to the Transaction which is expected to be filed with the U.S. Securities and Exchange Commission (“SEC”), and other documents filed from time to time with the SEC. These filings identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. In light of these factors, risks and uncertainties, the forward-looking events and circumstances discussed in this Presentation may not occur, and any estimates, assumptions, expectations, forecasts, views or opinions set forth in this Presentation should be regarded as preliminary and for illustrative purposes only and accordingly, undue reliance should not be placed upon the forward-looking statements. SPAC and the Company assume no obligation and do not intend to update or revise these forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by law. Moreover, the Company operates in a very competitive and rapidly changing environment, and new risks may emerge from time to time. It is not possible to predict all risks, nor assess the impact of all factors on the Company’s business or the extent to which any factor, or combination of factors, may cause the Company’s actual results, performance or financial condition to be materially different from the expected future results, performance of financial condition. In addition, the analyses of SPAC and the Company contained herein are not, and do not purport to be, appraisals of the securities, assets or business of the Company, SPAC or any other entity. There may be additional risks that neither SPAC nor the Company presently knows or that SPAC and the Company currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. These forward-looking statements should not be relied upon as representing the Company’s or SPAC’s assessment as of any date subsequent to the date of this Presentation. More generally, SPAC and the Company caution you against relying on these forward-looking statements, and SPAC and the Company qualify all of our forward-looking statements by these cautionary statements. DISCLAIMER (1/2) |

|

3 Industry and Market Data This Presentation also contains information, estimates and other statistical data derived from third party sources including Oliver Wyman, LLC. Such information involves a number of assumptions and limitations, and due to the nature of the techniques and methodologies used in market research, Oliver Wyman, LLC cannot guarantee the accuracy of such information. You are cautioned not to give undue weight to such estimates. Neither SPAC nor the Company have commissioned any of the industry publications or other reports generated by third-party providers that are referred to in this Presentation. SPAC and the Company may have supplemented such information where necessary, taking into account publicly available information about other industry participants. Presentation of Financial Data The financial information and data contained in this Presentation has not been audited in accordance with the standards of the Public Company Oversight Board (“PCAOB”) or prepared in accordance with Regulation S-X promulgated under the Securities Act (“Regulation S-X”). Accordingly, such information and data may not be included in, may be adjusted in, or may be presented differently in, any proxy statement, prospectus or other report or document filed or to be filed or furnished by the Company or SPAC with the SEC. Neither SPAC nor the Company can assure you that, had the financial information and data included in this Presentation been compliant with Regulation S-X and audited in accordance with PCAOB standards, there would not be differences, which differences could be material. This Presentation includes certain financial information of the Company that has not been audited or reviewed by the Company's independent auditor. In addition, certain projections or forecasts for the Company included in this Presentation are based on such unaudited and unreviewed financial information. Upon completion of the Company auditor's review or audit of the financial information included in this Presentation, it is possible that changes to the financial information and/or projections or forecasts included in this Presentation may be necessary. Therefore, undue reliance should not be placed on such financial information, projections or forecasts. Use of Projections This Presentation contains financial forecasts for the Company with respect to certain of its financial results for the fiscal years 2023-2025 for illustrative purposes. Neither SPAC’s nor the Company’s independent auditors have audited, studied, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, they did not express any opinion or provide any other form of assurance with respect thereto for the purpose of this Presentation. These projections are forward-looking statements and should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. While such information and projections are necessarily speculative, SPAC and the Company believe that the preparation of prospective financial information involves increasingly higher levels of uncertainty the further out the projection extends from the date of preparation. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. The inclusion of prospective financial information in this Presentation should not be regarded as a representation by any person that the results contained in the prospective financial

information will be achieved. All subsequent written and oral forward-looking statements concerning the Company or SPAC, the Transaction or other matters and attributable to the Company or SPAC or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements above. Non-GAAP Financial Measures This Presentation also includes non-GAAP financial measures, such as EBITDA. Such non-GAAP measures should be considered only as supplemental to, and not as superior to, financial measures prepared in accordance with GAAP. SPAC and the Company believe these non-GAAP measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to the Company’s financial condition and results of operations. SPAC and the Company believe that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends in and in comparing the Company’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. Management does not consider these non-GAAP measures in isolation or as an alternative to financial measures determined in accordance with GAAP. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. Additionally, to the extent that forward-looking non-GAAP financial measures are provided, they are presented on a non-GAAP basis without reconciliations of such forward-looking non-GAAP measures due to the inherent difficulty in forecasting and quantifying certain amounts that are necessary for such reconciliation. Additional Information In connection with the Transaction, the SPAC will be required to file a preliminary and definitive proxy statement, which may include a registration statement, and other relevant documents with the SEC. You are urged to read the proxy statement/prospectus and any other relevant documents filed with the SEC when they become available because, among other things, they will contain updates to the financial, industry and other information herein as well as important information about SPAC, the Company and the Transaction. Shareholders of SPAC will be able to obtain a free copy of the proxy statement when filed, as well as other filings containing information about SPAC, the Company and the Transaction, without charge, at the SEC’s website located at www.sec.gov. Participants in the Solicitation SPAC and the Company, and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from SPAC’s shareholders in connection with the Transaction. A list of the names of such directors and executive officers and information regarding their interests in the Transaction will be contained in the proxy statement. You may obtain free copies of these documents as described in the preceding paragraph. The definitive proxy statement will be mailed to shareholders of SPAC as of a record date to be established for voting on the Transaction when it becomes available. Participants in Solicitation SPAC, the Company and their respective directors, executive officers, other members of management, and employees, under SEC rules, may be deemed to be participants in the solicitation of proxies from SPAC' shareholders in connection with the Transaction. You can find information about SPAC' directors and executive officers and their interest in SPAC can be found in SPAC' Annual Report on Form 10-K for the fiscal year ended 31 December 2021, which was originally filed with the SEC on March 28, 2022. A list of the names of the directors, executive officers, other members of management and employees of SPAC and the Company, as well as information regarding their interests in the Transaction, will be contained in the Registration Statement on Form F-4 to be

filed with the SEC by the Company. Additional information regarding the interests of such potential participants in the solicitation process may also be included in other relevant documents when they are filed with the SEC. You may obtain free copies of these documents from the sources indicated above. No Offer or Solicitation This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act, or an exemption therefrom. Trademarks This Presentation may contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this Presentation may be listed without the TM, SM © or ® symbols, but such references are not intended to indicate, in any way, that SPAC, the Company or the third-parties will not assert, to the fullest extent under applicable law, their rights or the right of the applicable owners or licensors to these trademarks, service marks, trade names and copyrights. Neither SPAC, the Company, nor any of their respective directors, officers, employees, affiliates, advisors, representatives or agents, makes any representation or warranty of any kind, express or implied, as to the value that may be realised in connection with the Transaction, the legal, regulatory, tax, financial, accounting or other effects of the Transaction or the timeliness, accuracy or completeness of the information contained in this Presentation, and none of them shall have any liability based on or arising from, in whole or in part, any information contained in, or omitted from, this Presentation or for any other written or oral communication transmitted to any person or entity in the course of its evaluation of the Transaction, and they expressly disclaim any responsibility or liability for direct, indirect, incidental, exemplary, compensatory, punitive, special, or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with the use of the information herein. DISCLAIMER (2/2) |

|

4 Risks Relating to Lotus Tech's Business and Industry 1. The automotive market is highly competitive, and we may not be successful in competing in this industry. 2. Our reliance on a variety of arrangements with Geely Holding, including agreements related to research and development, procurement, manufacturing, and engineering, could subject us to risks. 3. We may not succeed in continuing to maintain and strengthen our brand, and our brand and reputation could be harmed by negative publicity with respect to us, our directors, officers, employees, shareholders, peers, business partners, or our industry in general. 4. We have a limited operating history and our ability to develop, manufacture, and deliver automobiles of high quality and appeal to customers, on schedule, and on a large scale is unproven and still evolving. 5. We have not been profitable and had negative net cash flows from operations. If we do not effectively manage our cash and other liquid financial assets, execute our plan to increase profitability and obtain additional financing, we may not be able to continue as a going concern. 6. Forecasts and projections of our operating and financial results relies in large part upon assumptions and analyses developed by our management. If these assumptions or analyses prove to be incorrect, our actual operating results may be materially different from those forecasted or projected. 7. We have received a limited number of orders for Eletre, some of which may be cancelled by customers despite their deposit payment and online confirmation. 8. We currently depend on revenues generated from a limited number of vehicle models. 9. Any delays in the manufacturing and launch of the commercial production vehicles in our pipeline could have a material adverse effect on our business. 10. Our vehicles are subject to homologations and motor vehicle safety standards and the failure to acquire homologations or satisfy mandated safety standards in jurisdictions we operate would materially and adversely affect our business and results of operations. 11. Our future growth is dependent on the demand for, and upon consumers’ willingness to adopt luxury electric vehicles, which is associated with consumers’ demand for automobile and luxury vehicles, and adoption of new energy vehicles. 12. Our sales depend in part on our ability to establish and maintain confidence in our business prospects among consumers, analysts and others within our industry. 13. Our industry and its technology are rapidly evolving and may be subject to unforeseen changes. Developments in alternative technologies or improvements in electric vehicles technology may materially and adversely affect the demand for our electric vehicles. 14. We are subject to risks associated with autonomous driving technology and uncertain and evolving regulations pertaining autonomous driving in jurisdictions we operate. 15. We are dependent on suppliers, many of whom are our single source suppliers for the components they supply. 16. We could experience cost increases or disruptions in supply of raw materials or other components used in our vehicles. 17. The global shortage in the supply of semiconductor chips may disrupt our operations and adversely affect our business, results of operations, and financial condition. 18. We plan to expand our business and operations internationally to various jurisdictions in which we do not currently operate and where we have limited operating experience, all of which exposes us to business, regulatory, political, operational and financial risk. 19. We may be unable to adequately control the costs associated with our operations. 20. If we fail to manage our growth effectively, we may not be able to market and sell our vehicles successfully. 21. Our business plans require a significant amount of capital. In addition, our future capital needs may require us to obtain additional equity or debt financing that may dilute our shareholders or introduce covenants

that may restrict our operations or our ability to pay dividends. 22. If our suppliers fail to use ethical business practices and comply with applicable laws and regulations, our brand image could be harmed due to negative publicity. 23. We may not be able to expand our physical sales network cost-efficiently. Our distribution model is different from the currently predominant distribution model for automakers, and its long-term viability is unproven. 24. Our vehicles may not perform in line with customer expectations and may contain defects. Risks Relating to Doing Business in China 1. Failure to meet the PRC government’s complex regulatory requirements on and significant oversight over our business operation could result in a material adverse change in our operations and the value of our securities. 2. We may be adversely affected by the complexity, uncertainties and changes in regulations of mainland China on automotive as well as internet-related businesses and companies. 3. The approval of and filing with the CSRC or other PRC government authorities may be required in connection with this Business Combination or our listing under laws of mainland China, and, if so required, we cannot predict whether or when we will be able to obtain such approval or complete such filing, and even if we obtain such approval, it could be rescinded. Any failure to or delay in obtaining such approval or complying with such filing requirements in relation to offering, or a rescission of such approval, could subject us to sanctions imposed by the CSRC or other PRC government authorities. 4. The PCAOB had historically been unable to inspect our auditor in relation to their audit work. 5. Our securities may be prohibited from trading in the United States under the Holding Foreign Companies Accountable Act, or the HFCAA, if the PCAOB is unable to inspect or investigate completely auditors located in China. The delisting of our securities, or the threat of their being delisted, may materially and adversely affect the value of your investment. 6. Additional disclosure requirements to be adopted by and regulatory scrutiny from the SEC in response to risks related to companies with substantial operations in China, which could increase our compliance costs, subject us to additional disclosure requirements, and/or suspend or terminate our future securities offerings, making capital-raising more difficult. 7. China’s M&A Rules and certain other regulations establish complex procedures for certain acquisitions of PRC companies by foreign investors, which could make it more difficult for us to pursue growth through acquisitions in China. 8. Substantial uncertainties exist with respect to the interpretation and implementation of newly enacted 2019 PRC Foreign Investment Law and its Implementation Rules. 9. Regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from making loans to or make additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business. 10. We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business. RISK FACTORS (1/2) |

|

5 Risks Relating to Intellectual Property and Legal Proceedings 1. We may need to defend ourselves against intellectual property right infringement, misappropriation, or other claims, which may be time -consuming and would cause us to incur substantial costs. 2. We may not be able to prevent others from unauthorized use of our intellectual property, which could harm our business and competitive position. 3. We may not be able to adequately obtain or maintain our proprietary and intellectual property rights in our data or technology. 4. As our patents may expire and may not be extended, our patent applications may not be granted, and our patent rights may be contested, circumvented, invalidated, or limited in scope, our patent rights may not protect us effectively. In particular, we may not be able to prevent others from developing or exploiting competing technologies, which could materially and adversely affect our business, financial condition, and results of operations. 5. In addition to patented technologies, we rely on our unpatented proprietary technologies, trade secrets, processes, and know -how. Risks Relating to LCAA and the Business Combination 1. LCAA’s current directors’ and executive officers’ affiliates own LCAA Shares that will be worthless if the Business Combination is not approved. Such interests may have influenced their decision to approve the Business Combination. 2. The process of taking a company public by means of a business combination with a special purpose acquisition company is different from taking a company public through a traditional initial public offering and may create risks for LCAA’s unaffiliated investors. 3. The Committee on Foreign Investment in the United States (“CFIUS”) may delay, prevent, or impose conditions on the Business Combination. 4. The Founder Shareholders agreed to vote in favor of the Business Combination, regardless of how LCAA Public Shareholders vote. 5. LCAA is dependent upon its directors and officers and their loss could adversely affect LCAA’s ability to complete the Business Combination. The foregoing summarizes certain of the general risks related to Lotus Tech and LCAA, and such list is not exhaustive . The foregoing list has been prepared solely for purpose of assisting interested parties in making their own evaluation with respect to the Business Combination and not for any other purpose . You should carefully consider these risks and uncertainties together with the other available information and should carry out your own diligence and consult with your own financial and legal advisors . A more expansive description of the key risk factors will be filed with the SEC as part of the Form F - 4 registration statement referred to above and in subsequent filings with the SEC, and such risk factors will be more extensive than, and may differ significantly from, the above summary . RISK FACTORS (2/2) |

|

6 TODAY’S PRESENTERS Note: In this presentation, “Lotus Tech,” "Lotus Technology," or "we" refer to Lotus Technology Inc. and its subsidiaries, "Lotus UK" refers to Lotus Group International Limited and its subsidiaries. Lotus Tech and Lotus UK currently operate separately and independently from each other under the "Lotus" brand. "Lotus" or "Lotus Group" refer to Lotus Tech and Lotus UK, taken as a whole. “LTIC” refers to Lotus Technology Innovation Centre Howard Steyn President, LCAA & Partner, L Catterton Alexious Lee Chief Financial Officer, Lotus Group & Executive Chairman, ESG Committee 20+ years experience in China's banking & auto sector Former Managing Director, Head of China Capital Access at CITIC-CLSA, China Strategist at Jefferies Former Head of Strategic Business at FIAT China Inv. Co. Mike Johnstone Chief Commercial Officer, Lotus Group Former Vice President and Global Head of Marketing & Brand at Volvo Cars Former International Director of Marketing Operations at Harley-Davidson Motor Company Maximilian Szwaj Vice President, Lotus Technology & Managing Director, LTIC Former Vice President and CTO at Aston Martin Former Head of Body Engineering, Innovations at Ferrari Former Manager at BMW Chinta Bhagat Co-CEO, LCAA & Chairman, L Catterton Asia Co-head of L Catterton’s Asia platform since mid 2019. Led the buildout of a new team, refreshed strategy, integration of the Asia business into a global platform and spearheaded several sizeable platform investments across the region Former co-head of Private Markets at Khazanah Nasional, the sovereign wealth fund of the government of Malaysia Former Managing Partner at McKinsey & Company’s Singapore office Leads L Catterton’s global initiatives, driving cross-geography investments and portfolio company expansion Former Principal at Bain Capital 20+ years of experience with Geely Group Campaigned the acquisition of Lotus by Geely and the forge of Vision80 Lotus Brand Strategy Former CTO and VP of Zhejiang Geely Auto, GM of Geely Auto Sales Qingfeng Feng Chief Executive Officer, Lotus Group & Senior Vice President, Geely Holdings Group |

|

Source: Public sources 1. The list of L Catterton portfolio companies includes historical and current investments L CATTERTON – TRUSTED PARTNER TO VISIONARY ENTREPRENEURS AND LEADING CONSUMER BUSINESSES Selected L Catterton Portfolio Companies1 • A leading global consumer-focused investment firm with approximately US$33bn of equity capital under management, investments in over 250 consumer companies and more than 200 investment and operating professionals across 17 offices • Focused exclusively on building iconic and enduring consumer brands since founding in 1989 • Strategic relationship with LVMH, the world’s largest luxury conglomerate with 75+ distinguished brands • Leveraging deep consumer insights and extensive operating capabilities to help build iconic brands and create significant shareholder value 1989 Founded ~US$33bn Equity capital under management 250+ Investments 17 Offices globally 7 |

|

Source: Geely company filings, news releases, public information 1. BEV: Battery Electric Vehicles; SEA: Sustainable Experience Architecture; EPA: Electrical Performance Architecture 2. Initial delivery year; Polestar started delivery in July 2020; Lynk & Co started delivery in December 2017; Zeekr started delivery in October 2021 8 GEELY HAS A PROVEN TRACK RECORD IN TRANSFORMING AND ACCELERATING THE GROWTH OF AUTO BRANDS Geely’s auto brand development track record Examples of growing and accelerating auto brands 374 615 2010 2022 Sales volume (unit, k) 6 72 2021 2022 Sales volume (unit, k) 6 180 2017 2022 Sales volume (unit, k) 10 52 2020 2022 Sales volume (unit, k) 1.6x 30.0x 12.0x 5.2x 2 2 2004 Geely Auto - the first Chinese automaker listed on HKEX 2016 Unveiled high-end Lynk & Co brand 2017 Acquired 8.2% stake and 15.6% voting rights in Volvo AB and became the single largest shareholder Founded Polestar with Volvo 2019 Formed JV with Daimler to own, operate and develop Smart 2021 Acquired 34% stake in Renault Korea 2022 Lotus Tech launched Eletre, its first lifestyle luxury BEV1 SUV 2010 Acquired 100% of Volvo Car Corporation from Ford Motor Company 2017 Acquired 51% stake in Lotus 2018 Chairman Eric Li acquired 9.7% stake in Daimler AG and became the single largest shareholder 2020 Launched SEA1 , world’s first open-source BEV architecture that sets the foundation of Lotus Tech’s EPA1 platform development 2021 Established BEV-focused subsidiary Zeekr 2 |

|

9 ▪ Iconic brand and heritage ▪ Pioneer in advanced auto technology ▪ Global distribution network ▪ Fully-electric product portfolio1 ▪ Architecture development ▪ Manufacturing capabilities ▪ Procurement & supply chain ▪ Incubation and human capital support ▪ Consumer insights ▪ Brand building expertise ▪ Strategic relationships with LVMH and Financière Agache (formerly known as Groupe Arnault) ▪ Capital markets credibility Strong foundational support from Geely Asset light and scalable Built upon the experience, technology and scale of Geely Consumer insights and brand building expertise from L Catterton A STRATEGIC PARTNERSHIP WITH INSTRUMENTAL SUPPORT FROM GEELY AND L CATTERTON Source: Lotus management 1. New car roll outs are all BEV models beginning in 2022 with ICE model production ending in 2026 |

|

10 1 Early mover in the modern sustainable luxury BEV market Lotus Tech targets the most attractive price segment and key regions within the global luxury BEV market 2 Iconic brand with racing heritage Leading sports car brand signifying innovation, driving performance and engineering prowess 3 Proprietary next-generation technology built on world-class R&D capabilities Pioneering powertrain, design and software technologies that are best placed for the BEV transformation 4 Asset-light business model supported by Geely ecosystem Proven asset-light model evidenced by Geely’s successful track record of seeding multiple BEV brands with attractive financial profiles 5 Unrivalled focus on sustainability targeting fully-electric product portfolio Target to be carbon-neutral by 2038 6 Luxury retailing experience and digital-first, omni-channel sales model Premium stores in high-footfall locations combined with omni-channel sales model to provide personalised and exclusive service 7 Global, experienced and visionary leadership Pioneering, tech-forward and design-led executive team Darker picture EXECUTIVE SUMMARY 10 |

|

BUSINESS OVERVIEW |

|

P E R F O R M A N C E MODERN SUSTAINABLE LUXURY BEV D E S I G N E N G I N E E R I N G ICONIC BRAND & HERITAGE ‒ ESTABLISHED BRITISH BRAND ‒ RACING HERITAGE WITH SUPERIOR AERODYNAMICS ‒ PIONEER IN LIGHTWEIGHT TECHNOLOGY ‒ EARLY MOVER IN THE LUXURY LIFESTYLE BEV SEGMENT ‒ LEADER IN ADVANCED TECHNOLOGY ‒ FULLY-ELECTRIC PORTFOLIO1 1. New car roll outs are all BEV models beginning in 2022; expect to achieve 100% BEV product portfolio by 2027 TRANSFORMATION OF THE ICONIC LOTUS BRAND 12 |

|

LOTUS CARS UK-BASED SPORTS CAR HERITAGE ENGINEERING EXCELLENCE ACQUIRED BY GEELY (51%) IN 2017 LOTUS TECHNOLOGY NEW LIFESTYLE BEV-FOCUSED PLATFORM GLOBAL SALES AND DISTRIBUTION FOUNDED IN 2021 AS PART OF “VISION80” 13 100% BEV PORTFOLIO2 BORN BRITISH, RAISED GLOBALLY 3 + 3 3 EXISTING MODELS + 3 DEVELOPING MODELS2 ~240K CARS EXPECTED TO BE SOLD BY 20253 4 CORE REGIONS1 Source: Company information, Lotus management estimates Note: 1. Europe (including UK), China, U.S. and ROW (including Middle East) 2. New car roll outs are all BEV models beginning in 2022; expect to achieve 100% BEV product portfolio by 2027 3. Includes (i) historical car sales of Lotus UK since 1948 and (ii) sales of Lotus expected ~140k in 2023-2025, in each case, following the completion of the buildup of the global sales and distribution platform (the "Global Commercial Platform") pursuant to the Distribution Agreement (the "Master Distribution Agreement") that has been entered into in connection with the business combination, under which a subsidiary of Lotus Tech is appointed as the global exclusive distributor of Lotus UK for all Lotus branded cars in all geographic markets (except for the U.S.) AN INTEGRATED GLOBAL PLATFORM 13 |

|

14 Technology-related growth Autonomous driving, smart cabin, human machine interface, IOV connectivity Auto-related growth Build distribution, launch models, drive volume, aftermarket services Ecosystem-related growth Lifestyle products, customised premium services, in-car purchases VISION80: A LONG-TERM BUSINESS TRANSFORMATION STRATEGY Source: Company information, Lotus management estimates 1. ICE model production ending in 2026 2. Including models launched or expected to be launched by Lotus UK and Lotus Tech 2018 2023E 2027E BEV1 0% 75% 100% Models2 2 sports cars 1 sports car 1 all-electric sports car 1 SUV BEV 1 sedan BEV 3 all-electric sports cars 2 SUV BEVs 1 sedan BEV Dedicated to transforming the Lotus brand to an all-electric, intelligent and luxury mobility provider before the Company’s 80th anniversary 14 TRANSFORM EXPAND BROADEN |

|

Source: Company information, Lotus management estimates 1. Average Manufacturer’s Suggested Retail Price (MSRP) 2. Forecasted annual sales volume in years when production level and sales volume are relatively stable: Evija (~2023 onwards), Emira (~2024 onwards), Eletre (~2026 onwards), Type 133 (~2027 onwards), Type 134 (~2027 onwards), Type 135 (~2029 onwards) 3. Developed and launched by Lotus UK 4. Originally released as the last ICE car by Lotus UK, the Emira is expected to be converted to BEV from 2027 onwards 15 Evija3 (BEV Sports car) Emira4 (ICE Sports car) Eletre (BEV SUV) Type 133 (BEV Sedan) Type 135 (BEV Sports car) Type 134 (BEV SUV) PRODUCT PORTFOLIO LEADING THE MODERN SUSTAINABLE LUXURY BEV MARKET 2019 / 2023 2021 / 2022 2022 / March 2023 2023 / 2024 2024 / 2026 2025 / 2027 Launch / delivery year 2,200,000+ 85,000+ 100,000+ 100,000+ 70,000+ 95,000+ MSRP (US$)1 25 5k-6k 40k-50k 30k-40k 80k-90k 10k-15k Exp. annual sales volume2 All new models after 2022 are BEVs |

|

<20 min CHARGING SPEED (10-80% CHARGE) 905 hp1 675KW 2.95s 1 0-100 KM/H 0-62 MPH 600 km2 TARGET RANGE (WLTP3 COMBINED CYCLE) US$100K+ AVERAGE MSRP Reader Award, 2022 Electric Car of the Year We’re most curious to drive, The Electric Awards 2022 Finalist, Car Design Award 2022 1. Figure for Eletre R models 2. Figure for Eletre S models 3. WLTP: Worldwide Harmonised Light Vehicle Test Procedure THE WORLD’S FIRST ALL-ELECTRIC HYPER-SUV 16 SUV of the year 2023 |

|

17 800V EPA designed and created by Lotus Self-developed software system for cognition, decision-making, design and control algorithm Deployable LiDAR technology Five 360° perception coverage Easily adaptable design UNPARALLELED SELF-DEVELOPED TECHNOLOGICAL CAPABILITIES Advanced Driver Assistance System (ADAS) Electrical Performance Architecture (EPA) Integrated systems and vehicle dynamics |

|

CELEBRATE 75TH ANNIVERSARY WITH ELETRE’S FIRST DELIVERY Source: Company Information 18 – Completion of the first delivery of Eletre on 29 March 2023, the Lotus Day – Celebrate the 75th anniversary of the Lotus brand at the Shanghai International Circuit F1 track; the ‘Lotus Yellow’ lit up in 7 metropolitan cities as part of the celebration – A captivating evening where 600+ customers and VIP guests enjoyed the dynamic displays of Lotus BEV models and classic Lotus models that showcase the brand’s iconic heritage |

|

17,000+ Source: Company information 1. Designed maximum annual manufacturing capacity at dedicated Wuhan, China factory, which has been in use since 2022; production based on contract manufacturing with Geely 2. Represent total number of stores in Lotus Tech’s retail network as of 30 June 2023, which includes self-owned, joint venture, partnership and dealership stores 19 ROBUST DEMAND AND EXTENSIVE GLOBAL FOOTPRINT Global cumulative orders of Eletre and Emira as of 30 June 2023 150k Production capacity1 of Wuhan facility Start of production (SoP) in Q4 2022 Global retail stores as of 30 June 20232 190+ Orderbook Production Distribution |

|

INVESTMENT HIGHLIGHTS |

|

Source: Oliver Wyman, LLC Note: Car market here indicates all powertrain types, i.e. BEV and non-BEV 1. BEV penetration of Luxury car segment (>US$80k) 21 ...driven by rapid BEV transformation EARLY MOVER IN THE MODERN SUSTAINABLE LUXURY BEV MARKET 1 Lotus Tech is leading the electrification transformation of the fast-growing luxury car segment (>US$80k) % 45% BEV penetration1 6% Luxury non-BEV CAGR 4% Luxury BEV CAGR 35% Global car market (BEV + non-BEV) sales volume by price band (unit, k) >US$80k (luxury car segment) Luxury car segment Luxury car segment is expected to outgrow the overall car market… Global luxury car market (BEV + non-BEV) sales volume (unit, k) 2021A 2031E 4,266 2021A 78,667 1,601 80,268 4,266 100,309 4,215 104,525 2031E 2,286 1,929 93 1,508 1,601 4,215 Luxury BEV Luxury non-BEV ⚫ Lotus Tech is well positioned to address the luxury BEV market, which is expected to grow at a CAGR of 35% from 2021 to 2031 ⚫ Fast growth in global luxury BEV market is driven by long-lasting sustainability awareness, and favourable policies phasing out ICE sales in the coming decade, e.g., Norway by 2025, 10 countries (incl. UK, Netherlands, etc.) by 2030 and 4 more countries including China to follow by 2035 <US$80k Luxury car CAGR 10% Non-luxury car CAGR 3% 78,667 93 |

|

22 EARLY MOVER IN THE MODERN SUSTAINABLE LUXURY BEV MARKET 1 Lotus Tech’s target price segment is the largest volume contributor in the luxury BEV segment… Global luxury car market (BEV) sales volume by region (unit, k) CAGR (‘21A-’31E) Global car market (BEV) sales volume by price band (unit, k) 46% 33% 36% 29% Lotus Tech’s target price segment (US$80-149k) is the largest volume contributor in the luxury BEV segment… …and is strategically positioned in all key regions that drive fast growths ROW China Europe(1) U.S. ⚫ Customers within the luxury segment who would like to switch from ICE to BEV are faced with the lack of product offerings ⚫ Lotus Tech’s first mover advantage perfectly addresses such market opportunity ⚫ Lotus Tech targets the largest price segment (>85%) within global luxury BEV market in the next decade 2021A 2031E 1,929 14 11 33 35 93 35,867 579 733 193 424 Source: Oliver Wyman, LLC Note: 1. UK included 34% 46% 23% >US$150k <US$80k 4,266 4,700 2021A 35,867 2031E 4,607 85 7 280 1,649 36,951 38,880 Key target of Lotus Tech Luxury US$80-149k CAGR (‘21A-’31E) BEV CAGR 24% Luxury BEV CAGR 35% |

|

23 EARLY MOVER IN THE MODERN SUSTAINABLE LUXURY BEV MARKET 1 …however, the global luxury BEV market is currently underserved and Lotus is well-positioned Comparison of global luxury vehicle models Source: Oliver Wyman, LLC Note: The charts cover a representative list of vehicle models and are not exhaustive BEV models: c.10 ICE models: 100+ VS Model X, S EQE, EQS Eletre iX e-tron Taycan … X6, X7, 7-Series, 8-Series Q8, A8 Cayenne (Coupe), Panamera, 911 DBX, Vantage Roma, 488, F8 GLE (Coupe), GLS, S-Class Levante, Quattroporte Range Rover (Sport) Urus, Huracan … |

|

24 FULLY-ELECTRIC PRODUCT PORTFOLIO1 Transformation to fully-electric portfolio Brand heritage and luxury positioning 1 Heading the electrification wave among all global luxury automakers Source: Oliver Wyman, LLC 1. New car roll outs are all BEV models beginning in 2022 with ICE model production ending in 2026 |

|

Panamera, 2027 DBX, 2025 Source: Company information, Oliver Wyman, LLC, public information 1. Peer group based on the luxury car brands including Ferrari, Porsche, Aston Martin, Bentley, Lamborghini and Land Rover 2. Excludes Porsche Taycan model 25 LOTUS’S LAUNCH OF ITS BEV MODELS IS AHEAD OF THE COMPETITION 1 Type 134 (D-segment SUV) Launch | 2024 D-segment SUV peer group1 model, launch year Type 133 (E-segment Sedan) Launch | 2023 Eletre (E-segment SUV) Launch | 2022 Gen 2 Launch | 2028 E-segment sedan peer group1, 2 model, launch year 2027 E-segment SUV peer group1 model, launch year 2029 2024 2025 Gen 2 Launch | 2029 F245, 2026 Audi Artemis, 2025 K1, 2027 F244, 2026 Bentayga, 2029 Urus, 2029 Cayenne, 2026 Macan, 2024 Defender, 2025 2025 |

|

26 5 star expected 5 star expected 5 star expected 5 star 5 star expected 5 star LEADING PRODUCT PERFORMANCE AGAINST CORE COMPETITOR MODELS Scoring: Low High BEV Companies Competitive performance Established MNCs MSRP, RMB Vehicle length, mm ES7 100kWH 548,000 4,912 Audi SQ8 etron ~850,0002 4,915 Tesla Model X Plaid 1,039,900 5,057 Lotus Eletre S 828,000 5,103 Porsche Taycan GTS 1,392,000 4,963 Polestar 3 LR Performance ~700,0002 4,900 HiPhi X Flagship 800,000 5,200 BMW iX M60 996,900 4,953 MB EQE SUV AMG ~850,0002 4,879 Lotus Eletre R 1,028,000 5,103 Acceleration, 0-100km/h, s Driving performance 4.5 2.95 4.3 3.8 4.5 3.7 2.6 3.9 4.0 4.7 Electrification Driving e-range, km in WLTP Charging speed, max. kw in DC charging1 180+switch 510 170 450 250 540 350 600 510 268 610 195 120 560 173 540 350 490 Smartification Smart Cabin (Hardware, functions and experience) AD/ADAS (Hardware readiness) Over-The-Air capability n.a. n.a. n.a. Traditional metrics Quality, problem per 100 vehicles in 2022 Safety, C-NCAP star Exterior design3 Interior design3 and comfort 128 (ES6) 5 star 4.0 4.0 n.a. n.a. n.a. 155 (Model Y) 4.2 3.9 n.a. 4.6 4.4 202 5 star 4.7 4.4 5 star expected n.a. n.a. 163 5 star 4.4 4.2 133 (iX3) 4.0 4.4 170 (EQC) 4.0 4.4 n.a. 4.6 4.4 1 n.a. n.a. Source: Public information 1. DC charging capability is evaluated based on vehicle capability only and actual charging capability may be impacted by charging pillar capability. Final charging speed depends on vehicle and charging pillar combined 2. Future car prices not announced yet; EQE, SQ8 etron and Polestar 3 with reference from prices in Germany; Tesla Model X price reference from Autohome 3. KOL scoring from Dongchedi as a reference (scores as of 7 January 2023), scoring/ranking intends to emphasize and differentiate top 3 players n.a. |

|

Source: Company information 1. From 2008-2012, Tesla Roadster rolled off from Lotus production line 27 ICONIC BRAND WITH RACING HERITAGE 6 FIA Formula 1 Drivers’ World Championships 81 FIA Formula 1 Grand Prix Wins 9 Le Mans Wins (In Class) 1 Indianapolis 500 Grand Prix Win 1 FIA World Rally Championship 2 Leading sports brand signifying innovation, driving performance and engineering prowess 1957 Lotus Eleven First Le Mans Win (750cc Index Class) 1963 Type 25 First Formula 1 Constructors' Championship First Formula 1 Drivers’ Championship 1960 Type 18 First Grand Prix Win-Monte Carlo First World Rally Constructors' Championship 1963 Lotus Cortina First British Saloon Car Championship 1965 Type 38 First INDY 500 Victory 1978 Lotus Sunbeam 2008 Tesla Roadster1 2019 Lotus 2020 Lotus Evija Rolled off from Lotus Production Line “Luxury brand of the year” at prestigious Luxury Briefing Awards 2020 MUSE Global Design Awards 7 FIA Formula 1 Constructors’ World Champions |

|

PROPRIETARY NEXT-GENERATION TECHNOLOGY BUILT ON WORLD-CLASS R&D CAPABILITIES 3 Integrated systems and vehicle dynamics powered by Lotus 800V EPA ‒ 800V technology with intelligent heat management operating system ‒ 112kWh battery pack capacity Battery System ‒ Up to 905 hp with 985 Nm torque ‒ Dual speed transmission EDS Motor & E-drivetrain ‒ Range of up to 600 km ‒ 10-80% charge in 20 min Super Charging ‒ 5 link suspension, RWS1 , ARC1 ‒ Digital integrated chassis control system Chassis & Dynamics ‒ High speed 1G bps ethernet, 5G, V2X connectivity ‒ LOTUS Hyper OS Hyper Intelligent EE Architecture Connectivity 28 Source: Company information 1. RWS: Rear Wheel Steering; ARC: Active Roll Control |

|

29 PROPRIETARY NEXT-GENERATION TECHNOLOGY BUILT ON WORLD-CLASS R&D CAPABILITIES 3 ADAS upgradeable through embedded L4 hardware capabilities and Over-The-Air software updates 360° (5x) perception coverage with LiDARs, HD cameras, radars and USS (ultrasonic sensor system) redefining travel safety Perception coverage Hardware embedded State of the art in terms of hardware readiness 4 LiDARs, 7 HD Cameras, 6 long/short range millimeter radars, 12 ultrasonic radars 500 - 1000 TOPS powered by dual NVIDIA Orin X chips Computing power Racetrack-level testing Built and tested under race track conditions and high speed for extreme processing and decision ADAS software and feature upgradable through OTA subscription, given fully embedded L4 hardware capability E2E Platform capability Source: Company information |

|

30 LOTUS Hyper OS – Graphic processing powered by dual Qualcomm 8155 chips – Superior graphic rendering – Intuitive control interface – Data-driven user experience – Global OTA updates on software and APPs – LOTUS TECH – KEF – DOLBY ATMOS provides the ultimate immersive sound system PROPRIETARY NEXT-GENERATION TECHNOLOGY BUILT ON WORLD-CLASS R&D CAPABILITIES 3 World-class, intuitive and seamless connected experience through Lotus’s intelligent cabin infotainment system Source: Company information |

|

PROPRIETARY NEXT-GENERATION TECHNOLOGY BUILT ON WORLD-CLASS R&D CAPABILITIES 3 World-class R&D capabilities supported by dedicated centres in the UK, Germany and China Lotus Technology (Global headquarters) Wuhan, China Cloud computing, online data & robotic technology Lotus Technology Software Centre Shanghai, China Global system integration & network security Lotus Technology Creative Centre Coventry, UK Design, future vehicle concepts Lotus Technology Research Institute Ningbo, China Electric architecture, charging & power system Lotus Technology Innovation Centre Frankfurt, Germany Innovative vehicle technologies and architecture, regional application Source: Company information 31 |

|

32 4 Synergistic businesses with independent governance structures Strong bond Mutually beneficial partnership Independently governed ‒ Procurement and supply chain ‒ Manufacturing support ‒ Incubation and human capital support ‒ Ancillary revenue to Geely’s group of companies ‒ Iconic, prestigious brand ‒ Pioneer in advanced auto technology ‒ Well-balanced global distribution presence ‒ The only Geely-affiliated brand with sports car DNA ASSET-LIGHT BUSINESS MODEL SUPPORTED BY GEELY ECOSYSTEM Source: Company information |

|

33 ASSET-LIGHT BUSINESS MODEL SUPPORTED BY GEELY ECOSYSTEM 4 Backed by Geely’s industry-leading production capability – BEV production facility1 in Wuhan, China opened in 2022 – Contract manufacturing by Geely – Designed maximum annual capacity of 150,000 units – Highly automated production with superior flexibility – ~3 km track with 16 turns enables up to 230 kph straight-line driving Source: Company information 1. Owned and operated by Geely Group |

|

34 UNRIVALLED FOCUS ON SUSTAINABILITY TARGETING FULLY-ELECTRIC PRODUCT PORTFOLIO Material science & design 5 Targeting carbon neutrality by 2038 (scope 1, 2 & 31 ) – Redefine luxury by using circular materials to minimize environmental impact, with vehicle recyclability of ~90% – First traditional luxury auto brand expected to achieve 100% BEV production by 2027 – ICE production ending in 2026 Green factory2 – Photovoltaic power generation system with expected capacity >16mn kWh in 2023 – Target 100% renewable energy usage by 2030 Contribution to SDGs Product plans Source: Company information 1. Scope 1 and 2 are emissions that are owned or controlled by a company; scope 3 emissions are a consequence of the activities of the company but occur from sources not owned or controlled by it 2. Owned and operated by Geely Group |

|

Source: Company information, ST Green Finance, as of Q3 2022 1. CSR: Corporate Social Responsibility 2. ST Green Finance ESG rating awarded to Wuhan Lotus Cars Technology Co., Ltd. in Jan 2023. Comprehensive governance level and overall ESG risk are evaluated based on the ESG rating methodology of non-listed companies 3. Number of non-listed companies rated is not public 35 Lotus launched its new CSR1 programme ‘Driving Change’ in 2021 aligned to its Vision80 strategy Social Governance ADHERENCE TO INTERNATIONAL ESG STANDARDS 5 Contribution to SDGs – US LOT - the global Lotus colleagues - at the heart of global sustainable growth – Safety and inclusion of customers and communities – Advancement of equal education and automobility technology through college sponsorship and R&D project partnership – Adherence to the highest standards of corporate governance – Commitment to being an ethical and transparent company – Dedicated Directors and ESG Management Committee A-ESG Rating2 5,514 listed companies rated3 7% awarded A- rating or above |

|

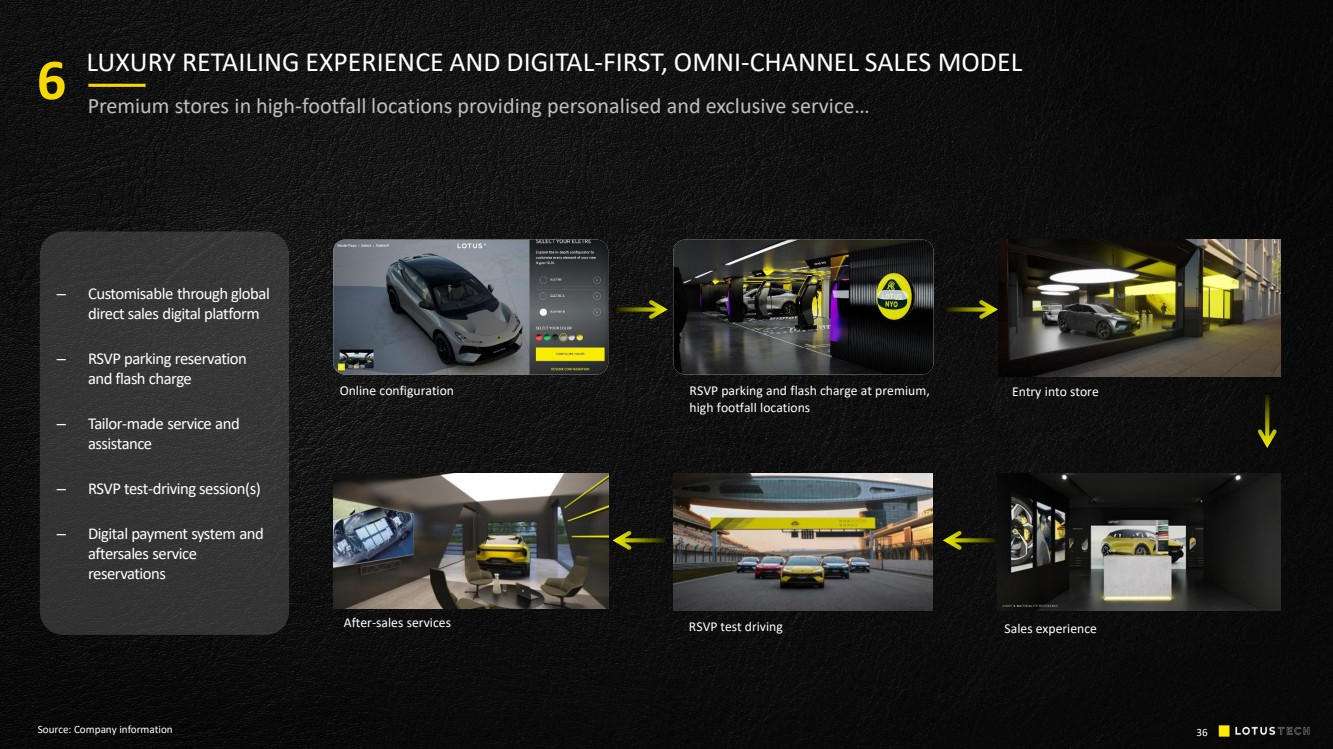

Source: Company information 36 LUXURY RETAILING EXPERIENCE AND DIGITAL-FIRST, OMNI-CHANNEL SALES MODEL 6 Premium stores in high-footfall locations providing personalised and exclusive service… – Customisable through global direct sales digital platform – RSVP parking reservation and flash charge – Tailor-made service and assistance – RSVP test-driving session(s) – Digital payment system and aftersales service reservations RSVP parking and flash charge at premium, high footfall locations Sales experience After-sales services Online configuration Entry into store RSVP test driving |

|

37 CUSTOMISATION CO-BRANDING AFTERMARKET CO-DEVELOPMENT CO-MARKETING RSVP SOFTWARE PURCHASE & TRADE-IN MOTORSPORTS PRIME FAST CHARGE RENTALS EVENTS LUXURY RETAILING EXPERIENCE AND DIGITAL-FIRST, OMNI-CHANNEL SALES MODEL Car-related business Lifestyle-related business 6 Lotus’ retail strategy will be supported by an omni-channel model Digital-centric, immensely flexible and scalable in response to individual market and customer requirements …enabled by digital-first, omni-channel sales model… |

|

Source: Lotus management estimates Note: Number of stores in Lotus Tech’s retail network 1. Dealership model only 2. Direct-to-customer (DTC) model only, which includes self-owned, joint venture stores and partnership stores 3. North America includes the U.S. and Canada; Europe includes the UK and others; ROW includes rest of Asia, Australia, the Middle East, South Africa and parts of South America, etc. 38 LUXURY RETAILING EXPERIENCE AND DIGITAL-FIRST, OMNI-CHANNEL SALES MODEL 6 …to cover prime locations globally with existing and newly-built hybrid model China2 • 52 existing stores • 100 stores by 2025 ROW1, 3 • 30 existing stores • 45 stores by 2025 North America1, 3 • 44 existing stores • 80 stores by 2025 Europe2, 3 • 67 existing stores • 105 stores by 2025 |

|

Self-owned 39 • Selected flagship stores in tier-1 cities • Located in strategically important, high-population cities across the world. i.e., London, Paris, Shanghai • Primary customer and brand experience centres LUXURY RETAILING EXPERIENCE AND DIGITAL-FIRST, OMNI-CHANNEL SALES MODEL 6 A balanced adoption of various sales models Partnership Distributor 1 • Strong ties with partners who have experience with the Lotus brand • Ability to scale up fast • Asset light model – capex, fixed and operating cost borne by the partner • Leveraging existing relationship with distributors – transferring Lotus UK’s existing distributor network to Lotus Tech2 • Distributors bear the inventory cost • Asset light model Source: Company information 1. Partnership model is known as agent model in Europe 2. On 31 January 2023 and concurrently with the execution of the Merger Agreement, Lotus Technology Innovative Limited, a wholly-owned subsidiary of Lotus Tech (“LTIL”), entered into the Master Distribution Agreement with Lotus Cars Limited, the entity carrying out the sportscar manufacturing operations of Lotus UK, pursuant to which LTIL is appointed as the exclusive global distributor of Lotus UK for all Lotus branded cars in all geographic markets (excluding the U.S., where LTIL will act as the head distributor with the existing regional distributor continuing its functions). The construction of the Company’s global sales and distribution platform is anticipated to complete in 3Q 2023 |

|

Source: Company information 40 GLOBAL, EXPERIENCED AND VISIONARY LEADERSHIP 7 Pioneering, tech-forward and design-led executive team Mike Johnstone Lotus Group Chief Commercial Officer Ben Payne Lotus Tech Chief Creative Officer Previous Experience: – Vice President and Global Head of Marketing & Brand at Volvo Cars – International Director of Marketing Operations at Harley-Davidson Motor Company Previous Experience: – Managing Director and Head of Studio at Lotus Tech Creative Centre (LTCC) – Lead Exterior Designer at Aston Martin – Lead Exterior Designer at Bugatti Alexious Lee Lotus Group CFO & ESG Committee Executive Chairman Jingbo Mao Lotus Tech China President Previous Experience: – Managing Director, Head of China Capital Access at CITIC-CLSA – China Strategist at Jefferies – Head of Strategic Business at FIAT China Inv. Co. Previous Experience: – President of Asia Pacific and China at Lincoln – Executive Vice President at Beijing Mercedes-Benz Sales Service Company Previous Experience: – CTO and VP at Zhejiang Geely Auto – GM at Geely Auto Sales Huifang Tang Lotus Tech Managing Director of Research Institute Qingfeng Feng Lotus Group CEO & Senior Vice President of Geely Holding Group Previous Experience: – Deputy General Manager of Geely Auto Research Institute – Vehicle Line Director at Geely Auto Research Institute Maximilian Szwaj Lotus Tech Vice President & Managing Director of LTIC Daniel Li Lotus Group Chairman & Geely Holding Group CEO Previous Experience: – GM at Cummins Generator Technologies China – Board Director, Senior Vice President & CFO at BMW Brilliance Previous Experience: – Vice President & CTO at Aston Martin – Head of Body Engineering and Innovations at Ferrari – Manager at BMW |

|

FINANCIAL OVERVIEW |

|

Source: Company information, Lotus management estimates 1. Number of stores in Lotus Tech’s retail network expected by 2025E 2. Existing models include Evija, Emira and Eletre, models in pipeline include Type 133, 134 and 135 3. Gross margin is expected to be higher after 2025, in years when production level and sales volume are relatively stable; specifically, Evija (~2023 onwards), Emira (~2024 onwards), Eletre (~2026 onwards), Type 133 (~2027 onwards), Type 134 (~2027 onwards) and Type 135 (~2029 onwards) 42 THE COMBINATION OF A MASSIVE MARKET, ADVANCED TECHNOLOGY AND A WORLD CLASS TEAM Revenue growth 2023E-2025E Attractive business outlook 2025E gross margin3 ~150% CAGR 3+3 models2 2025E targeted revenue ~US$8.2 – $8.6bn ~21% – 23% Continuous and well-balanced global expansion by 2025E 300+ stores1 Strong pipeline by 2027E |

|

8 33 42 16 25 4 6 6 12 54 73 2023E 2024E 2025E Eletre Type 133 Emira Evija Four models expected to power 147% CAGR volume growth... ...with China market contributing ~35% and other global markets contributing to the rest STRONG TOP-LINE GROWTH DRIVEN BY MODEL PIPELINE AND INTERNATIONAL EXPANSION 43 Unit, k Unit, k 5 19 23 4 19 23 1 11 19 2 5 8 12 54 73 2023E 2024E 2025E China Europe US ROW Source: Company information, Lotus management estimates 1. ’24E–’25E YoY growth 2. ROW includes rest of Asia, Australia, the Middle East, South Africa and parts of South America, etc. 2 CAGR (‘23-’25E) 39% 23% 59%1 130% CAGR (‘23-’25E) 88% 502% 130% 116% |

|

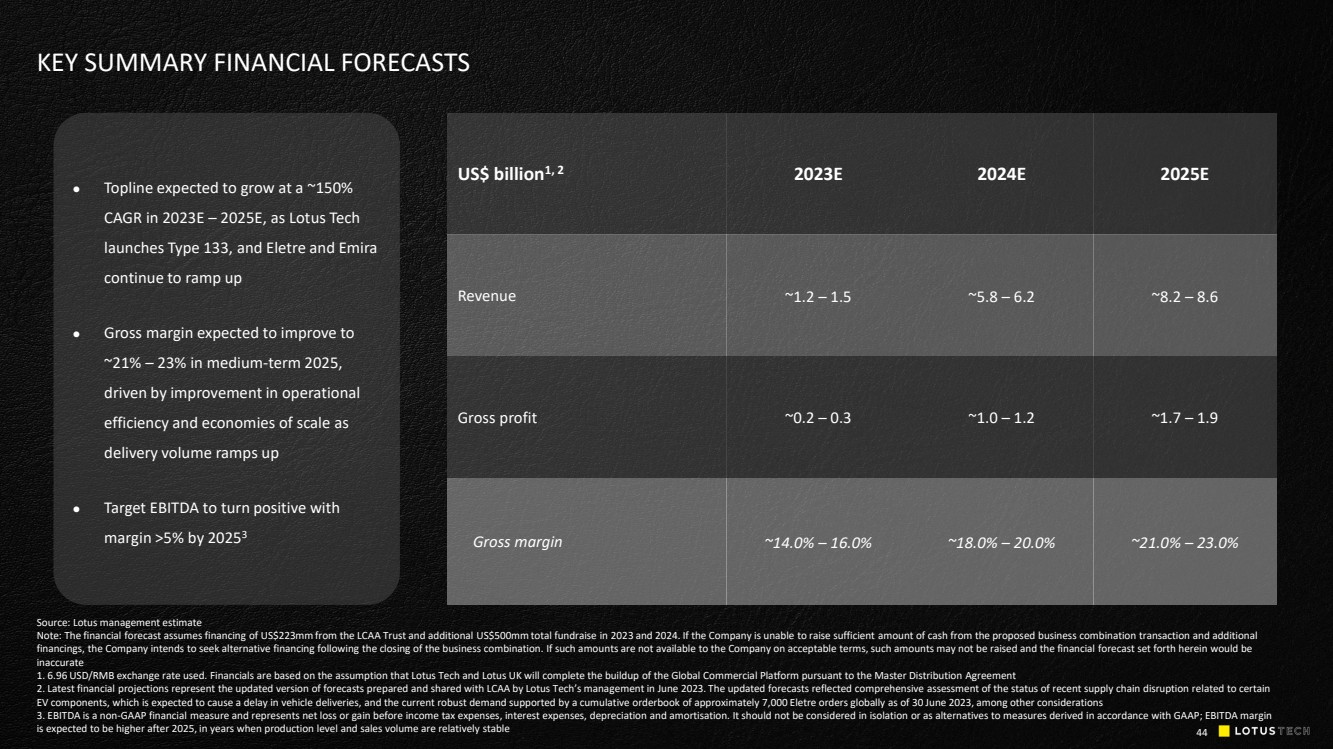

44 ⚫ Topline expected to grow at a ~150% CAGR in 2023E – 2025E, as Lotus Tech launches Type 133, and Eletre and Emira continue to ramp up ⚫ Gross margin expected to improve to ~21% – 23% in medium-term 2025, driven by improvement in operational efficiency and economies of scale as delivery volume ramps up ⚫ Target EBITDA to turn positive with margin >5% by 20253 KEY SUMMARY FINANCIAL FORECASTS US$ billion1, 2 2023E 2024E 2025E Revenue ~1.2 – 1.5 ~5.8 – 6.2 ~8.2 – 8.6 Gross profit ~0.2 – 0.3 ~1.0 – 1.2 ~1.7 – 1.9 Gross margin ~14.0% – 16.0% ~18.0% – 20.0% ~21.0% – 23.0% Source: Lotus management estimate Note: The financial forecast assumes financing of US$223mm from the LCAA Trust and additional US$500mm total fundraise in 2023 and 2024. If the Company is unable to raise sufficient amount of cash from the proposed business combination transaction and additional financings, the Company intends to seek alternative financing following the closing of the business combination. If such amounts are not available to the Company on acceptable terms, such amounts may not be raised and the financial forecast set forth herein would be inaccurate 1. 6.96 USD/RMB exchange rate used. Financials are based on the assumption that Lotus Tech and Lotus UK will complete the buildup of the Global Commercial Platform pursuant to the Master Distribution Agreement 2. Latest financial projections represent the updated version of forecasts prepared and shared with LCAA by Lotus Tech’s management in June 2023. The updated forecasts reflected comprehensive assessment of the status of recent supply chain disruption related to certain EV components, which is expected to cause a delay in vehicle deliveries, and the current robust demand supported by a cumulative orderbook of approximately 7,000 Eletre orders globally as of 30 June 2023, among other considerations 3. EBITDA is a non-GAAP financial measure and represents net loss or gain before income tax expenses, interest expenses, depreciation and amortisation. It should not be considered in isolation or as alternatives to measures derived in accordance with GAAP; EBITDA margin is expected to be higher after 2025, in years when production level and sales volume are relatively stable |

|

TRANSACTION OVERVIEW AND VALUATION |

|

46 DE-SPAC OVERVIEW Transaction Structure Lotus Tech has entered into a definitive business combination agreement ("BCA") with L Catterton Asia Acquisition Corp (NASDAQ: LCAA). Upon completion of the proposed business combination transaction, Lotus Tech will become a publicly-listed company. In connection with the parties’ entry into the BCA, Lotus Tech and Lotus UK (or their applicable subsidiaries) have also entered into the following agreements: • Master Distribution Agreement pursuant to which a subsidiary of Lotus Tech has been appointed the global distributor for Lotus UK • Put option agreements with existing shareholders of Lotus UK pursuant to which each of such shareholders will have the right to require Lotus Tech to acquire such shareholder's stake in Lotus UK at pre-agreed price and upon satisfaction of certain pre-agreed conditions at a future date The combined company will be responsible for sales and marketing for both Lotus BEV and ICE and existing shareholders of Lotus UK will have the right to require the combined company to purchase their stake in Lotus UK in the future Valuation Pro forma fully-diluted enterprise value of US$5.6bn, implying ~0.9x 2024E revenue and ~0.7x 2025E revenue Capital Structure Current Lotus Tech shareholders will roll 100% of their equity interest into the pro forma company, and retain approximately 87.3% ownership1 post transaction Note: The calculations on this slide assume an implicit value of US$10.00 per LCAA Class A ordinary share, which is based on convention and is not indicative of the real value of each LCAA Class A ordinary share or the value which the Lotus Tech attributes to each LCAA Class A ordinary share 1. Refer to the next page for ownership details |

|

Uses Estimated fees and expenses3 53 Existing Lotus shareholder equity rollover 5,500 Net cash to balance sheet at closing 292 Total 5,845 47 Estimated sources and uses US$ million Pro forma valuation US$ million Sources Existing Lotus shareholder equity 5,500 LCAA trust2 223 Pre-closing investors 122 Total 5,845 Base share price at merger US$10.00 PF shares outstanding (mm) 630 Pro forma equity value4 6,301 Plus: debt5 300 Less: existing cash balance6 (737) Less: net cash to balance sheet (292) Pro forma enterprise value 5,573 Illustrative pro forma ownership2,4,7 INDICATIVE TRANSACTION TERMS AND STRUCTURE ⚫ Pro forma equity value of US$6,301mm and pro forma enterprise value of US$5,573mm, which implies EV multiples of ~0.9x 2024E revenue and ~0.7x 2025E revenue ⚫ As of April 28, 2023, Company has entered into agreements with strategic partners and business partners for a total investment amount of approximately $122 million1 . Company will continue to seek to raise additional financing prior to closing of the business combination ⚫ To better align long-term incentives, LCAA Sponsor has agreed to subject 30% of the Sponsor Shares to earn-out and forfeiture arrangements tied to Sponsor affiliates' participation in the PIPE financing and strategic partnerships with Lotus Tech ⚫ Lotus Tech shareholders will roll over 100% of their equity interest into the pro forma company and retain approximately 87.3% ownership post-transaction ⚫ Proceeds to be used for further product innovation, next-generation automobility technology development, global distribution network expansion and general corporate purposes Note: The calculations on this slide assume an implicit value of US$10.00 per LCAA Class A ordinary share, which is based on convention and is not indicative of the real value of each LCAA Class A ordinary share or the value which the Lotus Tech attributes to each LCAA Class A ordinary share; they also exclude impact of 9.6 million public warrants and 5.5 million private placement warrants struck at $11.50. Existing Lotus shareholder equity includes equity in relation to employee stock options. 6.96 USD/RMB used in line with audited financials as of 31 December 2022 for Lotus Tech 1. Subject to customary terms and conditions (including regulatory approvals) included in the definitive agreements. The total investment amount of $122 million exceeded the previous pre-closing financing target amount of $100m 2. Cash-in-trust as of 31 March 2023. In connection with LCAA shareholders' approval to extend the deadline (the "Business Combination Deadline") by which LCAA must consummate a business combination on 10 March 2023, holders of approximately 23.97% of the LCAA public shares exercised their redemption rights for a pro rata portion of the funds in the trust account. Note that the cash-in-trust does not take into account additional contribution made by Sponsor in connection with extensions of the Business Combination Deadline and assumes no further redemptions by LCAA public shareholders 3. Estimated transaction fees and expenses of c.US$53mm 4. Pro forma equity value includes US$71.6mm founder shares, RMB 2.6bn / US$373mm from Jingkai Fund (through restructuring of its existing investment in Lotus Tech) 5. Pro forma total debt of US$300mm based on audited number as of 31 December 2022 for Lotus Tech, excluding the RMB 2.6bn Jingkai convertible note that will be restructured to invest in Lotus Tech 6. Existing cash balance of US$737mm based on audited number as of 31 December 2022 for Lotus Tech 7. Based on 7,162,718 Class B ordinary shares as of 31 March 2023. 30% of the SPAC shares held by Sponsor ("Sponsor Shares") are subject to earn-out and forfeiture arrangements tied to Sponsor affiliates' participation in the PIPE financing and strategic partnerships with Lotus Tech and 5% of Sponsor Shares may be transferred to certain LCAA public shareholders to induce such public shareholders not to

exercise their redemption rights of Class B ordinary shares, 87.3% 3.5% 1.1% 5.9% 2.1% Existing Lotus shareholders Public shareholders LCAA sponsor and independent directors Jingkai fund Pre-closing investors and others |

|

~0.9x 7.2x 5.0x 1.7x 1.3x 8.4x 2.5x 1.9x ~0.7x 5.6x 2.5x 0.9x 1.0x 7.7x 2.4x 1.7x 4.3x 3.9x Source: Company information, Lotus management estimates, FactSet as of 21 July 2023 1. Based on pro forma enterprise value of US$5.6bn 48 ATTRACTIVE ANTICIPATED ENTRY VALUATION WITH SIGNIFICANT DISCOUNT TO PEERS EV/Sales 2024E/2025E 2025E Average Average 2024E 1 BEVs Luxury OEMs 3.8x 2.5x |

|

Source: Company information, Lotus management estimates, FactSet as of 21 July 2023 Gross margin 2024E/2025E EBITDA margin 2025E SIGNIFICANT TOPLINE GROWTH EXPECTED GIVEN TOTAL MARKET OPPORTUNITY AND ATTRACTIVE MARGIN PROFILE 2025E 2024E Revenue CAGR 2023E–2025E 49 BEVs Luxury OEMs ~150.0% 28.4% 125.7% 79.8% 39.3% 8.5% 6.5% 12.4% ~18–20% 21.5% (15.4%) 8.3% 15.0% 51.2% 28.3% 36.2% ~21–23% 23.2% 8.1% 14.7% 17.2% 51.9% 28.1% 38.7% >5.0% 21.0% (10.2%) 0.8% 1.6% 39.2% 25.7% 24.5% |

|

APPENDIX |

|

Source: Company information 1. Under contract manufacturing and operated by Geely Group 51 1948–1960 Lotus was founded by Colin Chapman and moved to a factory in Cheshunt, UK. Stirling Moss won first Formula 1 Grand Prix in a Lotus car in Monaco 2000s–2010s Lotus was established as a niche brand with the launch of the Exige, Evora and Elise special editions. Lotus produced the Tesla Roadster in 2008–2012 1983–1996 Lotus changed ownership multiple times with Toyota, General Motors, Bugatti and eventually Malaysia-based Proton acquiring the company 1970s-1980s The iconic Lotus Esprit starred in two James Bond films, and Hollywood blockbusters Pretty Woman and Basic Instinct 2018–present On Lotus’s 70th anniversary in 2018, Lotus launched Vision80, a business transformation strategy 1960s–1970s In Formula 1, Lotus won seven Constructors’ Championships and six Drivers’ Championships. A new factory was built in Hethel, UK 1985–1988 Ayrton Senna joined Lotus for his first F1 Grand Prix win. World champion Nelson Piquet followed and the Lotus Type 100T wore #1 for the season 1990s The Elise, eventually Lotus’s most popular car, was launched and saw its 1000th sale in 1997. Total Lotus production reached 50,000 in 1995 2017 Geely Group Holding bought a 51% stake in Lotus 2022 Lotus launched its first lifestyle vehicle, the Lotus Eletre luxury BEV SUV 2022 BEV manufacturing facility1 opened in Wuhan, China in July 2022 with manufacturing capacity of 150,000 units annually ICONIC BRITISH RACING LEGEND WITH OVER SEVEN DECADES OF TRADITION |

|

SPORTS CAR STYLE SUV COMFORT AERODYNAMIC DESIGN The all-new and all-electric Lotus Eletre takes the core principles and Lotus DNA from 75 years of sports car design and engineering The Evija-derived aerodynamics guide air over and through its body for extra downforce and speed The Eletre takes Lotus comfort to an unprecedented new level. The performance-oriented and technical design is visually lightweight, using ultra-premium materials to deliver an exceptional customer experience 52 |

|

FIRST CLASS CABIN The driver-focused cockpit and high centre console are inspired by the Lotus Emira and Evija, creating a cossetted feeling. The layering of materials and textures creates a truly luxurious feel 53 |

|

REFINED ELEGANCE Eletre’s interior is as comfortable as it is beautiful, combining highly durable materials and immersive infotainment The High Definition OLED central screen works in tandem with the digital passenger display The Eletre operating system is future-proof by design, updatable wirelessly 54 |

|

ELETRE OFFERS THE BEST PRICE-TO-VALUE PROPOSITION AMONG PEERS Model Eletre S+1 Cayenne 3.0T Urus 4.0T V8 S Pricing (US$ k) 114 127 410 Powertrain type BEV ICE ICE 0-100km acceleration (s) 4.5 6.2 3.6 Horsepower (hp) 612 340 640 Torque (Nm) 710 450 850 Driving range (WLTP, km) 600 638 602 Leading performance on acceleration, horsepower, and torque with a competitive price 55 Source: Company information 1. Eletre S+ is only offered in China, with more premium configuration than Eletre S |

|

STUNNING DEBUT DISPLAY AT AUTO SHANGHAI 2023 56 Source: Company Information • Lotus booth attracted over 100,000 visitors at Auto Shanghai 2023, one of the leading international automotive exhibitions and the first one held in China after the COVID-19 pandemic • A self-developed Flash Charging Robot was introduced, demonstrating Lotus cutting-edge luxurious 480kw fast charging solution • Eletre was displayed along with Evija, Emira and Eleven, exemplifying Lotus' modern, luxurious and sustainable features and rich sportscar heritage |

|

The One to Watch, 2021 Electric Awards Product Design of the Year, 2021 Overall Automotive Transportation, 2020 Global Design Awards 2,000 hp 1,500KW DELIVERED THROUGH 4 MOTORS 9.1s 0-186 MPH 0-300 KM/H 200mph (320 KM/H) MAX SPEED 1,887kg LIGHTWEIGHT BEV 1,700Nm TORQUE (WITH TORQUE VECTORING) 1,800kg DOWNPOWER Note: Evija was launched and manufactured by Lotus UK 57 THE WORLD’S FIRST PURE ELECTRIC BRITISH HYPERCAR |

|

400hp 298KW POWER 1,405kg LIGHTWEIGHT BEV 420Nm TORQUE 180mph 290 KM/H MAX SPEED Source: Company information Note: Emira was launched and manufactured by Lotus UK 58 4.5s 0-62 MPH 0-100 KM/H BEST PERFORMANCE LOTUS EMIRA: THE MOST ACCOMPLISHED LOTUS EVER MADE SPORTS CAR OF THE YEAR |

|

59 L CATTERTON HAS AN INCREDIBLE TRACK RECORD OF CONNECTING ICONIC BRANDS GENTLE FENDI Source: Public information The two brands came together to create an extraordinary capsule collection inspired by Gentle Monster’s innovative designs and Fendi’s exquisite craftsmanship x • L Catterton’s strategic relationship with LVMH enabled it to facilitate the collaboration between Gentle Monster and Fendi • L Catterton played a crucial role in enacting the collaboration between Birkenstock and Dior Combining functionality and elegance, the debut collection subtly pays tribute to Monsieur Dior’s passion for gardening x DIOR BY BIRKENSTOCK |

|

www.group-lotus.com All contents contained in this document are owned by Lotus. © Lotus 2023 |

Forward-Looking Statements

This document contains forward-looking statements within the meaning

of Section 27A of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the U.S. Securities

Exchange Act of 1934, that are based on beliefs and assumptions and on information currently available to Lotus Technology Inc. (“Lotus

Tech”) and L Catterton Asia Acquisition Corp (“LCAA”). All statements other than statements of historical

fact contained in this document are forward-looking statements. In some cases, you can identify forward-looking statements by terminology

such as “may”, “should”, “expect”, “intend”, “will”, “estimate”,

“anticipate”, “believe”, “predict”, “potential”, “forecast”, “plan”,

“seek”, “future”, “propose” or “continue”, or the negatives of these terms or variations

of them or similar terminology although not all forward-looking statements contain such terminology. Such forward-looking statements are

subject to risks, uncertainties, and other factors which could cause actual results to differ materially from those expressed or implied

by such forward looking statements.

These forward-looking statements are based upon estimates and

assumptions that, while considered reasonable by LCAA and its management, and Lotus Tech and its management, as the case may

be, are inherently uncertain. Factors that may cause actual results to differ materially from current expectations include, but are

not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of

definitive agreements with respect to the proposed business combination between LCAA, Lotus Tech and the other parties

thereto (the “Business Combination”); (2) the outcome of any legal proceedings that may be instituted against LCAA,

the combined company or others following the announcement of the Business Combination and any definitive agreements with respect