0001342219

false

--12-31

2023

Q2

0001342219

2023-01-01

2023-06-30

0001342219

2023-08-08

0001342219

2023-06-30

0001342219

2022-12-31

0001342219

2023-12-31

0001342219

2023-04-01

2023-06-30

0001342219

2022-04-01

2022-06-30

0001342219

2022-01-01

2022-06-30

0001342219

us-gaap:CommonStockMember

2021-12-31

0001342219

NLSC:CommonStockToBeIssuedMember

2021-12-31

0001342219

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001342219

us-gaap:RetainedEarningsMember

2021-12-31

0001342219

2021-12-31

0001342219

us-gaap:CommonStockMember

2022-03-31

0001342219

NLSC:CommonStockToBeIssuedMember

2022-03-31

0001342219

us-gaap:AdditionalPaidInCapitalMember

2022-03-31

0001342219

us-gaap:RetainedEarningsMember

2022-03-31

0001342219

2022-03-31

0001342219

us-gaap:CommonStockMember

2022-12-31

0001342219

NLSC:CommonStockToBeIssuedMember

2022-12-31

0001342219

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001342219

us-gaap:RetainedEarningsMember

2022-12-31

0001342219

us-gaap:CommonStockMember

2023-03-31

0001342219

NLSC:CommonStockToBeIssuedMember

2023-03-31

0001342219

us-gaap:AdditionalPaidInCapitalMember

2023-03-31

0001342219

us-gaap:RetainedEarningsMember

2023-03-31

0001342219

2023-03-31

0001342219

us-gaap:CommonStockMember

2022-01-01

2022-03-31

0001342219

NLSC:CommonStockToBeIssuedMember

2022-01-01

2022-03-31

0001342219

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-03-31

0001342219

us-gaap:RetainedEarningsMember

2022-01-01

2022-03-31

0001342219

2022-01-01

2022-03-31

0001342219

us-gaap:CommonStockMember

2022-04-01

2022-06-30

0001342219

NLSC:CommonStockToBeIssuedMember

2022-04-01

2022-06-30

0001342219

us-gaap:AdditionalPaidInCapitalMember

2022-04-01

2022-06-30

0001342219

us-gaap:RetainedEarningsMember

2022-04-01

2022-06-30

0001342219

us-gaap:CommonStockMember

2023-01-01

2023-03-31

0001342219

NLSC:CommonStockToBeIssuedMember

2023-01-01

2023-03-31

0001342219

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-03-31

0001342219

us-gaap:RetainedEarningsMember

2023-01-01

2023-03-31

0001342219

2023-01-01

2023-03-31

0001342219

us-gaap:CommonStockMember

2023-04-01

2023-06-30

0001342219

NLSC:CommonStockToBeIssuedMember

2023-04-01

2023-06-30

0001342219

us-gaap:AdditionalPaidInCapitalMember

2023-04-01

2023-06-30

0001342219

us-gaap:RetainedEarningsMember

2023-04-01

2023-06-30

0001342219

us-gaap:CommonStockMember

2022-06-30

0001342219

NLSC:CommonStockToBeIssuedMember

2022-06-30

0001342219

us-gaap:AdditionalPaidInCapitalMember

2022-06-30

0001342219

us-gaap:RetainedEarningsMember

2022-06-30

0001342219

2022-06-30

0001342219

us-gaap:CommonStockMember

2023-06-30

0001342219

NLSC:CommonStockToBeIssuedMember

2023-06-30

0001342219

us-gaap:AdditionalPaidInCapitalMember

2023-06-30

0001342219

us-gaap:RetainedEarningsMember

2023-06-30

0001342219

2023-01-01

2023-04-30

0001342219

2022-01-01

2022-04-30

0001342219

2023-04-30

0001342219

2022-04-30

0001342219

country:HK

2023-06-30

0001342219

country:HK

2023-01-01

2023-06-30

0001342219

country:HK

2022-01-01

2022-06-30

0001342219

country:HK

2022-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

☒ QUARTERLY REPORT PURSUANT TO SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2023

or

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from

To

Commission File Number 000-55909

NAMLIONG SKYCOSMOS,

INC.

(Exact name of registrant as specified in its charter)

| Nevada |

|

20-3240178 |

(State or other jurisdiction of

incorporation or organization) |

|

(IRS Employer

Identification No.) |

No. 357, Ren’ai Street

Yongkang District

Tainan City, Taiwan |

|

71072 |

| (Address of principal executive offices) |

|

(Zip Code) |

| +886-2542372 |

| (Registrant’s telephone number, including area code) |

| |

| |

| (Former name, former address and former fiscal year, if changed since last report) |

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| N/A |

|

N/A |

|

N/A |

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Yes ☐ No

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

☐ |

Accelerated filer |

☐ |

| Non-accelerated filer |

☒ |

Smaller reporting company |

☒ |

| |

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act) ☒ Yes ☐ No

The number of shares outstanding of the registrant’s

common stock, par value $0.001 per share, as of August 8, 2023, was 14,706,513.

TABLE OF CONTENTS

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form

10-Q includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and

Section 21E of the Securities Exchange Act of 1934, as amended that are not historical facts, and involve risks and uncertainties that

could cause actual results to differ materially from those expected and projected. All statements, other than statements of historical

facts, included in this Form 10-Q including, without limitation, statements in the “Market Overview” and “Management’s

Discussion and Analysis of Financial Condition and Results of Operations” regarding the Company’s market projections, financial

position, business strategy and the plans and objectives of management for future operations, events or developments which the Company

expects or anticipates will or may occur in the future, including such things as future capital expenditures (including the amount and

nature thereof); expansion and growth of the Company's business and operations; and other such matters are forward-looking statements.

These statements are based on certain assumptions and analyses made by the Company in light of its experience and its perception of historical

trends, current conditions and expected future developments, as well as other factors it believes are appropriate under the circumstances.

However, whether actual results or developments will conform with the Company's expectations and predictions is subject to a number of

risks and uncertainties, including general economic, market and business conditions; the business opportunities (or lack thereof) that

may be presented to and pursued by the Company; changes in laws or regulation; and other factors, most of which are beyond the control

of the Company.

These forward-looking statements

can be identified by the use of predictive, future-tense or forward-looking terminology, such as “believes,” “anticipates,”

“expects,” “estimates,” “plans,” “may,” “will,” or similar terms. These statements

appear in a number of places in this filing and include statements regarding the intent, belief or current expectations of the Company,

and its directors or its officers with respect to, among other things: (i) trends affecting the Company's financial condition or results

of operations for its limited history; (ii) the Company's business and growth strategies; and (iii) the Company's financing plans. Investors

are cautioned that any such forward-looking statements are not guarantees of future performance and involve significant risks and uncertainties,

and that actual results may differ materially from those projected in the forward-looking statements as a result of various factors. Such

factors that could adversely affect actual results and performance include, but are not limited to, the Company's limited operating history,

potential fluctuations in quarterly operating results and expenses, government regulation, technological change and competition.

Consequently, all of the forward-looking

statements made in this Form 10-Q are qualified by these cautionary statements and there can be no assurance that the actual results or

developments anticipated by the Company will be realized or, even if substantially realized, that they will have the expected consequence

to or effects on the Company or its business or operations. The Company assumes no obligations to update any such forward-looking statements.

PART I. FINANCIAL INFORMATION.

Item 1. Financial Statements

NAMLIONG SKYCOSMOS, INC.

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

| | |

June 30, 2023 | | |

December 31, 2022 | |

| | |

| | |

(Restated) | |

| ASSETS | |

| | | |

| | |

| Non-current asset: | |

| | | |

| | |

| Right-of-use asset | |

$ | 17,074 | | |

$ | – | |

| | |

| | | |

| | |

| Current asset: | |

| | | |

| | |

| Cash | |

| 23,195 | | |

| – | |

| | |

| | | |

| | |

| TOTAL ASSETS | |

$ | 40,269 | | |

$ | – | |

| | |

| | | |

| | |

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | |

| | | |

| | |

| Current liabilities: | |

| | | |

| | |

| Accrued liabilities | |

$ | 1,280,250 | | |

$ | 16,000 | |

| Lease liabilities | |

| 25,829 | | |

| – | |

| Amount due to a related party | |

| 23,195 | | |

| – | |

| Amount due to a director | |

| 120,351 | | |

| 53,821 | |

| | |

| | | |

| | |

| Total current liabilities | |

| 1,449,625 | | |

| 69,821 | |

| | |

| | | |

| | |

| Non-current liability: | |

| | | |

| | |

| Lease liabilities | |

| 5,732 | | |

| – | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| TOTAL LIABILITIES | |

| 1,455,357 | | |

| 69,821 | |

| | |

| | | |

| | |

| Commitments and contingencies | |

| – | | |

| – | |

| | |

| | | |

| | |

| STOCKHOLDERS’ DEFICIT | |

| | | |

| | |

| Preferred stock, 10,000,000 shares authorized, $0.001 par value, 0 shares issued and outstanding as of June 30, 2023 and December 31, 2022 | |

| – | | |

| – | |

| Common stock, 300,000,000 shares authorized, $0.001 par value, 14,706,513 and 14,706,513 shares issued and outstanding as of June 30, 2023 and December 31, 2022, respectively | |

| 14,706 | | |

| 14,706 | |

| Common stock to be issued, $0.001 par value, 2,000,000 and 0 shares as of June 30, 2023 and December 31, 2022, respectively | |

| 2,000 | | |

| – | |

| Additional paid-in capital | |

| 48,283,531 | | |

| 49,435,627 | |

| Accumulated deficit | |

| (49,715,325 | ) | |

| (49,520,154 | ) |

| | |

| | | |

| | |

| Stockholders’ deficit | |

| (1,415,088 | ) | |

| (69,821 | ) |

| | |

| | | |

| | |

| TOTAL LIABILITIES AND STOCKHOLDERS’ DEFICIT | |

$ | 40,269 | | |

$ | – | |

See accompanying notes to condensed consolidated

financial statements.

NAMLIONG SKYCOSMOS, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS

OF OPERATIONS

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

| | |

| | |

| | |

| | |

| |

| | |

Three months ended

June 30, | | |

Six months ended

June 30, | |

| | |

2023 | | |

2022 | | |

2023 | | |

2022 | |

| | |

| | |

| | |

| | |

| |

| Revenue, net | |

$ | – | | |

$ | – | | |

$ | – | | |

$ | – | |

| | |

| | | |

| | | |

| | | |

| | |

| Operating expenses: | |

| | | |

| | | |

| | | |

| | |

| General and administrative expenses | |

| (132,652 | ) | |

| (17,174 | ) | |

| (195,494 | ) | |

| (51,924 | ) |

| Total operating expenses | |

| (132,652 | ) | |

| (17,174 | ) | |

| (195,494 | ) | |

| (51,924 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| LOSS FROM OPERATION | |

| (132,652 | ) | |

| (17,174 | ) | |

| (195,494 | ) | |

| (51,924 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| Other income (expense): | |

| | | |

| | | |

| | | |

| | |

| Interest expense | |

| (77 | ) | |

| – | | |

| (77 | ) | |

| – | |

| Foreign exchange gain | |

| 400 | | |

| – | | |

| 400 | | |

| – | |

| Total other income | |

| 323 | | |

| – | | |

| 323 | | |

| – | |

| | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | |

| Income tax expense | |

| – | | |

| – | | |

| – | | |

| – | |

| | |

| | | |

| | | |

| | | |

| | |

| NET LOSS | |

$ | (132,329 | ) | |

$ | (17,174 | ) | |

$ | (195,171 | ) | |

$ | (51,924 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| Net loss per share – Basic and Diluted | |

$ | (0.00 | ) | |

$ | (0.00 | ) | |

$ | (0.00 | ) | |

$ | (0.00 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | |

Weighted average common shares outstanding –

Basic and Diluted | |

| 14,706,513 | | |

| 14,706,513 | | |

| 14,706,513 | | |

| 14,706,513 | |

See accompanying notes to condensed consolidated

financial statements.

NAMLIONG SKYCOSMOS, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS

OF CHANGES IN STOCKHOLDERS’ DEFICIT

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

Three and Six Months Ended June 30, 2023 and 2022 | |

| | |

Common stock | | |

Common stock to be issued | | |

Additional

Paid-in | | |

Accumulated | | |

Total Stockholders’ | |

| | |

Shares | | |

Amount | | |

Shares | | |

Amount | | |

Capital | | |

Deficit | | |

Deficit | |

| Balance as of January 1, 2022 | |

| 14,706,513 | | |

$ | 14,706 | | |

| – | | |

$ | – | | |

$ | 49,435,627 | | |

$ | (49,451,088 | ) | |

$ | (755 | ) |

| Net loss for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (34,750 | ) | |

| (34,750 | ) |

| Balance as of March 31, 2022 | |

| 14,706,513 | | |

$ | 14,706 | | |

| – | | |

$ | – | | |

$ | 49,435,627 | | |

$ | (49,485,838 | ) | |

$ | (35,505 | ) |

| Net loss for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (17,174 | ) | |

| (17,174 | ) |

| Balance as of June 30, 2022 | |

| 14,706,513 | | |

$ | 14,706 | | |

| – | | |

$ | – | | |

$ | 49,435,627 | | |

$ | (49,503,012 | ) | |

$ | (52,679 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance as of January 1, 2023 | |

| 14,706,513 | | |

$ | 14,706 | | |

| – | | |

$ | – | | |

$ | 49,435,627 | | |

$ | (49,520,154 | ) | |

$ | (69,821 | ) |

| Net loss for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (62,842 | ) | |

| (62,842 | ) |

| Balance as of March 31, 2023 | |

| 14,706,513 | | |

$ | 14,706 | | |

| – | | |

$ | – | | |

$ | 49,435,627 | | |

$ | (49,582,996 | ) | |

$ | (132,663 | ) |

| Acquisition of a subsidiary | |

| – | | |

| – | | |

| 2,000,000 | | |

| 2,000 | | |

| (1,152,096 | ) | |

| – | | |

| (1,150,096 | ) |

| Net loss for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (132,329 | ) | |

| (132,329 | ) |

| Balance as of June 30, 2023 | |

| 14,706,513 | | |

$ | 14,706 | | |

| 2,000,000 | | |

$ | 2,000 | | |

$ | 48,283,531 | | |

$ | (49,715,325 | ) | |

$ | (1,415,088 | ) |

See accompanying notes to condensed consolidated

financial statements.

NAMLIONG SKYCOSMOS, INC.

UNAUDITED CONDENSED STATEMENTS OF CASH FLOWS

(Currency expressed in United States Dollars

(“US$”))

| | |

| | |

| |

| | |

Six months ended June 30, | |

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| Cash flows from operating activities: | |

| | | |

| | |

| Net loss | |

$ | (195,171 | ) | |

$ | (51,924 | ) |

| Adjustments to reconcile net loss to net cash used in operating activities: | |

| | | |

| | |

| Depreciation of right-of-use assets | |

| 964 | | |

| – | |

| Non-cash lease expense | |

| 77 | | |

| – | |

| | |

| | | |

| | |

| Change in operating assets and liabilities: | |

| | | |

| | |

| Accrued liabilities | |

| 128,000 | | |

| 6,245 | |

| Net cash used in operating activities | |

| (66,130 | ) | |

| (45,679 | ) |

| | |

| | | |

| | |

| Cash flows from financing activities: | |

| | | |

| | |

| Advance from a director | |

| 66,530 | | |

| 45,679 | |

| Advance from a related party | |

| 23,195 | | |

| – | |

| Net cash provided by financing activities | |

| 89,725 | | |

| 45,679 | |

| | |

| | | |

| | |

| Effect on exchange rate change on cash and cash equivalents | |

| (400 | ) | |

| – | |

| | |

| | | |

| | |

| Net change in cash and cash equivalents | |

| 23,195 | | |

| – | |

| | |

| | | |

| | |

| BEGINNING OF PERIOD | |

| – | | |

| – | |

| | |

| | | |

| | |

| END OF PERIOD | |

$ | 23,195 | | |

$ | – | |

| | |

| | | |

| | |

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | |

| | | |

| | |

| Cash paid for income taxes | |

$ | – | | |

$ | – | |

| Cash paid for interest | |

$ | – | | |

$ | – | |

See accompanying notes to condensed consolidated

financial statements.

NAMLIONG SKYCOSMOS, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

FOR THE THREE AND SIX MONTHS ENDED JUNE 30,

2023 AND 2022

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

NOTE – 1 DESCRIPTION OF BUSINESS

AND ORGANIZATION

Namliong Skycosmos, Inc. (the “Company”

or “KRBF”) was incorporated as Gemwood Productions, Inc. under the laws of the State of Nevada on February 7, 2005. Gemwood

Productions, Inc. changed its name to Kreido Biofuels, Inc. on November 2, 2006. The Company took its current form on January 12, 2007

when Kreido Laboratories, Inc. (“Kreido Labs”), completed a reverse triangular merger with Kreido Biofuels, Inc. On April

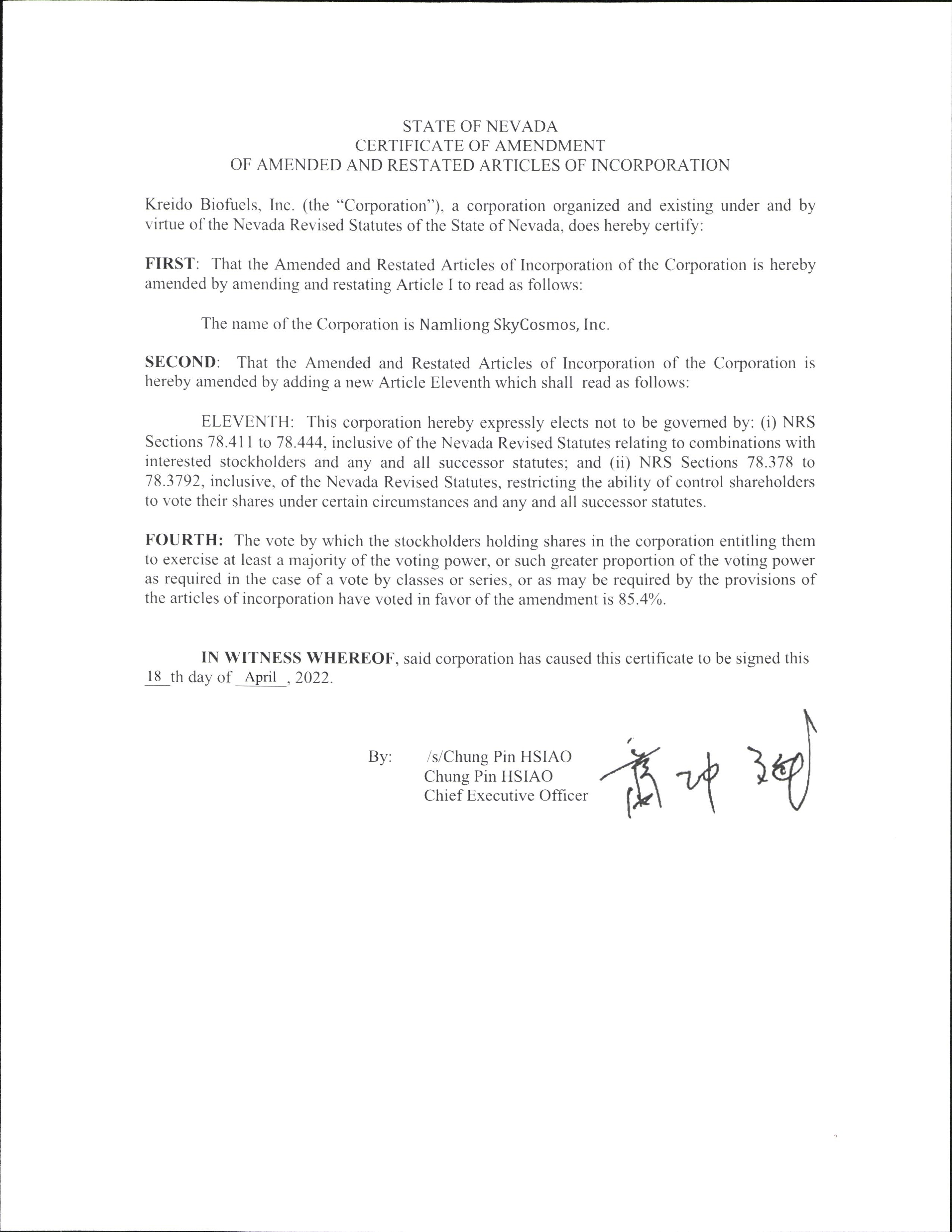

19, 2022, the Company changed its current name to Namliong SkyCosmos, Inc.

On March 31, 2023, the Company entered into a

Share Exchange Agreement with Continental Development Corporation, a Samoa company (“CDC”) that is controlled by Cheng Hsing

HSU, our sole executive officer and director, to purchase 1,000,000 shares of common stock of Orient Express & Co., Ltd. ("OEC"),

a SAMOA company, constituting all of the issued and outstanding ordinary shares of OEC, held by CDC. In consideration for such OEC shares,

the Company agreed to issue to CDC two million shares of its common stock at a per share price of $0.50. Mr. HSU is the director and sole

executive officer of CDC. The acquisition was consummated on April 30, 2023, and as a result, OEC became a wholly owned subsidiary of

the Company.

Prior to the Share Exchange, the Company was considered

as a shell company due to its nominal assets and limited operation. The transaction will be treated as a recapitalization of the Company.

Upon the Share Exchange between the Company and

OEC on March 31, 2023, is a merger of entities under common control that Mr. HSU is the common director and shareholder of both the Company

and OEC. Under the guidance in ASC 805 for transactions between entities under common control, the assets, liabilities and results of

operations, are recognized at their carrying amounts on the date of the Share Exchange, which required retrospective combination of the

Company and OEC for all periods presented.

The details of the Company’s subsidiary

are described below:

| Schedule of subsidiary information |

|

|

|

|

|

|

|

|

| Name |

|

Place of incorporation

and kind of

legal entity |

|

Principal activities

and place of operation |

|

Particulars of issued/

registered share

capital |

|

Effective interest

Held |

| |

|

|

|

|

|

|

|

|

| Orient Express & Co., Ltd (“OEC”) |

|

Samoa, a limited liability company |

|

Sales of rubber foaming machine |

|

1,000,000 issued shares of US$1 each |

|

100% |

NOTE – 2 SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES

The accompanying condensed consolidated financial

statements reflect the application of certain significant accounting policies as described in this note and elsewhere in the accompanying

condensed consolidated financial statements and notes.

These accompanying condensed consolidated financial

statements have been prepared in U.S. Dollars in conformity with generally accepted accounting principles in the United States of America

(“U.S. GAAP”) for interim financial information pursuant to the rules and regulations of the Securities and Exchange Commission

(the “SEC”). Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial

statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary to make the financial

statements not misleading have been included. Operating results for the interim period ended June 30, 2023 are not necessarily indicative

of the results that may be expected for the fiscal year ending December 31, 2023. The information included in this Form 10-Q should be

read in conjunction with Management’s Discussion and Analysis, and the financial statements and notes thereto included in the Company’s

Form 10-K for the fiscal year ended December 31, 2022 filed with the SEC on March 15, 2023.

| l |

Use of estimates and assumptions |

In preparing these condensed consolidated financial

statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheet

and revenues and expenses during the periods reported. Actual results may differ from these estimates.

Basic loss per share is calculated by dividing

the Company’s net loss applicable to common shareholders by the weighted average number of common shares during the period. Diluted

earnings per share is calculated by dividing the Company’s net income available to common shareholders by the diluted weighted average

number of shares outstanding during the period.

Accounts receivables are recorded at the invoiced

amount and do not bear interest, which are due within contractual payment terms, generally required deposits received in advance and the

remaining is due upon installation and inspection. Credit is extended based on evaluation of a customer's financial condition, the customer

credit-worthiness and their payment history. Accounts receivable outstanding longer than the contractual payment terms are considered

past due. Past due balances over 90 days and over a specified amount are reviewed individually for collectability. At the end of fiscal

year, the Company specifically evaluates individual customer’s financial condition, credit history, and the current economic conditions

to monitor the progress of the collection of accounts receivables. The Company will consider the allowance for doubtful accounts for any

estimated losses resulting from the inability of its customers to make required payments. For the receivables that are past due or not

being paid according to payment terms, the appropriate actions are taken to exhaust all means of collection, including seeking legal resolution

in a court of law. Account balances are charged off against the allowance after all means of collection have been exhausted and the potential

for recovery is considered remote. The Company does not have any off-balance-sheet credit exposure related to its customers.

The Company adopted Accounting Standards Update

("ASU") No. 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”).

Under ASU 2014-09, the Company recognizes revenue

when control of the promised goods or services is transferred to customers, in an amount that reflects the consideration the Company expects

to be entitled to in exchange for those goods or services.

The Company applies the following five steps in

order to determine the appropriate amount of revenue to be recognized as it fulfills its obligations under each of its agreements:

| · |

identify the contract with a customer; |

| · |

identify the performance obligations in the contract; |

| · |

determine the transaction price; |

| · |

allocate the transaction price to performance obligations in the contract; and |

| · |

recognize revenue as the performance obligation is satisfied. |

The Company’s revenue is derived from the

sales of rubber foaming machine. The Company considers customer order confirmations to be a contract with the customer. Customer confirmations

are executed at the time an order is placed. Revenue is recognized when control of the product is transferred to the customer (i.e., when

the Company’s performance obligation is satisfied), which typically occurs at shipment date. As a result, the Company has a present

and unconditional right to payment and record its accounts receivable.

For each contract, the Company considers the promise

to transfer products to be the only identified performance obligation. The Company’s revenues are recognized at a point in time.

| l |

Cash and Cash Equivalent |

Cash and cash equivalents are carried at cost

and represent cash on hand, demand deposits placed with banks or other financial institutions and all highly liquid investments with an

original maturity of three months or less as of the purchase date of such investments.

| l |

Impairment of Long-lived Assets |

In accordance with the provisions of ASC Topic

360, “Impairment or Disposal of Long-Lived Assets”, all long-lived assets such as intangible asset held and used by the Company

are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.

Recoverability of assets to be held and used is evaluated by a comparison of the carrying amount of an asset to its estimated future undiscounted

cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured

by the amount by which the carrying amounts of the assets exceed the fair value of the assets.

The Company adopted Topic 842, Leases (“ASC

842”). At the inception of an arrangement, the Company determines whether the arrangement is or contains a lease based on the unique

facts and circumstances present. Leases with a term greater than one year are recognized on the balance sheet as right-of-use (“ROU”)

assets, lease liabilities and long-term lease liabilities. The Company has elected not to recognize on the balance sheet leases with terms

of one year or less. Operating lease liabilities and their corresponding right-of-use assets are recorded based on the present value of

lease payments over the expected remaining lease term. However, certain adjustments to the right-of-use asset may be required for items

such as prepaid or accrued lease payments. The interest rate implicit in lease contracts is typically not readily determinable. As a result,

the Company utilizes its incremental borrowing rates, which are the rates incurred to borrow on a collateralized basis over a similar

term an amount equal to the lease payments in a similar economic environment.

In accordance with the guidance in ASC 842, components

of a lease should be split into three categories: lease components (e.g. land, building, etc.), non-lease components (e.g. common area

maintenance, consumables, etc.), and non-components (e.g. property taxes, insurance, etc.). Subsequently, the fixed and in-substance fixed

contract consideration (including any related to non-components) must be allocated based on the respective relative fair values to the

lease components and non-lease components.

Lease expense is recognized on a straight-line

basis over the lease terms. Lease expense includes amortization of the ROU assets and accretion of the lease liabilities. Amortization

of ROU assets is calculated as the periodic lease cost less accretion of the lease liability. The amortized period for ROU assets is limited

to the expected lease term.

The Company has elected a practical expedient

to combine the lease and non-lease components into a single lease component. The Company also elected the short-term lease measurement

and recognition exemption and does not establish ROU assets or lease liabilities for operating leases with terms of 12 months or less.

The Company follows the guidance of the ASC Topic

820-10, Fair Value Measurements and Disclosures ("ASC 820-10"), with respect to financial assets and liabilities that are measured

at fair value. ASC 820-10 establishes a three-tier fair value hierarchy that prioritizes the inputs used in measuring fair value as follows:

| ● |

Level 1 - Inputs are based upon unadjusted quoted prices for identical instruments traded in active markets; |

| ● |

Level

2 - Inputs are based upon quoted prices for similar instruments in active markets, quoted prices for identical or similar

instruments in markets that are not active, and model-based valuation techniques (e.g., the Black-Scholes Option-Pricing model) for

which all significant inputs are observable in the market or can be corroborated by observable market data for substantially the

full term of the assets or liabilities. Where applicable, these models project future cash flows and discount the future amounts to

a present value using market-based observable inputs; and |

| ● |

Level 3 - Inputs are generally unobservable and typically reflect management’s estimates of assumptions that market participants would use in pricing the asset or liability. The fair values are therefore determined using model-based techniques, including option pricing models and discounted cash flow models. |

The carrying value of the Company’s financial

instruments: cash and cash equivalents, restricted cash, accounts receivable, loans receivable and amount due to or from a related party,

approximate their fair values because of the short-term nature of these financial instruments.

Fair value estimates are made at a specific point

in time based on relevant market information about the financial instrument. These estimates are subjective in nature and involve uncertainties

and matters of significant judgment and, therefore, cannot be determined with precision. Changes in assumptions could significantly affect

the estimates.

The Company adopted the ASC 740 Income tax

provisions of paragraph 740-10-25-13, which addresses the determination of whether tax benefits claimed or expected to be claimed on a

tax return should be recorded in the condensed consolidated financial statements. Under paragraph 740-10-25-13, the Company may recognize

the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination

by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the condensed consolidated financial

statements from such a position should be measured based on the largest benefit that has a greater than fifty percent (50%) likelihood

of being realized upon ultimate settlement. Paragraph 740-10-25-13 also provides guidance on de-recognition, classification, interest

and penalties on income taxes, accounting in interim periods and requires increased disclosures. The Company had no material adjustments

to its liabilities for unrecognized income tax benefits according to the provisions of paragraph 740-10-25-13.

The estimated future tax effects of temporary

differences between the tax basis of assets and liabilities are reported in the accompanying balance sheets, as well as tax credit carry-backs

and carry-forwards. The Company periodically reviews the recoverability of deferred tax assets recorded on its balance sheets and provides

valuation allowances as management deems necessary.

| |

l |

Uncertain tax positions |

The Company did not take any uncertain tax positions

and had no adjustments to its income tax liabilities or benefits pursuant to the ASC 740 provisions of Section 740-10-25 for the periods

ended June 30, 2023 and 2022.

The Company follows the ASC 850-10, Related

Party for the identification of related parties and disclosure of related party transactions.

Pursuant to section 850-10-20 the related parties

include a) affiliates of the Company; b) entities for which investments in their equity securities would be required, absent the election

of the fair value option under the Fair Value Option Subsection of section 825–10–15, to be accounted for by the equity method

by the investing entity; c) trusts for the benefit of employees, such as pension and Income-sharing trusts that are managed by or under

the trusteeship of management; d) principal owners of the Company; e) management of the Company; f) other parties with which the Company

may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one

of the transacting parties might be prevented from fully pursuing its own separate interests; and g) other parties that can significantly

influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting

parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully

pursuing its own separate interests.

The condensed consolidated financial statements

shall include disclosures of material related party transactions, other than compensation arrangements, expense allowances, and other

similar items in the ordinary course of business. However, disclosure of transactions that are eliminated in the preparation of consolidated

or combined financial statements is not required in those statements. The disclosures shall include: a) the nature of the relationship(s)

involved; b) a description of the transactions, including transactions to which no amounts or nominal amounts were ascribed, for each

of the periods for which income statements are presented, and such other information deemed necessary to an understanding of the effects

of the transactions on the financial statements; c) the dollar amounts of transactions for each of the periods for which income statements

are presented and the effects of any change in the method of establishing the terms from that used in the preceding period; and d) amount

due from or to related parties as of the date of each balance sheet presented and, if not otherwise apparent, the terms and manner of

settlement.

| l |

Commitments and contingencies |

The Company follows the ASC 450-20, Commitments

to report accounting for contingencies. Certain conditions may exist as of the date the financial statements are issued, which may result

in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company assesses such

contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal

proceedings that are pending against the Company or un-asserted claims that may result in such proceedings, the Company evaluates the

perceived merits of any legal proceedings or un-asserted claims as well as the perceived merits of the amount of relief sought or expected

to be sought therein.

If the assessment of a contingency indicates that

it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would

be accrued in the Company’s condensed consolidated financial statements. If the assessment indicates that a potentially material

loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent

liability, and an estimate of the range of possible losses, if determinable and material, would be disclosed.

Loss contingencies considered remote are generally

not disclosed unless they involve guarantees, in which case the guarantees would be disclosed. Management does not believe, based upon

information available at this time that these matters will have a material adverse effect on the Company’s financial position, results

of operations or cash flows. However, there is no assurance that such matters will not materially and adversely affect the Company’s

business, financial position, and results of operations or cash flows.

| l |

Recent accounting pronouncements |

The FASB established the Accounting Standards

Codification (“Codification” or “ASC”) as the source of authoritative accounting principles recognized by the

FASB to be applied by nongovernmental entities in the preparation of financial statements in accordance with generally accepted accounting

principles in the United States (“GAAP”).

Rules and interpretative releases of the Securities

and Exchange Commission (“SEC”) issued under authority of federal securities laws are also sources of GAAP for SEC registrants.

Other accounting standards that have been issued

or proposed by FASB that do not require adoption until a future date are not expected to have a material impact on the financial statements

upon adoption. The Company does not discuss recent pronouncements that are not anticipated to have an impact on or are unrelated to its

financial condition, results of operations, cash flows or disclosures.

NOTE – 3 GOING CONCERN UNCERTAINTIES

The accompanying condensed consolidated financial

statements have been prepared using the going concern basis of accounting, which contemplates the realization of assets and the satisfaction

of liabilities in the normal course of business.

In order to continue as a going concern, the Company

will need, among other things, additional capital resources. Management's plan is to obtain such resources for the Company by obtaining

capital from management sufficient to meet its minimal operating expenses and seeking equity and/or debt financing. However, Management

cannot provide any assurances that the Company will be successful in accomplishing any of its plans, which raises substantial doubt about

the ability of the Company to continue as a going concern.

The ability of the Company to continue as a going

concern is dependent upon its ability to successfully accomplish the plans described in the preceding paragraph and eventually secure

other sources of financing and attain profitable operations. The accompanying condensed consolidated financial statements do not include

any adjustments that might be necessary if the Company is unable to continue as a going concern.

NOTE – 4 LEASES

Operating lease right-of-use (“ROU”)

asset and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. ROU asset

represents the Company’s right to use an underlying asset for the lease term and lease liabilities represent the Company’s

obligation to make lease payments arising from the lease.

As of June 30, 2023 and December 31, 2022, right-of-use

assets consisted of the following:

| Right of use assets | |

June 30, 2023 | | |

December 31, 2022 | |

| Operating lease: | |

| | | |

| | |

| Lease of office at cost | |

$ | 31,349 | | |

$ | – | |

| Less: accumulated amortization | |

| (14,275 | ) | |

| – | |

| Right-of-use asset, net | |

$ | 17,074 | | |

$ | – | |

| | |

| | | |

| | |

| Lease liabilities: | |

| | | |

| | |

| Current lease liabilities | |

$ | 25,829 | | |

$ | – | |

| Non-current lease liabilities | |

| 5,732 | | |

| – | |

| Total lease liabilities | |

$ | 31,561 | | |

$ | – | |

Maturities of operating lease liabilities as of

June 30, 2023 were as follows:

| Schedule of lease maturity | |

Operating lease | |

| For the period ending June 30, | |

| | |

| 2024 | |

$ | 26,409 | |

| 2025 | |

| 5,821 | |

| 2026 | |

| – | |

| 2027 | |

| – | |

| 2028 | |

| – | |

| Thereafter | |

| – | |

| Total future minimum lease payments | |

| 32,230 | |

| Less: imputed interest | |

| (669 | ) |

| Present value of operating lease liabilities | |

$ | 31,561 | |

The Company leases various office and their lease

agreements are typically contracted for the fixed periods of 2.5 to 3 years.

NOTE-5 ACCRUED LIABILITIES

| Schedule of accrued liabilities | |

June 30, 2023 | | |

December 31, 2022 | |

| | |

| | |

| |

| Accrued salaries | |

$ | 1,255,750 | | |

$ | – | |

| Other accrued expenses | |

| 24,500 | | |

| 16,000 | |

| Total accrued liabilities | |

$ | 1,280,250 | | |

$ | 16,000 | |

NOTE – 6 AMOUNT DUE TO A DIRECTOR

AND A RELATED PARTY

The amount represented temporary advances from

a related party and Company’s director, which were unsecured, interest-free and no fixed terms of repayment.

NOTE – 7 STOCKHOLDERS’ DEFICIT

Common Stock

The Company’s Articles of Incorporation

authorize the issuance of up to 300,000,000 common shares, par value $0.001 per share, and 10,000,000 preferred shares, also $0.001 par

value. There were 14,706,513 shares and 14,706,513 shares of common stock outstanding at June 30, 2023 and December 31, 2022, respectively.

There were no preferred shares outstanding during any periods presented.

Common Stock to be issued

On March 31, 2023, the Company entered into a

Share Exchange Agreement with Continental Development Corporation, a Samoa company (“CDC”) that is controlled by Cheng Hsing

HSU, our sole executive officer and director, to purchase 1,000,000 shares of common stock of Orient Express & Co., Ltd. (“OEC”),

a SAMOA company, constituting all of the issued and outstanding ordinary shares of OEC, held by CDC. In consideration for such OEC shares,

the Company agreed to issue to CDC two million shares of its common stock at a per share price of $0.50.

As of June 30, 2023 and December 31, 2022, the

Company had 2,000,000 and 0 shares of its common stock committed to be issued but pending to be consummated, respectively.

NOTE – 8 INCOME TAX

United States of America

On December 22, 2017, the 2019 Tax Cuts and Jobs

Act (the “Tax Act”) was enacted into law including a one-time mandatory transition tax on accumulated foreign earnings and

a reduction of the corporate income tax rate to 21% effective January 1, 2018, among others. We are required to recognize the effect of

the tax law changes in the period of enactment, such as determining the transition tax, remeasuring our U.S. deferred tax assets and liabilities

as well as reassessing the net realizability of our deferred tax assets and liabilities. The Company does not have any foreign earnings

and therefore, we do not anticipate the impact of a transition tax.

The cumulative tax effect at the expected rate

of 21% as of June 30, 2023 and December 31, 2022 of significant items comprising our net deferred tax amount is as follows:

| Schedule of deferred tax asset | |

June 30, 2023 | | |

December 31, 2022 | |

| | |

| | |

| |

| Net operating loss carryforward | |

$ | 49,595,184 | | |

$ | 49,520,154 | |

| | |

| | | |

| | |

| Deferred tax asset | |

| 10,414,988 | | |

| 10,399,232 | |

| Less: valuation allowance | |

| (10,414,988 | ) | |

| (10,399,232 | ) |

| Net deferred tax asset | |

$ | – | | |

$ | – | |

At June 30, 2023, the Company had net operating

loss carry forwards of approximately $49,595,184 that may be offset against future taxable income. The Tax Act also changed the rules

on net operating loss carry forwards. The 20-year limitation was eliminated, giving the taxpayer the ability to carry forward losses indefinitely.

However, NOL carry forward arising after January 1, 2020, will now be limited to 80 percent of taxable income.

No tax benefit has been reported in the period

ended June 30, 2023, the Company’s financial statements since the potential tax benefit is offset by a valuation allowance of the

same amount. Due to the change in ownership provisions of the Tax Reform Act of 1986, net operating loss carry forwards for federal income

tax reporting purposes are subject to annual limitations. A change in ownership may limit net operating loss carry forwards in future

years. The benefits of our deferred tax assets, including our NOLs, built-in losses and tax credits would be reduced or potentially eliminated

if we experienced an “ownership change” under Section 382.

Hong Kong

OEC is subject to Hong Kong Profits Tax at the

two-tiered profits tax rates from 8.25% to 16.5% on the estimated assessable profits arising in Hong Kong.

The reconciliation of income tax rate to the effective

income tax rate for the six months ended June 30, 2023 and 2022 is as follows:

| Reconciliation of income tax expense | |

Six months ended June 30 | |

| | |

2023 | | |

2022 | |

| | |

| | |

| |

| Loss before income taxes | |

$ | (120,141 | ) | |

$ | – | |

| Statutory income tax rate | |

| 16.5% | | |

| 16.5% | |

| Income tax expense at statutory rate | |

| (19,823 | ) | |

| – | |

| Non-deductible expenses | |

| 19,823 | | |

| – | |

| Income tax expense | |

$ | – | | |

$ | – | |

As of June 30, 2023, the operations in Hong Kong

incurred $826,388 of cumulative net operating losses which can be carried forward to offset future taxable income. The net operating loss

carryforwards has no expiry under Hong Kong tax regime. The Company has provided for a full valuation allowance against the deferred tax

assets of $136,354 on the expected future tax benefits from the net operating loss carryforwards as the management believes it is more

likely than not that these assets will not be realized in the future.

The following table sets forth the significant

components of the deferred tax assets of the Company as of June 30, 2023 and December 31, 2022:

| Deferred tax assets - Hong Kong | |

June 30, 2023 | | |

December 31, 2022 | |

| | |

| | |

| |

| Deferred tax assets: | |

| | | |

| | |

| Net operating loss carryforwards | |

| | | |

| | |

| -Hong Kong | |

$ | 136,354 | | |

$ | – | |

| Less: valuation allowance | |

| (136,354 | ) | |

| – | |

| Net deferred tax asset | |

$ | – | | |

$ | – | |

NOTE – 9 RELATED PARTY TRANSACTIONS

During the three and six months ended June 30,

2023 and 2022, the Company has been provided with free office space by its shareholders. The management determined that such cost is nominal

and did not recognize the rent expense in its financial statements.

For the three months ended June 30, 2023 and 2022,

the Company paid the allowance of $25,000 and $0 to the director for his service.

For the six months ended June 30, 2023 and 2022,

the Company paid the allowance of $25,000 and $0 to the director for his service.

On March 31, 2023, the Company entered into a

Share Exchange Agreement with Continental Development Corporation, a Samoa company (“CDC”) that is controlled by Cheng Hsing

HSU, our sole executive officer and director, to purchase 100% equity interest (equal to 1,000,000 shares of common stock) of Orient Express

& Co., Ltd. (“OEC”), a SAMOA company, constituting all of the issued and outstanding ordinary shares of OEC. NLSC will issue

2 million shares of its common stock at a price of $0.5 per share to CDC, the sole shareholder of OEC. The acquisition is considered as

related party transaction, whereas Mr. Cheng Hsing HSU is a sole shareholder of the Company and also currently controls OEC.

Apart from the transactions and balances detailed

elsewhere in these accompanying financial statements, the Company has no other significant or material related party transactions during

the periods presented.

NOTE – 10 COMMITMENTS AND CONTINGENCIES

As of June 30, 2023, the Company has no material

commitments or contingencies.

NOTE – 11 SUBSEQUENT EVENTS

In accordance with ASC Topic 855, “Subsequent

Events”, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date

but before condensed consolidated financial statements are issued, the Company has evaluated all events or transactions that occurred

after June 30, 2023, up through the date the Company issued the unaudited condensed consolidated financial statements.

Item 2. Management’s Discussion

and Analysis of Financial Condition and Results of Operations.

Namliong SkyCosmos, Inc. (“we” or

the “Company”) was incorporated on February 7, 2005 under the name Gemwood Productions. On November 2, 2006, we

changed our name to Kreido Biofuels, Inc. On April 19, 2022, the Company changed its name to Namliong SkyCosmos, Inc.

Our registration statement

on Form SB-2, file number 333-140718, became effective on June 28, 2007. Subsequent to the filing of our Annual Report on Form 10-K

for the year ended December 31, 2008, we continued to file annual and quarterly reports with the Securities and Exchange Commission on

a voluntary basis through the quarter ended September 30, 2009. On February 16, 2009, we elected to terminate our registration and

our election to file periodic reports. On March 2, 2018, we filed a registration statement on Form 10, and the registration statement

became effective on May 8, 2018.

On November 10, 2017, the

Company issued 142,924,167 shares of common stock to Reed Petersen, its then officer and director in consideration of cash of $21,434

paid by him to satisfy accounts payable of the Company, and in conversion of $150,075 in accounts payable which he had acquired from the

owners of that debt. This transaction was exempt under section 4(2) of the Securities Act of 1933 as one not involving any public solicitation

or public offering, and was also exempt under Section 4(5) as an offering solely to accredited investors not involving any public solicitation

or public offering.

On June 5, 2018, the Company

and its sole officer and director, G. Reed Petersen, entered into that certain Stock Purchase Agreement (the “Stock Purchase

Agreement”), pursuant to which Mr. Petersen agreed to sell to certain purchasers an aggregate of 142,924,167 shares of common

stock of the Company (the “Control Shares”), representing approximately 73% of the issued and outstanding stock of

the Company, for aggregate cash consideration of $420,000 in accordance with the terms and conditions of the Stock Purchase Agreement.

The sale of the Control Shares consummated on June 29, 2018. In connection with the sale of the Control Shares, G. Reed Petersen resigned

from his positions as the sole executive officer and director of the Company, effective June 29, 2018. Mr. Petersen’s departure

was not due to any dispute or disagreement with the Company on any matter related to the Company’s operations, policies or practices.

Concurrently, the Board of Directors appointed Wai Lim Wong to fill the vacancies created by Mr. Petersen’s resignation, and

to serve as the Company’s sole Director, Chief Executive Officer, Chief Financial Officer and Secretary.

On September 7, 2021, Board

of Directors Board of Directors accepted the resignation of Wai Lim Wong, and appointed CHAN Kwok Wai Davy as a new member of the Board

of Directors and CEO.

On December 14, 2021, the

Company, nine stockholders (the “Selling Stockholders”) and six purchasers (the “Purchasers”) entered

into a Stock Purchase Agreement (the “SPA”), pursuant to which the Purchasers agreed to purchase from the Selling Stockholders

13,099,243 shares of common stock of the Company, par value $0.001 (collectively, the “Shares”), constituting approximately

89% of the issued and outstanding shares of common stock of the Company, for aggregate consideration of Four Hundred Twenty Thousand Dollars

($420,000) in accordance with the terms and conditions of the SPA. The acquisition of the Shares consummated on December 20, 2021, and

the Shares were ultimately purchased by the following individuals:

| Selling Shareholder |

No. of Common Stock |

Purchaser |

| DOU Chu Ju |

554,856 |

PG MAX & CO, LLC |

| ZHANG Chao |

214,387 |

CHEN,HSUEH-NI |

| HEUNG Kin Leung Kenny |

55,000 |

HSIAO, CHUNG-PIN |

| HEUNG Pak Kuen |

55,000 |

HSIAO, CHUNG-PIN |

| HEUNG Teui Yee |

55,000 |

HSIAO, YU-CHIAO |

| KWAN Chin Man |

55,000 |

HSIAO, YU-CHIAO |

| LEUNG Wong Hung |

55,000 |

HSU, CHENG-HSING |

| MAK Chit Ming Brian |

55,000 |

HSU, CHENG-HSING |

| Pang King Sau Nelson |

12,000,000 |

Orient Express & Co., Ltd. |

| |

|

|

| Total |

13,099,243 |

|

Orient Express & Co.,

Ltd. holds a controlling interest in the Company, and may unilaterally determine the election of the Board and other substantive matters

requiring approval of the Company’s stockholders. Cheng Hsing Hsu, our new Chief Financial Officer and Director, is the director

and controlling shareholder of Orient Express & Co., Ltd.

Upon the consummation of the

sale, Chan Kwok Wai Davy, our sole executive officer and director, resigned from all of his positions with the Company, effective December

20, 2021. His resignation was not due to any dispute or disagreement with the Company on any matter relating to the Company’s operations,

policies or practices.

Concurrently with such resignation,

the following individuals were appointed to serve in the positions set forth next to their names, until the next annual meeting of stockholders

of the Company and until such director’s successor is elected and qualified or until such director’s earlier death, resignation

or removal:

| Name |

Position |

| HSIAO, Chung Pin |

Chief Executive Officer and Director |

| HSIAO, Yu-Chiao |

Secretary and Director |

| HSU, Cheng Hsing |

Chief Financial Officer and Director |

Chung Pin HSIAO and Yu Chiao

HSIAO are siblings.

Effective May 31, 2022, Chung

Pin HSIAO resigned from his positions as the Chief Executive Officer and Director of Namliong SkyCosmos, Inc. (the “Company”),

and Yu Chiao HSIAO resigned from her positions as the Secretary and Director of the Company. The departures of Mr. HSIAO and Ms. HSIAO

were for personal reasons and not due to any disagreement with the Company on any matter related to the Company’s operations, policies

or practices.

In connection with the foregoing

resignations, the Board of Directors of the Company appointed Cheng Hsing HSU, our current Chief Financial Officer and Director, to serve

as the Company’s Chief Executive Officer and Secretary, effective May 31, 2022.

Except as set forth in the

foregoing, none of the directors or executive officers has a direct family relationship with any of the Company’s directors or executive

officers, or any person nominated or chosen by the Company to become a director or executive officer. All officers and directors will

serve in his or her positions without compensation. The Company hopes to enter into a compensatory arrangement with each officer in the

future.

Our current business

is to seek to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination

with one or more businesses. Our acquisition strategy is to assess a broad range of potential business combination targets and complete

a business combination. In doing so, we will evaluate the historical financial statements of the target, its management, and projected

future results. In evaluating a prospective target business, we expect to conduct a thorough due diligence review that will encompass,

among other things, meetings with incumbent management and employees, document reviews, inspection of facilities, as well as a review

of financial and other information that will be made available to us.

Results of Operations

Following is management’s

discussion of the relevant items affecting results of operations for the three and six months ended June 30, 2022 and 2021.

Comparison of the three months

ended June 30, 2023 and 2022

Revenues, net.

The Company has not generated revenues during the three months ended June 30, 2023 and 2022.

General and

Administrative Expenses. For the three months ended June 30, 2023, the Company had general and administrative expenses of $132,652,

as compared to $17,174 for the same period ended June 30, 2022. The increase was mainly due to the addition of salaries, depreciation

of right-of-use assets, legal fee, accounting and audit fee incurred by the Company.

Net Loss.

For the three months ended June 30, 2023, the Company incurred a net loss of $132,329, as compared to a net loss of $17,174 for the same

period ended June 30, 2022. The increase in net loss was due to the increase in salaries, depreciation of right-of-use assets,

professional fees and general and administrative fees incurred by the Company.

Comparison of the six months

ended June 30, 2023 and 2022

Revenues, net.

The Company has not generated revenues during the six months ended June 30, 2023 and 2022.

General and

Administrative Expenses. For the six months ended June 30, 2023, the Company had general and administrative expenses of $195,494,

as compared to $51,924 for the same period ended June 30, 2022. The increase was mainly due to the addition of salaries, depreciation

of right-of-use assets, legal fee, accounting and audit fee incurred by the Company.

Net Loss.

For the six months ended June 30, 2023, the Company incurred a net loss of $195,171, as compared to a net loss of $51,924 for the same

period ended June 30, 2022. The increase in net loss was due to the increase in in salaries, depreciation of right-of-use

assets, professional fees and general and administrative fees incurred by the Company.

Liquidity and Capital Resources

As of June 30,

2023, our primary source of liquidity consisted of $23,195 in cash and cash equivalents. We hold most of our cash reserves in local checking

accounts with local financial institutions. Since inception, we have financed our operations through a combination of short and long-term

loans, and through the private placement of our common stock.

We have sustained

significant net losses which have resulted in a total stockholders’ deficit as of June 30, 2023 of $1,415,088 and are currently

experiencing a substantial shortfall in operating capital which raises doubt about our ability to continue as a going concern. We anticipate

a net loss for the six months ended June 30, 2023 and with the expected cash requirements for the coming months, without additional cash

inflows from an increase in revenues combined with continued cost-cutting or a receipt of cash from capital investment, there is substantial

doubt as to the Company’s ability to continue operations.

There is presently

no agreement in place with any source of financing for the Company and we cannot assure you that the Company will be able to raise any

additional funds, or that such funds will be available on acceptable terms. Funds raised through future equity financing will likely

be substantially dilutive to current shareholders. Lack of additional funds will materially affect the Company and its business

and may cause us to cease operations. Consequently, shareholders could incur a loss of their entire investment in the Company.

Net Cash Used in Operating Activities

For the six months ended June 30, 2023,

net cash used in operating activities was $66,130, which consisted primarily of a net loss of $195,171, and offset by an increase in accrued

liabilities of $128,000, depreciation of right-of-use asset of $964, non-cash expense related to lease liabilities of $77.

For the six months ended June 30, 2022,

net cash used in operating activities was $45,679, which consisted primarily of a net loss of $51,924, and an increase in accrued liabilities

of $6,245.

Net Cash Provided By Investing Activities

There was no net cash used in or provided

by investing activities during the six months ended June 30, 2023 and 2022.

Net Cash Provided By Financing Activities

For the six months ended June 30, 2023,

net cash provided by financing activities was $89,725, which consisted of advance from a director of $66,530 and advance from a related

party $23,195.

For the six months ended June 30, 2022,

net cash provided by financing activities was $45,679, from advance from a director of $45,679.

Off-Balance Sheet Arrangements

We do not have

any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes

in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material

to investors.

Contractual Obligations

As a “smaller

reporting company” as defined by Item 10 of Regulation S-K, the Company is not required to provide this information.

Critical accounting policies

| |

l |

Use of estimates and assumptions |

In preparing these condensed consolidated financial

statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheet

and revenues and expenses during the periods reported. Actual results may differ from these estimates.

Basic loss per share is calculated by dividing

the Company’s net loss applicable to common shareholders by the weighted average number of common shares during the period. Diluted

earnings per share is calculated by dividing the Company’s net income available to common shareholders by the diluted weighted average

number of shares outstanding during the period.

The Company adopted the ASC 740 Income tax

provisions of paragraph 740-10-25-13, which addresses the determination of whether tax benefits claimed or expected to be claimed on a

tax return should be recorded in the condensed financial statements. Under paragraph 740-10-25-13, the Company may recognize the tax benefit

from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing

authorities, based on the technical merits of the position. The tax benefits recognized in the condensed financial statements from such

a position should be measured based on the largest benefit that has a greater than fifty percent (50%) likelihood of being realized upon

ultimate settlement. Paragraph 740-10-25-13 also provides guidance on de-recognition, classification, interest and penalties on income

taxes, accounting in interim periods and requires increased disclosures. The Company had no material adjustments to its liabilities for

unrecognized income tax benefits according to the provisions of paragraph 740-10-25-13.

The estimated future tax effects of temporary

differences between the tax basis of assets and liabilities are reported in the accompanying balance sheets, as well as tax credit carry-backs

and carry-forwards. The Company periodically reviews the recoverability of deferred tax assets recorded on its balance sheets and provides

valuation allowances as management deems necessary.

| |

l |

Uncertain tax positions |

The Company did not take any uncertain tax positions

and had no adjustments to its income tax liabilities or benefits pursuant to the ASC 740 provisions of Section 740-10-25 for the periods

ended June 30, 2023 and 2022.

The Company follows the ASC 850-10, Related

Party for the identification of related parties and disclosure of related party transactions.

Pursuant to section 850-10-20 the related parties

include a) affiliates of the Company; b) entities for which investments in their equity securities would be required, absent the election

of the fair value option under the Fair Value Option Subsection of section 825–10–15, to be accounted for by the equity method

by the investing entity; c) trusts for the benefit of employees, such as pension and Income-sharing trusts that are managed by or under

the trusteeship of management; d) principal owners of the Company; e) management of the Company; f) other parties with which the Company

may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one

of the transacting parties might be prevented from fully pursuing its own separate interests; and g) other parties that can significantly

influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting

parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully

pursuing its own separate interests.

The condensed financial statements shall include

disclosures of material related party transactions, other than compensation arrangements, expense allowances, and other similar items

in the ordinary course of business. However, disclosure of transactions that are eliminated in the preparation of consolidated or combined

financial statements is not required in those statements. The disclosures shall include: a) the nature of the relationship(s) involved;

b) a description of the transactions, including transactions to which no amounts or nominal amounts were ascribed, for each of the periods

for which income statements are presented, and such other information deemed necessary to an understanding of the effects of the transactions

on the financial statements; c) the dollar amounts of transactions for each of the periods for which income statements are presented

and the effects of any change in the method of establishing the terms from that used in the preceding period; and d) amount due from

or to related parties as of the date of each balance sheet presented and, if not otherwise apparent, the terms and manner of settlement.

| |

l |

Commitments and contingencies |

The Company follows the ASC 450-20, Commitments

to report accounting for contingencies. Certain conditions may exist as of the date the financial statements are issued, which may result

in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company assesses such

contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal

proceedings that are pending against the Company or un-asserted claims that may result in such proceedings, the Company evaluates the

perceived merits of any legal proceedings or un-asserted claims as well as the perceived merits of the amount of relief sought or expected

to be sought therein.

If the assessment of a contingency indicates that

it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would

be accrued in the Company’s condensed financial statements. If the assessment indicates that a potentially material loss contingency

is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, and an

estimate of the range of possible losses, if determinable and material, would be disclosed.

Loss contingencies considered remote are generally

not disclosed unless they involve guarantees, in which case the guarantees would be disclosed. Management does not believe, based upon

information available at this time that these matters will have a material adverse effect on the Company’s financial position, results

of operations or cash flows. However, there is no assurance that such matters will not materially and adversely affect the Company’s

business, financial position, and results of operations or cash flows.

| |

l |

Recent accounting pronouncements |

From time to time, new accounting pronouncements

are issued by the Financial Accounting Standard Board (“FASB”) or other standard setting bodies and adopted by the Company

as of the specified effective date. Unless otherwise discussed, the Company believes that the impact of recently issued standards that

are not yet effective will not have a material impact on its financial position or results of operations upon adoption.

The Company has reviewed all recently issued,

but not yet effective, accounting pronouncements and does not believe the future adoption of any such pronouncements may be expected to

cause a material impact on its financial condition or the results of its operations.

Item 3. Quantitative and Qualitative Disclosures

About Market Risk

As a “smaller reporting company”,

we are not required to provide the information required by this Item.

Item 4. Controls and Procedures

Evaluation of Disclosure Controls and Procedures.

We maintain disclosure controls

and procedures that are designed to ensure that information required to be disclosed in our reports filed under the Securities Exchange

Act of 1934, as amended, is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange

Commission's rules and forms, and that such information is accumulated and communicated to our management, to allow for timely decisions

regarding required disclosure.

As of June 30, 2023, the end

of our fiscal quarter, we carried out an evaluation, under the supervision of our Chief Executive Officer and Chief Financial Officer,

of the effectiveness of the design and operation of our disclosure controls and procedures. Based on the foregoing, we concluded that

our disclosure controls and procedures were not effective as of the end of the period covered by this quarterly report. We do not

have a formal audit committee.

Changes in Internal Controls

There have been no changes

in our internal controls over financial reporting identified in connection with the evaluation required by paragraph (d) of Securities

Exchange Act Rule 13a-15 or Rule 15d-15 that occurred in the quarter ended June 30, 2023 that have materially affected, or are reasonably

likely to materially affect, our internal control over financial reporting.

PART II - OTHER INFORMATION

Item 1. Legal Proceedings

From time to time, we may become involved in litigation

relating to claims arising out of its operations in the normal course of business. We are not involved in any pending legal proceeding

or litigation and, to the best of our knowledge, no governmental authority is contemplating any proceeding to which we area party or to