As filed with the Securities and Exchange Commission

on December 4, 2024.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GLOBAL

MOFY AI LIMITED

(Exact name of registrant as specified in its charter)

| Cayman Islands |

|

7370 |

|

Not Applicable |

(State or other jurisdiction of

incorporation or organization) |

|

(Primary Standard Industrial

Classification Code Number) |

|

(I.R.S. Employer

Identification Number) |

No. 102, 1st Floor, No. A12, Xidian

Memory Cultural and Creative Town

Gaobeidian Township, Chaoyang District, Beijing

People’s Republic of China, 100000

+86-10-64376636

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

+1 (800) 221-0102

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a Copy to:

William S. Rosenstadt, Esq.

Mengyi “Jason” Ye, Esq.

Yarona L. Yieh, Esq.

Ortoli Rosenstadt LLP

366 Madison Avenue, 3rd Floor

New York, NY 10017

212-588-0022

Approximate date of commencement of proposed

sale to the public: Promptly after the effective date of this registration statement.

If any of the securities being registered on this

Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the

following box. ☒

If this Form is filed to register additional securities

for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act

registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement

number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933

Emerging growth company ☒

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards** provided pursuant to Section 7(a)(2)(B) of the

Securities Act. ☐

| ** | The term “new or revised financial accounting standard”

refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5,

2012. |

The registrant hereby amends this registration

statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which

specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the

Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the U.S. Securities

and Exchange Commission, acting pursuant to such Section 8(a), may determine.

The information in this

preliminary prospectus is not complete and may be changed. We may not sell the securities until the registration statement filed with

the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and we are

not soliciting any offer to buy these securities in any jurisdiction where such offer or sale is not permitted.

| SUBJECT TO COMPLETION |

|

PRELIMINARY PROSPECTUS DATED DECEMBER 4, 2024 |

GLOBAL MOFY AI LIMITED

Up to 20,135,320 Class A Ordinary Shares

(Including up to 19,801,985 Class A Ordinary

Shares Issuable Upon Exercise of Warrants)

This prospectus is related to the resale, from time to time, by the selling

shareholders identified in this prospectus (the “Selling Shareholders”), of up to an aggregate of 20,135,320 Class A Ordinary

Shares, par value $0.00003 per share (the “Class A Ordinary Shares”), of GLOBAL MOFY AI LIMITED (“GMM”, the “Company”,

“we”, “our”, “us”), which include 333,335 Class A Ordinary Shares and 19,801,985 Class A Ordinary

Shares issuable upon the exercise of warrants (the “Warrants”) that were issued in a private placement completed on October

31, 2024 (the “Private Placement”) pursuant to certain securities purchase agreement dated October 13, 2024, as amended on

October 31, 2024, by and between the Company and the Selling Shareholders (the “Securities Purchase Agreement”), as further

described below under “Prospectus Summary – Our Corporate History and Structure – The 2024 Private Placement”

on page 7 of this prospectus.

This prospectus also covers any additional ordinary

shares that may become issuable upon any adjustment pursuant to the terms of the Warrants issued to the Selling Shareholders by reason

of share splits, share dividends, share combinations, recapitalizations and other events described therein.

The Selling Shareholders are identified in the

table commencing on page 64 of this prospectus. No Class A Ordinary Shares are being registered hereunder for sale by us. We will

not receive any proceeds from the sale of the Class A Ordinary Shares by the selling shareholder. All net proceeds from the sale of the

Class A Ordinary Shares covered by this prospectus will go to the selling shareholder. See “Use of Proceeds.” Information

regarding the selling shareholder, the amounts of Class A Ordinary Shares that may be sold by it, and the times and manner in which it

may offer and sell the Class A Ordinary Shares under this prospectus is provided under the sections titled “Selling Shareholder”

and “Plan of Distribution,” respectively, in this prospectus. We do not know when or in what amount the selling shareholder

may offer the Class A Ordinary Shares for sale. The selling shareholder may sell any, all, or none of the Class A Ordinary Shares offered

by this prospectus.

Our authorized share capital is a dual class structure

consisting of Class A Ordinary Shares and class B ordinary shares of a par value of US$0.00003 each (“Class B Ordinary Shares”).

Holders of Class A Ordinary Shares and Class B Ordinary Shares shall vote together as one class on all resolutions of the shareholders

and have the same rights except each Class A Ordinary Share shall entitle its holder to one (1) vote and each Class B Ordinary

Share shall entitle its holder to twenty (20) votes. The Class B Ordinary Shares would not be convertible into Class A Ordinary

Shares or any other equity securities authorized to be issued by the Company.

Our Class A Ordinary Shares are currently traded on

the Nasdaq Capital Market, or Nasdaq, under the symbol “GMM.” On December 2, 2024, the last reported sale price of our Class

A Ordinary Shares on Nasdaq was $4.60.

We received a written notification from the Nasdaq Stock Market LLC (the

“Nasdaq”) on September 25, 2024, notifying us that we are not in compliance with the minimum bid price requirement set forth

in the Nasdaq rules for continued listing on the Nasdaq (the “Minimum Bid Price Requirement”). To regain compliance, our Class

A Ordinary Shares must have a closing bid price of at least US$1.00 for a minimum of 10 consecutive trading days by March 24, 2025. In

the event the Company does not regain compliance by March 24, 2025, we are eligible for an additional 180 calendar day period to regain

compliance with the Minimum Bid Price Requirement. On November 1, 2024, the Company convened its special meeting of shareholders, during

which the shareholders of the Company adopted resolutions approving an increase of the Company’s share capital and a share consolidation

(the “Reverse Share Split”) in a ratio of one (1)-for-fifteen (15) of the Company’s issued and outstanding Class A Ordinary

Shares and class B ordinary shares (the “Class B Ordinary Shares”), as well as the number of authorized Class A Ordinary Shares

and Class B Ordinary Shares. As a result, as of the date of this prospectus, there are 2,811,569 Class A Ordinary Shares and 848,203 Class

B Ordinary Shares issued and outstanding and the Company’s authorized share capital is US$1,020,000 and is divided into: (a) 30,000,000,000

Class A Ordinary Shares of par value of US$0.00003 each, and (b) 4,000,000,000 Class B Ordinary Shares of par value of US$0.00003 each.

The Reverse Share Split was implemented to regain compliance with the Minimum Bid Price Requirement. Our Class A ordinary shares began

trading on an adjusted basis, reflecting the Reverse Share Split, on November 26, 2024, under the existing ticker symbol “GMM.”

Unless specified otherwise, and except as provided in the financial statements and footnotes thereto, all references in this prospectus

to share and per share data have been adjusted, including historical data which has been retroactively adjusted, to give effect to the

Reverse Share Split. For more information, see “Risk Factors- Risks related to our Class A Ordinary Shares – The market price

of our Class A Ordinary Shares has recently declined significantly, and our Class A Ordinary Shares could be delisted from the Nasdaq

or trading could be suspended.” on page 51 of this prospectus.

Investors are cautioned that you are not

buying shares of a China-based operating company but instead are buying shares of a Cayman Islands holding company with operations conducted

by our subsidiaries based in China and that this structure involves unique risks to investors.

This prospectus is related to the Class A

Ordinary Shares of the Cayman Islands holding company. We conduct our business through the PRC subsidiaries. You will not and may never

have direct ownership in the operating subsidiaries based in China. After the restructure that dissolved the Variable Interest Entity

(“VIE”) structure, GLOBAL MOFY AI LIMITED now controls and receives the economic benefits of the PRC subsidiaries’

business operation, if any, through equity ownership. We do not use a VIE structure.

Unless otherwise stated, as used in this prospectus, the terms “Global

Mofy Cayman,” “we,” “us,” “our Company,” and the “Company” refer to GLOBAL MOFY

AI LIMITED, an exempted company with limited liability incorporated under the laws of the Cayman Islands; the term the “operating

subsidiaries” refers to the following entities organized under the laws of the PRC: Zhejiang Mofy Metaverse Technology Co., Ltd.,

or Global Mofy Zhejiang WFOE, Global Mofy (Beijing) Technology Co., Ltd., or Global Mofy China, Kashi Mofy Interactive Digital Technology

Co., Ltd., or Kashi Mofy, and Shanghai Mo Ying Fei Huan Technology Co., Ltd., or Shanghai Mofy.

Global Mofy Cayman is a Cayman Islands holding company and is not a Chinese

operating company. As a holding company with no material operations of its own, it conducts all of its operations and operates its business

in China through its PRC subsidiaries, in particular, Global Mofy China and its subsidiaries, Beijing Mofy, Kashi Mofy, Shanghai Mofy,

and Xi’an Mofy. Because of our corporate structure as a Cayman Islands holding company with operations conducted by our PRC subsidiaries,

it involves unique risks to investors. Furthermore, Chinese regulatory authorities could change the rules and regulations regarding foreign

ownership in the industry in which the Company operates, which would likely result in a material change in our operations and/or a material

change in the value of the securities we are registering for sale, including that it could cause the value of such securities to significantly

decline or become worthless. Investors in our Class A Ordinary Shares should be aware that they do not directly hold equity interests

in the Chinese operating subsidiaries, but rather are purchasing equity solely in Global Mofy Cayman, our Cayman Islands holding company,

which indirectly owns 100% equity interests in the PRC subsidiaries. Our Class A Ordinary Shares offered in this offering are shares of

our Cayman Islands holding company instead of shares of our subsidiaries in China. See “Risk Factors — Risks Related

to Doing Business in China — The filing, approval or other administration requirements of the Chinese Securities Regulatory

Commission (the “CSRC”) or other PRC government authorities may be required in connection with our future offshore offering

under PRC law, and, if required, we cannot predict whether or for how long we will be able to complete the filing procedure with the CSRC

and obtain such approval or complete such filing, as applicable.” on page 24.

Investing in our Class A Ordinary Shares involves

a high degree of risk. Before buying any Class A Ordinary Shares, you should carefully read the discussion of material risks of investing

in our Class A Ordinary Shares in “Risk Factors” beginning on page 22 of this prospectus and in the documents incorporated

by reference into this prospectus to read about factors you should consider before buying our Class A Ordinary Shares.

In particular, as substantially all of our operations

are conducted through the PRC subsidiaries, we are subject to certain legal and operational risks associated with our operations in China,

including that changes in the legal, political and economic policies of the Chinese government, the relations between China and the United States,

or Chinese or United States regulations may materially and adversely affect our business, financial condition and results of operations.

PRC laws and regulations governing our current business operations are sometimes vague and uncertain, and therefore, these risks could

result in a material change in our operations and/or the value of our Class A Ordinary Shares or could significantly limit or completely

hinder our ability to offer or continue to offer securities to investors and cause the value of our Class A Ordinary Shares to significantly

decline or be worthless. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations

in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over

China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity

reviews, and expanding the efforts in anti-monopoly enforcement.

It is the opinion of our PRC counsel, Jingtian &

Gongcheng, that we will not be subject to cybersecurity review with the Cyberspace Administration of China, or the “CAC,”

after the Cybersecurity Review Measures became effective on February 15, 2022, since we currently do not have over one million users’

personal information and do not anticipate that we will be collecting over one million users’ personal information in the foreseeable

future, which we understand might otherwise subject us to the Cybersecurity Review Measures; we are also not subject to network data security

review by the CAC if the Draft Regulations on the Network Data Security Administration are enacted as proposed, since we currently do

not have over one million users’ personal information and do not collect data that affects or may affect national security and we

do not anticipate that we will be collecting over one million users’ personal information or data that affects or may affect national

security in the foreseeable future, which we understand might otherwise subject us to the Security Administration Draft. See “Risk

Factors — Risks Related to Doing Business in China — The filing, approval or other administration requirements

of the Chinese Securities Regulatory Commission (the “CSRC”) or other PRC government authorities may be required in connection

with our future offshore offering under PRC law, and, if required, we cannot predict whether or for how long we will be able to complete

the filing procedure with the CSRC and obtain such approval or complete such filing, as applicable” on page 24.

On February 17, 2023, the China Securities

Regulatory Commission, or the CSRC, announced the Circular on the Administrative Arrangements for Filing of Securities Offering and Listing

by Domestic Companies, or the Circular, and released a set of new regulations which consists of the Trial Administrative Measures of Overseas

Securities Offering and Listing by Domestic Companies, or the Trial Measures, and five supporting guidelines. On the same date, the CSRC

also released the Notice on the Arrangements for the Filing Management of Overseas Listing of Domestic Companies, or the Notice. The Trial

Measures came into effect on March 31, 2023. The Trial Measures refine the regulatory system by subjecting both direct and indirect

overseas offering and listing activities to the CSRC filing-based administration. Requirements for filing entities, time points and procedures

are specified. A PRC domestic company that seeks to offer and list securities in overseas markets shall fulfill the filing procedure with

the CSRC per the requirements of the Trial Measures. Where a PRC domestic company seeks to indirectly offer and list securities in overseas

markets, the issuer shall designate a major domestic operating entity, which shall, as the domestic responsible entity, file with the

CSRC. The Trial Measures also lay out requirements for the reporting of material events.

According to the Trial Measures and the Circular,

we were subject to and have completed the filing requirements of the CSRC in connection with our initial public offering completed in

October 2023.

In addition, an overseas-listed company must also submit the filing with

respect to its follow-on offerings, issuance of convertible corporate bonds and exchangeable bonds, and other equivalent offering activities,

within the time frame specified by the Trial Measures. As a result, we were required to file with the CSRC within three business

days after the filing of the registration statement of which this prospectus forms a part with the SEC.

Breaches of the Trial Measures, such as offering

and listing securities overseas without fulfilling the filing procedures, shall bear legal liabilities, including a fine between RMB 1.0 million

(approximately $150,000) and RMB 10.0 million (approximately $1.5 million), and the Trial Measures heighten the cost for offenders

by enforcing accountability with administrative penalties and incorporating the compliance status of relevant market participants into

the Securities Market Integrity Archives. In addition, if we do not maintain the permissions and approvals of the filing procedure in

a timely manner under PRC laws and regulations, we may be subject to investigations by competent regulators, fines or penalties, ordered

to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering,

and these risks could result in a material adverse change in our operations, limit our ability to offer or continue to offer securities

to investors, or cause such securities to significantly decline in value or become worthless. As the Circular and Trial Measures were

newly published, there exists uncertainty with respect to the filing requirements and their implementation. Any failure or perceived failure

of us to fully comply with such new regulatory requirements could significantly limit or completely hinder our ability to offer or continue

to offer securities to investors, cause significant disruption to our business operations, and severely damage our reputation, which could

materially and adversely affect our financial condition and results of operations and could cause the value of our securities to significantly

decline or be worthless. See “Risk Factors — Risks Related to Doing Business in China — The filing,

approval or other administration requirements of the Chinese Securities Regulatory Commission (the “CSRC”) or other PRC government

authorities may be required in connection with our future offshore offering under PRC law, and, if required, we cannot predict whether

or for how long we will be able to complete the filing procedure with the CSRC and obtain such approval or complete such filing, as applicable”

on page 24.

It is the opinion of our PRC counsel, Jingtian &

Gongcheng, that as of the date of this prospectus, although we are required to complete the filing procedure in connection with our offering

(including this offering and any subsequent offering) under the Trial Measures, no relevant PRC laws or regulations in effect require

that we obtain permission from any PRC authorities to issue securities to foreign investors, and we have not received any inquiry, notice,

warning, sanction, or any regulatory objection to this offering from the CSRC, the CAC, or any other PRC authorities that have jurisdiction

over our operations.

The Standing Committee of the National People’s

Congress, or the SCNPC, or other PRC regulatory authorities may in the future promulgate laws, regulations or implementing rules that

requires our company or any of our subsidiaries to obtain regulatory approval from Chinese authorities before listing in the U.S. In

other words, although the Company has not received any denial to list on the U.S. exchange, our operations could be adversely affected,

directly or indirectly; our ability to offer, or continue to offer, securities to investors would be potentially hindered and the value

of our securities might significantly decline or be worthless, by existing or future laws and regulations relating to its business or

industry or by intervene or interruption by PRC governmental authorities, if we or our subsidiaries (i) do not receive or maintain

such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, (iii) applicable

laws, regulations, or interpretations change and we are required to obtain such permissions or approvals in the future, or (iv) any

intervention or interruption by PRC governmental with little advance notice. See “Risk Factors — Risks

Related to Doing Business in China” beginning on page 23 and “— Risks Related to Our Class A Ordinary Shares,” beginning

on page 51 of this prospectus for a discussion of these legal and operational risks and information that should be considered before

making a decision to purchase our Class A Ordinary Shares.

In addition, since 2021, the Chinese government

has strengthened its anti-monopoly supervision, mainly in three aspects: (1) establishing the National Anti-Monopoly Bureau; (2) revising

and promulgating anti-monopoly laws and regulations, including: the Anti-Monopoly Law (draft Amendment published on October 23, 2021

for public opinions), the anti-monopoly guidelines for various industries, and the detailed Rules for the Implementation of the Fair Competition

Review System; and (3) expanding the anti-monopoly law enforcement targeting Internet companies and large enterprises. As of the

date of this prospectus, the Chinese government’s recent statements and regulatory actions related to anti-monopoly concerns have

not impacted our ability to conduct business, accept foreign investments, or list on a U.S. or other foreign exchange because neither

the Company nor its PRC subsidiaries engage in monopolistic behaviors that are subject to these statements or regulatory actions.

Pursuant to the Holding Foreign Companies Accountable

Act, or the HFCAA, if the Public Company Accounting Oversight Board, or the PCAOB, is unable to inspect an issuer’s auditors for

three consecutive years, the issuer’s securities are prohibited to trade on a U.S. stock exchange. The PCAOB issued a

Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public

accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one

or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because

of a position taken by one or more authorities in Hong Kong. Furthermore, the PCAOB’s report identified the specific registered

public accounting firms which are subject to these determinations. On June 22, 2021, the U.S. Senate passed the Accelerating

Holding Foreign Companies Accountable Act, and on December 29, 2022, legislation entitled “Consolidated Appropriations Act,

2023” (the “Consolidated Appropriations Act”) was signed into law by President Biden, which contained, among other things,

an identical provision to the Accelerating Holding Foreign Companies Accountable Act and amended the HFCAA by requiring the SEC to prohibit

an issuer’s securities from trading on any U.S stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years

instead of three, thus reducing the time period for triggering the prohibition on trading. On August 26, 2022, the PCAOB announced

that it had signed a Statement of Protocol (the “SOP”) with the China Securities Regulatory Commission and the Ministry of

Finance of China. The SOP, together with two protocol agreements governing inspections and investigations (together, the “SOP Agreement”),

establishes a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based

in mainland China and Hong Kong, as required under U.S. law. On December 15, 2022, the PCAOB announced that it was able

to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong

completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely

registered public accounting firms headquartered in mainland China and Hong Kong. However, whether the PCAOB will continue to be

able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong

is subject to uncertainties and depends on a number of factors out of our and our auditor’s control. The PCAOB continues to demand

complete access in mainland China and Hong Kong moving forward and is making plans to resume regular inspections in early 2023 and

beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has also indicated

that it will act immediately to consider the need to issue new determinations with the HFCAA if needed.

As of the date of the prospectus, YCM CPA INC., our current auditor, is

not subject to the determinations as to inability to inspect or investigate completely as announced by the PCAOB on December 16,

2021. The Company’s auditor is based in the U.S. and is registered with PCAOB and subject to PCAOB inspection. As of the date

of the prospectus, Marcum Asia CPAs LLP, the independent registered public account firm that issued the audit report for the fiscal years

ended September 30, 2023 and 2022 included elsewhere in this prospectus,, is not subject to the determinations as to inability to inspect

or investigate completely as announced by the PCAOB on December 16, 2021. The Company’s auditor is based in the U.S. and

is registered with PCAOB and subject to PCAOB inspection. See “Risk Factors — Risks Related to Doing Business in

China — The recent joint statement by the SEC and PCAOB, proposed rule changes submitted by Nasdaq, and the Holding Foreign

Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing

the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB.” on page 40.

Our management monitors the cash position of each

entity within our organization regularly and prepare budgets on a monthly basis to ensure each entity has the necessary funds to fulfill

its obligation for the foreseeable future and to ensure adequate liquidity. In the event that there is a need for cash or a potential

liquidity issue, it will be reported to our Chief Financial Officer and subject to approval by our board of directors, we will enter into

an intercompany loan for the subsidiary in accordance with the applicable PRC laws and regulations. However, the funds or assets may not

be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions

and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets. See “Risk Factors — Risks

Related to Doing Business in China — To the extent cash or assets in the business is in the PRC or Hong Kong or a

PRC or Hong Kong entity, the funds or assets may not be available to fund operations or for other use outside of the PRC or Hong Kong

due to interventions in or the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government

to transfer cash or assets.”

Under existing PRC foreign exchange regulations,

payment of current account items, such as profit distributions and trade and service-related foreign exchange transactions, can be made

in foreign currencies without prior approval from the State Administration of Foreign Exchange, or the SAFE, by complying with certain

procedural requirements. Therefore, our PRC subsidiaries are able to pay dividends in foreign currencies to us without prior approval

from SAFE, subject to the condition that the remittance of such dividends outside of the PRC complies with certain procedures under PRC

foreign exchange regulations, such as the overseas investment registrations by our shareholders or the ultimate shareholders of our corporate

shareholders who are PRC residents. Approval from, or registration with, appropriate government authorities is, however, required where

the RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated

in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account

transactions. Current PRC regulations permit our PRC subsidiaries to pay dividends to the Company only out of their accumulated profits,

if any, determined in accordance with Chinese accounting standards and regulations. As of the date of this prospectus, there are no restrictions

or limitations imposed by the Hong Kong government on the transfer of capital within, into and out of Hong Kong (including funds

from Hong Kong to the PRC), except for transfer of funds involving money laundering and criminal activities. Cayman Islands law prescribes

that a company may only pay dividends out of its profits or share premium, and that a company may only pay dividends if, immediately following

the date on which the dividend is paid, the company remains able to pay its debts as they fall due in the ordinary course of business.

Other than that, there is no restrictions on Global Mofy Cayman’s ability to pay dividends to its shareholders. See “Prospectus

Summary — Transfers of Cash to and from Our Subsidiaries,” “Prospectus Summary — Summary of

Risk Factors,” and “Risk Factors — Risks Related to Doing Business in China — To the extent

cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may not be available

to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions and

limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets,” “Risk Factors — Risks

Related to Doing Business in China — We are a holding company and we rely on our subsidiaries for funding dividend payments,

which are subject to restrictions under PRC laws,” and “Risk Factors — Risks Related to Doing Business in

China — Our PRC subsidiaries are subject to restrictions on paying dividends or making other payments to us, which may

have a material adverse effect on our ability to conduct our business.”

As a holding company, we may rely on dividends and

other distributions on equity paid by our subsidiaries, including those based in the PRC, for our cash and financing requirements. If

any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability

to pay dividends to us. Global Mofy Cayman is permitted under the laws of the Cayman Islands to provide funding to our subsidiaries incorporated

in Hong Kong through loans or capital contributions without restrictions on the amount of the funds. Our subsidiaries are permitted

under the respective laws of Hong Kong to provide funding to Global Mofy Cayman through dividend distribution without restrictions

on the amount of the funds. There are no restrictions on dividend transfers from Hong Kong to the Cayman Islands. Current PRC regulations

permit Mofy Metaverse (Beijing) Technology Co., Ltd. (“Global Mofy WFOE” or “WFOE”) to pay dividends to the Company

only out of its accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. The transfer

of funds among companies are subject to the Provisions of the Supreme People’s Court on Several Issues Concerning the Application

of Law in the Trial of Private Lending Cases (2020 Revision, the “Provisions on Private Lending Cases”), which was implemented

on August 20, 2020 to regulate the financing activities between natural persons, legal persons and unincorporated organizations.

It is the opinion of our PRC counsel, Jingtian & Gongcheng, that the Provisions on Private Lending Cases does not prohibit using cash

generated from one subsidiary to fund another subsidiary’s operations. We have not been notified of any other restriction which

could limit our PRC subsidiaries’ ability to transfer cash between PRC subsidiaries. As of the date of this prospectus, neither

the Company nor its subsidiaries have made transfers, dividends, or distributions to investors and no investors have made transfers, dividends,

or distributions to the Company or its subsidiaries. As of the date of this prospectus, no dividends, distributions or transfers have

been made between Global Mofy Cayman and any of its subsidiaries. We do not expect to pay any cash dividends in the foreseeable future.

Also, as of the date of this prospectus, no cash generated from one subsidiary is used to fund another subsidiary’s operations and

we do not anticipate any difficulties or limitations on our ability to transfer cash between subsidiaries. See “Prospectus Summary — Transfers

of Cash to and from Our Subsidiaries,” on page 13.

We are an “emerging growth company”

as defined under federal securities laws and, as such, will be subject to reduced public company reporting requirements. See “Prospectus

Summary — Implications of Being an Emerging Growth Company” and “Implications of Being a Foreign Private Issuer”

on page 19 for additional information.

Neither the Securities and Exchange Commission

nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus.

Any representation to the contrary is a criminal offense.

Prospectus dated ________, 2024.

TABLE OF CONTENTS

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form F-1 that

we filed with the U.S. Securities and Exchange Commission (the “SEC”). As permitted by the rules and regulations of the SEC,

the registration statement filed by us includes additional information not contained in this prospectus. You may read the registration

statement and the other reports we file with the SEC at the SEC’s website described below under the heading “Where You Can

Find Additional Information.”

You should rely only on the information that is

contained in this prospectus or that is incorporated by reference into this prospectus. We have not authorized anyone to provide you with

information that is in addition to or different from what is contained in, or incorporated by reference into, this prospectus. If anyone

provides you with different or inconsistent information, you should not rely on it.

This prospectus contains summaries of certain

provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information.

All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have

been filed, will be filed or will be incorporated herein by reference as exhibits to the registration statement, and you may obtain copies

of those documents as described below under the section entitled “Where You Can Find Additional Information.”

We have not authorized anyone to provide any information

or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by us or on

our behalf or to which we have referred you and which we have filed with the U.S. Securities and Exchange Commission (the “SEC”).

We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you.

This prospectus is an offer to sell only the Class A Ordinary Shares offered hereby, but only under circumstances and in jurisdictions

where it is lawful to do so. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted

or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer

or sale. For the avoidance of doubt, no offer or invitation to subscribe for our Class A Ordinary Shares is made to the public in the

Cayman Islands. The information contained in this prospectus is current only as of the date on the front cover of the prospectus. Our

business, financial condition, results of operations and prospects may have changed since that date.

Commonly Used Defined Terms

Unless otherwise indicated or the context requires

otherwise, references in this prospectus to:

| |

● |

“Beijing Mofy” refers to Mofy (Beijing) Film Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is 60% owned by Global Mofy China; |

| |

|

|

| |

● |

“Century Mofy” refers to Anji Century Mofy Education Consulting Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy Zhejiang WFOE; |

| |

|

|

| |

● |

“Class A Ordinary Shares” refers to the Class A Ordinary Shares of the Company, par value US$0.00003 per share; |

| |

|

|

| |

● |

“Class B Ordinary Shares” refers to the Class A Ordinary Shares of the Company, par value US$0.00003 per share; |

| |

|

|

| |

● |

“Gauss Intelligence” refers to Gauss Intelligence (Beijing) Technology Co.. Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy Zhejiang WFOE; |

| |

|

|

| |

● |

“Global Mofy Cayman” refers to GLOBAL MOFY AI LIMITED, an exempted company incorporated under the laws of the Cayman Islands; |

| |

● |

“Global Mofy HK” refers to Global Mofy HK Limited, a limited liability company organized under the laws of Hong Kong, which is wholly-owned by Global Mofy Cayman; |

| |

|

|

| |

● |

“Global Mofy California” refers to Global Mofy (Beijing) Technology Co., Ltd., a limited liability company organized under the laws of the State of California, which is wholly-owned by Global Mofy China; |

| |

|

|

| |

● |

“Global Mofy WFOE” refers to Mofy Metaverse (Beijing) Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy HK; |

| |

|

|

| |

● |

“Global Mofy Zhejiang WFOE” refers to Zhejiang Mofy Metaverse Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy HK; |

| |

|

|

| |

● |

“Global Mofy China” refers to Global Mofy (Beijing) Technology Co., Ltd., a limited liability company organized under the laws of PRC, which is wholly-owned by Global Mofy WFOE; |

| |

|

|

| |

● |

“GMM Discovery” refers to GMM Discovery LLC, a limited liability company organized under the laws of the State of Delaware, which is wholly-owned by Global Mofy Cayman; |

| |

|

|

| |

● |

“Kashi Mofy” refers to Kashi Mofy Interactive Digital Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy China; |

| |

|

|

| |

● |

“Kuyu Intelligent” refers to Kuyu Intelligent Technology (Anji) Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy Zhejiang WFOE; |

| |

|

|

| |

● |

“RMB” refers to the legal currency of China; |

| |

|

|

| |

● |

“Securities Act” refers to the Securities Act of 1933, as amended; |

| |

|

|

| |

● |

“Shanghai Mofy” Shanghai Mo Ying Fei Huan Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is wholly-owned by Global Mofy China; |

| |

|

|

| |

● |

“U.S. dollars,” “$,” “US$,” and “dollars” refer to the legal currency of the United States; |

| |

|

|

| |

● |

“we,” “us,” “our Company,” “the Company,” “our,” “Global Mofy Cayman” refer to GLOBAL MOFY AI LIMITED; |

| |

|

|

| |

● |

“Xi’an Mofy” refers to Xi’an Digital Cloud Technology Co., Ltd., a limited liability company organized under the laws of the PRC, which is 60% owned by Global Mofy China. |

Global Mofy China and its subsidiaries conduct

business in the PRC, using Renminbi, or RMB, the official currency of China. Our consolidated financial statements are presented in United States

dollars. In this prospectus, we refer to assets, obligations, commitments and liabilities in our consolidated financial statements in

United States dollars. These dollar references are based on the exchange rate of RMB to United States dollars, determined as

of a specific date or for a specific period. Changes in the exchange rate will affect the amount of our obligations and the value of our

assets in terms of United States dollars which may result in an increase or decrease in the amount of our obligations (expressed

in dollars) and the value of our assets, including accounts receivable (expressed in dollars).

We have relied on statistics provided by a variety

of publicly-available sources regarding China’s expectations of growth. We did not directly or indirectly sponsor or participate

in the publication of such materials, and these materials are not incorporated in this prospectus other than to the extent specifically

cited in this prospectus. We have sought to provide current information in this prospectus and believe that the statistics provided in

this prospectus remain up-to-date and reliable, and these materials are not incorporated in this prospectus other than to the extent specifically

cited in this prospectus.

PROSPECTUS SUMMARY

This summary highlights selected information

that is presented in greater detail elsewhere, or incorporated by reference, in this prospectus. It does not contain all of the information

that may be important to you and your investment decision. Before investing in the securities that the Selling Shareholders are offering,

you should carefully read this entire prospectus, including the matters set forth under the section of this prospectus captioned “Risk

Factors,” “Special Note Regarding Forward-Looking Statements” and the financial statements and related notes and other

information that we incorporate by reference herein, including, but not limited to, our annual report on Form 20-F for the fiscal year

ended September 30, 2023 (the “2023 Annual Report”) and other SEC reports.

Overview

We are an AI-Driven technology solutions provider

engaged in virtual content production, and digital assets development for the digital content industry. Utilizing our proprietary “Mofy

Lab” technology platform which consists of cutting-edge three-dimensional (“3D”) rebuilt technology and artificial intelligence

(“AI”) interactive technology, we are able to create 3D high definition virtual version of a wide range of physical world

objects such as human, animal and scenes which can be used in different applications. According to the industry datasheet generated by

Frost & Sullivan, we are one of the leading digital asset banks in China. As of the date of this report, our digital asset bank

has more than 100,000 high precision 3D digital assets. High precision means 4K (4096*2160) resolution of movie precision. With our strong

technology platform and industry track record, we attract high-profile customers such as L’Oreal and Pepsi and earn repeat business.

Additionally, we have developed the Gausspeed platform, an innovative generative AI solution NIVIDIA Omniverse and NVIDIA RTX GPUs to

further enhance our capabilities in creating high-quality digital content. We primarily operate in two lines of business (i) virtual

technology service and (ii) digital asset development and others. We had another business line of digital marketing during the

fiscal years ended September 30, 2022 and 2021. However, we did not have revenue from this line of business in the six months ended March

31, 2024 and the fiscal year ended September 30, 2023 and we plan to cease this line of business in the future.

Virtual Technology Service

We provide comprehensive technology solution to

assist customers in virtual content production, which can be used in a variety of settings such as movies, television series, animations,

advertising and gaming, etc. Leveraging our proprietary “Mofy Lab” technology platform and developing AI technologies, we

produce high-quality virtual content quickly and cost-effectively to meet highly differentiated customers’ needs. The virtual content

production contracts are primarily on a fixed price basis, payable on a milestone basis, which require us to perform services for visual

effect design, content development, production and integration based on customers’ specific needs.

Digital Asset Development

Through our virtual content production business

and opportunistic acquisition of certain digital assets, we have built a robust digital asset bank with more than 100,000 3D digital assets.

We grant specific use right of these digital assets to customers who use them based on their specific needs across different applications

such as movies, TV series, AR/VR, animation, advertising and gaming. Additionally, leveraging our robust digital asset bank, we have started

further in-depth development of AI-based 3D model and video generative tool to further enhance our operation efficiency and profitability.

Our digital assets, which build up our digital asset bank, mainly consist of high precision 3D renders of scenes, characters, objects

and, items that can be licensed for use in virtual environment.

Depending on customers’ needs, these digital

assets can be quickly deployed and integrated with minimal customization, thus reducing project costs and expediate completion time. With

the rapid development of digital content industry, we believe digital assets will become increasingly valuable and have abundant use cases.

We plan to continue to actively expand our digital asset bank and develop more digital asset products that we believe have more uses to

serve this rapidly growing market.

Global Mofy China has its own technology platform,

called “Mofy Lab”. Mofy Lab contains self-developed and optimized technologies, including 3D rebuilt technology and AI interactive

technology, which can: (i) create 3D high-definition virtual version of real world objects, or the digital assets; and (ii) provide

a one-stop, low barrier, low-cost solution to assist digital content industry companies in creating high quality virtual contents.

For the six months ended March 31, 2024,

our revenues were $20.0 million, of which approximately 45% and 55% were generated from our two lines of business, virtual technology

service and digital assets development and others, respectively. For the six months ended March 31, 2023, our revenues were $12.8 million

of which approximately 62% and 38% were generated from our two lines of business, virtual technology service and digital assets development

and others, respectively.

We position ourselves as a comprehensive technology

solutions provider that act as a building block for the development of the digital content industry. Our goal is to become a leading digital

asset provider to empower companies in the digital content value chain with high quality and cost-effective solutions and products. Our

experienced management team has utilized the opportunities from this emerging market to achieve the long-term development and growth of

Global Mofy China through our growth strategies.

Competitive Advantages

We are committed to provide our customers with

quality technology service and to become the largest 3D digital asset provider in China. We believe that we have a number of competitive

advantages that will enable us to maintain and further improve our market position in the industry. Our competitive advantages include:

| |

● |

We own proprietary “Mofy Lab” technology platform. Our technology platform consists of 3D rebuilt technology and AI interactive technology which enable us to precisely convert almost all physical world objects into high definition 3D digital assets. With this technology platform, we are able to create high-quality virtual contents and digital assets quickly and cost-effectively to meet highly differentiated needs of our customers. |

| |

● |

We are an established player in the metaverse industry. We are one of the early entrants in the metaverse industry in China. Through our virtual content production business and opportunistic acquisition of certain digital assets, we are able to build a robust digital asset bank with more than 100,000 3D digital assets. These digital assets can be quickly deployed and integrated by our customers with minimal customization, thus reducing project costs and expedite completion time. |

| |

● |

Our staff and management are experienced and diversified in operations and managements. Our key team members have more than 10 years of experience in their respective fields. The founder, Haogang Yang, is a seasoned entrepreneur with extensive experience in business management and operation. He realized the value of digital assets in the field of virtual contents as early as in early 2019 and firmly led Global Mofy China to reserve digital assets, which has brought Global Mofy China to occupy the dominant position. In addition, Global Mofy China features with a diverse senior management team. Ms. Wenjun Jiang, the Chief Technology Officer of the Company, has more than 15 years’ experience in virtual technology. Global Mofy China’s principal operation is intelligence intensive. Since inception, Global Mofy China has pooled a large number of managerial talents in the industry forming a professional and stable operation and management team. |

Our Growth Strategy

We position ourselves as a comprehensive technology

solutions provider that act as a building block for the development of the metaverse industry. Our goal is to become a leading digital

asset provider to empower companies in the metaverse value chain with high quality and cost-effective solutions and products. We plan

to implement the following growth strategies to achieve our goal:

| |

● |

We will continue to focus on the research and development of our technologies. Global Mofy China has been focusing on research and development since its inception and there were approximately 17 employees engaging in research and development as of the date of this prospectus. Global Mofy China is a national certified high-tech enterprise by both the Beijing Municipal Science & Technology Commission and the Administrative Commission of Zhongguancun Science Park for its cutting-edge 3D rebuilt and AI interactive technologies. As our company continues to grow in size and the rapid development of technologies in the metaverse industry, Global Mofy China is placing an increasing emphasis on research and development. In addition to continuously optimizing our technology, we, through our PRC subsidiaries, will accelerate the development of digital assets, with the expectation to convert at least 10,000 assets a year to expand our competitive advantage. |

| |

● |

We aim to maintain and further develop business relationships with our customers and potential players in the metaverse industry. We have developed years of relationships with both upstream and downstream entities of the industry. Our founding team has built solid connections with Tencent, Alibaba, and other first-line leading metaverse platforms in China. We have also developed business relationships with Youku, Perfect World, Wimi Hologram, and other content companies across many varied segments of the industry. |

| |

● |

We plan to cooperate with or acquire similar digital assets providers to expand our digital assets content in order to implement our business strategy. Besides Global Mofy China, there are currently handful independent high-definition 3D digital asset providers worldwide. However, they achieve merely average performance due to outdated operating concepts. Within 12 to 24 months of listing on Nasdaq, Global Mofy China plans to develop strategic partnership, or to eventually acquire similar digital assets providers to further expand our digital assets reserve. |

Our Corporate History and Structure

GLOBAL MOFY AI LIMITED, or Global Mofy Cayman,

is a holding company incorporated in the Cayman Islands. As a holding company with no material operations, Global Mofy Cayman conducts

its operations in China through Global Mofy China and its PRC subsidiaries. After the restructure that dissolved the VIE structure, Global

Mofy Cayman now controls and receives the economic benefits of the PRC subsidiaries’ business operation, if any, through equity

ownership. We do not use a VIE structure.

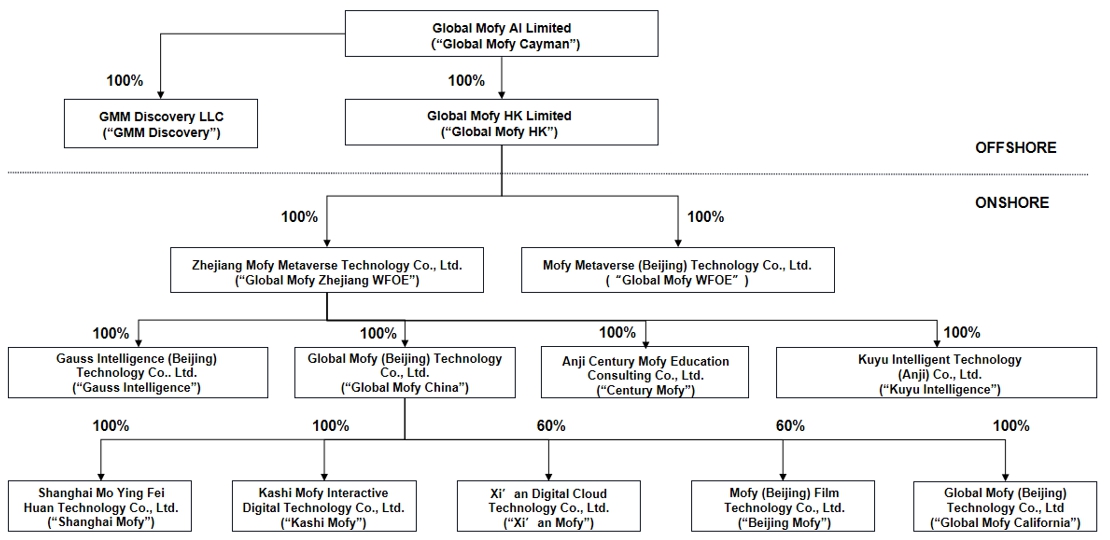

The following diagram illustrates our corporate

structure as of the date of this prospectus. For more detail on our corporate history, please refer to “Business — Corporate

History and Structure” beginning on page 3 of this prospectus.

Global Mofy Cayman is a Cayman Islands exempted

company incorporated on September 29, 2021. As a holding company with no significant assets or operation, it conducts business in

China through Global Mofy China and its subsidiaries.

GMM Discovery was incorporated on May 22, 2024, under the laws of the State

of Delaware. GMM Discovery is a wholly owned subsidiary of Global Mofy Cayman and is currently not engaging in any active business.

Global Mofy HK was incorporated on October 21,

2021, under the laws of Hong Kong SAR. Global Mofy HK is the wholly-owned subsidiary of Global Mofy Cayman and is currently

not engaging in any active business and merely acting as a holding company.

Global Mofy WFOE was incorporated on December 9, 2021, under the laws

of the People’s Republic of China. It is a wholly-owned subsidiary of Global Mofy HK and a wholly foreign-owned entity under the

PRC laws. It is currently not engaging in any active business.

Global Mofy Zhejiang WFOE was incorporated on April 3,

2023, under the laws of the People’s Republic of China. It is a wholly-owned subsidiary of Global Mofy HK and a wholly foreign-owned

entity under the PRC laws. It is one of the operating subsidiaries and is engaged in technology development, technical services, and software

development.

Gauss Intelligence was incorporated on February 28,

2024, under the laws of the PRC. Gauss Intelligence is a wholly owned subsidiary of Global Mofy Zhejiang WFOE. It is currently not

engaging in any active business.

Global Mofy China was incorporated on November 22,

2017, under the laws of the People’s Republic of China. It is one of the operating subsidiaries and is engaged in technology development,

technical services, design and produce advertisement, and film screening.

Century Mofy was incorporated on March 5, 2024, under

the laws of the PRC. Century Mofy is a wholly owned subsidiary of Global Mofy Zhejiang WFOE. It is currently not engaging in any active

business.

Kuyu Intelligent was incorporated on September 3,

2024, under the laws of the PRC. Kuyu Intelligent is a wholly owned subsidiary of Global Mofy Zhejiang WFOE. It is currently not engaging

in any active business.

Shanghai Mofy was incorporated on May 11, 2020,

under the laws of the PRC. Shanghai Mofy is a wholly owned subsidiary of Global Mofy China. It is one of the operating subsidiaries.

Kashi Mofy was incorporated on July 31, 2019,

under the laws of the PRC. Kashi Mofy is a wholly owned subsidiary of Global Mofy China. It is one of the operating subsidiaries.

Xi’an Mofy was incorporated on June 8,

2018, under the laws of the PRC. Xi’an Mofy is a majority owned subsidiary of Global Mofy China. It is currently not engaging

in any active business.

Beijing Mofy was incorporated on February 7,

2018, under the laws of the PRC. Beijing Mofy is a majority owned subsidiary of Global Mofy China. It is currently not engaging in

any active business.

Global Mofy California was incorporated on December 14, 2023, under the

laws of the State of California. Global Mofy California is a wholly owned subsidiary of Global Mofy China. It is currently not engaging

in any active business.

The Restructure

On January 5, 2022, Global Mofy WFOE entered

into a series of VIE agreements (the “VIE Agreements”) with Global Mofy China and all the shareholders of Global Mofy China,

which established the VIE structure. As a result of the VIE Agreements, Global Mofy WFOE was regarded as the primary beneficiary of Global

Mofy China, and we treated Global Mofy China and its subsidiaries as the variable interest entities under U.S. GAAP for accounting

purposes. We have consolidated the financial results of Global Mofy China and its subsidiaries in our consolidated financial statements

in accordance with the U.S. GAAP.

On June 28, 2022, Global Mofy WFOE entered

into equity transfer agreements with each shareholder of Global Mofy China to purchase all the equity interest in Global Mofy China. On

July 8, 2022, Global Mofy WFOE, Global Mofy China and shareholders of Global Mofy China signed a termination agreement of the VIE

Agreements. The VIE structure was dissolved. The restructure was completed on July 8, 2022. As a result, Global Mofy China became

a wholly owned subsidiary of Global Mofy WFOE. Global Mofy China was a foreign-invested joint venture at the time of the acquisition

of its 100% equity interests by Global Mofy WFOE.

With respect to the application of the M&A

Rules, we acquired the domestic operating entities through a “two-step slow-walk” method, so the approval process of the Ministry

of Commerce is not applicable. The acquisition was broken into two steps: 1) adding a non-PRC shareholder so that the domestic operating

entity will be categorized as a Sino-foreign joint venture (an entity with mixed capital between one or more foreign and Chinese shareholders);

2) Global Mofy WFOE to complete the equity acquisition of Global Mofy China from both the Chinese and foreign shareholders so that it

would become a foreign-owned enterprise. Our PRC counsel, Jingtian & Gongcheng, has completed substantial amount of research and study

of the regulation and precedents and found that this approach has been widely used in the past. In addition, it has never been penalized

or challenged with respect to the legality of this matter. While our PRC counsel, Jingtian & Gongcheng, believes that it is permitted

to structure the acquisition in this manner and the acquisition, in fact, has been completed without any challenge by any regulator, there

is uncertainty with respect to the interpretation of the current regulation as it is still evolving. In the event that this approach is

deemed invalid or illegal and it is applied retroactively, Global Mofy WFOE’s acquisition of Global Mofy China could be deemed invalid

and we will not be able to consolidate the financial statements of Global Mofy China. We have added a risk factor to disclose such risk

on page 42 under “Risk Factors — Risks Related to Doing Business in China — We circumvent

the application of M&A rules by taking a “two-step slow-walk” method. In the event that this approach is deemed invalid

or illegal and it is applied retroactively, Global Mofy WFOE’s acquisition of Global Mofy China could be deemed invalid and we will

not be able to consolidate the financial statements of Global Mofy China.”

Global Mofy China previously planned to provide

radio and television program production and film projection services and obtained a related business license in order to do so. According

to the Foreign Investment Law and the Special Administrative Measures for Access of Foreign Investment (Negative List), foreign investment

ratio in entities for the provision of such radio and television program production and film projection services shall not exceed 50%

and consequently it was agreed that the VIE agreements be entered so that Global Mofy China would not run afoul of such laws. However,

those services were not operated by Global Mofy China and the reason to use the VIE structure was no longer relevant. Global Mofy China

excluded the radio and television program production and film projection services as its business scope in June 2022 and the related

business license was canceled in June 2022. Global Mofy China is then able to be held by Global Mofy WFOE directly. Currently, the

Chinese securities laws does not differentiate a VIE structure and an equity holding structure when it comes to overseas listing. However,

we concern about the risk of future changes in the Chinese securities laws that may disallow the VIE structure, and decided that it would

be in the best interest of our shareholders to dissolve the VIE structure and assume a direct parent-subsidiary holding structure between

Global Mofy WFOE and Global Mofy China.

One of our beneficial owners, Zhenquan Ren, who

is a PRC resident, has not and will not completed the Circular 37 Registration. Mr. Ren owns 970,701 shares, through Mofy Yi Limited,

a BVI company, which is 3.74% of the Company’s issued and outstanding shares. We will ask our prospective shareholders who are Chinese

residents to make the necessary applications and filings as required by Circular 37. However, not each of our shareholders, who are PRC

residents will, in the future, complete the registration process as required by Circular 37. Failure to comply with the registration procedures

set forth in SAFE Circular 37 and the subsequent notice, or making misrepresentation on or failure to disclose controllers of the foreign-invested

enterprise that is established through round-trip investment, may result in restrictions being imposed on the foreign exchange activities

of the relevant foreign-invested enterprise, including restrictions on its ability to receive registered capital as well as additional

capital from PRC resident shareholders who fail to complete Circular 37 registration; and repatriation of profits and dividends derived

from special purpose vehicles to China, by the PRC resident shareholders who fail to complete Circular 37 registration, are also illegal.

In addition, the failure of the PRC resident shareholders to complete Circular 37 registration may subject each of the shareholders to

fines less than RMB50,000. Please see “Risk Factors — Risks Related to Doing Business in China — One

of our shareholders has not and will not completed the Circular 37 Registration. The Chinese resident shareholders’ failure to comply

with Circular 37 registration may result in restrictions being imposed on part of foreign exchange activities of the offshore special

purpose vehicles, including restrictions on its ability to receive registered capital as well as additional capital from Chinese resident

shareholders who fail to complete Circular 37 registration” on page 35 of this prospectus.

The Forward Share Split and Share Surrender

On September 16, 2022, we amended our Memorandum

and Articles of Association and effected a 1-to-5 share split (“Forward Share Split”) of our ordinary shares. We had 5,130,631

ordinary shares issued and outstanding immediately prior to the Forward Share Split. After the Forward Share Split, there were 25,653,155

ordinary shares issued and outstanding. All shareholders then subsequently surrendered in an aggregative of 1,653,155 ordinary shares

on a pro-rata basis, which were cancelled by the Company.

On November 15, 2022, all existing shareholders

surrendered in an aggregative of 381,963 ordinary shares on a pro-rata basis, which were cancelled by the Company. On the same date, the

Company, together with Mr. Haogang Yang, our founder and CEO, certain BVI founder entities and all its subsidiaries in Hong Kong

and mainland China, entered into a share purchase agreement with certain investor, pursuant to which the Company issued 381,963 ordinary

shares to such investor, for an aggregate issue price of USD1,500,000.

The Pre-IPO Investment

On February 10, 2023, the Company entered

into a share purchase agreement with three investors, pursuant to which we issued a total of 1,926,155 ordinary shares, par value US$0.000002,

of the Company to the investors for an aggregate issue price of $9.4 million (RMB65,000,000). As of March 31, 2023, we have

received the $9.4 million from these investors.

The IPO

On October 12, 2023, the Company completed its initial

public offering of 1,200,000 ordinary shares at a price of $5.00 per share. On November 6, 2023, the underwriter for the initial public

offering exercised its over-allotment option in part to purchase 40,000 ordinary shares at a price of $5.00. The total gross proceeds

received from the initial public offering, including proceeds from the exercise of the over-allotment option, was US$6.2 million.

The 2023 Registered Offering

On January 3, 2024 , the Company issued a total of

1,379,313 ordinary shares and warrants for the purchase of up to 2,068,970 ordinary shares at an exercise price of $8.00 per share pursuant

to certain securities purchase agreements dated December 29, 2023 with certain institutional investors. The purchase price per one share

and accompany warrant is $7.25. The Company received gross proceeds in the amount of $10 million.

On March 1, 2024, the Company entered into warrant exchange agreements

with each of the investors, pursuant to which the Investors conveyed, assigned, transferred, and surrendered the initial warrants in exchange

for new warrants. The initial warrants were automatically deemed cancelled by the Company upon the time of issuance of the new warrants.

The new warrants have the same terms and conditions as the initial warrants except that the new warrants allow each Investor to, after

6 months from the original issuance date of the Initial Warrants, alternatively exchange all or any portion of the new warrants into such

aggregate number of ordinary shares equal to the product of (x) 0.4 and (y) such aggregate number of ordinary shares underlying such portion

of the new warrants to be exercised (the “Alternative Cashless Exercise”). The exchange of the initial warrants for the new

warrants was made in reliance upon the exemption from registration provided by Section 3(a)(9) of the Securities Act of 1933, as amended.

On July 5 and July 10, 2024, the Company issued

a total of 827,589 ordinary shares upon delivery of notices from the investors exercising the new warrants in full through Alternative

Cashless Exercise. As a result, all of the new warrants have been retired.

The Dual Class Structure

On August 15, 2024, the Company convened its annual

general meeting of shareholders, during which the shareholders of the Company adopted resolutions approving all of the proposals considered

at the meeting. As a result, (i) all of the issued and outstanding ordinary shares of US$0.000002 par value each in the capital of the

Company were designated into class A Ordinary Shares of US$0.000002 par value each, each having one (1) vote per share and the other rights

attached to it as set out in the Second Amended and Restated Memorandum and Articles of Association on a one for one basis, (ii) 3,000,000,000

authorized but unissued Ordinary Shares were designated into 3,000,000,000 Class B Ordinary Shares of US$0.000002 par value each, each

having 20 votes per share and the other rights attached to it as set out in the Second Amended and Restated Memorandum and Articles of

Association on a one for one basis; and (iii) the remaining authorized but unissued ordinary shares were designated into Class A Ordinary

Shares on a one for one basis. Concurrently, the shareholders approved for the Company to repurchase 10,913,894 and 1,809,142 Class A

Ordinary Shares registered in the names of James Yang Mofy Limited and New JOLENE&R L.P., respectively, at an amount equal to the

aggregate par value of US$26 (the “Repurchase Price”) and the Repurchase Price out of the proceeds from a fresh issue of 10,913,894

and 1,809,142 Class B Ordinary Shares to James Yang Mofy Limited and New JOLENE&R L.P., respectively. Mr. Haogang Yang, the Chief

Executive Officer and Chairman of the Company, is the sole shareholder and director of James Yang Mofy Limited and holds 75% interest

and has voting and dispositive control of New JOLENE&R L.P.

The 2024 Equity Incentive Plans

On August 21, 2024 and on October 7, 2024, the Board of Directors of the

Company approved and adopted two equity incentive plans, which collectively authorized 7,800,000 Class A Ordinary Shares to be issued

to the directors, officers, managers, employees, consultants and advisors (and prospective directors, officers, managers, employees, consultants

and advisors) of the Company and its affiliates. In September 2024 and October 2024, the Company issued a total of 7,800,000 Class A Ordinary

Shares to several consultants of the Company.

The 2024 Private Placement

On October 31, 2024, the Company sold and issued (i) 5,000,000 Class A

Ordinary Shares, (ii) Warrants to purchase up to 10,000,000 Class A Ordinary Shares at an initial exercise price of $3.00 per Class A

Ordinary Share, subject to adjustment, pursuant to the Securities Purchase Agreement dated October 13, 2024, as amended on October 31,

2024 by and between the Company and the Selling Shareholders. The purchase price of each Class A Ordinary Share and two Warrants

is $0.50. The Company received gross proceeds in the amount of $2,500,000 (assuming the Warrants are not exercised). The Company

intends to use the proceeds to provide financing for its generative AI platform, general research and development, administrative expenses,

talent acquisition, and working capital needs.

The Warrants

Pursuant to the Securities Purchase Agreement,

as amended pursuant to the Amendment Agreement dated October 31, 2024, by and among the Company and the Purchasers, on the fourteenth

(14th) calendar days after the closing of the Private Placement, the exercise price of the Warrants shall be reset to 20% of

Nasdaq Minimum Price of the Company’s Class A Ordinary Share determined on the date of the Securities Purchase Agreement (the “Reset”).

In addition, upon the Reset of the exercise price, the number of Class A Ordinary Share underlying the Warrants (the “Warrant Shares”)

issuable immediately prior to such Reset shall be adjusted to the number of Class A Ordinary Share determined by multiplying the initial

exercise price by the number of Warrant Shares acquirable upon exercise of the Warrants immediately prior to such Reset and dividing the

product thereof by the exercise price resulting from such Reset.

The exercise price of the Warrants is subject

to further adjustment including share dividends, share splits, share combination, subsequent rights offering, pro rata distributions,

and certain fundamental transaction. If at any time on or after the issuance of the Warrants, there occurs any share split, reverse share

split, share dividend, share combination recapitalization or other similar transaction involving the Class A ordinary shares (each, a

“Share Combination Event”, and such date on which the Share Combination Event is effected, the “Share Combination Event

Date”) and the lowest weighted average price of the Class A ordinary shares during the period commencing on the trading day

immediately following the applicable Share Combination Event Date and ending on the fifth (5th) trading day immediately following the

applicable Share Combination Event Date (such period the “Share Combination Adjustment Period” and such price the “Event

Market Price”), is less than the exercise price then in effect (after giving effect to the adjustment of the share splits share

combination by multiplying a fraction of which the numerator shall be the number of Class A ordinary shares outstanding immediately before

such event and of which the denominator shall be the number of Class A ordinary shares outstanding immediately after such event), then,

at the close of trading on the last day of the Share Combination Adjustment Period, the exercise price then in effect on such 5th trading

day shall be reduced (but in no event increased) to the Event Market Price and the number of Warrant Shares issuable upon exercise of

the Warrants shall be increased such that the aggregate exercise price payable, after taking into account the decrease in the exercise

price, shall be equal to the aggregate exercise price for the Warrant Shares prior to such adjustment.

As a result of the Reset and after giving effect to

the effectiveness of the Reverse Share Split discussed in the section “The Reverse Share Split” below, the exercise price

of the Warrants was adjusted to $1.515 per share and the number of Warrant Shares was adjusted to 19,801,985.

The Warrants are exercisable upon issuance and

will expire five years from their initial date of exercise. The Warrants are exercisable for cash; provided, however that they may be

exercised on a cashless exercise if, at the time of exercise, there is no effective registration statement registering, or no current

prospectus available for the resale of the Warrant Shares. In addition, if at any time after the three months’ anniversary of the

date of issuance, the holder of the Warrant may alternatively exchange all, or any part, of the Warrants into such aggregate number of

Class A ordinary shares equal to the product of (x) 0.8 and (y) such aggregate number of Class A ordinary shares underlying such portion

of the Warrants to be exercised.

Registration Rights

The Company has also entered into a Registration