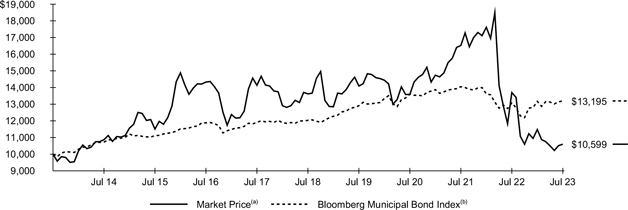

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-21053

| Name of Fund: |

|

BlackRock Virginia Municipal Bond Trust (BHV) |

| Fund Address: |

|

100 Bellevue Parkway, Wilmington, DE 19809 |

Name and address of agent for

service: John M. Perlowski, Chief Executive Officer, BlackRock Virginia

Municipal Bond Trust, 50 Hudson Yards, New York, NY 10001

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 07/31/2023

Date of reporting period: 07/31/2023

Item 1 – Report to Stockholders

(a) The Report to Shareholders is attached herewith.

|

|

|

|

|

|

JULY 31, 2023 |

BlackRock MuniHoldings New York

Quality Fund, Inc. (MHN)

BlackRock Virginia Municipal Bond Trust (BHV)

|

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

The Markets in Review

Dear Shareholder,

Despite an uncertain economic

landscape during the 12-month reporting period ended July 31, 2023, the resilience of the U.S. economy in the face of ever tighter financial conditions provided an encouraging backdrop for investors.

While inflation was near multi-decade highs at the beginning of the period, it declined precipitously as commodity prices dropped. Labor shortages also moderated, although wages continued to grow and unemployment rates reached the lowest levels in

decades. This robust labor market powered further growth in consumer spending, backstopping the economy.

Equity returns were solid, as the durability

of consumer sentiment eased investors’ concerns about the economy’s trajectory. The U.S. economy resumed growth in the third quarter of 2022 and continued to expand thereafter. Most major classes of equities advanced, including large- and

small-capitalization U.S. stocks and equities from developed and emerging markets.

The 10-year U.S. Treasury

yield rose during the reporting period, driving its price down, as investors reacted to elevated inflation and attempted to anticipate future interest rate changes. The corporate bond market also faced inflationary headwinds, although high-yield

corporate bond prices fared significantly better than investment-grade bonds as demand from yield-seeking investors remained strong.

The U.S. Federal

Reserve (the “Fed”), acknowledging that inflation has been more persistent than expected, raised interest rates seven times during the 12-month period ended July 31, 2023. Furthermore, the Fed

wound down its bond-buying programs and incrementally reduced its balance sheet by not replacing securities that reach maturity. However, the Fed declined to raise interest rates at its June 2023 meeting, the first time it paused its tightening in

the current cycle, before again raising rates in July 2023.

Supply constraints appear to have become an embedded feature of the new macroeconomic

environment, making it difficult for developed economies to increase production without sparking higher inflation. Geopolitical fragmentation and an aging population risk further exacerbating these constraints, keeping the labor market tight and

wage growth high. Although the Fed has decelerated the pace of interest rate hikes and recently opted for a pause, we believe that the new economic regime means that the Fed will need to maintain high rates for an extended period to keep inflation

under control. Furthermore, ongoing structural changes may mean that the Fed will be hesitant to cut interest rates in the event of faltering economic activity lest inflation accelerate again. We believe investors should expect a period of higher

volatility as markets adjust to the new economic reality and policymakers attempt to adapt.

While we favor an overweight position to developed market

equities in the long term, we prefer an underweight stance in the near-term. Expectations for corporate earnings remain elevated, which seems inconsistent with macroeconomic constraints. Nevertheless, we are overweight on emerging market stocks in

the near-term as growth trends for emerging markets appear brighter. We also believe that stocks with an A.I. tilt should benefit from an investment cycle that is set to support revenues and margins. We are neutral on credit overall amid tightening

credit and financial conditions; however, there are selective opportunities in the near term. For fixed income investing with a six- to twelve-month horizon, we see the most attractive investments in

short-term U.S. Treasuries, U.S. inflation-linked bonds, U.S. mortgage-backed securities, and hard-currency emerging market bonds.

Overall, our view

is that investors need to think globally, position themselves to be prepared for a decarbonizing economy, and be nimble as market conditions change. We encourage you to talk with your financial advisor and visit blackrock.com for further

insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

|

|

|

|

|

| Total Returns as of July 31, 2023 |

| |

|

6-Month

|

|

12-Month

|

| U.S. large cap

equities

(S&P 500® Index) |

|

13.52% |

|

13.02% |

| U.S. small cap

equities

(Russell 2000® Index) |

|

4.51 |

|

7.91 |

| International

equities

(MSCI Europe, Australasia,

Far East Index) |

|

6.65 |

|

16.79 |

| Emerging market

equities

(MSCI Emerging Markets Index) |

|

3.26 |

|

8.35 |

| 3-month Treasury bills

(ICE BofA 3-Month

U.S. Treasury Bill Index) |

|

2.34 |

|

3.96 |

| U.S. Treasury

securities

(ICE BofA 10-Year

U.S. Treasury Index) |

|

(2.08) |

|

(7.56) |

| U.S. investment

grade bonds

(Bloomberg U.S. Aggregate Bond Index) |

|

(1.02) |

|

(3.37) |

| Tax-exempt municipal bonds

(Bloomberg Municipal Bond Index) |

|

0.20 |

|

0.93 |

| U.S. high yield

bonds

(Bloomberg U.S. Corporate

High Yield 2%

Issuer Capped Index) |

|

2.92 |

|

4.42 |

|

| Past performance is not an indication of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. |

|

|

|

| 2 |

|

T H I S P A G E

I S N O T P A R T O F Y O U

R F U N D R E P O R T |

Table of Contents

|

|

|

| Municipal Market Overview For the Reporting Period Ended July 31, 2023 |

|

|

Municipal Market Conditions

Municipal bonds posted positive total returns amid heightened volatility. Interest rates rose rapidly early in the period as the Fed continued its

historic hiking cycle but became increasingly rangebound later in the reporting period as economic activity slowed, inflation expectations moderated, and the Fed tempered the magnitude and pace of its policy tightening. Strong credit fundamentals,

bolstered by robust post-pandemic revenue growth and elevated fund balances, drove strong positive excess returns versus comparable U.S. Treasuries. Lower-rated investment grade credits and the 15-year part of

the yield curve performed best.

|

|

|

|

|

| During the 12-month period ended July 31, 2023, municipal bond funds experienced net

outflows totaling $52 billion (based on data from the Investment Company Institute), transitioning from the largest outflow cycle on record in 2022 to mixed in 2023. At the same time, the market contended with just $324 billion in

issuance, well below the $422 billion issued during the prior 12-months. However, elevated bid-wanted activity filled some of the gap as investors raised cash to

meet redemptions, portfolio leverage was repositioned, and the Federal Deposit Insurance Corporation (“FDIC”) liquidated collapsed bank assets. |

|

|

|

Bloomberg Municipal Bond Index(a)

Total Returns as of July 31, 2023

6

months: 0.20% 12 months: 0.93% |

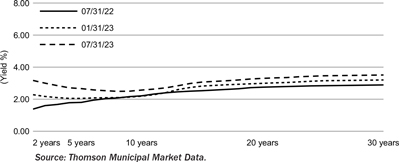

A Closer Look at Yields

|

|

|

| AAA Municipal Yield Curves

|

|

From July 31, 2022, to July 31, 2023, yields on AAA-rated 30-year municipal bonds increased by 62 basis points (“bps”) from 2.89% to 3.51%, ten-year yields increased by 36 bps from 2.21% to 2.57%, five-year yields increased

by 86 bps from 1.80% to 2.66%, and two-year yields increased by 140 bps from 1.60% to 3.00% (as measured by Refinitiv Municipal Market Data). As a result, the municipal yield curve flattened over the 12-month period with the spread between two- and 30-year maturities flattening by 78 bps to a slope of 51 bps. Still, the curve

remained relatively steep compared to the deeply inverted U.S. Treasury curve.

Outperformance throughout the period prompted historically rich valuations across the curve. Municipal-to-Treasury ratios tightened well through their 5-year averages led by short and intermediate maturities. |

Financial Conditions of Municipal Issuers

Buoyed by successive federal aid injections, vaccine distribution, and the re-opening of the economy, states and

many local governments experienced revenue growth above forecasts in 2021 and 2022. However, revenue collections through April 2023, particularly personal income tax receipts, have softened or declined in many states, such as California and New

York. A slowing economy could cause more widespread declines in overall revenue collections. While the inflation rate has slowed, higher wages and interest rates in the post-Covid recovery will pressure state and local government costs.

Nevertheless, overall credit fundamentals remain solid, particularly near-record reserve levels. Other sectors also exhibit strong credit fundamentals. Municipal utilities typically benefit from autonomous rate-setting that allows them to adjust for

rising fuel costs. Rising commodity prices over a prolonged period could test affordability and the political will to raise rates to balance operations. State housing authority bonds, flagship universities, and strong national and regional health

systems may also be pressured but are better poised to absorb the impact of the economic shock. Critical providers (safety net hospitals, mass transit systems, airports) with limited resources may still experience fiscal strain from the economic

fallout from high inflation, but aid and demand in the service sector of the economy will continue to support operating results through 2023. Work-from-home policies remain headwinds for mass transit farebox revenue and commercial real estate

values.

The opinions expressed are those of BlackRock as of July 31, 2023 and are subject to change at any time due to changes in market or

economic conditions. The comments should not be construed as a recommendation of any individual holdings or market sectors. Investing involves risk including loss of principal. Bond values fluctuate in price so the value of your investment can go

down depending on market conditions. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not

be able to make principal and interest payments. There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may

be subject to Alternative Minimum Tax (“AMT”). Capital gains distributions, if any, are taxable.

| (a) |

|

The Bloomberg Municipal Bond Index, a broad, market value-weighted index, seeks to measure the performance of the U.S.

municipal bond market. All bonds in the index are exempt from U.S. federal income taxes or subject to the AMT. Past performance is not an indication of future results. Index performance is shown for illustrative purposes only. It is not possible to

invest directly in an index. |

|

|

|

| 4 |

|

2 0 2 3 B L A C

K R O C K A N N U A L R E P O R

T T O S H A R E H O L D E R

S |

|

|

|

| The Benefits and Risks of Leveraging |

|

|

The Trusts may utilize leverage to seek to

enhance the distribution rate on, and net asset value (“NAV”) of, their common shares (“Common Shares”). However, there is no guarantee that these objectives can be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is

normally lower than the income earned by a Trust on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of each Trust (including the assets obtained from leverage) are invested in

higher-yielding portfolio investments, each Trust’s shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage (after paying the leverage costs) is paid to shareholders in

the form of dividends, and the value of these portfolio holdings (less the leverage liability) is reflected in the per share NAV.

To illustrate these

concepts, assume a Trust’s Common Shares capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If

prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, a Trust’s financing costs on the $30 million of proceeds obtained from leverage are based on

the lower short-term interest rates. At the same time, the securities purchased by a Trust with the proceeds from leverage earn income based on longer-term interest rates. In this case, a Trust’s financing cost of leverage is significantly

lower than the income earned on a Trust’s longer-term investments acquired from such leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit Common Shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the

leverage. If interest and other costs of leverage exceed a Trust’s return on assets purchased with leverage proceeds, income to shareholders is lower than if a Trust had not used leverage. In such circumstance, the investment adviser may

nevertheless determine to maintain a Trust’s leverage if it deems such action to be appropriate. Furthermore, the value of the Trusts’ portfolio investments generally varies inversely with the direction of long-term interest rates,

although other factors can influence the value of portfolio investments. In contrast, the amount of each Trust’s obligations under its respective leverage arrangement generally does not fluctuate in relation to interest rates. As a result,

changes in interest rates can influence the Trusts’ NAVs positively or negatively. Changes in the future direction of interest rates are very difficult to predict accurately, and there is no assurance that a Trust’s intended leveraging

strategy will be successful.

The use of leverage also generally causes greater changes in each Trust’s NAV, market price and dividend rates than

comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of a Trust’s Common Shares than if the Trust were not leveraged. In addition, each Trust may be required to

sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Trust to incur losses.

The use of leverage may limit a Trust’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Trust incurs expenses in connection with the use of leverage, all of which are borne by Common

Shareholders and may reduce income to the Common Shares. Moreover, to the extent the calculation of each Trust’s investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the

Trusts’ investment adviser will be higher than if the Trusts did not use leverage.

To obtain leverage, each Trust has issued Variable Rate

Demand Preferred Shares (“VRDP Shares” or “Preferred Shares”) and/or leveraged its assets through the use of tender option bond trusts (“TOB Trusts”) as described in the Notes to Financial Statements.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), each Trust is permitted to borrow money (including through the use of TOB

Trusts) or issue debt securities up to 33 1/3% of its total managed assets or equity securities (e.g., Preferred Shares) up to 50% of its total managed assets. A Trust may voluntarily elect to limit its leverage to less than the maximum amount

permitted under the 1940 Act. In addition, a Trust may also be subject to certain asset coverage, leverage or portfolio composition requirements imposed by the Preferred Shares’ governing instruments or by agencies rating the Preferred Shares,

which may be more stringent than those imposed by the 1940 Act.

Derivative Financial Instruments

The Trusts may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market,

and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative

financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the

transaction or illiquidity of the instrument. Pursuant to Rule 18f-4 under the 1940 Act, among other things, the Trusts must either use derivative financial instruments with embedded leverage in a limited

manner or comply with an outer limit on fund leverage risk based on value-at-risk. The Trusts’ successful use of a derivative financial instrument depends on the

investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation a Trust can

realize on an investment and/or may result in lower distributions paid to shareholders. The Trusts’ investments in these instruments, if any, are discussed in detail in the Notes to Financial Statements.

|

|

|

| T H E B E N E F I

T S A N D R I S K S O F L E

V E R A G I N G / D E R I V A

T I V E F I N A N C I A L I N

S T R U M E N T S |

|

5 |

|

|

|

| Trust Summary as of July 31, 2023 |

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

Investment Objective

BlackRock MuniHoldings NewYork Quality

Fund, Inc.’s (MHN) (the “Trust”) investment objective is to provide shareholders with current income exempt from U.S. federal income tax and New York State and New York City personal income taxes. The Trust seeks to achieve its

investment objective by investing, under normal market conditions, at least 80% of its assets in investment grade (as rated or, if unrated, considered to be of comparable quality at the time of investment by the Trust’s investment adviser) New

York municipal obligations exempt from U.S. federal income taxes (except that the interest may be subject to the U.S. federal alternative minimum tax) and New York State and New York City personal income taxes (“New York Municipal Bonds”),

except at times when, in the judgment of its investment adviser, New York Municipal Bonds of sufficient quality and quantity are unavailable for investment by the Trust. At all times, except during temporary defensive periods, the Trust invests at

least 65% of its assets in New York Municipal Bonds. The Trust invests, under normal market conditions, at least 80% of its assets in municipal obligations with remaining maturities of one year or more. The Trust may invest up to 20% of its managed

assets in securities that are rated below investment grade, or are considered by BlackRock to be of comparable quality, at the time of purchase. The Trust may invest directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective will be achieved.

Trust Information

|

|

|

| |

|

| Symbol on New York Stock Exchange |

|

MHN |

|

|

| Initial Offering Date |

|

September 19, 1997 |

|

|

| Yield on Closing Market Price as of July 31, 2023 ($

10.44)(a) |

|

3.85% |

|

|

| Tax Equivalent Yield(b) |

|

7.97% |

|

|

| Current Monthly Distribution per Common Share(c)

|

|

$ 0.033500 |

|

|

| Current Annualized Distribution per Common Share(c)

|

|

$ 0.402000 |

|

|

| Leverage as of July 31, 2023(d) |

|

40% |

| |

(a) |

Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing

market price. Past performance is not an indication of future results. |

|

| |

(b) |

Tax equivalent yield assumes the maximum marginal U.S. federal and state tax rate of 51.7%, which includes the 3.8%

Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

|

| |

(c) |

The distribution rate is not constant and is subject to change. A portion of the distribution may be deemed a return of

capital or net realized gain. |

|

| |

(d) |

Represents VRDP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust,

including any assets attributable to VRDP Shares and TOB Trusts, minus the sum of its accrued liabilities. Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized

by the Trust, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments. |

|

Market Price and Net Asset Value Per Share Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

07/31/23 |

|

|

|

07/31/22 |

|

|

|

Change |

|

|

|

High |

|

|

|

Low |

|

|

|

|

|

|

|

| Closing Market Price |

|

$ |

10.44 |

|

|

$ |

11.23 |

|

|

|

(7.03 |

)% |

|

$ |

11.50 |

|

|

$ |

9.22 |

|

|

|

|

|

|

|

| Net Asset Value |

|

|

12.12 |

|

|

|

12.58 |

|

|

|

(3.66 |

) |

|

|

12.72 |

|

|

|

10.68 |

|

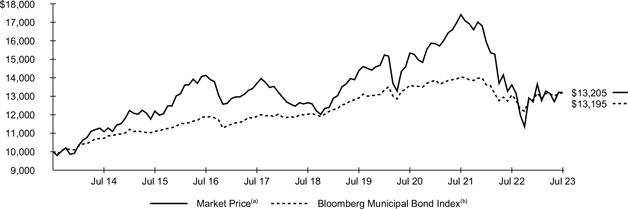

GROWTH OF $10,000 INVESTMENT

| |

(a) |

Represents the Trust’s closing market price on the NYSE and reflects the reinvestment of dividends and/or

distributions at actual reinvestment prices. |

|

| |

(b) |

An unmanaged index that tracks the U.S. long term tax-exempt bond market,

including state and local general obligation bonds, revenue bonds, pre-refunded bonds, and insured bonds. |

|

|

|

|

| 6 |

|

2 0 2 3 B L A C

K R O C K A N N U A L R E P O R

T T O S H A R E H O L D E R

S |

|

|

|

| Trust Summary as of July 31, 2023 (continued) |

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

Performance

Returns for the period ended July 31, 2023

were as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Average Annual Total Returns |

|

|

|

|

|

| |

|

1 Year |

|

|

5 Years |

|

|

10 Years |

|

| Trust at NAV(a)(b) |

|

|

0.53 |

% |

|

|

1.06 |

% |

|

|

3.84 |

% |

| Trust at Market

Price(a)(b) |

|

|

(3.00 |

) |

|

|

0.86 |

|

|

|

2.82 |

|

|

|

|

|

| New York Customized Reference Benchmark(c)

|

|

|

1.40 |

|

|

|

1.85 |

|

|

|

N/A |

|

|

|

|

|

| Bloomberg Municipal Bond Index |

|

|

0.93 |

|

|

|

1.87 |

|

|

|

2.81 |

|

| |

(a) |

All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results

reflect the Trust’s use of leverage, if any. |

|

| |

(b) |

The Trust’s discount to NAV widened during the period, which accounts for the difference between performance based

on market price and performance based on NAV. |

|

| |

(c) |

The New York Customized Reference Benchmark is comprised of the Bloomberg Municipal Bond: New York Exempt Total Return

Index Unhedged (90%) and the New York Bloomberg Municipal Bond: High Yield (non-Investment Grade) Total Return Index (10%). The New York Customized Reference Benchmark commenced on September 30, 2016.

|

|

Performance results may include adjustments made for financial reporting purposes in accordance with U.S.

generally accepted accounting principles. Past performance is not an indication of future results.

The Trust is presenting the performance of one or

more indices for informational purposes only. The Trust is actively managed and does not seek to track or replicate the performance of any index. The index performance shown is not intended to be indicative of the Trust’s investment strategies,

portfolio components or past or future performance.

More information about the Trust’s historical performance can be found in the “Closed

End Funds” section of blackrock.com.

The following discussion relates to the Trust’s absolute performance based on NAV:

Municipal bonds posted slightly positive returns in the annual period. Bond market performance, in general, was dampened by the combination of high

inflation and continued interest rate increases by the Fed. However, the contribution from income outweighed the impact of falling prices. New York municipals outperformed the national market.

Portfolio income was a large contributor to the Trust’s total return at a time of negative price performance. The Trust’s use of U.S. Treasury

futures to manage interest rate risk added value in the rising-rate environment, with most of the contribution occurring in the first half of the period. (Prices and yields move in opposite directions.) Positions in bonds with 15- to 25-year maturities contributed, as well.

With respect to credit

tiers, AA rated bonds were the largest contributor due to their sizable weighting in both the New York market and the Trust. BBB rated securities, which consisted mainly of holdings within the transportation and higher education sectors, also

performed well. The tax-backed sector was another positive contributor.

On the negative side, positions in low-coupon bonds—particularly in the housing sector—detracted. Holdings in bonds with maturities of 25 years and longer also detracted, as did the Trust’s allocation to high yield bonds.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or

other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

|

|

|

| T R U S T S U M M

A R Y |

|

7 |

|

|

|

| Trust Summary as of July 31, 2023 (continued) |

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN) |

Overview of the Trust’s Total Investments

|

|

|

|

|

| SECTOR ALLOCATION |

|

| |

|

| Sector(a)(b) |

|

Percentage of

Total Investments |

|

| Transportation |

|

|

33.3 |

% |

| County/City/Special District/School District |

|

|

19.2 |

|

| Utilities |

|

|

13.6 |

|

| State |

|

|

10.4 |

|

| Education |

|

|

9.1 |

|

| Housing |

|

|

5.4 |

|

| Health |

|

|

4.8 |

|

| Corporate |

|

|

2.4 |

|

| Tobacco |

|

|

1.8 |

|

|

|

|

|

|

| CALL/MATURITY SCHEDULE |

|

| |

|

| Calendar Year Ended December 31,(a)(c) |

|

Percentage |

|

| 2023 |

|

|

7.3 |

% |

| 2024 |

|

|

6.9 |

|

| 2025 |

|

|

11.7 |

|

| 2026 |

|

|

4.8 |

|

| 2027 |

|

|

12.2 |

|

|

|

|

|

|

| CREDIT QUALITY ALLOCATION |

|

| |

|

| Credit Rating(a)(d) |

|

Percentage of

Total Investments |

|

| AAA/Aaa |

|

|

9.4 |

% |

| AA/Aa |

|

|

56.1 |

|

| A |

|

|

20.4 |

|

| BBB/Baa |

|

|

7.0 |

|

| BB/Ba |

|

|

0.8 |

|

| B |

|

|

0.1 |

|

| N/R(e) |

|

|

6.2 |

|

| (a) |

Excludes short-term securities. |

| (b) |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may

combine such sector sub-classifications for reporting ease. |

| (c) |

Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years.

|

| (d) |

For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either

S&P Global Ratings or Moody’s Investors Service, Inc. if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of

BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are

subject to change. |

| (e) |

The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but

not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of

July 31, 2023, the market value of unrated securities deemed by the investment adviser to be investment grade represents 1.2% of the Trust’s total investments. |

|

|

|

| 8 |

|

2 0 2 3 B L A C

K R O C K A N N U A L R E P O R

T T O S H A R E H O L D E R

S |

|

|

|

| Trust Summary as of July 31, 2023 |

|

BlackRock Virginia Municipal Bond Trust (BHV) |

Investment Objective

BlackRock Virginia Municipal Bond

Trust’s (BHV) (the “Trust”) investment objective is to provide current income exempt from regular U.S. federal income tax and Virginia personal income taxes. The Trust seeks to achieve its investment objective by investing

primarily in municipal bonds exempt from U.S. federal income taxes (except that the interest may be subject to the U.S. federal alternative minimum tax) and Virginia personal income taxes. The Trust invests, under normal market conditions, at least

80% of its managed assets in municipal bonds that are investment grade quality at the time of investment or, if unrated, determined to be of comparable quality at the time of investment by the Trust’s investment adviser. The Trust may invest

directly in such securities or synthetically through the use of derivatives.

No assurance can be given that the Trust’s investment objective

will be achieved.

Trust Information

|

|

|

| Symbol on New York Stock Exchange |

|

BHV |

| Initial Offering Date |

|

April 30, 2002 |

| Yield on Closing Market Price as of July 31, 2023 ($

10.78)(a) |

|

2.95% |

| Tax Equivalent Yield(b) |

|

5.52% |

| Current Monthly Distribution per Common Share(c)

|

|

$ 0.026500 |

| Current Annualized Distribution per Common Share(c)

|

|

$ 0.318000 |

| Leverage as of July 31, 2023(d) |

|

40% |

| |

(a) |

Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing

market price. Past performance is not an indication of future results. |

|

| |

(b) |

Tax equivalent yield assumes the maximum marginal U.S. federal and state tax rate of 46.55%, which includes the 3.8%

Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

|

| |

(c) |

The distribution rate is not constant and is subject to change. A portion of the distribution may be deemed a return of

capital or net realized gain. |

|

| |

(d) |

Represents VRDP Shares and TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust,

including any assets attributable to VRDP Shares and TOB Trusts, minus the sum of its accrued liabilities. Does not reflect derivatives or other instruments that may give rise to economic leverage. For a discussion of leveraging techniques utilized

by the Trust, please see The Benefits and Risks of Leveraging and Derivative Financial Instruments. |

|

Market Price and Net Asset Value Per Share Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

07/31/23 |

|

|

|

07/31/22 |

|

|

|

Change |

|

|

|

High |

|

|

|

Low |

|

|

|

|

|

|

|

| Closing Market Price |

|

$ |

10.78 |

|

|

$ |

14.41 |

|

|

|

(25.19 |

)% |

|

$ |

15.00 |

|

|

$ |

10.44 |

|

|

|

|

|

|

|

| Net Asset Value |

|

|

12.44 |

|

|

|

13.32 |

|

|

|

(6.61 |

) |

|

|

13.46 |

|

|

|

11.18 |

|

GROWTH OF $10,000 INVESTMENT

| |

(a) |

Represents the Trust’s closing market price on the NYSE and reflects the reinvestment of dividends and/or

distributions at actual reinvestment prices. |

|

| |

(b) |

An unmanaged index that tracks the U.S. long term tax-exempt bond market,

including state and local general obligation bonds, revenue bonds, pre-refunded bonds, and insured bonds. |

|

|

|

|

| T R U S T S U M

M A R Y |

|

9 |

|

|

|

| Trust Summary as of July 31, 2023 (continued) |

|

BlackRock Virginia Municipal Bond Trust (BHV) |

Performance

Returns for the period ended July 31, 2023 were as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Average Annual Total Returns |

|

|

|

|

|

| |

|

1 Year |

|

|

5 Years |

|

|

10 Years |

|

| Trust at NAV(a)(b) |

|

|

(3.42 |

)% |

|

|

(0.19 |

)% |

|

|

2.77 |

% |

| Trust at Market

Price(a)(b) |

|

|

(22.64 |

) |

|

|

(4.89 |

) |

|

|

0.58 |

|

|

|

|

|

| Virginia Customized Reference Benchmark(c)

|

|

|

0.59 |

|

|

|

1.90 |

|

|

|

N/A |

|

|

|

|

|

| Bloomberg Municipal Bond Index |

|

|

0.93 |

|

|

|

1.87 |

|

|

|

2.81 |

|

| |

(a) |

All returns reflect reinvestment of dividends and/or distributions at actual reinvestment prices. Performance results

reflect the Trust’s use of leverage, if any. |

|

| |

(b) |

The Trust moved from a premium to NAV to a discount during the period, which accounts for the difference between

performance based on market price and performance based on NAV. |

|

| |

(c) |

The Virginia Customized Reference Benchmark is comprised of the Bloomberg Municipal Bond: Virginia Exempt Total Return

Index Unhedged (90%) and the Virginia Bloomberg Municipal Bond: High Yield (non-Investment Grade) Total Return Index (10%). The Virginia Customized Reference Benchmark commenced on September 30, 2016.

|

|

Performance results may include adjustments made for financial reporting purposes in accordance with U.S.

generally accepted accounting principles. Past performance is not an indication of future results.

The Trust is presenting the performance of one or

more indices for informational purposes only. The Trust is actively managed and does not seek to track or replicate the performance of any index. The index performance shown is not intended to be indicative of the Trust’s investment strategies,

portfolio components or past or future performance.

More information about the Trust’s historical performance can be found in the “Closed

End Funds” section of blackrock.com.

The following discussion relates to the Trust’s absolute performance based on NAV:

Municipal bonds posted slightly positive returns in the annual period. Bond market performance, in general, was dampened by the combination of high

inflation and continued interest rate increases by the Fed. However, the contribution from income outweighed the impact of falling prices.

The

Trust’s use of U.S. Treasury futures to manage interest rate risk added value in the rising-rate environment. At the sector level, tax backed states, transportation, and development districts made the largest contributions. Despite the

volatility throughout the period, low new issuance led to tighter yield spreads for higher-quality securities. Strong fundamental trends in the transportation sectors, especially airports, also helped fuel positive performance. Bonds with maturities

of 20 to 25 years were especially notable contributors in this area.

On the negative side, long-dated securities with maturities of 25 years and

above—particularly those with lower coupons—detracted from performance due to their higher interest rate sensitivity. Healthcare and transportation were the worst performing sectors, although this had more to do with the duration and

coupon characteristics of the debt rather than any specific credit issues or spread widening. The long duration securities were concentrated in the higher-quality credit tiers: AA, A, and BBB. The Trust’s use of leverage, which amplified the

effect of falling prices, was another detractor of note.

The Trust’s cash position was above typical levels at the close of the period, since

higher cash balances were required for the potential unwinding of leverage. Additionally, new issuance and secondary market opportunities were not accretive to portfolio income relative to cash yields, which have risen with the increase in

short-term rates. However, the Trust reduced cash incrementally late in the period to participate in new issuance.

The views expressed reflect the

opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

|

|

|

| 10 |

|

2 0 2 3 B L A C

K R O C K A N N U A L R E P O R

T T O S H A R E H O L D E R

S |

|

|

|

| Trust Summary as of July 31, 2023 (continued) |

|

BlackRock Virginia Municipal Bond Trust (BHV) |

Overview of the Trust’s Total Investments

|

|

|

|

|

| SECTOR ALLOCATION |

|

| |

|

| Sector(a)(b) |

|

Percentage of

Total Investments |

|

| County/City/Special District/School District |

|

|

19.9 |

% |

| State |

|

|

18.2 |

|

| Health |

|

|

17.7 |

|

| Transportation |

|

|

9.9 |

|

| Housing |

|

|

8.3 |

|

| Utilities |

|

|

7.9 |

|

| Tobacco |

|

|

7.9 |

|

| Education |

|

|

6.6 |

|

| Corporate |

|

|

3.6 |

|

|

| CALL/MATURITY SCHEDULE |

|

| |

|

| Calendar Year Ended December 31,(a)(c) |

|

Percentage |

|

| 2023 |

|

|

14.9 |

% |

| 2024 |

|

|

4.6 |

|

| 2025 |

|

|

2.3 |

|

| 2026 |

|

|

9.1 |

|

| 2027 |

|

|

13.5 |

|

|

|

|

|

|

| CREDIT QUALITY ALLOCATION |

|

| |

|

| Credit Rating(a)(d) |

|

Percentage of

Total Investments |

|

| AAA/Aaa |

|

|

15.4 |

% |

| AA/Aa |

|

|

46.6 |

|

| A |

|

|

10.1 |

|

| BBB/Baa |

|

|

1.7 |

|

| B |

|

|

4.8 |

|

| N/R(e) |

|

|

21.4 |

|

| (a) |

Excludes short-term securities. |

| (b) |

For Trust compliance purposes, the Trust’s sector classifications refer to one or more of the sector sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may

combine such sector sub-classifications for reporting ease. |

| (c) |

Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years.

|

| (d) |

For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either

S&P Global Ratings or Moody’s Investors Service, Inc. if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of

BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are

subject to change. |

| (e) |

The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but

not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of

July 31, 2023, the market value of unrated securities deemed by the investment adviser to be investment grade represents 5.4% of the Trust’s total investments. |

|

|

|

| T R U S T S U M M

A R Y |

|

11 |

|

|

|

| Schedule of Investments

July 31, 2023 |

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN)

(Percentages shown are based on Net Assets) |

|

|

|

|

|

|

|

|

|

| Security |

|

Par

(000) |

|

|

Value |

|

|

| Municipal Bonds |

|

|

| Alabama — 0.3% |

|

|

|

|

| Corporate — 0.3% |

|

|

|

|

|

|

| Lower Alabama Gas District, RB, Series A, 5.00%, 09/01/46 |

|

$ |

1,185 |

|

|

$ |

1,205,197 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Guam — 0.2% |

|

|

|

|

|

|

|

|

|

| Utilities — 0.2% |

|

|

|

|

|

|

| Guam Power Authority, Refunding RB, Series A, 5.00%, 10/01/41 |

|

|

580 |

|

|

|

601,229 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| New York — 153.9% |

|

|

|

|

|

|

|

|

|

| Corporate — 3.7% |

|

|

|

|

|

|

| New York Liberty Development Corp., RB, 5.50%, 10/01/37 |

|

|

830 |

|

|

|

953,823 |

|

| New York Liberty Development Corp., Refunding RB, 5.25%, 10/01/35 |

|

|

5,500 |

|

|

|

6,290,779 |

|

| New York State Energy Research & Development Authority, Refunding RB, Series C,

4.00%, 04/01/34 |

|

|

740 |

|

|

|

747,673 |

|

| New York State Environmental Facilities Corp., RB, AMT, 2.75%, 09/01/50(a) |

|

|

175 |

|

|

|

168,100 |

|

| New York Transportation Development Corp., RB |

|

|

|

|

|

|

|

|

| AMT, 5.00%, 10/01/35 |

|

|

1,565 |

|

|

|

1,638,616 |

|

| AMT, 5.00%, 10/01/40 |

|

|

2,400 |

|

|

|

2,447,904 |

|

| New York Transportation Development Corp., Refunding ARB, AMT, 3.00%, 08/01/31 |

|

|

1,465 |

|

|

|

1,290,035 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13,536,930 |

|

|

| County/City/Special District/School District — 30.7% |

|

| Battery Park City Authority, RB, Sustainability Bonds, 4.00%, 11/01/44 |

|

|

3,750 |

|

|

|

3,772,657 |

|

| City of New York, GO |

|

|

|

|

|

|

|

|

| Series A-1, 4.00%, 09/01/46 |

|

|

2,305 |

|

|

|

2,253,520 |

|

| Series B, 5.25%, 10/01/47 |

|

|

4,605 |

|

|

|

5,145,217 |

|

| Series D-1, 5.50%, 05/01/46 |

|

|

1,140 |

|

|

|

1,298,527 |

|

| Series F-1, 5.00%, 04/01/45 |

|

|

4,950 |

|

|

|

5,230,620 |

|

| Series F-1, 4.00%, 03/01/47 |

|

|

2,270 |

|

|

|

2,232,509 |

|

| Sub-Series D-1, 5.00%,

08/01/31 |

|

|

945 |

|

|

|

945,865 |

|

| Sub-Series E-1, 4.00%,

04/01/45 |

|

|

2,485 |

|

|

|

2,450,011 |

|

| City of New York, Refunding GO |

|

|

|

|

|

|

|

|

| Series E, 5.50%, 08/01/25 |

|

|

460 |

|

|

|

460,583 |

|

| Series E, 5.00%, 08/01/32 |

|

|

2,000 |

|

|

|

2,001,832 |

|

| County of Nassau New York, GO |

|

|

|

|

|

|

|

|

| Series A, 5.00%, 01/15/31 |

|

|

1,400 |

|

|

|

1,511,338 |

|

| Series C, 5.00%, 10/01/31 |

|

|

1,980 |

|

|

|

2,174,173 |

|

| County of Nassau New York, Refunding GO, Series B, (AGM), 5.00%, 04/01/40 |

|

|

1,795 |

|

|

|

1,937,851 |

|

|

| Erie County Industrial Development Agency, Refunding RB, Series A, (SAW), 5.00%,

05/01/28 |

|

|

1,685 |

|

|

|

1,761,368 |

|

|

| Ithaca City School District, Refunding GO, (BAM SAW), 2.00%, 06/15/33 |

|

|

365 |

|

|

|

321,516 |

|

|

| Mahopac Central School District, Refunding GO, (SAW), 2.00%, 06/01/32 |

|

|

555 |

|

|

|

500,388 |

|

|

| New York City Industrial Development Agency, RB, (AGC), 0.00%, 03/01/39(b) |

|

|

1,380 |

|

|

|

652,922 |

|

|

| New York City Industrial Development Agency, Refunding RB, (AGM), 4.00%, 03/01/45 |

|

|

3,600 |

|

|

|

3,523,666 |

|

|

| New York City Transitional Finance Authority Future Tax Secured Revenue, RB |

|

|

|

|

|

|

|

|

|

| Series A-1, 5.00%, 11/01/38 |

|

|

950 |

|

|

|

953,524 |

|

| Series A-1, 5.00%, 08/01/40 |

|

|

860 |

|

|

|

918,267 |

|

|

|

|

|

|

|

|

|

|

| Security |

|

Par

(000) |

|

|

Value |

|

|

| County/City/Special District/School District (continued) |

|

| New York City Transitional Finance Authority Future Tax Secured Revenue, RB (continued) |

|

|

|

|

|

|

|

|

|

| Series B-1, 5.00%, 08/01/45 |

|

$ |

6,575 |

|

|

$ |

6,852,925 |

|

| Sub-Series A-3, 4.00%,

08/01/43 |

|

|

2,790 |

|

|

|

2,760,499 |

|

| Sub-Series B-1, 5.00%,

11/01/35 |

|

|

2,100 |

|

|

|

2,134,178 |

|

| Sub-Series B-1, 5.00%,

11/01/36 |

|

|

1,690 |

|

|

|

1,714,819 |

|

| Sub-Series B-1, 5.00%,

11/01/38 |

|

|

1,455 |

|

|

|

1,511,212 |

|

| Sub-Series E-1, 5.00%,

02/01/39 |

|

|

2,730 |

|

|

|

2,869,301 |

|

| Sub-Series E-1, 5.00%,

02/01/43 |

|

|

4,760 |

|

|

|

4,966,279 |

|

| Series A, Subordinate, 4.00%, 05/01/53 |

|

|

1,365 |

|

|

|

1,318,743 |

|

| Series A-2, Subordinate, 5.00%, 08/01/39 |

|

|

3,440 |

|

|

|

3,631,594 |

|

| Series C, Subordinate, 4.00%, 05/01/45 |

|

|

2,275 |

|

|

|

2,213,700 |

|

| Series F-1, Subordinate, 5.00%, 02/01/44 |

|

|

355 |

|

|

|

386,338 |

|

| New York Convention Center Development Corp., RB, CAB(b) |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Series B, Sub Lien, 0.00%, 11/15/42 |

|

|

2,185 |

|

|

|

831,950 |

|

| Series B, Sub Lien, 0.00%, 11/15/47 |

|

|

5,600 |

|

|

|

1,579,032 |

|

| Series B, Sub Lien, 0.00%, 11/15/48 |

|

|

2,665 |

|

|

|

746,339 |

|

| Series B, Sub Lien, (AGM-CR), 0.00%, 11/15/55 |

|

|

2,485 |

|

|

|

475,035 |

|

| Series B, Sub Lien, (AGM-CR), 0.00%, 11/15/56 |

|

|

3,765 |

|

|

|

681,653 |

|

| New York Convention Center Development Corp., Refunding RB |

|

| 5.00%, 11/15/40 |

|

|

6,150 |

|

|

|

6,298,725 |

|

| 5.00%, 11/15/45 |

|

|

12,215 |

|

|

|

12,449,455 |

|

| New York Liberty Development Corp., Refunding RB |

|

|

|

|

|

|

|

|

| Series 1, 5.00%, 11/15/44(c) |

|

|

5,075 |

|

|

|

4,952,997 |

|

| Series A, 3.00%, 11/15/51 |

|

|

1,460 |

|

|

|

1,059,611 |

|

| South Glens Falls Central School District, Refunding GO |

|

|

|

|

|

|

|

|

|

| Series A, (SAW), 2.00%, 07/15/34 |

|

|

1,160 |

|

|

|

995,386 |

|

| Series A, (SAW), 2.00%, 07/15/35 |

|

|

685 |

|

|

|

594,119 |

|

| Triborough Bridge & Tunnel Authority Sales Tax Revenue, RB |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Class A, 4.00%, 05/15/57 |

|

|

1,300 |

|

|

|

1,264,717 |

|

| Series A, 4.13%, 05/15/53 |

|

|

1,705 |

|

|

|

1,679,991 |

|

| Series A, 5.00%, 05/15/53 |

|

|

3,415 |

|

|

|

3,725,191 |

|

| Trust for Cultural Resources of The City of New York, Refunding RB(d) |

|

|

|

|

|

|

|

|

| 5.00%, 08/01/23 |

|

|

2,000 |

|

|

|

2,000,000 |

|

| Series A, 5.00%, 08/01/23 |

|

|

2,840 |

|

|

|

2,840,000 |

|

| Yonkers Industrial Development Agency, Refunding RB, (SAW), 4.00%, 05/01/41 |

|

|

1,000 |

|

|

|

1,005,106 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

113,585,249 |

|

|

|

|

| Education — 14.8% |

|

|

|

|

|

|

| Albany Capital Resource Corp., Refunding RB 4.00%, 07/01/41 |

|

|

740 |

|

|

|

466,315 |

|

| 4.00%, 07/01/51 |

|

|

765 |

|

|

|

424,785 |

|

| Build NYC Resource Corp., RB, 5.75%, 06/01/62(c)

|

|

|

860 |

|

|

|

844,401 |

|

| Build NYC Resource Corp., Refunding RB 4.00%, 08/01/42 |

|

|

525 |

|

|

|

475,289 |

|

| Series A, 5.00%, 06/01/43 |

|

|

450 |

|

|

|

457,113 |

|

| Dobbs Ferry Local Development Corp., RB, 5.00%, 07/01/39 |

|

|

750 |

|

|

|

763,549 |

|

| Dutchess County Local Development Corp., RB 5.00%, 07/01/43 |

|

|

570 |

|

|

|

598,125 |

|

| 5.00%, 07/01/48 |

|

|

855 |

|

|

|

890,606 |

|

| 5.00%, 07/01/52 |

|

|

1,365 |

|

|

|

1,455,446 |

|

| Dutchess County Local Development Corp., Refunding RB |

|

| 5.00%, 07/01/42 |

|

|

985 |

|

|

|

1,032,841 |

|

|

|

|

| 12 |

|

2 0 2 3 B L A C

K R O C K A N N U A L R E P O R

T T O S H A R E H O L D E R

S |

|

|

|

| Schedule of Investments (continued)

July 31, 2023 |

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN)

(Percentages shown are based on Net Assets) |

|

|

|

|

|

|

|

|

|

| Security |

|

Par

(000) |

|

|

Value |

|

|

|

|

| Education (continued) |

|

|

|

|

|

|

| Dutchess County Local Development Corp., Refunding RB (continued) |

|

| 4.00%, 07/01/46 |

|

$ |

1,865 |

|

|

$ |

1,852,421 |

|

| Madison County Capital Resource Corp., RB |

|

|

|

|

|

|

|

|

| Series B, 5.00%, 07/01/40 |

|

|

685 |

|

|

|

704,114 |

|

| Series B, 5.00%, 07/01/43 |

|

|

2,480 |

|

|

|

2,542,211 |

|

| Monroe County Industrial Development Corp.,

Refunding RB |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Series A, 4.00%, 07/01/39 |

|

|

350 |

|

|

|

352,062 |

|

| Series A, 4.00%, 07/01/50 |

|

|

11,950 |

|

|

|

11,441,611 |

|

| New York State Dormitory Authority, RB 1st Series, (AMBAC), 5.50%, 07/01/40 |

|

|

3,500 |

|

|

|

4,293,156 |

|

| Series A, 5.00%, 07/01/46 |

|

|

410 |

|

|

|

414,183 |

|

| New York State Dormitory Authority, Refunding RB 5.00%, 07/01/44 |

|

|

1,900 |

|

|

|

1,918,001 |

|

| Series A, 5.00%, 07/01/35 |

|

|

1,030 |

|

|

|

1,066,329 |

|

| Series A, 4.00%, 07/01/37 |

|

|

510 |

|

|

|

511,189 |

|

| Series A, 5.00%, 07/01/43 |

|

|

1,520 |

|

|

|

1,548,999 |

|

| Series A, 5.00%, 07/01/48 |

|

|

5,600 |

|

|

|

5,725,877 |

|

| Onondaga County Trust for Cultural Resources, Refunding RB |

|

|

|

|

|

|

|

|

| 5.00%, 12/01/38 |

|

|

1,490 |

|

|

|

1,619,547 |

|

| 5.00%, 12/01/39 |

|

|

2,650 |

|

|

|

2,872,277 |

|

| 4.00%, 12/01/47 |

|

|

1,800 |

|

|

|

1,754,537 |

|

| Orange County Funding Corp., Refunding RB |

|

|

|

|

|

|

|

|

| Series A, 5.00%, 07/01/37 |

|

|

715 |

|

|

|

714,980 |

|

| Series A, 5.00%, 07/01/42 |

|

|

445 |

|

|

|

444,890 |

|

| Troy Capital Resource Corp., Refunding RB 5.00%, 09/01/35 |

|

|

450 |

|

|

|

495,648 |

|

| 5.00%, 09/01/36 |

|

|

2,360 |

|

|

|

2,575,539 |

|

| 4.00%, 09/01/40 |

|

|

1,320 |

|

|

|

1,275,886 |

|

| Trust for Cultural Resources of The City of New York,

Refunding RB |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Series A, 5.00%, 07/01/37 |

|

|

1,775 |

|

|

|

1,809,128 |

|

| Series A, 5.00%, 07/01/41 |

|

|

750 |

|

|

|

762,317 |

|

| Yonkers Economic Development Corp., Refunding RB |

|

|

|

|

|

|

|

|

| Series A, 5.00%, 10/15/40 |

|

|

320 |

|

|

|

304,057 |

|

| Series A, 5.00%, 10/15/50 |

|

|

540 |

|

|

|

485,702 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

54,893,131 |

|

|

|

|

| Health — 7.9% |

|

|

|

|

|

|

| Build NYC Resource Corp., RB |

|

|

|

|

|

|

|

|

| Class A, 5.25%, 07/01/37 |

|

|

1,250 |

|

|

|

1,144,658 |

|

| Class A, 5.50%, 07/01/47 |

|

|

765 |

|

|

|

680,369 |

|

| Genesee County Funding Corp., Refunding RB, |

|

|

|

|

|

|

|

|

| Series A, 5.25%, 12/01/52 |

|

|

1,325 |

|

|

|

1,373,761 |

|

| Huntington Local Development Corp., RB, Series A, 5.25%, 07/01/56 |

|

|

240 |

|

|

|

188,517 |

|

| Monroe County Industrial Development Corp., RB 4.00%, 12/01/41 |

|

|

500 |

|

|

|

451,991 |

|

| 5.00%, 12/01/46 |

|

|

235 |

|

|

|

237,019 |

|

| Series A, 5.00%, 12/01/37 |

|

|

1,180 |

|

|

|

1,180,614 |

|

| Monroe County Industrial Development Corp., Refunding RB |

|

|

|

|

|

|

|

|

| 4.00%, 12/01/38 |

|

|

1,150 |

|

|

|

1,080,285 |

|

| 4.00%, 12/01/39 |

|

|

475 |

|

|

|

443,294 |

|

| 4.00%, 12/01/46 |

|

|

4,595 |

|

|

|

4,072,999 |

|

| New York State Dormitory Authority, RB |

|

|

|

|

|

|

|

|

| Series C, 4.25%, 05/01/39 |

|

|

1,000 |

|

|

|

999,877 |

|

| Series D, 4.25%, 05/01/39 |

|

|

685 |

|

|

|

684,916 |

|

|

|

|

|

|

|

|

|

|

| Security |

|

Par

(000) |

|

|

Value |

|

|

|

|

| Health (continued) |

|

|

|

|

|

|

| New York State Dormitory Authority, Refunding RB 4.00%, 07/01/45 |

|

$ |

380 |

|

|

$ |

257,585 |

|

| 4.00%, 07/01/47 |

|

|

2,660 |

|

|

|

2,597,267 |

|

| 4.25%, 05/01/52 |

|

|

3,645 |

|

|

|

3,569,658 |

|

| 5.00%, 05/01/52 |

|

|

3,850 |

|

|

|

4,113,205 |

|

| Series A, 5.00%, 05/01/32 |

|

|

2,645 |

|

|

|

2,727,479 |

|

| Oneida County Local Development Corp., Refunding |

|

|

|

|

|

|

|

|

| RB, (AGM), 3.00%, 12/01/44 |

|

|

2,540 |

|

|

|

1,959,773 |

|

| Suffolk County Economic Development Corp., RB, |

|

|

|

|

|

|

|

|

| Series C, 5.00%, 07/01/32 |

|

|

460 |

|

|

|

467,446 |

|

| Westchester County Local Development Corp., Refunding

RB(c) |

|

|

|

|

|

|

|

|

| 5.00%, 07/01/41 |

|

|

510 |

|

|

|

429,895 |

|

| 5.00%, 07/01/56 |

|

|

570 |

|

|

|

440,299 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29,100,907 |

|

|

|

|

| Housing — 8.0% |

|

|

|

|

|

|

| New York City Housing Development Corp., RB, M/F

Housing |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Series G-1, 3.90%, 05/01/45 |

|

|

450 |

|

|

|

400,569 |

|

| Sustainability Bonds, 4.80%, 02/01/53 |

|

|

2,915 |

|

|

|

2,951,012 |

|

| Class F-1, Sustainability Bonds, 4.60%, 11/01/42 |

|

|

225 |

|

|

|

227,001 |

|

| Series A, Sustainability Bonds, 4.75%, 11/01/48 |

|

|

365 |

|

|

|

370,103 |

|

| Series E-1, Sustainability Bonds, (SONYMA HUD SECT 8), 4.20%,

11/01/42 |

|

|

920 |

|

|

|

889,432 |

|

| New York City Housing Development Corp., Refunding |

|

|

|

|

|

|

|

|

| RB, Series F-1-A,

Sustainability Bonds, 3.30%, 11/01/46 |

|

|

460 |

|

|

|

389,575 |

|

| New York City Housing Development Corp., Refunding |

|

|

|

|

|

|

|

|

| RB, M/F Housing |

|

|

|

|

|

|

|

|

| Sustainability Bonds, 3.85%, 05/01/58 |

|

|

1,726 |

|

|

|

1,449,036 |

|

| Series B-1-A, Sustainability

Bonds, 3.75%, 11/01/54 |

|

|

1,345 |

|

|

|

1,147,546 |

|

| New York State Housing Finance Agency, RB |

|

|

|

|

|

|

|

|

| Series D, (SONYMA), 3.80%, 11/01/49 |

|

|

1,700 |

|

|

|

1,435,446 |

|

| Series B-1, Sustainability Bonds, (SONYMA), 4.85%, 11/01/48 |

|

|

1,310 |

|

|

|

1,328,218 |

|

| New York State Housing Finance Agency, RB, M/F |

|

|

|

|

|

|

|

|

| Housing |

|

|

|

|

|

|

|

|

| (SONYMA), 4.65%, 11/01/48 |

|

|

515 |

|

|

|

516,986 |

|

| Series B, (FHLMC, FNMA, GNMA, SONYMA), 4.00%, 11/01/42 |

|

|

845 |

|

|

|

774,275 |

|

| Series E, (SONYMA), 3.80%, 11/01/49 |

|

|

945 |

|

|

|

797,377 |

|

| Series H, (FNMA, SONYMA), 4.15%, 11/01/43 |

|

|

1,375 |

|

|

|

1,278,844 |

|

| Series H, (FNMA, SONYMA), 4.20%, 11/01/48 |

|

|

905 |

|

|

|

824,405 |

|

| Series I, (FNMA, SONYMA), 4.05%, 11/01/48 |

|

|

1,090 |

|

|

|

969,982 |

|

| Series A, AMT, 4.65%, 11/15/38 |

|

|

1,000 |

|

|

|

970,381 |

|

| New York State Housing Finance Agency, Refunding |

|

|

|

|

|

|

|

|

| RB, Series C, (FNMA, SONYMA), 3.85%, 11/01/39 |

|

|

2,005 |

|

|

|

1,847,197 |

|

| State of New York Mortgage Agency, RB, S/F Housing 250th Series, (SONYMA), 4.80%, 10/01/48 |

|

|

3,410 |

|

|

|

3,483,475 |

|

| Series 239, (SONYMA), 2.70%, 10/01/47 |

|

|

1,360 |

|

|

|

979,371 |

|

| State of New York Mortgage Agency, Refunding RB |

|

|

|

|

|

|

|

|

| Series 190, 3.80%, 10/01/40 |

|

|

1,395 |

|

|

|

1,364,602 |

|

| Series 194, AMT, 3.80%, 04/01/28 |

|

|

2,065 |

|

|

|

2,065,694 |

|

| Series 218, AMT, 3.60%, 04/01/33 |

|

|

855 |

|

|

|

842,054 |

|

| Series 218, AMT, 3.85%, 04/01/38 |

|

|

115 |

|

|

|

114,261 |

|

| Yonkers Industrial Development Agency, RB, AMT, |

|

|

|

|

|

|

|

|

| (SONYMA), 5.25%, 04/01/37 |

|

|

2,000 |

|

|

|

2,000,192 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29,417,034 |

|

|

|

|

| S C H E D U L E

O F I N V E S T M E N T S |

|

13 |

|

|

|

| Schedule of Investments (continued)

July 31, 2023 |

|

BlackRock MuniHoldings New York Quality Fund, Inc. (MHN)

(Percentages shown are based on Net Assets) |

|

|

|

|

|

|

|

|

|

| Security |

|

Par

(000) |

|

|

Value |

|

|

|

|

| State — 11.8% |

|

|

|

|

|

|

| New York City Transitional Finance Authority Building |

|

|

|

|

|

|

|

|

| Aid Revenue, Refunding RB |

|

|

|

|

|

|

|

|

| Series S-1, Subordinate, (SAW), 4.00%, 07/15/35 |

|

$ |

910 |

|

|

$ |

962,485 |

|

| Series S-3, Subordinate, (SAW), 4.00%, 07/15/38 |

|

|

5,045 |

|

|

|

5,121,815 |

|

| New York State Dormitory Authority, RB |

|

|

|

|

|

|

|

|

| Series A, 5.00%, 03/15/38 |

|

|

3,425 |

|

|

|

3,663,901 |

|

| Series A, 5.00%, 03/15/40 |

|

|

3,700 |

|

|

|

3,900,085 |

|

| Series A, 5.00%, 03/15/44 |

|

|

7,475 |

|

|

|

7,894,364 |

|

| Series B, 5.00%, 03/15/38 |

|

|

1,000 |

|

|

|

1,057,060 |

|

| Series B, 5.00%, 03/15/39 |

|

|

1,465 |

|

|

|

1,544,873 |

|

| New York State Dormitory Authority, Refunding RB, |

|

|

|

|

|

|

|

|

| Series A, 5.00%, 03/15/40 |

|

|

2,950 |

|

|

|

3,167,902 |

|

| New York State Urban Development Corp., RB |

|

|

|

|

|

|

|

|

| Series A, 4.00%, 03/15/45 |

|

|

5,265 |

|

|

|

5,211,418 |

|

| Series A, 3.00%, 03/15/50 |

|

|

3,105 |

|

|

|

2,416,482 |

|

| Series C, 5.00%, 03/15/32 |

|

|

2,000 |

|

|

|

2,001,958 |

|

| New York State Urban Development Corp., Refunding |

|

|

|

|

|

|

|

|

| RB, 4.00%, 03/15/46 |

|

|

6,880 |

|

|

|

6,766,163 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

43,708,506 |

|

|

|

|

| Tobacco — 2.9% |

|

|

|

|

|

|

| Chautauqua Tobacco Asset Securitization Corp., Refunding RB |

|

|

|

|

|

|

|

|

| 4.75%, 06/01/39 |

|

|

1,875 |

|

|

|

1,803,319 |

|

| 5.00%, 06/01/48 |

|

|

680 |

|

|

|

638,852 |

|

| New York Counties Tobacco Trust VI, Refunding RB |

|

|

|

|

|

|

|

|

| Series A-2B, 5.00%, 06/01/45 |

|

|

2,010 |

|

|

|

1,902,909 |

|

| Series A-2B, 5.00%, 06/01/51 |

|

|

765 |

|

|

|

716,022 |

|

| Series B, 5.00%, 06/01/41 |

|

|

575 |

|

|

|

581,367 |

|

| Niagara Tobacco Asset Securitization Corp., Refunding RB |

|

|

|

|

|

|

|

|

| 5.25%, 05/15/34 |

|

|

1,495 |

|

|

|

1,513,383 |

|

| 5.25%, 05/15/40 |

|

|

1,500 |

|

|

|

1,520,407 |

|

| TSASC, Inc., Refunding RB, Series A, 5.00%, 06/01/35 |

|

|

260 |

|

|

|

268,771 |

|

| Westchester Tobacco Asset Securitization Corp., |

|

|

|

|

|

|

|

|

| Refunding RB, Sub-Series C, 4.00%, 06/01/42 |

|

|

1,720 |

|

|

|

1,691,214 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10,636,244 |

|

|

|

|