UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 13D

(Rule 13d-101)

INFORMATION TO BE INCLUDED IN STATEMENTS FILED

PURSUANT

TO RULE 13d-1(a) AND AMENDMENTS THERETO FILED

PURSUANT TO RULE 13d-2(a)

Under the Securities Exchange Act of 1934

(Amendment No. 15)*

Abcam plc

(Name of Issuer)

Ordinary Shares

(Title of Class of Securities)

000380204

(CUSIP Number)

Jonathan Milner

Honey Hill House, 20 Honey Hill

Cambridge CB3 0BG

With copies to:

|

Richard M. Brand

Cadwalader, Wickersham & Taft LLP

200 Liberty Street

New York, NY 10281

212-504-6000 |

Michael Newell

Cadwalader, Wickersham & Taft LLP

100 Bishopsgate

London EC2N 4AG

44 (0) 20 7170 8540 |

(Name, Address and Telephone Number of Person

Authorized to Receive Notices and Communications)

October 16, 2023

(Date of Event Which Requires Filing of This

Statement)

If the filing person

has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this

schedule because of Rule 13d-1(e), 13d-1(f) or 13d-1(g), check the following box. x

Note:

Schedules filed in paper format shall include a signed original and five copies of the schedule, including all exhibits. See Rule 13d-7

for other parties to whom copies are to be sent.

| * |

The remainder of this cover page shall be filled out for a reporting person’s initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page. |

The information required on the remainder of

this cover page shall not be deemed to be “filed” for the purpose of section 18 of the Securities Exchange Act of 1934 (“Act”)

or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however, see

the Notes).

| 1 |

NAME OF REPORTING PERSON

Dr. Jonathan Milner |

| 2 |

CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP

(a) ¨

(b) x

|

| 3 |

SEC USE ONLY

|

| 4 |

SOURCE OF FUNDS

PF (See Item 3) |

| 5 |

CHECK

BOX IF DISCLOSURE OF LEGAL PROCEEDINGS IS REQUIRED PURSUANT TO ITEMS 2(d) OR 2(e) ¨

|

| 6 |

CITIZENSHIP OR PLACE OF ORGANIZATION

United Kingdom |

|

Number of

shares

beneficially

owned by

each

reporting

person

with

|

|

7 |

SOLE VOTING POWER

11,763,1001 |

| |

8 |

SHARED VOTING POWER

2,410,8022 |

| |

9 |

SOLE DISPOSITIVE POWER

11,763,1001 |

| |

10 |

SHARED DISPOSITIVE POWER

2,410,8022 |

| 11 |

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH REPORTING PERSON

14,173,9021, 2 |

| 12 |

CHECK

BOX IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES ¨

|

| 13 |

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11)

6.16%* |

| 14 |

TYPE OF REPORTING PERSON

IN |

* All percentage calculations set forth herein are based upon the aggregate

of 230,151,118 Ordinary Shares as of October 2, 2023, as reported in Exhibit 99.2 of the Issuer’s Report of Foreign Private Issuer

on Form 6-K Filed with the SEC on October 5, 2023.

1 Includes 11,700,200 Ordinary Shares directly held by the

Reporting Person and 62,900 shares directly held by the Reporting Person through American Depository Shares representing, each, one Ordinary

Share (“ADS”).

2 Includes 399,382 ADSs held by the Reporting Person’s

spouse, 1,977,967 ADSs held by three limited companies over which the Reporting Person exercises investment discretion and 33,453 ADSs

held by a charitable trust to which the Reporting Person is a trustee and signatory. The Reporting Person disclaims beneficial ownership

over the shares beneficially owned by his spouse, except to the extent of his pecuniary interest therein.

This Amendment No. 15 to Schedule

13D (this “Amendment No. 15”) amends and supplements the Schedule 13D filed on May 1, 2023, as amended and supplemented on

May 18, 2023, May 30, 2023, June 5, 2023, June 6, 2023, June 12, 2023, June 20, 2023, June 21, 2023, June 23, 2023, June 27, 2023, August

16, 2023, September 14, 2023, September 28, 2023, October 10, 2023 and October 12, 2023 (the “Original 13D,” and as amended

and supplemented by this Amendment No. 15, the “Schedule 13D”) by the Reporting Person, relating to the Ordinary Shares of

the Issuer. Except as specifically provided herein, this Amendment No. 15 does not modify any of the information previously reported in

the Schedule 13D. Capitalized terms not defined in this Amendment No. 15 shall have the meaning ascribed to them in the Original 13D.

The purpose of this Amendment No. 15 is to update

the disclosure in Items 4 and 7 of the Schedule 13D as hereinafter set forth.

| ITEM 1. |

SECURITY AND ISSUER |

This statement on Schedule

13D relates to the Ordinary Shares of the Issuer. The principal executive offices of the Issuer are located at Discovery Drive, Cambridge

Biomedical Campus, Cambridge, CB2 0AX, United Kingdom.

| ITEM 2. |

IDENTITY AND BACKGROUND |

(a), (f) This statement is being filed by

Dr. Jonathan Milner, a citizen of the United Kingdom.

(b) The address of the Reporting Person is

Honey Hill House, 20 Honey Hill, Cambridge, CB3 0BG.

(c) The Reporting Person’s

principal occupation is as an investor and executive in life sciences companies.

(d), (e) During the last

five years, the Reporting Person (i) has not been convicted in a criminal proceeding (excluding traffic violations or similar misdemeanors)

and (ii) was not a party to a civil proceeding of a judicial or administrative body of competent jurisdiction and as a result of such

proceeding was or is subject to a judgment, decree or final order enjoining future violations of, or prohibiting or mandating activities

subject to, federal or state securities laws or finding any violations with respect to such laws.

| ITEM 4. |

PURPOSE OF TRANSACTION |

Item 4 is hereby amended to add the following:

On October 16, 2023, the Reporting Person published

a slide deck presentation regarding the Issuer, as set forth more fully in Exhibit 99.22 hereto.

On October 16, 2023, the Reporting Person published

a press release regarding the Issuer, as set forth more fully in Exhibit 99.23 hereto.

On October 16, 2023, the Reporting Person published a press release regarding a recent analyst report, as set forth more fully in Exhibit

99.24 hereto.

| ITEM 5. |

INTEREST IN SECURITIES OF THE ISSUER |

(a) The Reporting Person is the holder of 11,700,200

Ordinary Shares and 62,900 ADSs. In addition, the Reporting Person may be deemed to share beneficial ownership over (a) 1,977,967 ADSs

beneficially owned by three limited companies over which the Reporting Person exercises investment discretion, (b) 399,382 ADSs beneficially

owned by the Reporting Person’s spouse and (c) 33,453 ADSs held by a charitable trust to which the Reporting Person is a trustee

and signatory. The Reporting Person disclaims beneficial ownership over the shares beneficially owned by his spouse, except to the extent

of his pecuniary interest therein. The shares described in this Item 5 represent approximately 6.16% of the outstanding Ordinary

Shares.

(b)

| |

(i) |

Sole power to vote or to direct the vote: 11,763,100 |

| |

(ii) |

Shared power to vote or direct the vote: 2,410,802 |

| |

(iii) |

Sole power to dispose or to direct the disposition of: 11,763,100 |

| |

(iv) |

Shared power to dispose or to direct the disposition of: 2,410,802 |

(c) See Schedule V, which is incorporated herein

by reference, describes the transactions by the Reporting Person in the Common Stock during the past sixty days.

(d) N/A

(e) N/A

| ITEM 7. |

MATERIAL TO BE FILED AS EXHIBITS |

Item 7 is hereby amended to add the following

exhibit:

SIGNATURES

After reasonable inquiry and to the best of my

knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

Date: October 16, 2023

| |

By: |

/s/ Jonathan Milner |

| |

|

Name: Jonathan Milner |

Schedule V

TRADING DATA

The following table sets forth all transactions in the Ordinary Shares

of the Issuer effected by the Reporting Person in the past 60 days. Except as otherwise noted below, all such transactions were purchases

or sales of Ordinary Shares effected in the open market and the table excludes commissions paid in per share prices.

| Reporting Person | |

Trade Date | |

Buy/Sell | |

No. of

Shares/

Quantity | | |

Unit Cost/

Proceeds | | |

Security |

| Jonathan Milner | |

9/11/2023 | |

Buy | |

| 4,500 | | |

$ | 22.8599 | | |

ADS |

| Jonathan Milner | |

9/12/2023 | |

Buy | |

| 4,500 | | |

$ | 22.7899 | | |

ADS |

| Jonathan Milner | |

9/13/2023 | |

Buy | |

| 4,500 | | |

$ | 22.8389 | | |

ADS |

| Jonathan Milner | |

9/14/2023 | |

Buy | |

| 4,500 | | |

$ | 22.8172 | | |

ADS |

| Jonathan Milner | |

9/15/2023 | |

Buy | |

| 4,500 | | |

$ | 22.8200 | | |

ADS |

| Jonathan Milner | |

9/18/2023 | |

Buy | |

| 4,500 | | |

$ | 22.7244 | | |

ADS |

| Jonathan Milner | |

9/19/2023 | |

Buy | |

| 4,500 | | |

$ | 22.6700 | | |

ADS |

| Jonathan Milner | |

9/20/2023 | |

Buy | |

| 4,500 | | |

$ | 22.6500 | | |

ADS |

| Jonathan Milner | |

9/21/2023 | |

Buy | |

| 4,500 | | |

$ | 22.6800 | | |

ADS |

| Jonathan Milner | |

9/22/2023 | |

Buy | |

| 4,500 | | |

$ | 22.6000 | | |

ADS |

| Jonathan Milner | |

9/29/2023 | |

Buy | |

| 4,400 | | |

$ | 22.6722 | | |

ADS |

| Jonathan Milner | |

9/29/2023 | |

Buy | |

| 4,400 | | |

$ | 22.7461 | | |

ADS |

| Jonathan Milner | |

10/02/2023 | |

Buy | |

| 4,400 | | |

$ | 22.6457 | | |

ADS |

| Jonathan Milner | |

10/09/2023 | |

Buy | |

| 4,500 | | |

$ | 22.6700 | | |

ADS |

Exhibit 99.22

Dr Jonathan Milner FOCUS ABCAM

2 • Activism campaign brought to bring focus to governance, execution and cost control • All have been lacking and have hit company performance • Precipitated review of strategic alternatives including a potential sale • Culminated in $24 per share offer from Danaher which I believe significantly undervalues Abcam • No premium being paid for control • Questions raised by approaches used in fairness opinions • Abcam’s own numbers paint a highly attractive independent future • 5 - year investment plan is bearing fruit from FY2024 as I knew it would (despite the missteps) • Board must have no faith in management to deem now the right time to sell • I know this business, I have a plan for this business and I believe in this business Wrong deal, wrong time, wrong price Abcam is a prized UK life sciences asset…under threat

3 0 5 10 15 20 25 30 35 40 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21 Jan-22 Apr-22 Jul-22 Oct-22 Abcam Peers composite Russell 3000 Share price performance has been dismal… Sources: Refinitiv Eikon and Company announcements Prices rebased to Abcam share price • …which caused me to agitate for change Raises $180m via secondary offering of ADSs at $17.50 H1 trading update, revenues of £147.5m, 8.3% up on CC basis Acquiring BioVision for $340m in cash, 10x sales, EPS accretive in first full year H1/FY results. H1 sales up 23% to £150m, EBIT of £10.3m FY trading update, revenues of £315m up 22% on CC basis, EBIT to be in line FY results, EBIT of £7.1m, adj. EBIT of £60.4m, up 19% H1 trading update, revenues of £185m, 19% growth on CC basis. Confirms plan to cancel trading on AIM Interim results, EBIT of £9.3m, down 10%, adj. EBIT of £42.6m, up 61% AIM delisting becomes effective Interim results, EBIT of £15.5m down 42%

4 Share price performance has been dismal… (cont.) Sources: Refinitiv Eikon and Company announcements Prices rebased to Abcam share price 0 5 10 15 20 25 30 35 40 Jan-23 Feb-23 Mar-23 Apr-23 May-23 Jun-23 Jul-23 Aug-23 Sep-23 Oct-23 Abcam Peers composite Russell 3000 FY trading update, revenues of ~£360m. ERP system and China impacted revenues FY results EBIT loss of £10.1m, adj. EBIT of £76.3m up 26% Q1 update, revenues >£100m, China returns to growth. Guides to £420m - £440m FY23 revenues Confirms regular meetings with Dr Milner Incremental cost refinement actions to reduce annualised OPEX by >£15m by FY24 Receives notice from Dr. Milner to convene an EGM EGM convened for 12 July Abcam initiates a process to explore strategic alternatives including a potential sale of the Company Reiterates ’23 guidance, FY24 guidance of revenues of £475m - £525m Dr Milner withdraws EGM requisition notice H1 update, revenues >£203m, est. adj EBIT margin of >26% Danaher to acquire Abcam for $24 per share in cash Scheme document posted, court and general meetings on 6 Nov ‘23 • Only when my agitation for change became public did Abcam’s share price stop underperforming its peer group c.25% share price increase on news of Dr Milner’s activism alone (prior to initiation of strategic review)

5 0 10 20 30 40 50 60 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 EV/NTM EBITDA multiple (x) EV/EBITDA 12M fwd DHR bid Covid period Abcam is being sold below its historical trading multiple – why? ABCM valuation Average EV / NTM EBITDA (excl. Covid - 19) 22.1x Danaher bid implied FY24 EV / adj. EBITDA multiple 21.4x Source: CapIQ Period runs 9 September 2014 (date Jonathan Milner stepped down as CEO to become Deputy Chairman) through to 16 May 2023 (bei ng the last trading date prior to Dr Milner stating his intention to call an EGM) and excludes the Covid - 19 period from the long - term average multiple. (1) UK Covid - 19 lockdown announced on 23 October 2020, at which point the NTM EV/EBITDA multiple was 23.3x. Period of excluded d ata through to 12 January 2022 which marked the return to multiple seen on entering into the pandemic period. Long - term multiple including the whole period is 25.1x. Entry and exit from Covid - 19 period, excluded from analysis (1) • Abcam’s long - term average EV / NTM EBITDA trading multiple is above the level of the $24 per share bid (excluding positive impact of pandemic), but including management’s recent dismal period • Abcam is being sold with no premium for control

6 • The timing of the sale process is wrong for two reasons • Abcam is still working through the 5 - year plan and is not yet reaping its benefits, but they are close • Abcam’s peer group is experiencing a period of lower valuation multiples likely impacting take - out multiples • The huge discrepancy between reported and adjusted margins highlights the magnitude of the adjustments made during the investment phase The timing is wrong Source: Abcam financial statements & Peel Hunt equity research (Nov 2019) -5% 0% 5% 10% 15% 20% 25% 30% 35% 40% FY18 FY19 FY20 FY21 FY22 June June June Dec Dec Operating margin EBITDA margin Operating & EBITDA margins Operating & EBITDA margins (adjusted) Original margin suppression cost (4 - 7%) per Peel Hunt research dated November 2019 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% FY18 FY19 FY20 FY21 FY22 FY23 FY24 June June June Dec Dec Dec Dec Adjusted Operating margin Adjusted EBITDA margin

7 The 5 - year investment plan: 6 months late and over budget Source: 2019 Abcam Capital Markets Day, Abcam financial statements, Peel Hunt Equity Research (November 2019) Lost dividend calculated based on flat FY2019 DPS • I was an architect of the 5 - year plan in 2019 and believed in the objectives it set out to achieve • I was also a supporter of bearing the medium - term margin suppression required to pay for the necessary investments • The execution has been botched by management with poor oversight by the Board Original expected costs Additional pain for shareholders c.4 - 7% suppression of operating margin from FY20 to FY23/24 Evidence of significant operating inefficiencies Shareholder dilution: £110m 2020 offering Shareholder dilution: £127m Nasdaq IPO c.£80m lost dividends since suspension

8 Source: Scheme Circular Exchange rate used consistent with that in the Scheme Circular (1 GBP: 1.2 USD) Management’s projections are strong and Abcam is now poised to reap the returns of the 5 - year plan and significant investments made • FY23 - FY24 EBITDA margins up 600bps with 16% revenue growth • >£400m in unlevered free cash flow by 2032, a c.5 - fold increase • Such delivery I would expect to result in a significant uplift in Abcam’s share price The Danaher offer is not due to close until mid - 2024 , a transformational year for Abcam $ 24 per share will look particularly poor at closing Abcam’s own numbers paint an attractive outlook £ in millions 2022A 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E 2032E 2033E 2034E Revenue 362 430 500 572 653 744 840 942 1048 1142 1222 1296 1360 Y - o - Y growth 19% 16% 14% 14% 14% 13% 12% 11% 9% 7% 6% 5% Adjusted EBITDA 109 163 221 268 323 376 434 497 563 614 657 696 731 EBITDA margin 30% 38% 44% 47% 49% 51% 52% 53% 54% 54% 54% 54% 54% Adjusted EBIT 76 124 174 219 270 322 379 442 510 556 594 630 662 Unlevered Free Cash Flow 86 138 137 193 208 268 309 354 392 424 453 478

9 • Abcam’s financial advisers set out detailed fairness opinions examining multiple different ways of valuing the business • 7 of the 10 approaches were excluded from the analysis • A highly selective approach has been taken with inclusion / exclusion criteria • Referencing the 16 May 2023 share price of $ 17 . 23 to benchmark the $ 24 per share offer is arguably flawed • My efforts to focus and improve governance, execution and cost control resonated with investors and reversed the decline in share price that had persisted • If the company was not under offer, c . $ 24 per share is likely fair value today ; it is not a price for control of a prized life - sciences asset with very strong growth prospects ahead Observations on the fairness opinions by Abcam’s financial advisers

10 Summary of fairness opinion valuation ranges Source: Implied value per share numbers extracted from Abcam Scheme Circular $40.0 $30.0 $20.7 $22.7 $22.6 $28.3 $21.7 $24.2 $29.1 $14.4 $18.3 $17.9 $25.0 $23.5 $18.6 $13.9 $17.7 $14.7 $21.7 $15.1 $12.6 $17.0 $20.7 10 15 20 25 30 35 40 45 DCF Comps FY23 Comps FY24 Precedent transactions Future share price analysis LBO analysis Bio-Techne '23 EBITDA Bio-Techne '24 EBITDA Tier 2 Comps 23 EBITDA Tier 2 Comps 24 EBITDA Historical trading range Equity research target prices Premia paid Used in MS/Lazard analyses Excluded from MS/Lazard analyses Entirely backward - looking valuation metric on a very diverse group of transactions Appears to be a highly selective approach Appears to be a highly selective approach and impacted by Abcam’s investment phase Peculiar reason for exclusion – often seen as closest peer Rightly excluded – the reason I became an activist Excluded a key metric which reflects potential valuation impact of strong future financial performance Another approach which reflects potential valuation impact of strong future financial performance $24

11 • Extract from slide 17 of “Executing on Strategic Priorities to Drive Long Term Value” presentation published by Abcam on 20 June 2023 • Clearly outlines the Right Set of Life Science Tools Peers to value Abcam • However, Abcam’s financial advisers have minimised or left out 6 of the 8 peers in their fairness opinions that Abcam itself considered to have the scale and financial profile closest aligned to Abcam • Premium - rated companies like Repligen Corporation, Maravai Lifesciences and Illumina did not contribute to the comparable company analysis • This has depressed the multiples and the implied value per share detailed Trading comparables

12 Abcam is at the top end of its peer group 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0% Repligen Abcam Sartorius Maravai Bio-Techne Illumina Revvity Qiagen Tecan Group Bio Rad Laboratories Waters Corp Agilent Technologies Abcam’s trading comps - revenue CAGR (2023 - 2025) Abcam’s trading comps – EBITDA margin (FY24) 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0% Abcam Bio-Techne Qiagen Waters Corp Revvity Sartorius Agilent Technologies Maravai Repligen Bio Rad Laboratories Tecan Group Illumina Revenue CAGRs and EBITDA margins for all companies other than Abcam sourced from Bloomberg estimates as at 12 October 2023 Abcam’s revenue CAGR and 2024 adj. EBITDA margin is sourced from the Scheme Circular Excluded by Abcam’s financial advisers Excluded by Abcam’s financial advisers

13 0.0x 5.0x 10.0x 15.0x 20.0x 25.0x 30.0x 35.0x 40.0x 45.0x Repligen Illumina Maravai Abcam Bio-Techne Sartorius Tecan Group Waters Corp Bio Rad Laboratories Trading comparables – FY24 EV / EBITDA Abcam trading comps (as per June 2023 presentation) Morgan Stanley & Lazard selected trading comps (as per Scheme Circular) • Even if one continues to exclude Repligen from the comps the average FY24 multiple for Illumina and Maravai is 28.1x, representing a 31% premium to the Danaher multiple of 21.4x Comp multiple range Implied value per share Waters Sartorius Waters Sartorius EV / Estimated 2024 EBITDA 15.9x 19.1x $17.76 $21.47 Comp multiple range Implied value per share Min Max Min Max EV / Estimated 2024 EBITDA 15.4x 28.3x $17.21 $31.86 Comp multiples exclude Repligen , in line with the Scheme Circular. EV and 2024 EBITDA data, for all companies except for Abcam, is sourced from Bloomberg as of 12 October 2023. Abcam multiple is derived from the Danaher offer information sourced from the Scheme Circular document. Abcam’s EV is sourced from pg 95 of the Scheme Circular; Abcam’s EBITDA is sourced from pg 34 of the Scheme Circular 0.0x 5.0x 10.0x 15.0x 20.0x 25.0x 30.0x 35.0x 40.0x 45.0x Repligen Maravai Abcam Bio-Techne Sartorius Agilent Technologies Revvity Waters Corp Qiagen

14 Your interest in Abcam is important • $24 per share offer from Danaher significantly undervalues Abcam • Accept a higher offer incorporating a premium for control from Danaher or another acquirer • Abcam remains a strong, independent business (new strong Chair and CEO) • Abcam shareholders reap the benefits of the 5 - year plan and accelerated future growth • Significant transfer of value from Abcam shareholders to Danaher shareholders DO NOTHING JOIN ME, VOTE AGAINST

15 Abcam 3.0

16 Dr Jonathan Milner • As Deputy Chairman, he guided the current CEO until February 2020 when he stepped down from the Board and the company listed on Nasdaq with a market cap of c.$3.6bn • With an insiders and outsiders unique perspective he has the skillset and the passion to return Abcam to a high - performing and highly valued life science tools company • He is highly respected and trusted by employees, customers and shareholders – very little disruption and can hit the ground running • As the co - author of the 5 year Strategic Plan (see CMD presentation 2019) he knows the strategy inside out.

17 0 500 1000 1500 2000 2500 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11 Nov-12 Nov-13 Nov-14 Nov-15 Nov-16 Nov-17 Nov-18 Nov-19 Nov-20 Nov-21 Nov-22 Abcam share price performance and TSR under Dr Milner and others Source: Bloomberg AIM IPO to Dr Milner stepping down as CEO Dr Milner serves as Deputy Chairman +1,037% (TSR) +223% (TSR) +13% (TSR) Other Abcam acquisition of Epitomics

18 Abcam’s Mission is simple We improve health and save lives by enabling our customers to achieve their mission faster

19 • A unique opportunity to buy into a stellar growth story • Abcam’s Founder, Dr Jonathan Milner has exclusive knowledge of Abcam’s operations, strategy and markets, and will lead Abcam 3.0 into its next phase • This has the potential to unlock extraordinary shareholder value • This is NOT a turnaround - minimal disruption and execution risk • Seamless transition maintaining where Abcam excels, eliminating ‘anchors’ holding us back, boosting best performing markets and products and adding easy win growth opportunities Introducing Abcam 3.0

20 The vision – Abcam 3.0 • This is not a turnaround – primarily fixing Abcam’s operational and management issues • Disciplined execution and cost control over the next 3 years will maximise the return on the 5 year plan investment • Three year plan (2024 – 2026 inclusive) overlaps by one year with the 5 year plan coming to an end in 2024 giving seamless continuity and minimal disruption • Return transparency and clear communication with investors

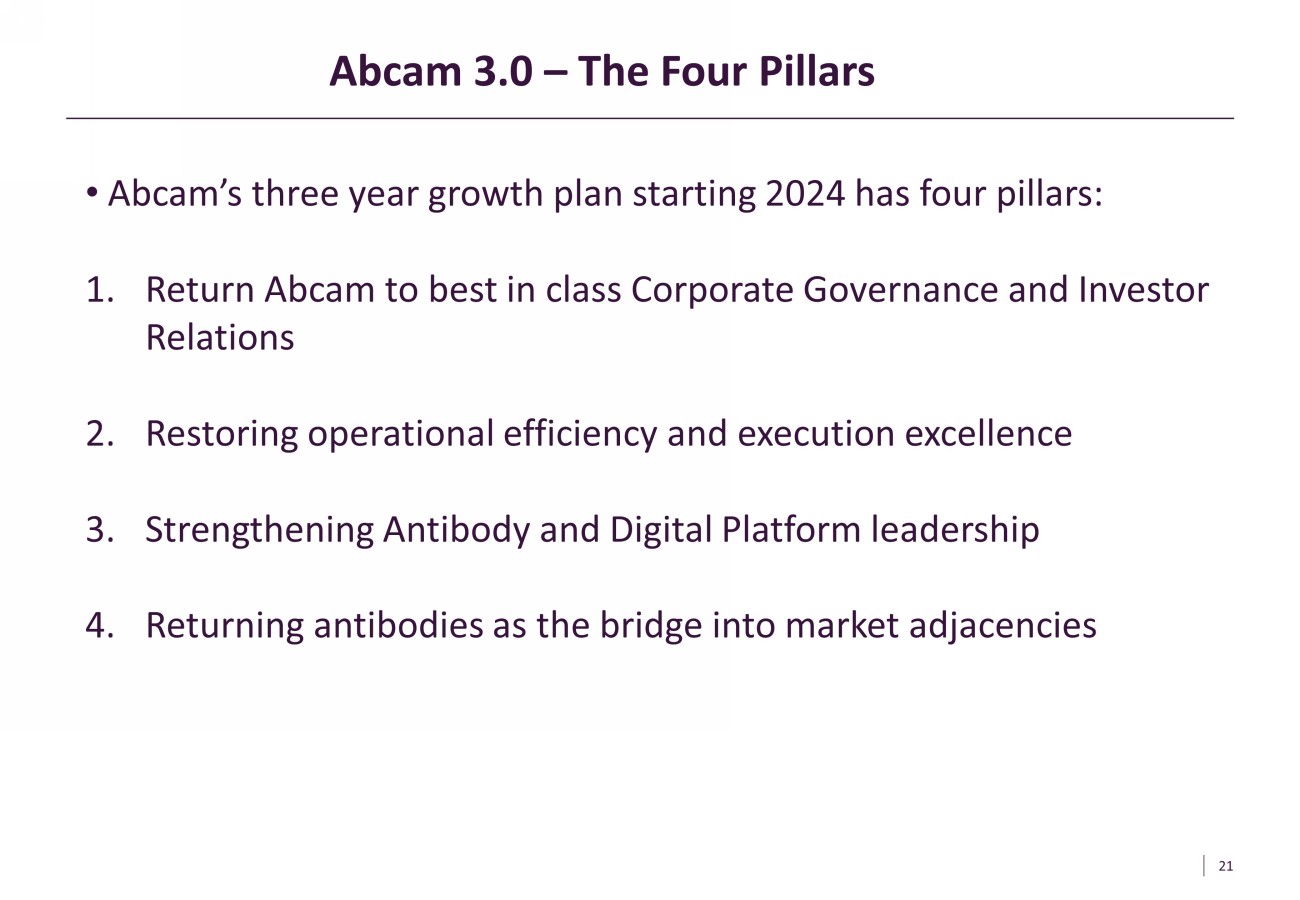

21 • Abcam’s three year growth plan starting 2024 has four pillars: 1. Return Abcam to best in class Corporate Governance and Investor Relations 2. Restoring operational efficiency and execution excellence 3. Strengthening Antibody and Digital Platform leadership 4. Returning antibodies as the bridge into market adjacencies Abcam 3.0 – The Four Pillars

22 Return Abcam to Best in Class Corporate Governance * www.abcamfocus.com Eliminate Boost Maintain Add • excessive executive bonuses that reward failure • poor treatment of shareholders • weaknesses in Financial Controls* • machinations of performance metrics* • changing the goalposts on performance metrics* • the CFO from the Board of Directors • shareholder representation (6.15%) • a strong Chair to hold the CEO to account • new heads of Rem., Audit and Nom • quarterly reporting • long term supportive shareholder base • UK Main Market listing, increase analyst coverage • investor meetings and interactions • transparency and clearer performance metrics • the role of the Remcom in setting Executive rewards • face to face investor meetings • diverse and experienced Board of Directors • a NASDAQ primary listing • existing US and UK Analysts • Board Cycle and Board Meeting Frequency • Annual General Meeting in Cambridge UK HQ • Cambridge UK HQ

23 Restoring Operational Efficiency and Execution Excellence * www.abcamfocus.com Eliminate Boost Maintain Add • all activities not serving customers or adding value • duplication of costs across geographic sites • spending ‘like drunken sailors’ and mistaking excessive spending for investment • excessive adjusting items eating into FCF • ‘Key Performance Indicators’ to restore focus • Sales per $ spent on remuneration • ROCE – return to >20% • An operationally and profit focused CFO • Dividends • free cash flow (FCF) • adjusted EBITDA margins to 50% • operating margins to 40% • revenues per employee metric • world class scientists • manufacturing in Eugene, OR, Waltham and Cambridge • personalized and swift customer service

24 Strengthen Antibody and Digital Platform Leadership * www.abcamfocus.com Eliminate Boost Maintain Add • functions not associated with protein assay and detection • expansion from reagents tools and Abcam inside into capital intensive equipment – China growth robust unlike competitors selling equipment • AI engine to select targets • recombinant antibody binder technology • other high margin immunoassay technologies such as SimpleStep ELISA • cellular editing technology to uniquely validate antibodies • global capacity and capability in manufacturing • website functionality and ordering • discovery partner with biopharmaceutical organizations • powerful data - driven innovation platform • product validation and quality • >750,000 customers worldwide • 24 - 48 hours to ship most products • >100,000 products and >300,000 SKUs • Talented global team of >1,500 employees • Disruptive e - commerce platform revolutionizing the purchase of antibodies • >60% customer engagement and transactional net promoter score (NPS)

25 Returning antibodies as the bridge into market adjacencies * www.abcamfocus.com Eliminate Boost Maintain Add • products that are not protein research related • distracting low margin cell lines and DNA research reagents • drift away from best in the world, passionate and high margin products • capabilities and content via acquisitions • new protein detection tools such as camelids and aptamers (essentially antibodies in different format) • business development capability to address ‘Abcam inside’ opportunities • to >75% by sales of in house manufactured products • innovation engine to increase scale and throughput • geographic and market expansion into • capacity and capability to deliver • leadership in RUO antibodies • Abcam’s global antibody citation share • innovation engine to increase scale and throughput • KPI from target identification to product release • Focus on core research markets • $8bn research market and $5bn Clinical Development market • High - quality products, ensuring conclusive, consistent and repeatable experiments

26 Appendix

27 Source: Refinitiv Eikon, for the two year period prior to 16 May 2023. • Biotechne is has often been regarded as Abcam’s closest peer • Yet both financial advisers’ fairness opinions excluded it from comparable company analysis due to “persistent historical trading patterns” • The last two years’ share price performances for Abcam and Biotechne show a 0 . 87 correlation – not unreasonable for a peer … Biotechne has been wrongly excluded from the fairness opinions 10 12 14 16 18 20 22 24 26 28 30 May-21 Aug-21 Nov-21 Feb-22 May-22 Aug-22 Nov-22 Feb-23 Share price (rebased to Abcam) Abcam Plc Bio-Techne

28 Source: Peel Hunt analysis to back - calculate the implied EV/NTM EBITDA multiples used in this analysis which is based upon the p resent value of the December 2025 share price as determined by the product of a range of EV / NTM EBITDA multiples and the Ab cam FY2026 EBITDA forecast (Discount rate = 10%). • One of Abcam’s financial advisers calculates an illustrative future share price range of Abcam as of Dec 25 discounted to today using a range of EV/NTM EBITDA multiples • Implied trading range today : $ 22 . 10 – $ 28 . 30 • Implied multiples : 18 x – 23 x • A range of EV/NTM EBITDA multiples that are around the long - term average EV/NTM EBITDA multiple for Abcam (see earlier) excluding the impact of the pandemic • The financial adviser elected to exclude this metric from valuation included in their fairness opinion • This is a valid approach to valuation in circumstances such as this • And it elegantly shows the future share price performance of Abcam (in today’s numbers) once the full benefit of the 5 - year plan has started to be reaped • There is again no premium for control factored into this analysis Future share price analysis has been wrongly excluded

29 Abcam is an outstanding investment opportunity Source: Abcam and Peel Hunt analysis • Well - positioned for long - term profitable growth, underpinned by: • Large addressable markets: c.$8bn • Favourable industry and macro forces to sustain long - term growth • Resulting in increasing long - term demand for our unique products • Repeatable and predictable sales highly correlated with ‘work at the lab bench’ • “Abcam is a differentiated company with terrific brand and long - term sustainable business model” - Rainer M. Blair, President and Chief Executive Officer, Danaher • Strong and defensible ‘just in time’ high margin unique reagents used in ALL life science research labs worldwide. No supply chain backlog or capital equipment budget exposure • Robust growth in China (c.5% in first half 2023) vs Danaher, Thermo and Biotechne hit by capital budgets reduction in China and down Executing on Strategic Priorities to Drive Long Term Value” presentation published by Abcam on 20 June 2023

30 Defeating a takeover offer is not impossible TSR data sourced from Refinitiv Eikon • There are numerous examples of poorly timed takeovers being defeated and companies going on to deliver additional returns to investors • Nearly 10 years ago, AstraZeneca faced an unwanted bid from Pfizer • Believers made a strong case for the future and received the support of long - term shareholders • Rewarded with 257% TSR over and above the final £55 bid over the period • Illumina is worth 3.8x Roche’s unwelcome bid in January 2012 • Shareholders made the case that the bid failed to properly value Illumina’s pipeline of products • Investors rewarded with 192% TSR since

31 Disclaimer This document has been prepared by and on behalf of Dr. Jonathan Milner ( Dr. Milner). Dr. Milner is providing this document for informational and discussion purposes only. Dr. Milner has published a Proxy Statement and accompanying White Proxy Card to be used to solicit votes against the proposed acquisition of Ab cam plc (the "Company") by Diadem Holdco Limited, a wholly owned indirect subsidiary of Danaher Corporation, at $24 per share at a meeting of the shareholders convened pursuant to the Companies Act 2006 (the “Court Meeting”). Dr. Milner strongly advises all shareholders of the Company to read the Proxy Statement and other proxy materials as they become availab le because they will contain important information. Such proxy materials will be made available at no charge online on the website of the U.S. Securities and Exchange Commission at www.sec .go v and on a website hosted by Dr. Milner to provide information to shareholders about the Court Meeting at www.abcamfocus.com. Holders of Company securities also should receive cop ies of the Proxy Statement and Proxy Card by mail, and copies will be provided at no charge upon request made to Dr. Milner’s proxy solicitor, Alliance Advisors, by email to focusabcam@allianceadvisors.com or by phone to 877 - 777 - 8211 from North America or to 0800 - 102 - 6998 from elsewhere. The views expressed herein reflect the opinions of Dr. Milner as of the date hereof. Dr. Milner reserves the right to change or modify any opinions expressed herein at any time and for any reason and expressly disclaims any obligation to correct, update, or revise th e information contained herein or to otherwise provide any additional materials. All the information contained herein is based on Dr. Milner’s independent research and analysis and publicly available information, which may include, but is not limited to, publicly available disclosures, earnings calls and other Company - hosted events open to the public, news articles and other m edia reports, sell - side analyst reports, independent research projects conducted by third parties, and publicly - available databases. The materials in this document have not been prepared or endorsed by the Company and may not be attributed to the Company in any way. The information expressed herein is unaudited, reflects the judgment of Dr. Milner only through the date of this document, and is subject to change at any time. Facts have been obtained from sources considered reliable but are not guaranteed. Dr. Milner recognizes that there may be confidential or otherwise non - public information with respect to the Company that could alter his opinions were such information known. This document does not purport to contain all the informat ion that may be relevant to an evaluation of the Company, Company securities, or the matters described herein. Dr. Milner disclaims any obligation to correct, update or revise these documents or to otherwise provide any additional materials t o any recipient of these documents. Dr Milner has a beneficial ownership interest, and/or an economic interest, in the securities d isc ussed herein, which is disclosed in the Proxy Statement and other proxy materials. Nothing in this document should be taken as any indication of Dr. Milner’s current or future trading or voting intentions which may change from time - to - time. Dr. Milner intends to review his investments in the Company on a continuing basis and depending on various factors, including wit hou t limitation, the Company’s financial position, strategic direction, the outcome of any discussions with the Company, overall market conditions, and the pricing of securities, transac t i n the securities of the Company and reserves the right to take any actions with respect to his investments in the Company as he may deem appropriate. Dr. Milner expressly disclaims any obligation to notify others of any such changes. Except for the historical information contained herein, the information and opinions contained in this document constitute forward - looking stat ements, including estimates, projections and other forward - looking statements, some of which can be identified by the use of forward-looking terminology such as “may,” “will,” “should, ” “ anticipate,” “expect,” “project,” “intend,” “believe,” or variations thereon or comparable terminology. Forward - looking statements are inherently unreliable as they are based on estimate s and assumptions about exit and valuation multiples, and events and conditions that have not yet occurred, all of which may prove to be incorrect. Forward - looking statements are subject to uncertainties and changes (including changes in market valuation multiples, earnings assumptions, economic, operational, political or other circumstances or management), all of whi ch are beyond Dr. Milner’s control and that may cause the relevant actual results to be materially different from the results expressed or implied by the forward - looking statements. No a ssurance, representation or warranty is made by any person that any of the forward - looking statements will be achieved, that the Company will be able to avoid losses or that any company w ill be able to implement its intended activities. Neither Dr. Milner nor any of his affiliates, advisers and agents makes any assurance, representation or warranty as to the accuracy or r eas onableness of the forward - looking statements nor have any of them independently verified the forward - looking statements. This document should not be construed as, directly or indirectly, se eking any confidential information. Dr. Milner disclaims any obligation to treat the receipt of such information as confidential, unless done so expressly in writing. No agreement, commi tme nt, understanding, or other legal relationship exists or may be deemed to exist between or among Dr. Milner and any other person by virtue of furnishing this document. Dr. Milner is not acting for or on behalf of, and is not providing any advice or service to, any recipient of this document. Before determining any course of action, any recipient should consider any associated ris ks and consult with its own independent advisors as it deems necessary. This communication does not constitute an offer to buy or solicitation of an offer to sell any securities or a rec omm endation to buy or sell any securities.

Exhibit

99.23

Jonathan

Milner releases presentation to Abcam plc shareholders, outlining reasons to reject Danaher's bid and strategic vision for the Company

CAMBRIDGE,

England, 16 October 2023 – Dr. Jonathan Milner, the founder and one of the largest shareholders in Abcam plc (“Abcam”

or the “Company”) (NYSE: ABCM) with ownership of 6.16%, today issued a presentation covering the reasons for Abcam shareholders

to vote against the $24 per share bid from Danaher Corporation (NYSE: DHR) or its affiliates (“Danaher”).

These

include:

| · | The

positioning of Abcam to reap the returns of the five-year investment plan, rendering the

$24 offer price as the wrong price at the wrong time |

| · | Data

showing that the forward multiple implied by the $24 bid price is below Abcam’s long-term

trading multiple |

| · | The

anticipation of a transformational year ahead with increased EBITDA margins and revenue growth

for FY24, not reflected in Danaher's offer |

| · | Details

of the selective approach in the fairness opinions included in the Scheme Circular, resulting

in the omission of key peer group companies from the analysis which depressed the multiples

and the implied value per share |

Dr.

Milner firmly believes that Abcam stands as an exceptional UK asset and should not be undersold to Danaher. However, he is open to selling

to Danaher or another suitor at a fair price that genuinely reflects the Company’s true value and potential.

In

the presentation, Dr. Milner unveiled “Abcam 3.0,” his strategy for Abcam. Should the "Vote AGAINST" campaign conclude

successfully, he intends to convene an Extraordinary General Meeting (EGM) aimed at overhauling the Company's Board. His strategy focuses

on four strategic pillars essential for the Company's three-year growth plan commencing in 2024:

| · | Returning

Abcam to best-in-class Corporate Governance and Investor Relations |

| · | Restoring

operational efficiency and achieving execution excellence |

| · | Strengthening

leadership in Antibody and Digital Platforms |

| · | Reestablishing

antibodies as the conduit into market adjacencies |

The

full presentation can be found at this link and has been made available on www.abcamfocus.com

Jonathan

Milner

https://abcamfocus.com/

Investor

contact

Alliance

Advisors (Europe)

T: +44 7733

265 198 / E: focusabcam@allianceadvisors.com

Michael Roper

Alliance

Advisors (US)

T: +1 917

414 4766

Thomas Ball

Peel Hunt

LLP

T: +44 (0)

20 7418 8900

Christopher

Golden / James Steel

Sohail Akbar

/ Jock Maxwell Macdonald

International

PR advisers

ICR Consilium

(Europe)

T: +44 (0)20

3709 5700 / E: focusabcam@consilium-comms.com

Mary-Jane

Elliott / Matthew Neal / Davide Salvi

ICR (US)

T: +1 646

677 1811 / E: FocusAbcam@icrinc.com

Dan McDermott

IMPORTANT

ADDITIONAL INFORMATION

THIS

DOCUMENT HAS BEEN ISSUED BY DR. JONATHAN MILNER ("DR. MILNER").

DR.

MILNER HAS PUBLISHED A PROXY STATEMENT AND ACCOMPANYING WHITE PROXY CARD TO BE USED TO SOLICIT VOTES AGAINST THE PROPOSED ACQUISITION

OF ABCAM PLC (THE "COMPANY") BY DIADEM HOLDCO LIMITED, A WHOLLY OWNED INDIRECT SUBSIDIARY OF DANAHER CORPORATION, AT $24 PER

SHARE, AT A MEETING OF THE SHAREHOLDERS CONVENED PURSUANT TO THE COMPANIES ACT 2006 (THE “COURT MEETING”).

DR.

MILNER STRONGLY ADVISES ALL SHAREHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE

BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE MADE AVAILABLE AT NO CHARGE ONLINE ON THE WEBSITE OF THE

U.S. SECURITIES AND EXCHANGE COMMISSION AT WWW.SEC.GOV AND ON A WEBSITE HOSTED BY DR. MILNER TO PROVIDE INFORMATION TO SHAREHOLDERS

ABOUT THE COURT MEETING AT WWW.ABCAMFOCUS.COM. HOLDERS OF COMPANY SECURITIES ALSO SHOULD RECEIVE COPIES OF THE PROXY STATEMENT

AND PROXY CARD BY MAIL, AND COPIES WILL BE PROVIDED AT NO CHARGE UPON REQUEST MADE TO DR. MILNER’S PROXY SOLICITOR, ALLIANCE ADVISORS,

BY EMAIL TO FOCUSABCAM@ALLIANCEADVISORS.COM OR BY PHONE TO 877-777-8211 FROM NORTH AMERICA OR TO 0800-102- 6998 FROM ELSEWHERE.

THIS

DOCUMENT IS FOR DISCUSSION AND INFORMATIONAL PURPOSES ONLY. THE VIEWS EXPRESSED HEREIN REPRESENT THE OPINIONS OF DR. MILNER AS OF THE

DATE HEREOF. DR. MILNER RESERVES THE RIGHT TO CHANGE ANY OF HIS OPINIONS EXPRESSED HEREIN AT ANY TIME AND FOR ANY REASON AND EXPRESSLY

DISCLAIMS ANY OBLIGATION TO CORRECT, UPDATE OR REVISE THE INFORMATION CONTAINED HEREIN OR TO OTHERWISE PROVIDE ANY ADDITIONAL MATERIALS.

SUBJECT TO THE FOREGOING, AND AS SET FORTH BELOW, DR. MILNER INTENDS TO MAKE AVAILABLE AT AN APPROPRIATE TIME ADDITIONAL INFORMATION

ABOUT THE COURT MEETING INCLUDING HOW TO VOTE AT SUCH MEETING.

DR.

MILNER HAS INVESTMENTS IN THE COMPANY WHICH ARE DISCLOSED IN THE PROXY STATEMENT AND OTHER PROXY MATERIALS, AND CONSEQUENTLY HAS A FINANCIAL

INTEREST IN THE PROFITABILITY OF HIS POSITIONS IN THE COMPANY. ACCORDINGLY THIS DOCUMENT SHOULD NOT BE REGARDED AS IMPARTIAL. NOTHING

IN THIS DOCUMENT SHOULD BE TAKEN AS ANY INDICATION OF DR. MILNER 'S CURRENT OR FUTURE TRADING OR VOTING INTENTIONS AND/OR ACTIVITIES

WHICH MAY CHANGE AT ANY TIME.

CERTAIN

INFORMATION IN THIS DOCUMENT IS BASED ON PUBLICLY AVAILABLE INFORMATION WITH RESPECT TO THE COMPANY, INCLUDING PUBLIC FILINGS AND DISCLOSURES

MADE BY THE COMPANY AND OTHER SOURCES, AS WELL AS DR. MILNER'S ANALYSIS OF SUCH PUBLICLY AVAILABLE INFORMATION. DR. MILNER HAS RELIED

UPON AND ASSUMED, WITHOUT INDEPENDENT VERIFICATION, THE ACCURACY AND COMPLETENESS OF SUCH INFORMATION, AND NO REPRESENTATION OR WARRANTY

IS MADE THAT ANY SUCH DATA OR INFORMATION IS COMPLETE OR ACCURATE. DR. MILNER RECOGNISES THAT THERE MAY BE CONFIDENTIAL OR OTHERWISE

NON-PUBLIC INFORMATION WITH RESPECT TO THE COMPANY THAT COULD ALTER THE OPINIONS OF DR. MILNER WERE SUCH INFORMATION KNOWN.

NO

REPRESENTATION, WARRANTY OR UNDERTAKING, EXPRESS OR IMPLIED, IS GIVEN AND NO RESPONSIBILITY OR LIABILITY OR DUTY OF CARE IS OR WILL BE

ACCEPTED BY DR. MILNER CONCERNING: (I) THIS DOCUMENT AND ITS CONTENTS, INCLUDING WHETHER THE INFORMATION AND OPINIONS CONTAINED HEREIN

ARE ACCURATE, FAIR, COMPLETE OR CURRENT; (II) THE PROVISION OF ANY FURTHER INFORMATION, WHETHER BY WAY OF UPDATE TO THE INFORMATION AND

OPINIONS CONTAINED IN THIS DOCUMENT OR OTHERWISE TO THE RECIPIENT AFTER THE DATE OF THIS DOCUMENT; OR (III) THAT DR. MILNER'S INVESTMENT

PROCESSES OR INVESTMENT OBJECTIVES WILL OR ARE LIKELY TO BE ACHIEVED OR SUCCESSFUL OR THAT DR. MILNER'S INVESTMENTS WILL MAKE ANY PROFIT

OR WILL NOT SUSTAIN LOSSES. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. TO THE FULLEST EXTENT PERMITTED BY LAW, DR. MILNER

WILL NOT BE RESPONSIBLE FOR ANY LOSSES, WHETHER DIRECT, INDIRECT OR CONSEQUENTIAL, INCLUDING LOSS OF PROFITS, DAMAGES, COSTS, CLAIMS

OR EXPENSES RELATING TO OR ARISING FROM THE RECIPIENT'S OR ANY PERSON'S RELIANCE ON THIS DOCUMENT.

EXCEPT

FOR THE HISTORICAL INFORMATION CONTAINED HEREIN, THE INFORMATION AND OPINIONS INCLUDED IN THIS DOCUMENT CONSTITUTE FORWARD-LOOKING STATEMENTS,

INCLUDING ESTIMATES AND PROJECTIONS PREPARED WITH RESPECT TO, AMONG OTHER THINGS, THE COMPANY'S ANTICIPATED OPERATING PERFORMANCE, THE

VALUE OF THE COMPANY'S SECURITIES, DEBT OR ANY RELATED FINANCIAL INSTRUMENTS THAT ARE BASED UPON OR RELATE TO THE VALUE OF SECURITIES

OF THE COMPANY (COLLECTIVELY, "COMPANY SECURITIES"), GENERAL ECONOMIC AND MARKET CONDITIONS AND OTHER FUTURE EVENTS. YOU SHOULD

BE AWARE THAT ALL FORWARD-LOOKING STATEMENTS, ESTIMATES AND PROJECTIONS ARE INHERENTLY UNCERTAIN AND SUBJECT TO SIGNIFICANT ECONOMIC,

COMPETITIVE, AND OTHER UNCERTAINTIES AND CONTINGENCIES AND HAVE BEEN INCLUDED SOLELY FOR ILLUSTRATIVE PURPOSES. ACTUAL RESULTS MAY DIFFER

MATERIALLY FROM THE INFORMATION CONTAINED HEREIN DUE TO REASONS THAT MAY OR MAY NOT BE FORESEEABLE. THERE CAN BE NO ASSURANCE THAT THE

COMPANY SECURITIES WILL TRADE AT THE PRICES THAT MAY BE IMPLIED HEREIN, AND THERE CAN BE NO ASSURANCE THAT ANY ESTIMATE, PROJECTION OR

ASSUMPTION HEREIN IS, OR WILL BE PROVEN, CORRECT.

THIS

DOCUMENT DOES NOT CONSTITUTE (A) AN OFFER OR INVITATION TO BUY OR SELL, OR A SOLICITATION OF AN OFFER TO BUY OR SELL, ANY SECURITY OR

OTHER FINANCIAL INSTRUMENT AND NO LEGAL RELATIONS SHALL BE CREATED BY ITS ISSUE, (B) A "FINANCIAL PROMOTION" FOR THE PURPOSES

OF THE FINANCIAL SERVICES AND MARKETS ACT 2000, (C) "INVESTMENT ADVICE" AS DEFINED BY THE FCA HANDBOOK, (D) "INVESTMENT

RESEARCH" AS DEFINED BY THE FCA HANDBOOK, OR (E) AN "INVESTMENT RECOMMENDATION" AS DEFINED BY REGULATION (EU) 596/2014

AND BY REGULATION (EU) NO. 596/2014 AS IT FORMS PART OF U.K. DOMESTIC LAW BY VIRTUE OF SECTION 3 OF THE EUROPEAN UNION (WITHDRAWAL) ACT

2018 ("EUWA 2018") INCLUDING AS AMENDED BY REGULATIONS ISSUED UNDER SECTION 8 OF EUWA 2018. THIS DOCUMENT IS NOT (AND MAY NOT

BE CONSTRUED TO BE) LEGAL, TAX, INVESTMENT, FINANCIAL OR OTHER ADVICE. EACH RECIPIENT SHOULD CONSULT THEIR OWN LEGAL COUNSEL AND TAX

AND FINANCIAL ADVISERS AS TO LEGAL AND OTHER MATTERS CONCERNING THE INFORMATION CONTAINED HEREIN. THIS DOCUMENT DOES NOT PURPORT TO BE

ALL-INCLUSIVE OR TO CONTAIN ALL OF THE INFORMATION THAT MAY BE RELEVANT TO AN EVALUATION OF THE COMPANY, COMPANY SECURITIES OR THE MATTERS

DESCRIBED HEREIN.

NO

AGREEMENT, COMMITMENT, UNDERSTANDING OR OTHER LEGAL RELATIONSHIP EXISTS OR MAY BE DEEMED TO EXIST BETWEEN OR AMONG DR. MILNER AND ANY

OTHER PERSON BY VIRTUE OF FURNISHING THIS DOCUMENT. DR. MILNER IS NOT ACTING FOR OR ON BEHALF OF, AND IS NOT PROVIDING ANY ADVICE OR

SERVICE TO, ANY RECIPIENT OF THIS DOCUMENT. DR. MILNER IS NOT RESPONSIBLE TO ANY PERSON FOR PROVIDING ADVICE IN RELATION TO THE SUBJECT

MATTER OF THIS DOCUMENT. BEFORE DETERMINING ON ANY COURSE OF ACTION, ANY RECIPIENT SHOULD CONSIDER ANY ASSOCIATED RISKS AND CONSEQUENCES

AND CONSULT WITH ITS OWN INDEPENDENT ADVISORS AS IT DEEMS NECESSARY.

DR.

MILNER HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION CONTAINED HEREIN. ANY SUCH STATEMENTS

OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. ALL TRADEMARKS AND

TRADE NAMES USED HEREIN ARE THE EXCLUSIVE PROPERTY OF THEIR RESPECTIVE OWNERS.

Exhibit 99.24

Jonathan Milner Issues Statement Responding

to ISS Report

Urges

shareholders to disregard the ISS report and continue to Vote AGAINST the current proposed acquisition of Abcam by

Danaher

CAMBRIDGE,

England, 16 October 2023 – Jonathan Milner, the founder and one of the largest shareholders in Abcam plc (“Abcam”

or the “Company”) (NYSE: ABCM) with ownership of 6.16% of the Company, has today issued the following statement in response

to a 16 October 2023 report from Institutional Shareholder Service (“ISS”). Jonathan Milner urges shareholders to continue

to vote AGAINST the current proposed acquisition of Abcam by Danaher Corporation (NYSE: DHR) or its affiliates (“Danaher”).

Commenting on the report, Jonathan Milner issued

the following statement:

“I unequivocally oppose the conclusions

drawn in the ISS report and its subsequent recommendation. I believe that Danaher’s $24 per share offer is a stark undervaluation

of Abcam’s true worth. Accepting $24 per share, devoid of a strategic premium, is the wrong price at the wrong time, a move that

blatantly overlooks Abcam's intrinsic value.

As I’ve said before, Abcam is poised

to reap the returns of its five-year plan and significant investments made. Furthermore, it is critical to note the forward multiple implied

by Danaher’s bid price undercuts Abcam’s long-term trading multiple.

I am also troubled by the details of the selective

approach evident in the fairness opinions provided in the Scheme Circular. This methodology resulted in the omission of key peer group

companies from the analysis, a choice that has artificially depressed the multiples and consequently, the implied value per share.

It's important to highlight the real shareholder

value that my advocacy has unlocked. While the ISS report itself acknowledges the positive impact, let's not overlook the facts: the share

price soared from roughly $16 to over $20, a significant 25% rise, in the wake of my campaign being made public.

I believe that voting AGAINST the transaction

would be a far better outcome for shareholders, returning the Company to the position it previously held as a premium-rated life sciences

company with a long track record of impeccable execution and an absolute focus on shareholder value.”

Dr Milner today issued a presentation covering

the reasons for Abcam shareholders to vote against the $24 per share bid from Danaher which can be found at this link and has

been made available on www.abcamfocus.com

THE CHOICE IS CLEAR – VOTE AGAINST THIS

PROPOSED TRANSACTION AND SEND A CLEAR

MESSAGE TO THE BOARD THAT THEY ARE DISSATISFIED

WITH THE PROPOSED ACQUISITION.

For more information, please visit https://abcamfocus.com/

Jonathan Milner

https://abcamfocus.com/

Investor contact

Alliance Advisors (Europe)

T: +44 7733 265 198 / E: focusabcam@allianceadvisors.com

Michael Roper

Alliance Advisors (US)

T: +1 917 414 4766

Thomas Ball

Peel Hunt LLP

T: +44 (0) 20 7418 8900

Christopher Golden / James Steel

Sohail Akbar / Jock Maxwell Macdonald

International PR advisers

ICR Consilium (Europe)

T: +44 (0)20 3709 5700 / E: focusabcam@consilium-comms.com

Mary-Jane Elliott / Matthew Neal / Davide Salvi

ICR (US)

T: +1 646 677 1811 / E: FocusAbcam@icrinc.com

Dan McDermott

IMPORTANT ADDITIONAL INFORMATION

THIS DOCUMENT HAS BEEN ISSUED BY DR. JONATHAN

MILNER ("DR. MILNER").

DR. MILNER IS PUBLISHING A PROXY STATEMENT AND

ACCOMPANYING [WHITE] PROXY CARD TO BE USED TO SOLICIT VOTES AGAINST THE PROPOSED ACQUISITION OF ABCAM PLC (THE "COMPANY") BY

DANAHER CORPORATION OR ONE OF ITS AFFILIATES AT $24 PER SHARE AT A MEETING OF THE SHAREHOLDERS CONVENED PURSUANT TO THE COMPANIES ACT

2006 (THE “COURT MEETING”).

DR. MILNER STRONGLY ADVISES ALL SHAREHOLDERS

OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION.

SUCH PROXY MATERIALS WILL BE MADE AVAILABLE AT NO CHARGE ONLINE ON THE WEBSITE OF THE U.S. SECURITIES AND EXCHANGE COMMISSION AT WWW.SEC.GOV

AND ON A WEBSITE HOSTED BY DR. MILNER TO PROVIDE INFORMATION TO SHAREHOLDERS ABOUT THE COURT MEETING AT WWW.ABCAMFOCUS.COM.

HOLDERS OF COMPANY SECURITIES ALSO SHOULD RECEIVE COPIES OF THE PROXY STATEMENT AND PROXY CARD BY MAIL, AND COPIES WILL BE PROVIDED AT

NO CHARGE UPON REQUEST MADE TO DR. MILNER’S PROXY SOLICITOR, ALLIANCE ADVISORS, , BY EMAIL TO FOCUSABCAM@ALLIANCEADVISORS.COM

OR BY PHONE TO 877-777-8211 FROM NORTH AMERICA OR TO 0800-102- 6998 FROM ELSEWHERE.

THIS DOCUMENT IS FOR DISCUSSION AND INFORMATIONAL

PURPOSES ONLY. THE VIEWS EXPRESSED HEREIN REPRESENT THE OPINIONS OF DR. MILNER AS OF THE DATE HEREOF. DR. MILNER RESERVES THE RIGHT TO

CHANGE ANY OF HIS OPINIONS EXPRESSED HEREIN AT ANY TIME AND FOR ANY REASON AND EXPRESSLY DISCLAIMS ANY OBLIGATION TO CORRECT, UPDATE OR

REVISE THE INFORMATION CONTAINED HEREIN OR TO OTHERWISE PROVIDE ANY ADDITIONAL MATERIALS. SUBJECT TO THE FOREGOING, AND AS SET FORTH BELOW,

DR. MILNER INTENDS TO MAKE AVAILABLE AT AN APPROPRIATE TIME ADDITIONAL INFORMATION ABOUT THE COURT MEETING INCLUDING HOW TO VOTE AT SUCH

MEETING.

DR. MILNER HAS INVESTMENTS IN THE COMPANY WHICH

ARE DISCLOSED IN THE PROXY STATEMENT AND OTHER PROXY MATERIALS, AND CONSEQUENTLY HAS A FINANCIAL INTEREST IN THE PROFITABILITY OF HIS

POSITIONS IN THE COMPANY. ACCORDINGLY THIS DOCUMENT SHOULD NOT BE REGARDED AS IMPARTIAL. NOTHING IN THIS DOCUMENT SHOULD BE TAKEN AS ANY

INDICATION OF DR. MILNER 'S CURRENT OR FUTURE TRADING OR VOTING INTENTIONS AND/OR ACTIVITIES WHICH MAY CHANGE AT ANY TIME.

CERTAIN INFORMATION IN THIS DOCUMENT IS BASED

ON PUBLICLY AVAILABLE INFORMATION WITH RESPECT TO THE COMPANY, INCLUDING PUBLIC FILINGS AND DISCLOSURES MADE BY THE COMPANY AND OTHER

SOURCES, AS WELL AS DR. MILNER'S ANALYSIS OF SUCH PUBLICLY AVAILABLE INFORMATION. DR. MILNER HAS RELIED UPON AND ASSUMED, WITHOUT INDEPENDENT

VERIFICATION, THE ACCURACY AND COMPLETENESS OF SUCH INFORMATION, AND NO REPRESENTATION OR WARRANTY IS MADE THAT ANY SUCH DATA OR INFORMATION

IS COMPLETE OR ACCURATE. DR. MILNER RECOGNISES THAT THERE MAY BE CONFIDENTIAL OR OTHERWISE NON-PUBLIC INFORMATION WITH RESPECT TO

THE COMPANY THAT COULD ALTER THE OPINIONS OF DR. MILNER WERE SUCH INFORMATION KNOWN.

NO REPRESENTATION, WARRANTY OR UNDERTAKING, EXPRESS

OR IMPLIED, IS GIVEN AND NO RESPONSIBILITY OR LIABILITY OR DUTY OF CARE IS OR WILL BE ACCEPTED BY DR. MILNER CONCERNING: (I) THIS

DOCUMENT AND ITS CONTENTS, INCLUDING WHETHER THE INFORMATION AND OPINIONS CONTAINED HEREIN ARE ACCURATE, FAIR, COMPLETE OR CURRENT;

(II) THE PROVISION OF ANY FURTHER INFORMATION, WHETHER BY WAY OF UPDATE TO THE INFORMATION AND OPINIONS CONTAINED IN THIS DOCUMENT

OR OTHERWISE TO THE RECIPIENT AFTER THE DATE OF THIS DOCUMENT; OR (III) THAT DR. MILNER'S INVESTMENT PROCESSES OR INVESTMENT OBJECTIVES

WILL OR ARE LIKELY TO BE ACHIEVED OR SUCCESSFUL OR THAT DR. MILNER'S INVESTMENTS WILL MAKE ANY PROFIT OR WILL NOT SUSTAIN LOSSES. PAST

PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. TO THE FULLEST EXTENT PERMITTED BY LAW, DR. MILNER WILL NOT BE RESPONSIBLE FOR ANY LOSSES,

WHETHER DIRECT, INDIRECT OR CONSEQUENTIAL, INCLUDING LOSS OF PROFITS, DAMAGES, COSTS, CLAIMS OR EXPENSES RELATING TO OR ARISING

FROM THE RECIPIENT'S OR ANY PERSON'S RELIANCE ON THIS DOCUMENT.

EXCEPT FOR THE HISTORICAL INFORMATION CONTAINED

HEREIN, THE INFORMATION AND OPINIONS INCLUDED IN THIS DOCUMENT CONSTITUTE FORWARD-LOOKING STATEMENTS, INCLUDING ESTIMATES AND PROJECTIONS

PREPARED WITH RESPECT TO, AMONG OTHER THINGS, THE COMPANY'S ANTICIPATED OPERATING PERFORMANCE, THE VALUE OF THE COMPANY'S SECURITIES,

DEBT OR ANY RELATED FINANCIAL INSTRUMENTS THAT ARE BASED UPON OR RELATE TO THE VALUE OF SECURITIES OF THE COMPANY (COLLECTIVELY, "COMPANY

SECURITIES"), GENERAL ECONOMIC AND MARKET CONDITIONS AND OTHER FUTURE EVENTS. YOU SHOULD BE AWARE THAT ALL FORWARD-LOOKING STATEMENTS,

ESTIMATES AND PROJECTIONS ARE INHERENTLY UNCERTAIN AND SUBJECT TO SIGNIFICANT ECONOMIC, COMPETITIVE, AND OTHER UNCERTAINTIES AND CONTINGENCIES

AND HAVE BEEN INCLUDED SOLELY FOR ILLUSTRATIVE PURPOSES. ACTUAL RESULTS MAY DIFFER MATERIALLY FROM THE INFORMATION CONTAINED HEREIN

DUE TO REASONS THAT MAY OR MAY NOT BE FORESEEABLE. THERE CAN BE NO ASSURANCE THAT THE COMPANY SECURITIES WILL TRADE AT THE PRICES

THAT MAY BE IMPLIED HEREIN, AND THERE CAN BE NO ASSURANCE THAT ANY ESTIMATE, PROJECTION OR ASSUMPTION HEREIN IS, OR WILL BE PROVEN,

CORRECT.

THIS DOCUMENT DOES NOT CONSTITUTE (A) AN

OFFER OR INVITATION TO BUY OR SELL, OR A SOLICITATION OF AN OFFER TO BUY OR SELL, ANY SECURITY OR OTHER FINANCIAL INSTRUMENT AND NO LEGAL

RELATIONS SHALL BE CREATED BY ITS ISSUE, (B) A "FINANCIAL PROMOTION" FOR THE PURPOSES OF THE FINANCIAL SERVICES AND MARKETS

ACT 2000, (C) "INVESTMENT ADVICE" AS DEFINED BY THE FCA HANDBOOK, (D) "INVESTMENT RESEARCH" AS DEFINED BY

THE FCA HANDBOOK, OR (E) AN "INVESTMENT RECOMMENDATION" AS DEFINED BY REGULATION (EU) 596/2014 AND BY REGULATION (EU) NO.

596/2014 AS IT FORMS PART OF U.K. DOMESTIC LAW BY VIRTUE OF SECTION 3 OF THE EUROPEAN UNION (WITHDRAWAL) ACT 2018 ("EUWA

2018") INCLUDING AS AMENDED BY REGULATIONS ISSUED UNDER SECTION 8 OF EUWA 2018. THIS DOCUMENT IS NOT (AND MAY NOT BE CONSTRUED

TO BE) LEGAL, TAX, INVESTMENT, FINANCIAL OR OTHER ADVICE. EACH RECIPIENT SHOULD CONSULT THEIR OWN LEGAL COUNSEL AND TAX AND FINANCIAL

ADVISERS AS TO LEGAL AND OTHER MATTERS CONCERNING THE INFORMATION CONTAINED HEREIN. THIS DOCUMENT DOES NOT PURPORT TO BE ALL-INCLUSIVE

OR TO CONTAIN ALL OF THE INFORMATION THAT MAY BE RELEVANT TO AN EVALUATION OF THE COMPANY, COMPANY SECURITIES OR THE MATTERS DESCRIBED

HEREIN.

NO AGREEMENT, COMMITMENT, UNDERSTANDING OR OTHER

LEGAL RELATIONSHIP EXISTS OR MAY BE DEEMED TO EXIST BETWEEN OR AMONG DR. MILNER AND ANY OTHER PERSON BY VIRTUE OF FURNISHING THIS

DOCUMENT. DR. MILNER IS NOT ACTING FOR OR ON BEHALF OF, AND IS NOT PROVIDING ANY ADVICE OR SERVICE TO, ANY RECIPIENT OF THIS DOCUMENT.

DR. MILNER IS NOT RESPONSIBLE TO ANY PERSON FOR PROVIDING ADVICE IN RELATION TO THE SUBJECT MATTER OF THIS DOCUMENT. BEFORE DETERMINING

ON ANY COURSE OF ACTION, ANY RECIPIENT SHOULD CONSIDER ANY ASSOCIATED RISKS AND CONSEQUENCES AND CONSULT WITH ITS OWN INDEPENDENT ADVISORS

AS IT DEEMS NECESSARY.

DR. MILNER HAS NOT SOUGHT OR OBTAINED CONSENT

FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION CONTAINED HEREIN. ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS

INDICATING THE SUPPORT OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. ALL TRADEMARKS AND TRADE NAMES USED HEREIN ARE THE EXCLUSIVE

PROPERTY OF THEIR RESPECTIVE OWNERS.

Abcam (CE) (USOTC:ABCZF)

Historical Stock Chart

From Dec 2024 to Jan 2025

Charts.")

Abcam (CE) (USOTC:ABCZF)

Historical Stock Chart

From Jan 2024 to Jan 2025

Charts.")